Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Canada online insurance market generated approximately USD ~ billion in direct written premiums through fully digital channels, based on a recent historical assessment by Insurance Bureau of Canada and OSFI digital distribution filings. Growth is driven by insurer investments in automated underwriting, rising consumer adoption of mobile financial services, and cost optimization pressures encouraging direct-to-consumer digital policy sales. Embedded insurance partnerships with banks and e-commerce platforms are further accelerating digital policy issuance volumes across personal and SME lines.

Toronto and Montreal dominate Canada online insurance activity due to concentration of insurers, insurtech firms, and regulatory sandboxes enabling digital distribution innovation. Strong broadband penetration, fintech ecosystems, and multilingual consumer markets support rapid digital policy adoption in these cities. Vancouver also shows high online insurance uptake driven by tech-savvy populations and property insurance demand linked to urban real estate values. These urban hubs host major insurers’ digital headquarters, reinforcing platform development and customer acquisition scale advantages.

Market Segmentation

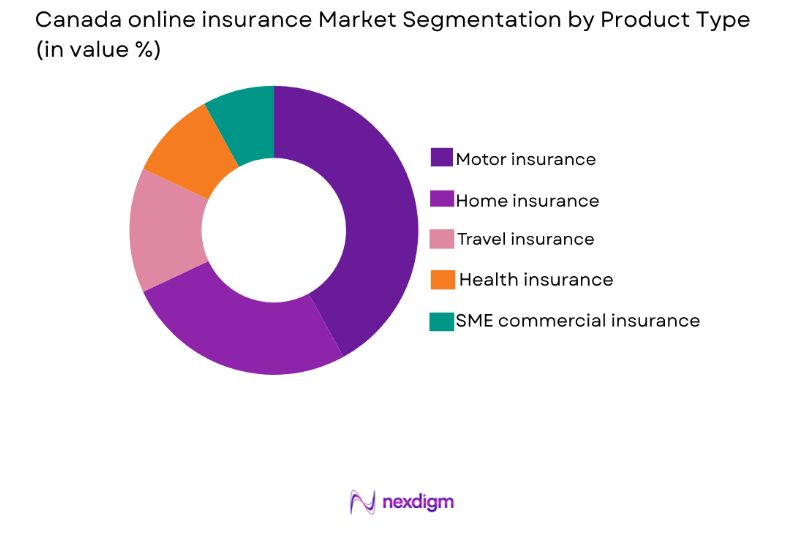

By Product Type

Canada online insurance market is segmented by product type into motor insurance, home insurance, travel insurance, health insurance, and SME commercial insurance. Recently, motor insurance has a dominant market share due to mandatory coverage requirements, high policy volumes, and established digital underwriting models enabling instant quotes and issuance. Strong brand competition and aggregator platforms also prioritize auto policies, reinforcing digital distribution leadership.

