Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Canada healthcare infrastructure market is valued at approximately USD ~ billion, driven by increasing investments in healthcare facilities, modernization of existing infrastructure, and expansion in the adoption of advanced medical technologies. Government support and funding initiatives, coupled with a rising aging population, contribute to the market’s strong growth trajectory. Additionally, the healthcare infrastructure sector is being propelled by the growing demand for innovative solutions to improve healthcare delivery, efficiency, and patient care.

Major cities such as Toronto, Vancouver, and Montreal are key contributors to the healthcare infrastructure sector, thanks to their large healthcare networks and government investments. Ontario, British Columbia, and Quebec lead the way with substantial healthcare budgets, policy support, and robust medical facilities. These regions continue to dominate due to their concentration of healthcare providers, medical research institutions, and innovation hubs that drive technological advancements in healthcare services.

Market Segmentation

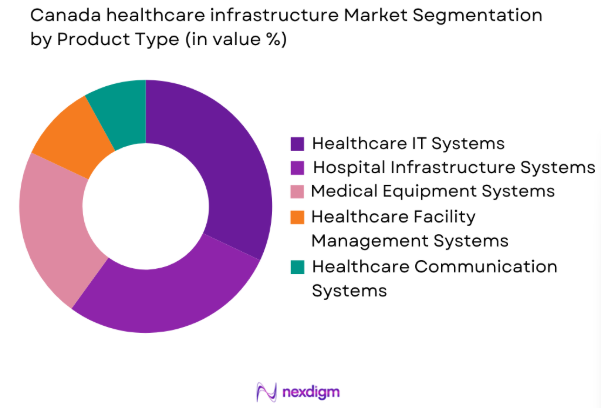

By Product Type

The Canadian healthcare infrastructure market is segmented by product type into healthcare IT systems, hospital infrastructure systems, medical equipment systems, healthcare facility management systems, and healthcare communication systems. Recently, healthcare IT systems have seen a dominant market share due to factors such as increasing demand for digital health solutions, government policies supporting e-health initiatives, and the need for better patient data management. The trend towards digitizing healthcare records and enhancing connectivity between systems has made IT infrastructure an essential part of healthcare facilities.

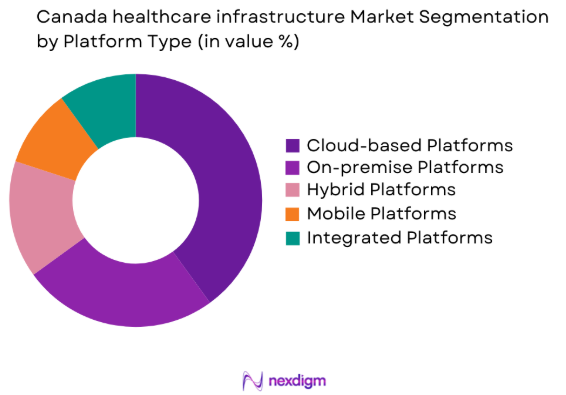

By Platform Type

The Canadian healthcare infrastructure market is also segmented by platform type into cloud-based platforms, on-premise platforms, hybrid platforms, mobile platforms, and integrated platforms. Cloud-based platforms have become the dominant sub-segment in recent years due to their scalability, cost-effectiveness, and ability to facilitate seamless integration across various healthcare systems. Healthcare providers are increasingly moving towards cloud infrastructure to handle large volumes of patient data, improve service delivery, and ensure data security in compliance with regulatory standards.

Competitive Landscape

The Canadian healthcare infrastructure market is highly competitive, with leading players focusing on mergers, acquisitions, and collaborations to expand their product portfolios and enhance service offerings. These players are also prioritizing innovation, technological advancements, and government collaborations to maintain a strong foothold in the market. The competitive landscape reflects a growing trend towards consolidations and the shift towards digital transformation in healthcare.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD) | Additional Parameter |

