Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Europe baby care products market was valued at USD ~ billion in 2025 in a public Europe market estimate, while the adjacent Europe baby toiletries market was valued at USD 33,282.9 million in 2024, showing the scale of recurring spend on hygiene-led categories. Demand is being supported by premiumization, ingredient sensitivity, and routine-use products such as lotions, washes, shampoos, and diaper-care items, even as the EU birth base moved from 3.67 million births to 3.55 million births across the latest two reported years.

Germany, the UK, France, Italy, and Spain remain the most influential countries because they combine large retail footprints, strong pharmacy and drugstore channels, higher penetration of premium baby care, and well-developed e-commerce ecosystems. Public country datapoints show the Germany baby toiletries market at USD 5,842.8 million and the UK at USD 4,276.9 million in 2024, while France continues to stand out demographically because it remains among the EU’s higher-fertility large markets, supporting replacement demand for baby skin and hair care products.

Market Segmentation

By Product Type

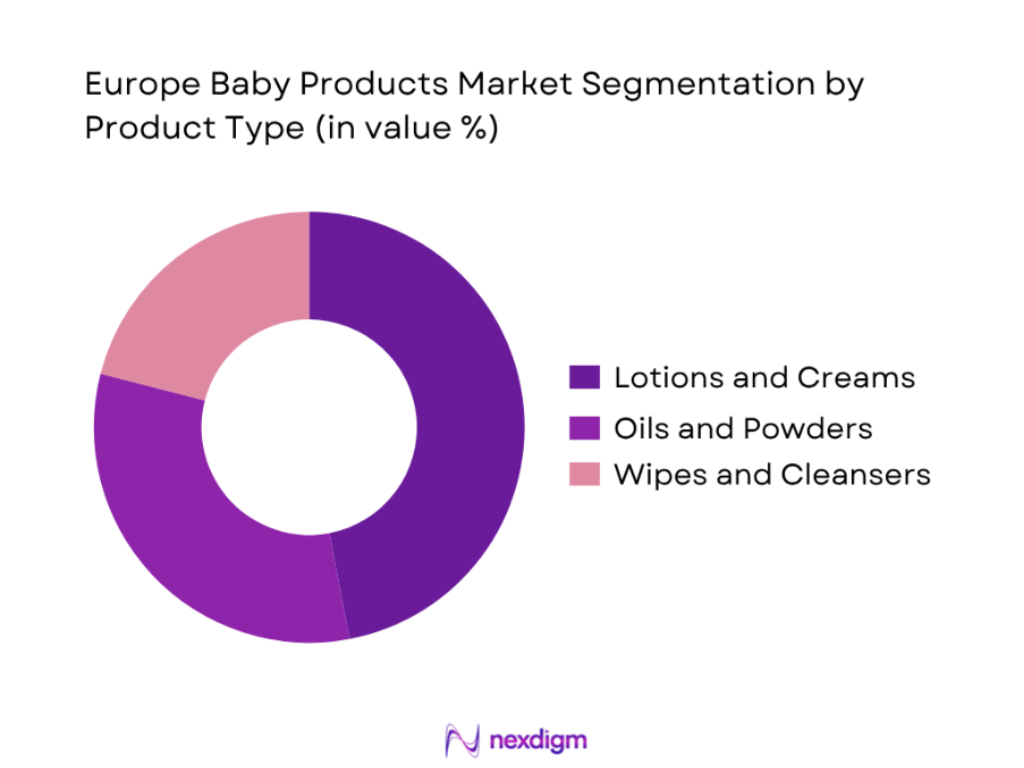

The Europe baby care products market, with a strong focus on skin care and hair care, is segmented by product type into lotions and creams, oils and powders, and wipes and cleansers. Lotions and creams currently dominate because they address the widest set of routine infant-care needs, including moisturization, barrier support, dryness relief, post-bath care, and daily skin protection. In Europe, this dominance is reinforced by parents’ preference for fragrance-free, hypoallergenic, dermatologist-tested, and organic-positioned formulations. Creams also benefit from higher average selling prices than basic cleansers and from broader usage occasions across newborn care, rash prevention, winter dryness, and sensitive-skin routines. They perform especially well in pharmacy-led and premium retail environments, where parents are more willing to trade up for safety, efficacy, and trust-backed formulations. That is why lotions and creams remain the core revenue engine within skin-focused baby care.