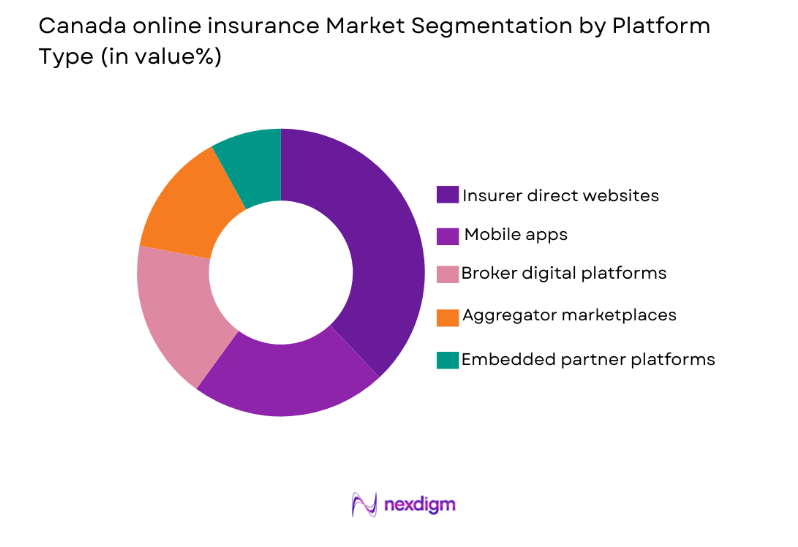

By Platform Type

Canada online insurance market is segmented by platform type into insurer direct websites, mobile apps, broker digital platforms, aggregator marketplaces, and embedded partner platforms. Recently, insurer direct websites have a dominant market share due to trusted brand presence, integrated policy servicing, and regulatory compliance controls. Consumers prefer purchasing directly from insurers’ digital portals for transparency, pricing confidence, and seamless claims management integration.

Competitive Landscape

Canada online insurance market shows moderate consolidation led by large multiline insurers and bank-affiliated insurers with strong digital platforms. Major players influence pricing, underwriting automation, and omnichannel integration strategies while insurtech entrants focus on niche digital experiences and usage-based offerings.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Digital Channel Strength |

| Intact Financial Corporation | 1809 | Toronto | ~ | ~ | ~ | ~ | ~ |

| Aviva Canada | 1835 | Markham | ~ | ~ | ~ | ~ | ~ |

| Desjardins Group | 1900 | Lévis | ~ | ~ | ~ | ~ | ~ |

| Manulife Financial | 1887 | Toronto | ~ | ~ | ~ | ~ | ~ |

| Sun Life Financial | 1865 | Toronto | ~ | ~ | ~ | ~ | ~ |

Canada Online Insurance Market Analysis

Growth Drivers

Rising Consumer Adoption of Digital Financial Services

Canada’s financial consumers increasingly prefer online channels for insurance discovery, comparison, and purchase due to convenience, transparency, and mobile-first behavior patterns shaped by digital banking and e-commerce adoption. Insurers have responded by expanding automated underwriting, instant quote engines, and self-service claims tools that reduce purchase friction and accelerate policy issuance times. High internet penetration and smartphone usage support broad demographic accessibility to online insurance platforms across personal and SME segments nationwide. Younger consumers entering homeownership and vehicle ownership cohorts show particularly strong digital insurance preference, reinforcing long-term demand growth. Aggregator and comparison platforms also educate consumers on price and coverage options, encouraging online policy switching and competitive digital acquisition strategies. Financial institutions and fintech ecosystems integrate insurance offerings into digital banking journeys, expanding embedded insurance distribution at scale. Pandemic-era remote service expectations have normalized digital-only interactions for insurance purchase and servicing across Canada. Cost-sensitive consumers increasingly compare premiums online, pushing insurers to enhance digital pricing transparency and responsiveness. Provincial regulators enabling electronic signatures and digital identity verification further legitimize online policy issuance processes. Together these behavioral, technological, and regulatory factors structurally reinforce sustained expansion of Canada’s online insurance market.

Insurer Cost Optimization and Automation Strategies

Canadian insurers face margin pressures from claims inflation, catastrophe losses, and operating costs, motivating investment in digital distribution to reduce acquisition and servicing expenses relative to broker-led channels. Online insurance platforms enable straight-through processing, automated underwriting decisions, and self-service policy management that lower administrative overhead per policy. Digital channels also provide granular customer data and analytics, improving risk pricing accuracy and cross-sell effectiveness across product lines. Direct online sales reduce commission costs associated with intermediaries while enabling insurers to maintain competitive pricing and profitability. Scalable cloud-based insurance cores support rapid product launches and digital experience improvements without heavy legacy infrastructure constraints. Claims automation tools shorten settlement cycles and reduce manual processing labor requirements, enhancing operational efficiency. Digital engagement increases retention through personalized communication and proactive renewal management. Insurers also leverage telematics and usage-based data collected through digital channels to refine underwriting and pricing precision. Strategic partnerships with insurtech firms accelerate deployment of AI and automation capabilities across underwriting and claims workflows. These structural cost and efficiency advantages continue to drive insurer commitment to expanding online insurance distribution across Canada.

