Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Canada home finance market represents one of the largest components of the country’s financial system, supported by strong banking infrastructure and government-backed mortgage insurance programs. Based on a recent historical assessment by the Bank of Canada and Canada Mortgage and Housing Corporation, total outstanding residential mortgage credit exceeded USD ~ trillion, reflecting sustained housing demand and refinancing activity. The market is driven by urban population growth, immigration-led household formation, rising property valuations, and widespread access to insured and conventional mortgage products across major provinces.

Dominant activity is concentrated in metropolitan regions such as Toronto, Vancouver, Montreal, and Calgary, where housing demand remains structurally elevated due to employment density, infrastructure, and new housing development. Ontario and British Columbia lead in mortgage originations because of higher property values and diversified economic bases. Quebec maintains strong participation through cooperative banking networks, while Alberta reflects cyclical energy-linked housing demand. These regions benefit from digital lending adoption, broker networks, and strong presence of federally regulated financial institutions.

Market Segmentation

By Product Type

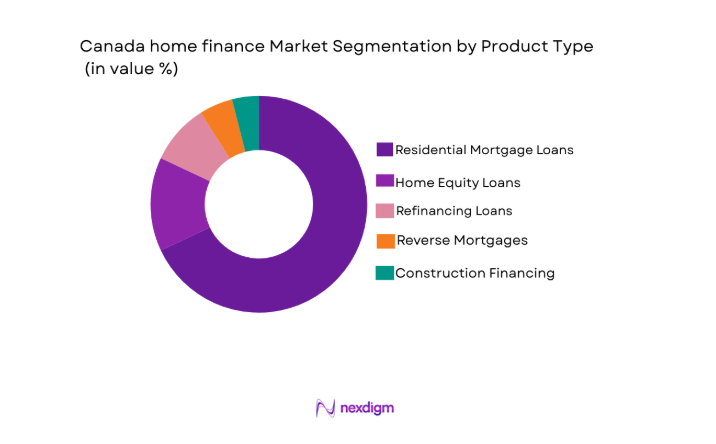

Canada home finance market is segmented by product type into residential mortgage loans, home equity loans, refinancing loans, reverse mortgages, and construction financing. Recently, residential mortgage loans has a dominant market share due to strong first-time buyer demand, refinancing cycles, regulatory-backed insurance availability, and established lender distribution networks across major urban centers, which collectively reinforce borrower preference for traditional amortized mortgage structures over alternative credit products.

By Platform Type

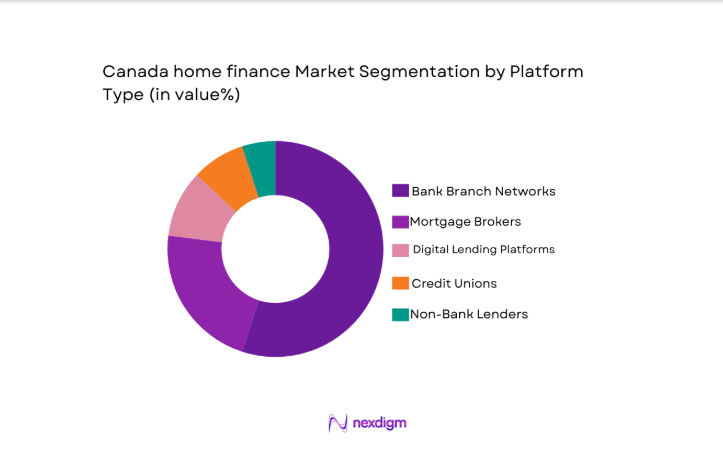

Canada home finance market is segmented by platform type into bank branch networks, mortgage brokers, digital lending platforms, credit unions, and non-bank lenders. Recently, bank branch networks has a dominant market share due to consumer trust in established financial institutions, integrated cross-selling capabilities, nationwide physical presence, bundled financial services, and competitive rate offerings supported by large balance sheets and diversified funding sources.