By Distribution Channel

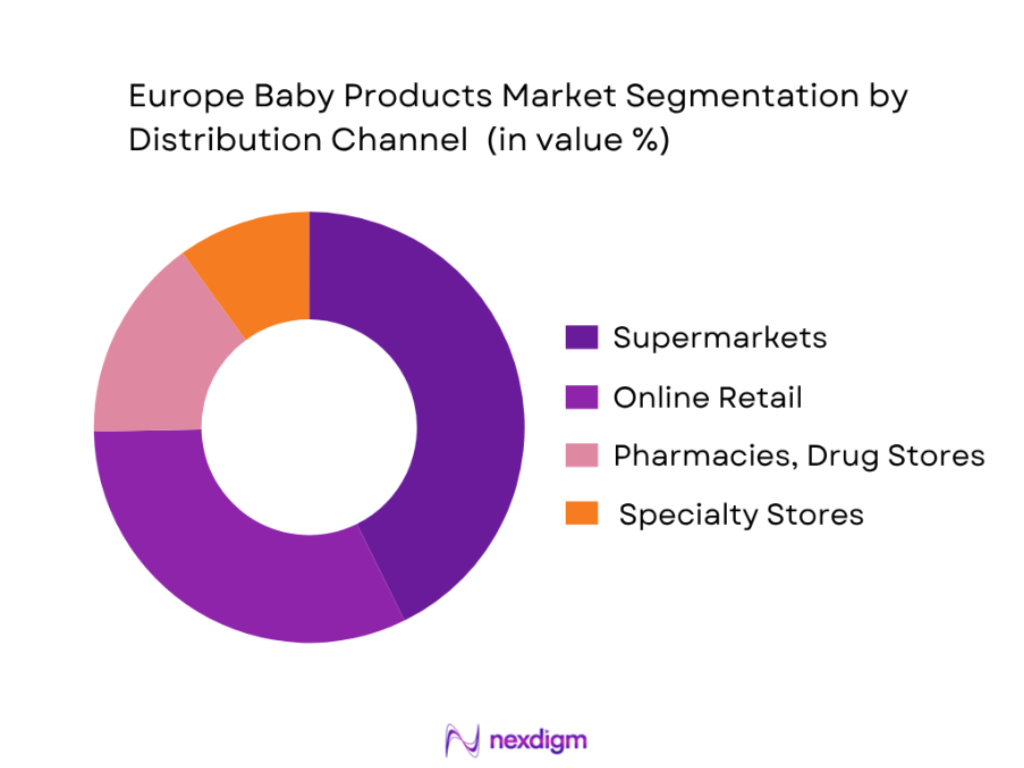

The Europe baby care products market is segmented by distribution channel into supermarkets and hypermarkets, online retail, pharmacies and drug stores, and specialty stores. Supermarkets and hypermarkets dominate because they combine convenience, wide assortment, promotional visibility, and routine grocery footfall. For baby skin care and hair care, this matters because a large part of demand is replenishment-led rather than occasional. Parents often buy shampoos, washes, lotions, and diaper creams alongside household essentials, making one-stop retail highly effective. Large-format chains also support strong shelf visibility for multinational brands and private labels, which is important in a category where packaging cues, ingredients, and price-pack architecture influence purchase. Although online retail is expanding quickly, physical grocery-led retail still holds the advantage in impulse replenishment, trust, and immediate product availability, especially for core skincare and bath-time essentials.

