Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Canada wealth management market manages approximately USD ~ trillion in client assets based on a recent historical assessment, according to Investment Funds Institute of Canada and Canadian Bankers Association disclosures. Growth is driven by sustained household financial wealth accumulation of about USD ~ trillion and strong retirement savings flows into managed products reported by Statistics Canada. Expansion of fee-based advisory mandates and discretionary portfolio adoption continues to shift assets from transactional brokerage toward holistic wealth management relationships.

Toronto and Montreal dominate Canada wealth management market activity due to concentration of financial institutions, affluent households, and capital markets infrastructure documented by federal financial sector data. Toronto hosts major bank-owned wealth platforms and accounts for over USD ~ trillion in managed financial assets linked to the metropolitan region’s investor base. Vancouver also shows strong wealth advisory density driven by high household net worth and cross-border investment flows connected to global real estate and technology wealth creation.

Market Segmentation

By Product Type

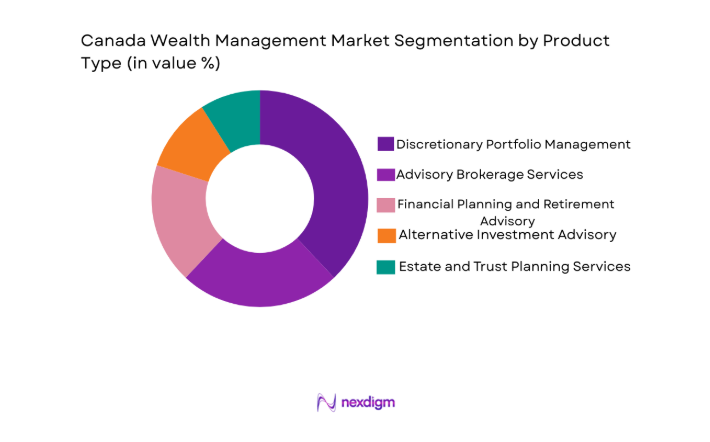

Canada wealth management market is segmented by product type into discretionary portfolio management, advisory brokerage, financial planning, alternative investment advisory, and estate and trust services. Recently, discretionary portfolio management has a dominant market share due to factors such as rising demand for delegated investment decision making, strong brand presence of bank-affiliated managers, established portfolio infrastructure, and client preference for holistic managed solutions amid complex markets.

By Platform Type

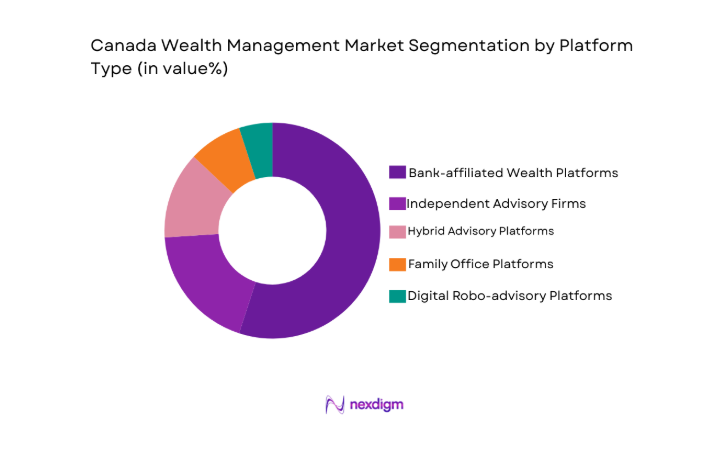

Canada wealth management market is segmented by platform type into bank-affiliated platforms, independent advisory firms, digital robo-advisory platforms, family office platforms, and hybrid advisory platforms. Recently, bank-affiliated platforms have a dominant market share due to factors such as nationwide branch distribution, integrated banking relationships, strong trust perception, large advisor networks, and comprehensive investment product manufacturing capabilities embedded within major financial institutions.