Competitive Landscape

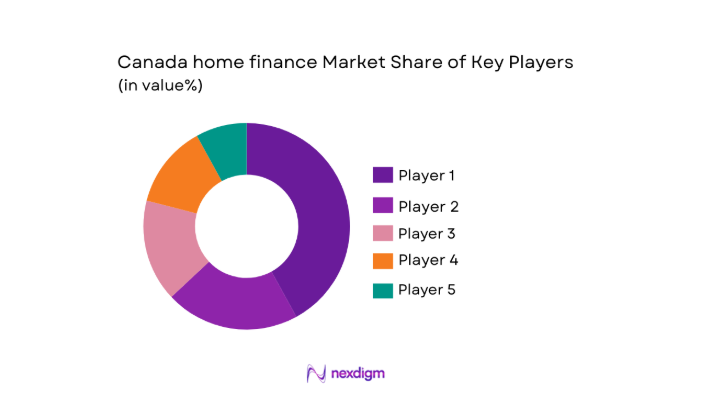

The Canada home finance market is moderately consolidated, with major chartered banks controlling a substantial share of mortgage originations and servicing portfolios. Large institutions leverage diversified funding sources, digital underwriting systems, and nationwide distribution, while non-bank lenders and brokers compete through specialized products and faster approvals. Consolidation is reinforced by regulatory capital requirements and mortgage insurance frameworks that favor well-capitalized lenders.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Mortgage Portfolio Size |

| Royal

Bank of Canada |

1864 | Toronto | ~ | ~ | ~ | ~ | ~ |

| Toronto-Dominion Bank | 1855 | Toronto | ~ | ~ | ~ | ~ | ~ |

| Bank of Montreal | 1817 | Montreal | ~ | ~ | ~ | ~ | ~ |

| Scotiabank | 1832 | Toronto | ~ | ~ | ~ | ~ | ~ |

| Canadian Imperial Bank of Commerce | 1867 | Toronto | ~ | ~ | ~ | ~ | ~ |

Canda Home Finance Market Analysis

Growth Drivers

Immigration Driven Household Formation and Urban Housing Demand

Canada’s sustained immigration inflows have significantly increased housing demand, directly influencing mortgage originations and home finance expansion across major metropolitan regions. New permanent residents and temporary workers typically transition toward rental housing initially but progressively enter homeownership markets, generating incremental demand for insured and conventional mortgage products. Urban centers with diversified employment bases experience concentrated household formation, leading to increased property transactions and refinancing cycles that support loan book expansion for lenders. Financial institutions respond by enhancing credit underwriting models tailored to new-to-credit borrowers and internationally mobile professionals. Population growth also stimulates new housing construction, indirectly boosting construction financing and developer-linked mortgage pipelines. Infrastructure expansion in transportation and commercial development further raises property valuations, reinforcing collateral strength for lenders. As household formation accelerates, competitive mortgage offerings intensify among banks and brokers, improving product accessibility. This demographic momentum provides structural stability to mortgage credit demand beyond cyclical interest rate movements.

Digitization of Mortgage Origination and Automated Credit Assessment Systems

The integration of advanced digital platforms across underwriting, document verification, and property valuation processes has reduced approval timelines and improved borrower convenience within the Canada home finance market. Automated valuation models and AI-based credit scoring tools allow lenders to process large volumes of applications with enhanced risk calibration and regulatory compliance. Digital onboarding systems minimize physical branch dependency while enabling remote income verification and identity authentication. Borrowers increasingly expect seamless application journeys supported by mobile interfaces and real-time rate comparison tools. Large financial institutions allocate significant investment toward cloud-based loan management systems that integrate analytics, fraud detection, and stress-testing capabilities. Efficiency gains lower operational costs per loan, supporting competitive pricing and portfolio scalability. Brokers and non-bank lenders leverage technology to differentiate through faster turnaround times. This structural shift toward digitized mortgage ecosystems strengthens long-term market expansion and resilience.

