Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Canada Semiconductor Manufacturing Market is valued at USD ~ billion and is experiencing significant growth due to increasing demand for advanced electronic devices and systems across various industries such as telecommunications, automotive, and consumer electronics. The market size is driven by advancements in technology, a robust supply chain, and substantial investments from both private and government sectors. The Canadian government’s support for research and development, along with international collaborations, has contributed to this market’s growth, positioning it as a key player in the global semiconductor supply chain.

Canada, particularly cities like Toronto, Ottawa, and Vancouver, is witnessing dominant growth due to the presence of leading semiconductor manufacturers and research institutions. The country’s well-established technology infrastructure, skilled workforce, and proximity to the U.S. market give it a competitive edge in the global semiconductor manufacturing landscape. Canada’s dominance is further supported by government initiatives focused on expanding its semiconductor capabilities, promoting innovation, and strengthening its supply chain resilience. These factors are instrumental in making Canada a key hub for semiconductor manufacturing in North America.

Market Segmentation

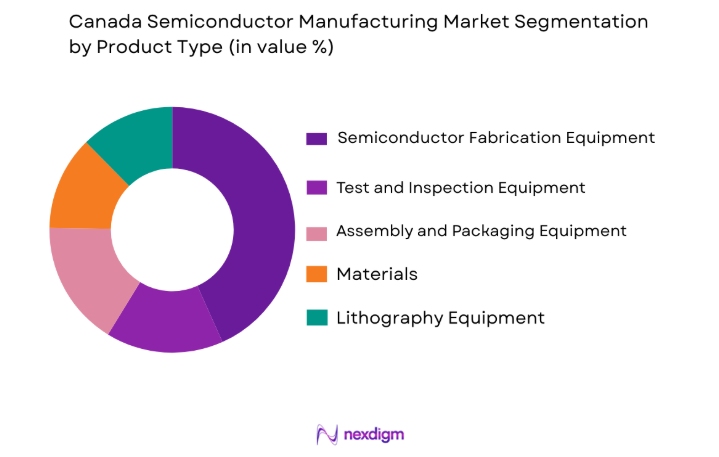

By Product Type:

The Canada Semiconductor Manufacturing Market is segmented by product type into semiconductor fabrication equipment, test and inspection equipment, assembly and packaging equipment, materials, and lithography equipment. Recently, semiconductor fabrication equipment has emerged as the dominant sub-segment. This is due to the high demand for advanced chips used in various industries, especially in the automotive, telecommunications, and consumer electronics sectors. The increasing complexity of chip designs and the shift towards smaller, more efficient devices are driving the demand for semiconductor fabrication equipment, making it the market leader in Canada.

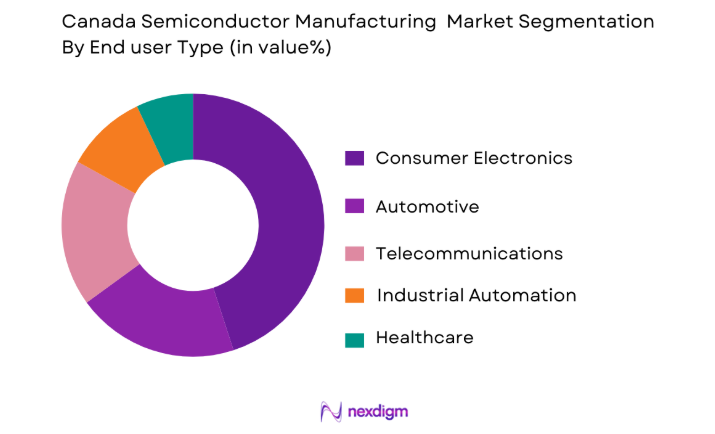

By End-User Industry:

The market is also segmented by end-user industry, which includes consumer electronics, automotive, telecommunications, industrial automation, and healthcare. The consumer electronics industry is currently leading the market due to the rapid expansion of demand for smartphones, wearable devices, and other smart consumer gadgets. The sector’s continuous growth and innovation in product designs, coupled with the rising demand for high-performance chips, have made consumer electronics the dominant force in Canada’s semiconductor manufacturing sector. As consumer electronics companies continue to invest in next-generation technology, the demand for semiconductors is expected to remain strong.