Competitive Landscape

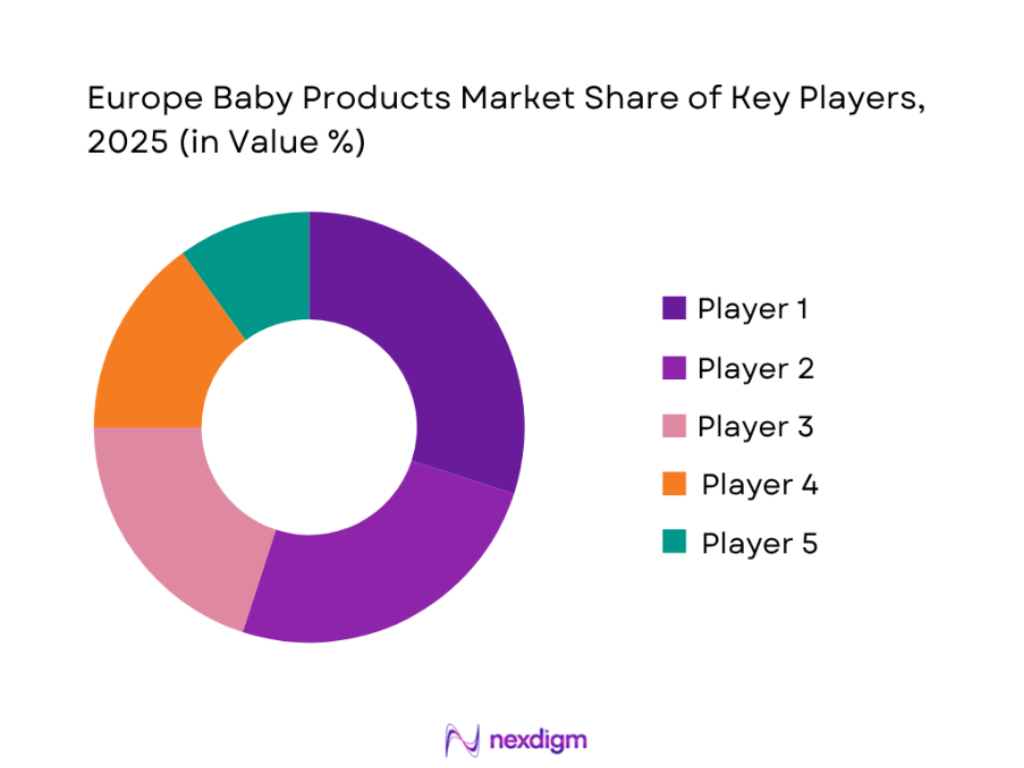

The Europe baby care products market is moderately concentrated, with a mix of global consumer-health groups, dermocosmetic specialists, natural-personal-care brands, and parenting-focused companies. In skin care and hair care specifically, competitive strength is shaped less by sheer scale alone and more by dermatology credibility, pharmacy access, gentle-ingredient positioning, and the ability to extend into daily-use regimes such as wash, lotion, cream, oil, and shampoo. Johnson’s Baby, Mustela, Weleda, Chicco, and PZ Cussons are among the most visible names because they combine broad baby-care portfolios with strong parent trust, established retail presence, and differentiated brand propositions across mass, premium, and sensitive-skin segments.

| Company | Established | Headquarters | Key Baby Skin/Hair Care Brand | Core Category Strength | Positioning | Channel Strength | Europe Manufacturing / Operating Footprint | Distinctive Market Lever |

| Kenvue | 2022 | Summit, New Jersey, U.S. | – | – | – | – | – | – |

| Laboratoires Expanscience | 1950 | Paris La Défense, France | – | – | – | – | – | – |

| Weleda | 1921 | Arlesheim, Switzerland | – | – | – | – | – | – |

| Artsana Group | 1946 | Grandate, Italy | – | – | – | – | – | – |

| PZ Cussons | 1884 | Manchester, UK | – | – | – | – | – | – |

Europe Baby Product Market Analysis

Growth Drivers

Premiumization of Infant Nutrition, Baby Care, and Mobility Products

Europe’s baby products market is being pushed upward by premiumization because parents are having fewer children but spending more intentionally per child. The EU recorded 3.55 million live births and a total fertility rate of 1.34 in 2024, while the average age at first birth reached 29.9 years, pointing to later and often more planned parenthood. At the same time, the EU population stood at 449.3 million on 1 January 2024, EU GDP reached USD 19.5 trillion in 2024, and GDP per capita reached USD 43,305, supporting stronger spending power in higher-income households. This combination benefits premium infant formula, sensitive-skin baby care, and higher-spec mobility products such as travel systems and safer car-seat formats because demand increasingly comes from smaller but more value-conscious family units rather than volume-led baby cohorts.

Rising Demand for Organic, Clean-Label, and Sensitive-Skin Baby Products

Demand for organic, clean-label, and sensitive-skin baby products is rising because Europe’s regulatory and consumer environment increasingly rewards ingredient transparency and low-risk formulations. The European cosmetics market generated €104 billion in retail sales in 2024, showing the scale of consumer willingness to spend on quality-led personal care. On the supply side, the share of EU utilised agricultural area under organic farming reached 11.0 in 2023, underscoring the broader regional shift toward certified and traceable inputs. On the safety side, 4,137 Safety Gate alerts were recorded in 2024, with cosmetics accounting for 36 of all alerts and chemical risks for 49, which reinforces parent preference for baby products positioned around fragrance-free, hypoallergenic, and tightly regulated formulations. In practice, this strengthens premium baby skin care, baby toiletries, and formula products that communicate purity, allergen control, and compliance more clearly than mass offerings.