Market Challenges

Rising Household Debt Levels and Affordability Constraints

Elevated household leverage within Canada presents systemic risks to mortgage lenders, particularly in periods of monetary tightening and interest rate volatility. High property valuations in major metropolitan regions increase loan sizes relative to income, intensifying borrower vulnerability to repayment shocks. Regulatory stress tests require lenders to assess affordability under higher qualifying rates, which constrains loan eligibility for first-time buyers. Reduced affordability dampens transaction volumes and refinancing activity during tightening cycles. Financial institutions must maintain higher capital buffers to mitigate potential credit losses, affecting profitability metrics. Affordability pressures also shift demand toward smaller units or suburban properties, altering portfolio composition. Persistent housing supply shortages exacerbate price escalation in high-demand corridors. These structural imbalances introduce cyclical volatility within mortgage origination and servicing performance.

Interest Rate Volatility and Regulatory Capital Requirements

Fluctuating benchmark interest rates directly influence borrowing costs, refinancing incentives, and borrower repayment capacity across the Canada home finance market. Monetary policy adjustments impact both fixed and variable rate mortgage pricing structures, creating uncertainty for consumers planning long-term financial commitments. Regulatory capital frameworks imposed on federally regulated lenders require prudent provisioning against potential credit deterioration. Higher capital charges may reduce lending appetite or tighten underwriting standards during risk-sensitive periods. Variable rate borrowers face payment adjustments that affect disposable income and consumption patterns. Market participants must continuously recalibrate product offerings in response to yield curve movements. Mortgage insurers also adapt premium structures to reflect macroeconomic conditions. This interplay between interest rates and regulatory oversight introduces operational complexity and cyclical earnings variability for lenders.

Opportunities

Expansion of Green and Energy Efficient Home Financing Programs

Growing environmental awareness and federal sustainability initiatives create opportunities for specialized mortgage products tied to energy-efficient housing and retrofitting projects. Financial institutions can integrate preferential rates or extended amortization terms for certified green properties to encourage environmentally responsible construction and renovation. Government-backed incentives for energy retrofits increase demand for financing solutions tailored to solar installations and insulation upgrades. Lenders adopting environmental risk assessment frameworks enhance long-term portfolio resilience. Green bond issuances linked to mortgage pools provide diversified funding channels for banks. Consumer demand for sustainable living standards aligns with property developers prioritizing low-carbon housing projects. Digital assessment tools facilitate energy efficiency verification within underwriting workflows. This convergence of policy support and consumer preference creates scalable avenues for differentiated mortgage offerings.

Growth of Alternative and Private Lending Channels for Underserved Borrowers

Segments such as self-employed professionals, new immigrants, and credit-thin applicants present untapped growth potential within the Canada home finance market. Alternative lenders can deploy flexible income verification models and risk-based pricing to serve borrowers excluded from traditional underwriting frameworks. Fintech-enabled platforms improve borrower matching with niche capital providers. Broker networks expand access to customized financing structures beyond conventional amortization models. Private capital funds increasingly allocate resources toward mortgage-backed lending strategies, diversifying funding pools. Data analytics enable more granular borrower segmentation and dynamic pricing strategies. Digital documentation systems streamline approval processes for complex income profiles. This structural diversification enhances competitive intensity while broadening overall credit access across the housing finance ecosystem.

Future Outlook

Over the next five years, the Canada home finance market is expected to maintain structural stability supported by immigration-led housing demand and continued digital transformation of mortgage processes. Technological integration in underwriting and valuation will enhance efficiency and risk management. Regulatory oversight will remain prudent, reinforcing systemic resilience. Demand-side momentum from urban development and sustainability-linked housing initiatives is likely to sustain loan origination volumes across key metropolitan regions.