Competitive Landscape

The competitive landscape of the Canada Semiconductor Manufacturing Market is highly dynamic, with a mix of established players and new entrants driving innovation. Key players are focusing on technological advancements and improving the efficiency of semiconductor manufacturing processes to stay competitive. The market has seen consolidation through strategic mergers and acquisitions as companies strive to expand their market presence and capabilities. Leading companies are also investing heavily in research and development to enhance their product offerings, addressing the increasing demand for smaller, more powerful chips.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Additional Parameter |

| Intel Corporation | 1968 | Santa Clara, CA | ~ | ~ | ~ | ~ | ~ |

| TSMC | 1987 | Hsinchu, Taiwan | ~ | ~ | ~ | ~ | ~ |

| Samsung Electronics | 1938 | Suwon, South Korea | ~ | ~ | ~ | ~ | ~ |

| Micron Technology | 1978 | Boise, ID | ~ | ~ | ~ | ~ | ~ |

| Qualcomm | 1985 | San Diego, CA | ~ | ~ | ~ | ~ | ~ |

Canada Semiconductor Manufacturing Market Analysis

Growth Drivers

Technological Advancements in Semiconductor Manufacturing:

Technological advancements in semiconductor manufacturing are one of the primary growth drivers for the Canada Semiconductor Manufacturing Market. Over the years, there have been significant breakthroughs in semiconductor technology, such as the development of smaller, more efficient microchips that meet the increasing demands of various sectors. The shift towards advanced technologies such as 5G, artificial intelligence (AI), and the Internet of Things (IoT) is driving the need for more powerful semiconductor solutions. As the demand for high-performance computing, cloud services, and connected devices grows, semiconductor manufacturers are investing heavily in next-generation technology to stay competitive. These advancements are not only enhancing the functionality of consumer electronics but also enabling the development of new applications in automotive and industrial sectors, further propelling the growth of semiconductor manufacturing. Companies are also focusing on improving manufacturing processes, such as leveraging artificial intelligence and machine learning to optimize production and enhance product quality, which will likely continue to drive the market forward. Moreover, the increasing demand for high-performance computing and data centers is expected to further fuel the expansion of semiconductor manufacturing capabilities in Canada, contributing to market growth.

Rising Demand for Consumer Electronics:

Rising demand for consumer electronics is another significant growth driver for the Canada Semiconductor Manufacturing Market. As consumer electronics continue to evolve, there is an increasing need for advanced semiconductors that can support new functionalities such as AI, 5G, and higher processing speeds. Products such as smartphones, laptops, smart wearables, and other connected devices are driving the demand for high-performance chips. The ongoing trend of smart homes, augmented reality, and virtual reality is also contributing to the increased need for semiconductors. The global demand for consumer electronics is expected to grow exponentially in the coming years, and Canada, with its well-developed semiconductor manufacturing capabilities, is positioned to play a significant role in meeting this demand. The increasing reliance on semiconductor-based technologies in various consumer gadgets will continue to fuel growth in Canada’s semiconductor manufacturing market. Additionally, innovations in consumer electronics, such as flexible displays, foldable smartphones, and more, will require the development of cutting-edge semiconductor solutions, thereby boosting the market further.

Market Challenges

High Capital Investment for Semiconductor Manufacturing:

One of the major challenges facing the Canada Semiconductor Manufacturing Market is the high capital investment required for establishing and maintaining semiconductor fabrication facilities. Semiconductor manufacturing is a highly capital-intensive process, requiring significant investments in advanced machinery, technology, and skilled labor. The cost of establishing state-of-the-art fabs, as well as the continuous need for technological upgrades to remain competitive, can be a major barrier for new entrants and smaller players. Additionally, the cost of raw materials and supply chain complexities further increase the financial burden on manufacturers. The high initial investment also presents challenges in terms of profitability, as semiconductor manufacturers need to ensure that production volumes are high enough to recover their capital expenditures. Despite these challenges, companies are exploring partnerships and collaborations to share costs and mitigate financial risks. However, the substantial capital expenditure remains a significant hurdle for many players in the semiconductor manufacturing sector, particularly in Canada, where competition is increasing and global market dynamics are constantly changing.

Supply Chain Vulnerabilities and Material Shortages:

Supply chain vulnerabilities and material shortages are another challenge faced by the Canada Semiconductor Manufacturing Market. The global semiconductor supply chain is highly complex and relies on various components from multiple regions, making it susceptible to disruptions. Recent events, such as the COVID-19 pandemic and geopolitical tensions, have highlighted the fragility of global supply chains, leading to delays and shortages in semiconductor production. Material shortages, particularly for essential raw materials such as silicon and rare earth metals, have caused significant challenges for semiconductor manufacturers. The disruption in the supply of key materials has led to production delays and higher prices, which in turn has impacted the overall market performance. Manufacturers are increasingly concerned about the dependence on foreign suppliers for critical materials, and this vulnerability is becoming a key challenge for the industry. Companies are now looking for ways to diversify their supply chains and reduce their reliance on a few key sources of materials, but overcoming these challenges will take time and substantial effort.

Opportunities

Expansion in Electric Vehicles and Automotive Electronics:

The growing demand for electric vehicles (EVs) presents a significant opportunity for the Canada Semiconductor Manufacturing Market. As automakers shift towards electric vehicles and incorporate more advanced technologies into their vehicles, there is a rising need for semiconductor solutions to power various systems such as battery management, electric drive systems, and infotainment. The automotive industry is undergoing a major transformation, with a greater emphasis on electrification, automation, and connected features. This trend presents an opportunity for semiconductor manufacturers in Canada to capitalize on the increasing demand for chips designed specifically for electric vehicles and related technologies. As EV adoption continues to rise, semiconductor manufacturers will be required to develop chips that can meet the unique demands of the automotive sector, such as ensuring reliability, efficiency, and integration with other in-vehicle technologies. This opportunity is likely to drive growth in the semiconductor manufacturing sector in Canada, as companies innovate and develop specialized solutions for the automotive industry.

