Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Canada telemedicine market is experiencing rapid growth, driven by increased adoption of digital health solutions and government initiatives aimed at improving healthcare accessibility. The market size, based on recent assessments, has reached USD ~ billion, reflecting a growing demand for virtual healthcare services. Factors such as the rising healthcare costs, the need for accessible healthcare in remote areas, and advancements in digital health technologies are contributing to this expansion. Moreover, the COVID-19 pandemic significantly accelerated the integration of telemedicine into the healthcare system, further reinforcing its importance in delivering care efficiently.

Major cities like Toronto, Vancouver, and Montreal are at the forefront of the telemedicine revolution, largely due to their strong healthcare infrastructure, high population density, and technological advancements. These regions benefit from robust internet connectivity, enabling seamless adoption of telehealth solutions. Provincial governments in these areas have actively supported telemedicine initiatives, making healthcare more accessible, especially in rural and underserved communities. Additionally, the presence of leading healthcare providers and technology firms has further solidified these cities’ dominance in the telemedicine market.

Market Segmentation

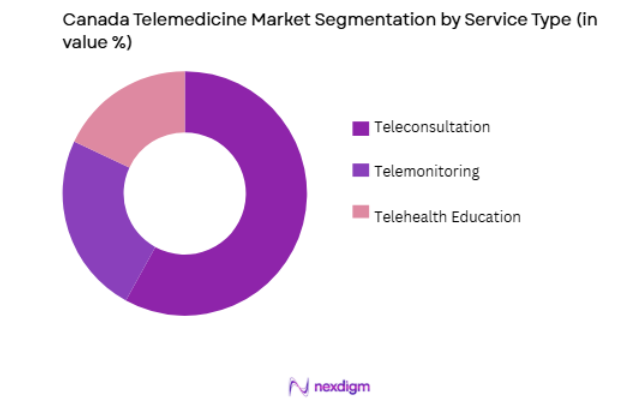

By Service Type

The Canada telemedicine market is segmented by service type into teleconsultation, telemonitoring, and telehealth education services. Among these, teleconsultation has emerged as the dominant sub-segment, largely due to the convenience and cost-effectiveness it offers for both patients and healthcare providers. This sub-segment is propelled by increasing patient demand for remote consultations and the widespread adoption of digital health platforms. Teleconsultation services are particularly popular for managing chronic diseases, mental health services, and follow-up care, which makes them a primary component of telemedicine in Canada. Additionally, growing healthcare infrastructure and government incentives further support the widespread adoption of teleconsultation services in urban and rural areas, leading to its dominant market share.

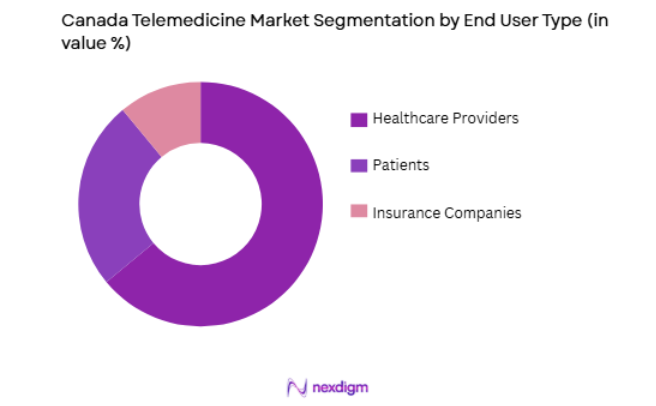

By End-User

The Canada telemedicine market is also segmented by end-user, with healthcare providers, patients, and insurance companies being the key players. Healthcare providers, such as hospitals and clinics, dominate the market share due to the increasing need for integrated telemedicine solutions to expand access to care and reduce operational costs. The adoption of telemedicine by healthcare providers is driven by the desire to streamline workflows, offer continuous care for chronic conditions, and enhance patient satisfaction. Additionally, the integration of telemedicine platforms with existing healthcare systems facilitates a seamless experience for both providers and patients, contributing to the sub-segment’s dominant position in the market.