Market Challenges

Legacy System Integration Constraints

Many Canadian insurers operate complex legacy policy administration systems that are difficult to integrate with modern digital front-end platforms, creating operational bottlenecks and limiting seamless online customer experiences. Migrating core insurance systems to cloud-based architectures requires significant capital investment, regulatory approvals, and operational transformation planning that can slow digital deployment timelines. Data silos across underwriting, claims, and customer systems hinder real-time pricing and servicing capabilities expected in online channels. Integration challenges also increase cybersecurity exposure during system transitions and interface development. Smaller regional insurers face resource limitations that constrain modernization efforts relative to larger competitors. Broker distribution models embedded in legacy processes complicate direct-to-consumer digital strategy alignment. Technical debt in legacy systems raises maintenance costs, reducing funds available for digital innovation. System downtime risks during migration projects can disrupt policy servicing and damage customer trust. Regulatory reporting and compliance requirements add complexity to system transformation initiatives. These legacy constraints remain a major structural barrier to rapid expansion of fully integrated online insurance ecosystems in Canada.

Consumer Trust and Advisory Expectations

Insurance products involve financial risk transfer and coverage complexity, leading many Canadian consumers to value human advisory interactions even when digital channels are available, which slows full online adoption. Trust concerns around claims fairness, coverage clarity, and insurer reliability influence purchasing decisions, particularly for higher-value home and commercial policies. Consumers may perceive online insurance as commoditized or lacking personalized advice compared to broker-assisted purchase experiences. Data privacy concerns related to digital identity verification and personal information sharing also affect online insurance confidence. Negative digital service experiences, such as claim delays or automated rejection perceptions, can reduce trust in online channels. Older demographics and rural populations maintain stronger reliance on brokers and agents for insurance guidance. Brand reputation and financial strength remain critical factors influencing online insurer selection beyond price comparison. Regulatory protections communicated through brokers may not be fully understood in digital journeys. Insurers must invest heavily in user experience design and transparent communication to build digital trust. These behavioral and perception barriers continue to moderate the pace of Canada’s online insurance adoption.

Opportunities

Expansion of Embedded Insurance in Digital Ecosystems

Partnerships between insurers and banks, e-commerce platforms, mobility services, and property marketplaces enable insurance products to be integrated seamlessly into digital purchase journeys, creating substantial growth opportunities in Canada online insurance distribution. Consumers increasingly expect insurance offers at the point of asset acquisition such as vehicle purchase, travel booking, or home rental transactions within digital platforms. Embedded distribution reduces acquisition friction and expands reach to previously untapped customer segments without standalone marketing costs. Canadian banks and fintech platforms with large digital user bases provide scalable channels for integrated insurance offerings. Regulatory acceptance of digital identity and consent frameworks supports secure embedded policy issuance processes. Usage-based and short-term insurance products align naturally with embedded contexts such as car-sharing or travel services. Data sharing within partnerships enables personalized pricing and product recommendations. Insurers benefit from lower acquisition costs and higher conversion rates through contextual digital offers. Ecosystem partnerships also strengthen customer engagement across financial services journeys. These structural advantages position embedded insurance as a major expansion avenue for Canada’s online insurance market.

AI-Driven Personalization and Risk-Based Pricing Models

Advanced analytics and artificial intelligence enable insurers to offer highly personalized insurance products through digital channels, creating opportunities for differentiated customer experiences and improved risk selection in Canada online insurance. Machine learning models analyze behavioral, demographic, and usage data to tailor coverage options and pricing to individual risk profiles. Telematics and IoT data integration supports dynamic pricing for auto and property insurance based on real-world usage patterns. Personalized digital journeys increase conversion rates by presenting relevant coverage bundles and recommendations. AI-driven chatbots and virtual advisors provide scalable personalized support across online platforms. Predictive analytics improves fraud detection and claims automation accuracy, enhancing operational performance. Customers increasingly expect personalized financial services aligned with broader digital experience trends. Regulatory frameworks allowing data-driven underwriting innovation encourage adoption. Insurers leveraging AI personalization gain competitive differentiation in online acquisition and retention. These technological capabilities present significant growth potential for Canada’s online insurance ecosystem.