Competitive Landscape

Canada wealth management market shows a highly consolidated structure dominated by large bank-owned platforms alongside a limited number of national independent firms, creating high entry barriers and scale advantages. Major players control distribution, product manufacturing, and advisory networks, enabling integrated client capture across banking and investment channels. Consolidation has intensified through acquisitions of independent advisors and technology platforms, reinforcing the leadership of established institutions while smaller firms specialize in niche advisory and ultra-wealth segments.

|

Company Name |

Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | AUM Focus |

| RBC Wealth Management | 1901 | Toronto | ~ | ~ | ~ | ~ | ~ |

| TD Wealth | 1855 | Toronto | ~ | ~ | ~ | ~ | ~ |

| BMO Wealth Management | 1817 | Montreal | ~ | ~ | ~ | ~ | ~ |

| Scotiabank Wealth Management | 1832 | Toronto | ~ | ~ | ~ | ~ | ~ |

| CIBC Private Wealth | 1867 | Toronto | ~ | ~ | ~ | ~ | ~ |

Canda Wealth Management Market Analysis

Growth Drivers

Intergenerational Wealth Transfer and Aging Demographics Expansion

Canada wealth management market is experiencing strong structural demand as a substantial portion of national household wealth transitions from older generations to heirs and beneficiaries who seek professional financial stewardship, and this transfer is occurring alongside the continued aging of the population that increases reliance on retirement income planning, tax optimization, estate structuring, and longevity risk management services across affluent households. The demographic shift is amplified by rising life expectancy and the maturation of defined contribution pension systems that place greater responsibility for retirement outcomes on individuals, leading families to adopt advisory relationships earlier and retain them across life stages. High net worth households are increasingly engaging advisors not only for investment performance but also for intergenerational governance, philanthropic structuring, and cross-border inheritance planning, which expands advisory scope and revenue pools across planning, trust, and portfolio mandates. Financial institutions have strengthened dedicated wealth transfer propositions including family office-style services, next-generation financial education programs, and consolidated reporting across family entities, reinforcing long-term client retention. As wealth recipients often prefer managed and discretionary solutions rather than transactional brokerage, assets migrate into fee-based mandates that deepen advisor engagement and stabilize revenue models. The scale of wealth held by older cohorts within Canada’s financial system ensures a sustained pipeline of advisory demand, particularly in urban wealth centers where private capital, real estate wealth, and business ownership converge. Estate complexity arising from business succession, cross-jurisdiction assets, and tax exposure further necessitates professional wealth management structures, making advisory services integral to wealth continuity strategies. These demographic and structural forces collectively underpin durable growth in managed assets and advisory penetration across the Canadian wealth management ecosystem.

Shift Toward Fee-Based Advisory and Discretionary Portfolio Mandates

Canada wealth management market is undergoing a structural transformation from commission-driven brokerage toward recurring fee-based advisory and discretionary portfolio models as investors prioritize transparency, alignment of incentives, and comprehensive planning over transaction-oriented relationships, and regulatory frameworks have reinforced this shift by emphasizing suitability, fiduciary standards, and client-focused reforms across the financial advisory sector. Investors increasingly prefer integrated wealth propositions that combine investment management, financial planning, tax coordination, and risk profiling within unified mandates, which naturally favors discretionary and managed account structures operated by institutional platforms with advanced portfolio infrastructure. Large financial institutions have invested heavily in portfolio construction engines, model portfolios, digital reporting, and centralized investment oversight that enable scalable discretionary services across advisor networks, enhancing consistency and performance monitoring while reducing operational complexity. Advisors benefit from stable recurring revenues and reduced compliance burden compared with transaction-based models, encouraging migration of client assets into managed mandates across both mass affluent and high net worth segments. Clients also gain behavioral and governance advantages as discretionary mandates reduce emotional trading, ensure disciplined asset allocation, and embed long-term financial planning into investment decisions. The availability of risk-graded model portfolios and goals-based frameworks further simplifies onboarding and suitability processes, accelerating adoption across diverse investor cohorts. This structural evolution expands managed asset pools, deepens advisory relationships, and strengthens platform economics for wealth institutions operating in Canada.

Challenges

Regulatory Compliance Burden and Fiduciary Accountability Expansion

Canada wealth management market faces escalating regulatory expectations requiring firms to demonstrate suitability, transparency, conflict management, and ongoing client outcome monitoring across advisory relationships, significantly increasing compliance costs, documentation requirements, and operational oversight complexity for both large institutions and independent advisors operating within the national financial framework. Client-focused reforms mandate detailed disclosure of fees, performance reporting, and product suitability assessments that require advanced compliance systems, advisor training, and supervisory structures, particularly challenging for smaller firms lacking scale resources. Cross-border tax reporting obligations, anti-money laundering controls, and know-your-client verification standards add further layers of regulatory scrutiny that lengthen onboarding processes and increase administrative overhead. Wealth platforms must maintain robust surveillance, audit trails, and reporting frameworks to satisfy regulators, creating continuous technology investment requirements and governance burdens. Advisors also face heightened liability exposure for investment recommendations and planning advice, necessitating conservative portfolio construction and extensive documentation that can constrain flexibility. Regulatory divergence across provinces and international jurisdictions complicates cross-border wealth management for globally mobile clients, increasing advisory complexity. Compliance-driven cost structures may compress margins or be passed to clients, affecting competitiveness. These expanding regulatory obligations create structural barriers to entry and operational strain across the Canadian wealth management landscape.