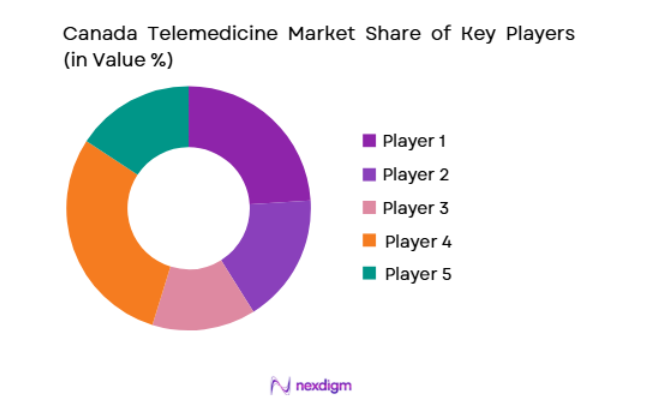

Competitive Landscape

The competitive landscape of the Canada telemedicine market is characterized by significant consolidation, with major players expanding their services to meet growing demand. Leading companies are investing heavily in research and development to enhance the capabilities of their platforms, focusing on improving user experience, scalability, and regulatory compliance. These players are also entering strategic partnerships with healthcare providers to integrate telemedicine solutions seamlessly into existing healthcare systems. As a result, there has been a noticeable shift toward more integrated, comprehensive telemedicine offerings, driving market growth and increasing competition.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (2024) | Key Partnerships |

| Telus Health | 2002 | Vancouver, Canada | ~ | ~ | ~ | ~ | ~ |

| Maple | 2015 | Toronto, Canada | ~ | ~ | ~ | ~ | ~ |

| Akira by TELUS Health | 2017 | Vancouver, Canada | ~ | ~ | ~ | ~ | ~ |

| Dialogue Health | 2016 | Montreal, Canada | ~ | ~ | ~ | ~ | ~ |

| MedeAnalytics | 2008 | Toronto, Canada | ~ | ~ | ~ | ~ | ~ |

Canada Telemedicine Market Analysis

Growth Drivers

Government Initiatives

The Canadian government has been a key player in driving the telemedicine market forward through funding initiatives and regulatory support. Over recent years, various provinces have implemented policies that promote the adoption of digital health solutions. This has included offering subsidies for telemedicine infrastructure, launching programs that integrate telehealth into public health services, and expanding healthcare access in rural areas. With an aging population and increasing demand for healthcare services, the government’s proactive approach has been crucial in facilitating the transition to telemedicine. Additionally, the push for cost-effective healthcare solutions that improve patient outcomes has further reinforced the government’s role as a growth driver.

Technological Advancements

The rapid advancements in telemedicine technology, such as AI-powered diagnostics, remote monitoring tools, and integrated patient management systems, are significantly driving the market. As technology evolves, it enables healthcare providers to offer more personalized, efficient, and accurate care remotely. Innovations in mobile health apps, wearable devices, and video consultation platforms have made telemedicine more accessible to both patients and healthcare providers. These advancements are reducing barriers to care, such as long wait times and geographical limitations, and improving the overall quality of remote healthcare, leading to a strong demand for telemedicine solutions.

Market Challenges

Data Security and Privacy Concerns

The issue of data security and patient privacy remains one of the primary challenges faced by the telemedicine market in Canada. With the rise of telehealth services, there has been a growing concern over the security of sensitive medical data, particularly in the face of cyber-attacks and data breaches. Regulatory requirements such as the Personal Health Information Protection Act (PHIPA) impose strict obligations on healthcare providers to safeguard patient data. While telemedicine platforms are increasingly adopting advanced encryption technologies to protect information, these concerns continue to hinder the widespread adoption of telehealth, especially in areas with less robust cybersecurity infrastructure.

Regulatory Barriers and Licensing Issues

Another significant challenge in the Canadian telemedicine market is the complex regulatory framework that governs telemedicine services across provincial lines. While the Canadian federal government has supported telehealth, each province has its own set of regulations regarding telemedicine delivery, licensure requirements, and reimbursement policies. This has led to inconsistencies in how telemedicine services are provided and reimbursed across the country. The lack of standardization has created confusion among healthcare providers and patients, leading to delays in the adoption of telemedicine solutions in some regions. Resolving these regulatory barriers remains a critical challenge for the market’s growth.

Opportunities

Expansion of Telehealth in Rural Areas

One of the biggest opportunities in the Canadian telemedicine market lies in the expansion of telehealth services to rural and remote communities. With fewer healthcare facilities in these areas and a high demand for accessible healthcare services, telemedicine presents a solution to bridge the gap. Government initiatives aimed at increasing healthcare access in underserved regions, combined with technological advancements, make rural telehealth a high-growth opportunity. As more rural areas are equipped with digital health infrastructure, the demand for telemedicine services will continue to rise, creating a significant market opportunity.