Future Outlook

Canada online insurance market is expected to expand steadily as insurers accelerate digital transformation and consumers normalize online policy purchase and servicing. Growth will be supported by AI underwriting, embedded insurance partnerships, and mobile-first customer engagement models. Regulatory acceptance of digital identity and electronic transactions will continue enabling fully online insurance journeys. Competitive dynamics will favor insurers with scalable digital platforms and advanced analytics capabilities. Demand from younger, tech-savvy consumers and SMEs will further strengthen digital insurance adoption nationwide.

Major Players

- Intact Financial Corporation

- Desjardins Group

- Aviva Canada

- Manulife Financial

- Sun Life Financial

- Canada Life

- TD Insurance

- RBC Insurance

- Beneva

- Economical Insurance

- The Co-operators

- Allstate Canada

- Travelers Canada

- Sonnet Insurance

- Policy Me

Key Target Audience

- Insurance companies

- Insurtech firms

- Banks and financial institutions

- Investments and venture capitalist firms

- Government and regulatory bodies

- Digital platform providers

- Brokerage networks

- Technology vendors

Research Methodology

Step 1: Identification of Key Variables

Core variables such as digital premiums, policy volumes, distribution channels, and technology adoption indicators were identified through regulatory filings and insurer disclosures. Demand drivers and consumer behavior metrics were also mapped.

Step 2: Market Analysis and Construction

Market size and segmentation were constructed using insurer financial reports, industry associations, and digital distribution data. Channel share estimates were derived from policy issuance and platform usage statistics.

Step 3: Hypothesis Validation and Expert Consultation

Findings were validated through consultations with insurance executives, digital distribution specialists, and regulatory experts. Assumptions on channel shares and technology adoption were cross-checked against market practices.

Step 4: Research Synthesis and Final Output

All validated data and insights were synthesized into structured market analysis covering segmentation, competitive landscape, and growth dynamics. Consistency checks ensured alignment with industry benchmarks and disclosures.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Rising consumer preference for digital financial services

Expansion of mobile-first insurance distribution

Cost efficiency pressures on insurers driving automation - Market Challenges

Legacy system integration constraints in insurers

Data privacy and cybersecurity compliance complexity

Consumer trust gaps in fully digital insurance purchase - Market Opportunities

Expansion of SME digital insurance offerings

AI-enabled personalized policy pricing

Partnerships with fintech and e-commerce platforms - Trends

Shift toward instant policy issuance online

Use of AI chatbots for claims and servicing - Government Regulations & Defense Policy

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Digital policy purchase platforms

Online claims management systems

Web-based underwriting engines

Customer self-service portals

Aggregator and comparison platforms - By Platform Type (In Value%)

Web browser platforms

Mobile app platforms

Embedded insurance APIs

Partner marketplace platforms

Cloud-native insurance suites - By Fitment Type (In Value%)

Standalone insurer platforms

Integrated broker systems

White-label digital storefronts

API-integrated ecosystems

Omnichannel unified platforms - By End User Segment (In Value%)

Individual retail customers

SME policyholders

Insurance brokers and advisors

- Market share of major players

- Cross Comparison Parameters (Digital channel maturity, Product breadth, AI underwriting capability, Claims automation level, Partner ecosystem depth, Mobile experience quality, Pricing competitiveness, Customer acquisition cost, Regulatory compliance readiness)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Intact Financial Corporation

Desjardins Group

Aviva Canada

Manulife Financial

Sun Life Financial

Canada Life

TD Insurance

RBC Insurance

Beneva

Economical Insurance

The Co-operators

Allstate Canada

Travelers Canada

Sonnet Insurance

PolicyMe

- Retail consumers prioritizing convenience and price transparency

- SMEs adopting online policies for speed and simplicity

- Brokers shifting to hybrid digital advisory models

- Enterprises integrating digital insurance procurement platforms

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now