| GE Healthcare | 1892 | Chicago, USA | ~ | ~ | ~ | ~ | ~ |

| Siemens Healthineers | 1847 | Erlangen, Germany | ~ | ~ | ~ | ~ | ~ |

| Philips Healthcare | 1891 | Amsterdam, Netherlands | ~ | ~ | ~ | ~ | ~ |

| Cerner Corporation | 1979 | Kansas City, USA | ~ | ~ | ~ | ~ | ~ |

| Medtronic | 1949 | Minneapolis, USA | ~ | ~ | ~ | ~ | ~ |

Canada healthcare infrastructure Market Analysis

Growth Drivers

Increased Government Investment in Healthcare Infrastructure

The Canadian healthcare infrastructure market is experiencing significant growth driven by substantial government investments. Initiatives like the Canadian Health Infrastructure Investment Fund are playing a key role in modernizing hospitals and building new healthcare centers, especially in underserved areas. These investments aim to increase healthcare capacity and improve patient care standards to accommodate a growing population. Additionally, the government’s focus on digital health transformation, including funding for healthcare IT infrastructure, is expected to continue driving market expansion. By enhancing healthcare accessibility and leveraging advanced technologies, these initiatives are helping to improve overall healthcare delivery and efficiency across the country, supporting the market’s long-term growth trajectory.

Technological Advancements in Medical Devices

Technological advancements in medical devices are driving the market by enabling better healthcare outcomes and more efficient management of healthcare infrastructure. The integration of cutting-edge technologies like AI, machine learning, and the Internet of Things (IoT) into medical devices enhances diagnostic accuracy, treatment effectiveness, and patient monitoring. These innovations are particularly relevant in diagnostic imaging systems, remote patient monitoring devices, and telehealth platforms. Hospitals and healthcare providers in Canada are increasingly adopting these technologies to streamline operations, reduce costs, and provide high-quality care to patients. As medical technology continues to evolve, it will play a crucial role in shaping the future of healthcare infrastructure.

Market Challenges

High Capital Expenditure in Healthcare Infrastructure

A significant challenge faced by the Canadian healthcare infrastructure market is the high capital expenditure required for the development of advanced healthcare facilities. The construction of new hospitals and the upgrading of existing infrastructure demand substantial investments in medical equipment, building construction, and IT systems. For many healthcare providers, especially smaller private healthcare facilities, this represents a major financial burden. Additionally, the procurement of state-of-the-art medical devices and the integration of new technologies into existing infrastructure can be prohibitively expensive, leading to a slower adoption rate in certain regions. This high cost factor remains a significant challenge for the sustainable growth of the healthcare infrastructure market.

Regulatory and Compliance Barriers

The Canadian healthcare infrastructure market faces challenges due to the complex regulatory environment. Strict compliance requirements for healthcare standards, data protection, and medical device certifications often delay project implementation and escalate costs. Continuous adherence to regulations such as the Personal Health Information Protection Act (PHIPA) and Health Canada’s medical device regulations can be burdensome for healthcare providers and infrastructure developers. These regulatory hurdles can significantly slow down the approval process, especially for projects involving advanced medical devices and healthcare IT systems. Thorough scrutiny required for compliance can hinder the timely deployment of new healthcare infrastructure, making it difficult to keep pace with demand and technological advancements in the sector.

Opportunities

Expansion in AI-driven Healthcare Solutions

The growing demand for AI-driven healthcare solutions presents significant opportunities for the Canadian healthcare infrastructure market. AI technologies are poised to transform healthcare delivery by enabling faster diagnoses, personalized treatment plans, and improved patient outcomes. The use of AI in medical imaging, diagnostic tools, and patient management systems is gaining traction across Canada, with healthcare providers focusing on AI’s potential to optimize operational efficiency and reduce costs. Additionally, AI-powered solutions help healthcare facilities provide real-time monitoring of patients, predict disease outbreaks, and enhance overall patient care quality. As AI technology evolves, the healthcare sector is expected to see further integration, improving the efficiency of healthcare infrastructure.

Partnerships Between Public and Private Sectors

Collaborations between public and private sector stakeholders present lucrative opportunities for the growth of the Canadian healthcare infrastructure market. Public-private partnerships (PPP) are becoming increasingly common in the healthcare sector, as they allow for the pooling of resources, expertise, and funding to address the country’s growing healthcare infrastructure needs. These partnerships enable the development of new healthcare facilities, the implementation of innovative technologies, and the modernization of existing infrastructure. The government’s role in financing infrastructure projects and the private sector’s expertise in technology solutions creates a synergistic environment for continued market expansion. Furthermore, PPPs provide an avenue to address regional healthcare disparities by improving access to medical services in underserved areas.