Integration with Wearable Health Devices

Another promising opportunity for the Canada telemedicine market is the integration of telemedicine platforms with wearable health devices such as smartwatches, fitness trackers, and remote patient monitoring tools. These devices allow healthcare providers to track patients’ health metrics in real-time, providing valuable insights for personalized care. The increasing adoption of wearable devices, combined with the growing trend of remote patient monitoring, creates an opportunity for telemedicine providers to expand their service offerings and enhance their value proposition. This integration will further drive the demand for telemedicine services, particularly in chronic disease management and preventive care.

Future Outlook

The Canada telemedicine market is expected to continue its upward trajectory over the next five years, fueled by ongoing technological advancements and government support for digital health solutions. The integration of AI, machine learning, and advanced telecommunication infrastructure is expected to enhance the quality and accessibility of telemedicine services, making them more efficient and affordable. In addition, regulatory frameworks are expected to evolve to accommodate the growing demand for remote healthcare services, creating a more streamlined environment for telemedicine providers. As patient expectations shift towards more accessible and personalized healthcare, the telemedicine market in Canada will remain a key component of the country’s healthcare ecosystem.

Major Players

- Telus Health

- Maple

- Akira by TELUS Health

- Dialogue Health

- MedeAnalytics

- Health Canada’s Telemedicine Services

- OnCall Health

- CareBridge

- MedeAnalytics

- RXNT

- Medchart

- Zoom Health

- Reliance Health

- eHealth Ontario

- Medisys Health Group

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Healthcare providers

- Digital health technology companies

- Pharmaceutical companies

- Medical device manufacturers

- Insurance providers

- Hospitals and clinics

Research Methodology

Step 1: Identification of Key Variables

The first step in the research process involves identifying key variables that will influence the Canada telemedicine market. These include technological advancements, regulatory changes, patient demographics, and industry partnerships.

Step 2: Market Analysis and Construction

A thorough market analysis is conducted to understand current market trends, challenges, and growth drivers. This step involves analyzing secondary data, including industry reports and market research publications.

Step 3: Hypothesis Validation and Expert Consultation

Expert consultations and primary research help validate hypotheses formed during the analysis phase. Interviews with key stakeholders in the telemedicine sector, including healthcare providers and technology firms, are conducted to gather insights.

Step 4: Research Synthesis and Final Output

The final step involves synthesizing all gathered data into a comprehensive report, which provides actionable insights and recommendations for stakeholders in the Canada telemedicine market.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Government Investments in Telehealth Infrastructure

Technological Advancements in Telecommunication

Rising Healthcare Demand in Remote Areas - Market Challenges

Data Security and Privacy Concerns

Technological Integration Challenges

Lack of Awareness Among Healthcare Providers - Market Opportunities

Telehealth Adoption in Rural Areas

Growing Demand for Remote Patient Monitoring

Expanding Telemedicine for Mental Health Services - Trends

Increase in AI and Machine Learning in Telemedicine

Growth of Wearable Health Technology - Government Regulations

Telemedicine Reimbursement Policies

Telemedicine Licensing and Accreditation

Privacy and Data Protection Laws - SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Telemedicine Software

Telemedicine Equipment

Telemedicine Services

Telehealth Platforms

Remote Monitoring Systems - By Platform Type (In Value%)

Mobile Platforms

Web Platforms

Hybrid Platforms

On-premise Platforms

Cloud-based Platforms - By Fitment Type (In Value%)

On-premise Solutions

Cloud-based Solutions

Hybrid Solutions

Integrated Solutions - By End User Segment (In Value%)

Hospitals

Clinics

Healthcare Providers

- Market Share Analysis

- Cross Comparison Parameters (System Type, Platform Type, Procurement Channel, End User Segment, Fitment Type, Technology Integration, Regulatory Compliance, Market Penetration, Service Availability, Cost Structure)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Telus Health

Rogers Communications

MedeAnalytics

Babylon Health

Doximity

Amwell

Doctor On Demand

MDTech

InTouch Health

Maple

Lifecare

SnapMD

OnDox

Kaiser Permanente

Cerner Corporation

- Hospitals Integrating Telemedicine for Patient Care

- Healthcare Providers Increasing Virtual Consultations

- Clinics Expanding Telehealth Services

- Patients Seeking Convenient Healthcare Solutions

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now