Fee Compression and Competitive Pricing Pressure Across Advisory Models

Canada wealth management market is experiencing sustained downward pressure on advisory fees as competition intensifies among bank-owned platforms, independent firms, and digital advisory providers offering low-cost portfolio management and automated investment services, forcing traditional advisors to justify pricing through differentiated planning and holistic wealth propositions rather than investment selection alone. Institutional model portfolios, exchange-traded funds, and passive investment strategies have reduced the cost of portfolio construction, leading clients to question high advisory fees unless accompanied by demonstrable value in tax, estate, or financial planning outcomes. Digital platforms and robo-advisors provide diversified portfolios at minimal cost, setting benchmark expectations for price transparency and service efficiency that influence broader market pricing structures. Large institutions leverage scale to offer competitive fees while maintaining profitability, placing smaller independent advisors at disadvantage due to higher relative operating costs. Client awareness of fees and performance comparisons has increased due to regulatory disclosure requirements, intensifying price sensitivity across affluent segments. Advisors must invest in technology, reporting, and planning capabilities to retain clients, raising cost bases while revenue margins narrow. Competitive fee compression pressures consolidation as firms seek scale efficiencies and integrated product manufacturing to sustain profitability. These dynamics collectively challenge traditional advisory economics across Canada.

Opportunities

Expansion of Hybrid Digital-Human Advisory Models Across Mass Affluent Segment

Canada wealth management market has substantial growth potential through scalable hybrid advisory models that combine automated portfolio construction with human financial planning guidance, enabling institutions to profitably serve the large and underserved mass affluent population whose investable assets fall below traditional private wealth thresholds yet require structured retirement, tax, and investment support within Canada’s evolving savings landscape. Hybrid platforms allow clients to access diversified portfolios, goals-based planning tools, and digital reporting at low cost while retaining access to advisors for complex decisions, improving engagement and affordability simultaneously. Financial institutions can extend advisory coverage without proportional advisor headcount expansion by leveraging centralized portfolio engines and digital onboarding. Mass affluent households increasingly accumulate retirement savings through defined contribution plans and personal investment accounts, creating demand for affordable managed solutions beyond self-directed brokerage. Hybrid models also support life-stage transitions such as home ownership, education planning, and retirement decumulation, embedding long-term relationships that may later migrate into full private wealth services as assets grow. Data analytics and personalization algorithms enhance client targeting and portfolio suitability, improving outcomes and retention. Regulatory acceptance of digital advice frameworks further legitimizes hybrid delivery models. These scalable advisory architectures represent a major expansion pathway within Canada’s wealth management ecosystem.

Growth of ESG and Sustainable Investment Advisory Integration

Canada wealth management market is positioned to capture expanding demand for environmental, social, and governance aligned investment strategies as investors increasingly seek portfolios reflecting sustainability preferences, responsible ownership principles, and climate transition considerations, and institutional managers across Canada have developed ESG integration frameworks, thematic funds, and impact investment solutions that advisors can incorporate into client mandates across discretionary and advisory portfolios. Affluent investors demonstrate strong interest in aligning wealth with values, including low-carbon strategies, social impact investments, and governance-screened portfolios, requiring advisory expertise in sustainability metrics, reporting, and product selection. Wealth institutions have expanded ESG research capabilities, stewardship programs, and sustainable product shelves that enable advisors to construct diversified ESG portfolios without sacrificing risk management. Regulatory initiatives promoting climate disclosure and sustainable finance standards reinforce credibility and transparency of ESG investments, supporting adoption across institutional and retail wealth segments. Advisors can differentiate through values-based planning and sustainability reporting integrated with financial goals, enhancing engagement and retention among younger investors. ESG portfolios also support intergenerational wealth continuity as heirs prioritize responsible investment philosophies. The institutionalization of sustainable investing across Canadian asset managers ensures long-term availability of ESG solutions. These dynamics create enduring opportunity for ESG-integrated advisory growth.