Future Outlook

The future outlook for the Canadian healthcare infrastructure market remains positive, with expected growth driven by continued government support and technological advancements. Increasing investments in healthcare facilities, alongside the integration of AI and digital health solutions, will foster modernization across the sector. Additionally, the rise in healthcare demand, driven by an aging population and the need for more efficient services, will support further infrastructure development. The next five years will see a continued focus on enhancing healthcare access, improving quality of care, and reducing costs through the adoption of innovative solutions.

Major Players

- Health Canada

- GE Healthcare

- Siemens Healthineers

- Philips Healthcare

- Cerner Corporation

- Medtronic

- InteleradMedical Systems

- Allscripts Healthcare Solutions

- IBM Watson Health

- Canon Medical Systems

- Oracle Health Sciences

- Stryker Corporation

- Varian Medical Systems

- Roche Diagnostics

- Johnson & Johnson

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Private healthcare providers

- Hospitals and healthcare facility managers

- Healthcare technology providers

- Medical equipment manufacturers

- Pharmaceutical companies

- Healthcare consultants

Research Methodology

Step 1: Identification of Key Variables

This step involves defining the key variables that will be analyzed in the study, including healthcare infrastructure investment, technology adoption, market drivers, and growth challenges.

Step 2: Market Analysis and Construction

The market is analyzed using both qualitative and quantitative data, constructing a comprehensive view of the Canadian healthcare infrastructure market by evaluating trends, demand factors, and technological advancements.

Step 3: Hypothesis Validation and Expert Consultation

Expert opinions are sought to validate assumptions and hypotheses about the healthcare infrastructure sector, ensuring that the analysis is based on reliable and expert-driven insights.

Step 4: Research Synthesis and Final Output

Data collected from multiple sources is synthesized into a final comprehensive report that presents a clear and actionable market analysis, forecasts, and recommendations.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Increased Government Investment in Healthcare Infrastructure

Technological Advancements in Medical Devices

Rising Demand for Telemedicine Solutions - Market Challenges

High Capital Expenditure in Healthcare Infrastructure

Regulatory and Compliance Barriers

Integration of New Technologies with Existing Systems - Market Opportunities

Expansion in AI-driven Healthcare Solutions

Partnerships between Public and Private Sectors

Growth in Digital Health and Telehealth Services - Trends

Adoption of AI in Healthcare Infrastructure

Rise in Smart Hospital Solutions

Increased Focus on Data Security and Privacy - Government Regulations

- SWOT Analysis of Key Competitors

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Healthcare IT Systems

Hospital Infrastructure Systems

Medical Equipment Systems

Healthcare Facility Management Systems

Healthcare Communication Systems - By Platform Type (In Value%)

Cloud-based Platforms

On-premise Platforms

Hybrid Platforms

Mobile Platforms

Integrated Platforms - By Fitment Type (In Value%)

On-premise Solutions

Cloud-based Solutions

Modular Solutions

Integrated Solutions

Hybrid Solutions - By End User Segment (In Value%)

Hospitals

Clinics

Government Healthcare Systems

Private Healthcare Providers

Ambulatory Care Centers - By Procurement Channel (In Value%)

Direct Procurement

Government Tenders

Private Sector Procurement

Online Bidding Platforms

Third-party Distributors

- Market Share Analysis

- Cross Comparison Parameters (System Type, Platform Type, Procurement Channel, End User Segment, Fitment Type, Technology Adoption, Regulatory Compliance, Service Integration, Market Access, Customer Support)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Health Canada

GE Healthcare

Siemens Healthineers

Philips Healthcare

Cerner Corporation

Medtronic

Intelerad Medical Systems

Allscripts Healthcare Solutions

IBM Watson Health

Canon Medical Systems

Oracle Health Sciences

Stryker Corporation

Varian Medical Systems

Roche Diagnostics

Johnson & Johnson

- Hospitals’ Growing Demand for Advanced Healthcare Solutions

- Government Policies Driving Public Healthcare Investments

- Private Healthcare Providers’ Adoption of Modern Infrastructure

- Growth of Ambulatory and Outpatient Care Centers

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now