Major Players

- Royal Bank of Canada

- Toronto-Dominion Bank

- Bank of Montreal

- Scotiabank

- Canadian Imperial Bank of Commerce

- National Bank of Canada

- Desjardins Group

- First National Financial

- Home Capital Group

- Equitable Bank

- MCAP

- RMG Mortgages

- Laurentian Bank

- Street Capital Bank

- Alterna Savings

Key Target Audience

- Investment and venture capitalist firms

- Government and regulatory bodies

- Commercial banks

- Credit unions

- Mortgage brokers

- Real estate developers

- Private equity firms

- Housing finance corporations

Research Methodology

Step 1: Identification of Key Variables

Core variables including mortgage outstanding balances, origination volumes, platform penetration, and regulatory frameworks were identified through secondary research and validated against institutional financial disclosures and central banking data sources.

Step 2: Market Analysis and Construction

Market sizing was constructed using top-down assessment of outstanding residential mortgage credit combined with bottom-up evaluation of lender portfolios, ensuring consistency with publicly reported financial statements and housing finance statistics.

Step 3: Hypothesis Validation and Expert Consultation

Preliminary findings were validated through structured consultations with banking professionals, housing finance analysts, and risk management experts to ensure alignment with operational realities and regulatory interpretations.

Step 4: Research Synthesis and Final Output

All quantitative and qualitative insights were synthesized into a structured analytical framework, integrating macroeconomic indicators, competitive positioning, and policy developments to produce a comprehensive market assessment.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Low-interest rate cycles stimulating housing demand

Government backed mortgage insurance accessibility

Urban population growth and housing shortages

Expansion of digital mortgage origination channels

Immigration driven household formation - Market Challenges

Rising household debt burden and affordability constraints

Interest rate volatility impacting borrower eligibility

Stringent mortgage stress test regulations

Housing supply shortages in major cities

Credit risk exposure for lenders - Market Opportunities

Growth of green and energy efficient home financing

Expansion of digital only mortgage providers

Innovative products for aging homeowner equity access - Trends

Shift toward fully digital mortgage journeys

Increased adoption of variable and hybrid rate products

Growth of alternative and private lending markets

Integration of AI in underwriting and risk scoring

Sustainability linked housing finance products - Government Regulations & Defense Policy

Federal mortgage stress test framework enforcement

Mortgage insurance eligibility and LTV limits

Consumer protection and disclosure regulations - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Residential Mortgage Loans

Home Equity Loans

Refinancing Solutions

Reverse Mortgage Products

Construction and Self-Build Financing - By Platform Type (In Value%)

Bank Branch Networks

Digital Lending Platforms

Mortgage Broker Channels

Credit Union Networks

Non Bank Financial Institutions - By Fitment Type (In Value%)

Fixed Rate Financing

Variable Rate Financing

Hybrid Rate Structures

Open Term Mortgages

Closed Term Mortgages - By End User Segment (In Value%)

First Time Homebuyers

Property Investors

Homeowners Seeking Refinancing

Senior Homeowners

Self Employed Borrowers - By Procurement Channel (In Value%)

Direct Bank Origination

Mortgage Broker Intermediation

Online Aggregator Platforms

Credit Union Lending

Private Lender Channels

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (Interest Rates, Loan Tenure Flexibility, Digital Origination Capability, Approval Time, LTV Ratio, Product Range, Distribution Reach, Customer Support, Risk Assessment Model)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Royal Bank of Canada

TorontoDominion Bank

Bank of Montreal

Scotiabank

Canadian Imperial Bank of Commerce

National Bank of Canada

Desjardins Group

First National Financial

Home Capital Group

Equitable Bank

MCAP

RMG Mortgages

Laurentian Bank

Street Capital Bank

Alterna Savings

- First time buyers prioritizing affordability and insured mortgages

- Investors leveraging refinancing and equity extraction

- Seniors adopting reverse mortgage and equity release products

- Self employed borrowers relying on alternative lending channels

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now