Advancements in 5G Infrastructure:

Advancements in 5G infrastructure are another key opportunity for the Canada Semiconductor Manufacturing Market. The global rollout of 5G networks is expected to create a surge in demand for semiconductors, as 5G technologies require high-performance chips for applications such as network equipment, smartphones, and connected devices. In Canada, the demand for 5G infrastructure and related devices is growing, and semiconductor manufacturers are well-positioned to meet this demand. The increasing adoption of 5G-enabled devices, along with the expansion of 5G networks in urban and rural areas, will drive the need for advanced semiconductor solutions that can support high-speed connectivity and low-latency communication. As 5G becomes a critical enabler for a wide range of industries, including healthcare, industrial automation, and transportation, semiconductor manufacturers in Canada will have significant opportunities to develop and supply the necessary components for 5G infrastructure. This trend will continue to contribute to the growth of the semiconductor manufacturing market in Canada.

Future Outlook

The future outlook for the Canada Semiconductor Manufacturing Market is highly positive, with expected growth driven by advancements in technology and rising demand for consumer electronics, automotive solutions, and 5G infrastructure. The market is anticipated to benefit from government support and investments aimed at boosting the local semiconductor supply chain. Additionally, ongoing technological developments in AI, IoT, and renewable energy solutions are expected to further fuel demand for high-performance semiconductors, ensuring steady market expansion over the next five years.

Major Players

- Intel Corporation

- TSMC

- Samsung Electronics

- Micron Technology

- Qualcomm

- NXP Semiconductors

- Texas Instruments

- Broadcom

- STMicroelectronics

- Infineon Technologies

- ON Semiconductor

- Renesas Electronics

- Analog Devices

- Skyworks Solutions

- Maxim Integrated

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Semiconductor manufacturers

- Automotive and electronics manufacturers

- Telecommunications service providers

- Healthcare technology providers

- Electric vehicle companies

- Technology and IT solution providers

Research Methodology

Step 1: Identification of Key Variables

Key variables such as market trends, growth drivers, and challenges are identified through industry reports, expert consultations, and primary research.

Step 2: Market Analysis and Construction

The market is analyzed using historical data, current market performance, and growth trends, alongside projections for future growth.

Step 3: Hypothesis Validation and Expert Consultation

Hypotheses regarding market performance and trends are validated with experts in the semiconductor and electronics industries through interviews and surveys.

Step 4: Research Synthesis and Final Output

The findings from analysis and expert validation are synthesized to create the final report, providing actionable insights into the market.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Increasing Demand for Consumer Electronics

Government Initiatives Supporting Semiconductor Manufacturing

Technological Advancements in Semiconductor Design - Market Challenges

High Capital Expenditure for Semiconductor Manufacturing

Supply Chain Disruptions in Raw Materials

Intense Global Competition in Semiconductor Production - Market Opportunities

Expansion in Electric Vehicle Production

Rising Demand for Semiconductor Solutions in 5G Networks

Growth in Artificial Intelligence and Machine Learning Applications - Trends

Advancement in Semiconductor Materials

Integration of AI in Semiconductor Design

Increasing Demand for Energy-Efficient Semiconductor Solutions - Government Regulations

- SWOT Analysis of Key Competitors

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Semiconductor Fabrication Equipment

Test and Inspection Equipment

Assembly and Packaging Equipment

Materials

Lithography Equipment - By Platform Type (In Value%)

Integrated Circuits

Discrete Semiconductors

Optoelectronics

Microelectromechanical Systems (MEMS)

Sensors - By Fitment Type (In Value%)

On-premise Solutions

Cloud-based Solutions

Hybrid Solutions

Modular Solutions

Integrated Solutions - By EndUser Segment (In Value%)

Consumer Electronics

Automotive

Telecommunications

Healthcare

- Market Share Analysis

- CrossComparison Parameters (System Type, Platform Type, Procurement Channel, EndUser Segment, Fitment Type)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Porter’s Five Forces

- Key Players

Intel Corporation

TSMC

Samsung Electronics

GlobalFoundries

NXP Semiconductors

Micron Technology

Broadcom

Qualcomm

STMicroelectronics

Infineon Technologies

ON Semiconductor

Renesas Electronics

Texas Instruments

Analog Devices

Skyworks Solutions

- Increased Investment in Semiconductor Solutions for Automotive

- Growth in Consumer Electronics Market Driving Semiconductor Demand

- Telecommunications Industry’s Need for 5G Semiconductor Solutions

- Healthcare Industry Adopting Semiconductors for Medical Devices

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now