Future Outlook

Canada wealth management market is expected to expand steadily driven by demographic wealth transfer, continued accumulation of financial assets, and deeper advisory penetration across mass affluent and high net worth segments. Digital hybrid advisory platforms will scale distribution while artificial intelligence enhances portfolio personalization and reporting. Regulatory frameworks emphasizing transparency and fiduciary duty will strengthen client trust and professionalization of advisory services. ESG integration and cross-border wealth structuring will broaden advisory scope. Consolidation among institutions will continue shaping competitive dynamics.

Major Players

- RBC Wealth Management

- TD Wealth

- BMO Wealth Management

- Scotiabank Wealth Management

- CIBC Private Wealth

- National Bank Financial Wealth Management

- CI Financial

- iA Private Wealth

- Manulife Wealth

- Sun Life Global Investments

- Mackenzie Investments

- Fidelity Canada

- IG Wealth Management

- Raymond James Ltd Canada

- Canaccord Genuity Wealth Management

Key Target Audience

- Private banks

- Asset management firms

- Family offices

- Pension funds

- Insurance companies

- Investment and venture capitalist firms

- Government and regulatory bodies

- High-net-worth investor networks

Research Methodology

Step 1: Identification of Key Variables

Core market variables including assets under management, advisory penetration, investor demographics, regulatory structure, and platform distribution were identified through financial sector datasets and institutional disclosures. These variables define market boundaries and structural drivers across Canada wealth management ecosystem.

Step 2: Market Analysis and Construction

The market framework was constructed by integrating asset pools, advisory models, platform types, and client segments to map value flows across institutions and investor cohorts. Historical financial statistics and institutional reports informed segmentation and structural relationships.

Step 3: Hypothesis Validation and Expert Consultation

Industry hypotheses on growth drivers, challenges, and opportunities were validated through expert viewpoints from wealth advisors, portfolio managers, and financial sector analysts. Regulatory publications and industry associations provided cross-verification of structural trends.

Step 4: Research Synthesis and Final Output

All validated insights were synthesized into a coherent market narrative integrating quantitative asset context with qualitative structural dynamics. Final outputs align segmentation, competitive landscape, and strategic outlook within Canada wealth management market framework.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising High Net Worth Population in Canada

Intergenerational Wealth Transfer Expansion

Growing Demand for Personalized Advisory - Market Challenges

Fee Compression and Margin Pressure

Regulatory Compliance Complexity

Talent Shortage in Advisory Roles - Market Opportunities

Expansion of Digital Hybrid Advisory Models

ESG and Sustainable Investment Advisory Growth

Cross-border Wealth Structuring Demand - Trends

Shift Toward Goals-based Wealth Planning

Integration of AI in Portfolio Construction

Consolidation Among Advisory Firms - Government Regulations & Defense Policy

Client-focused Reforms and Fiduciary Standards

Enhanced AML and KYC Requirements

Cross-border Tax Compliance Frameworks - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Discretionary Portfolio Management

Advisory Brokerage Services

Financial Planning and Retirement Advisory

Alternative Investment Advisory

Estate and Trust Planning Services - By Platform Type (In Value%)

Bank-affiliated Wealth Platforms

Independent Advisory Firms

Digital Robo-advisory Platforms

Family Office Platforms

Hybrid Advisory Platforms - By Fitment Type (In Value%)

On-premise Advisory Systems

Cloud-based Wealth Platforms

Hybrid Wealth Management Systems

Modular Advisory Tools

Integrated End-to-End Platforms - By End User Segment (In Value%)

High Net Worth Individuals

Ultra High Net Worth Individuals

Mass Affluent Clients

Institutional and Pension Clients

Family Offices - By Procurement Channel (In Value%)

Direct Advisory Engagement

Private Banking Channels

Brokerage and Dealer Networks

Digital Direct Platforms

Third-party Financial Intermediaries

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (Product Breadth, Advisory Model, AUM Tier Focus, Fee Structure, Digital Platform Capability)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

RBC Wealth Management

TD Wealth

BMO Wealth Management

Scotiabank Wealth Management

CIBC Private Wealth

National Bank Financial Wealth Management

CI Financial

iA Private Wealth

Manulife Wealth

Sun Life Global Investments

Mackenzie Investments

Fidelity Canada

IG Wealth Management

Raymond James Ltd Canada

Canaccord Genuity Wealth Management

- High Net Worth clients increasingly demand holistic wealth planning and tax optimization

- Ultra wealthy families adopt family office structures and alternative assets

- Mass affluent segment shifts toward hybrid and digital advisory channels

- Institutional clients seek customized liability-driven investment solutions

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now