Market Challenges

Declining Fertility and Live Birth Base Across Several European Countries

The biggest structural challenge for Europe’s baby products market is that the addressable newborn base is shrinking. The EU recorded 3.55 million births in 2024 and a total fertility rate of 1.34, the lowest level in the current Eurostat series. The range across countries is also wide, from 1.01 in Malta to 1.72 in Bulgaria, showing that demographic momentum is uneven across the region. In several of Europe’s largest consumer markets, fertility is particularly soft: Spain recorded 1.10, while Italy recorded 31.9 years as the average age at first birth, indicating continued postponement of parenthood. For the baby products industry, this means many categories cannot rely on population-led volume growth. Companies need to offset the smaller birth cohort through premiumization, greater spend per child, and stronger replenishment models in diapers, formula, skin care, and baby hygiene.

Regulatory Complexity Across Nutrition, Cosmetics, Toy Safety, and General Product Safety

Europe remains one of the most compliance-intensive baby product markets in the world. On the cosmetics side, only products with an EU-based responsible person can be placed on the market, and notification through the CPNP is mandatory. On the product-safety side, the General Product Safety Regulation became applicable on 13 December 2024, changing obligations for traceability, recalls, and online marketplace accountability. The compliance burden is reinforced by enforcement outcomes: the EU recorded 4,137 Safety Gate alerts in 2024, the highest on record, and cosmetics represented 36 of all alerts while chemical risk represented 49. For baby product suppliers that sell formula, baby skin care, toys, feeding accessories, and nursery gear across multiple EU countries, the result is a higher operational load in testing, documentation, labeling, authorized representation, and post-market surveillance.

Market Opportunities

White Space in Specialist Formula, Goat Milk, Plant-Forward, and Allergy-Sensitive Nutrition

A meaningful opportunity exists in specialist baby nutrition because Europe combines a regulated infant-food system with a parent base that is increasingly attentive to ingredient sensitivity. The EU still recorded 3.55 million births in 2024, and 23.5 out of every 100 households included children, giving specialist infant nutrition a substantial consumer base even in a lower-birth environment. Regulation also supports category sophistication: infant and follow-on formula in the EU is governed by dedicated compositional and labeling rules under Regulation 2016/127, while foods for infants and young children remain part of the EU’s foods-for-specific-groups framework. On the demand side, the European Academy of Allergy and Clinical Immunology stated in a 2024 advocacy document that more than 150 million Europeans live with chronic allergic diseases. That broader allergy burden strengthens the commercial logic for goat milk, allergy-sensitive, digestive-comfort, and cleaner-label infant nutrition products positioned around tolerance, reassurance, and precise regulatory compliance.

Premium Diapering with Bio-Based Materials and Dermatology Positioning

Premium diapering has room to grow because Europe’s sustainability agenda and skincare consciousness are moving closer together. The EU generated 517 kg of municipal waste per person in 2024 and recycled 248 kg per person, while the PPWR entered into force on 11 February 2025 and begins applying from 12 August 2026. At the same time, the safety environment keeps chemical scrutiny high: in 2024 the EU recorded 4,137 Safety Gate alerts, with chemical risk accounting for 49. These conditions favor diaper brands that move beyond absorption and leakage claims toward lower-plastic formats, fiber innovation, and dermatology-oriented positioning for rash prevention and skin-barrier protection. The opportunity is especially strong because diapers are high-frequency purchases; even modest shifts toward bio-based materials, refill-oriented formats, or skin-health claims can create meaningful category value. In Europe, premium diapering can therefore win both through sustainability compliance and through skin-wellness differentiation.

Future Outlook

The Europe baby care products market is expected to expand steadily over the long term, with skin care and hair care remaining among the most innovation-intensive parts of the category. Growth is likely to come less from volume expansion and more from premiumization, ingredient transparency, higher repeat purchases in sensitive-skin routines, and wider uptake of dermatologist-led and organic-positioned products. Online discovery, refill formats, eco-conscious packaging, and pharmacy-backed recommendations should continue to influence category development. At the same time, brands will need to offset slower birth trends through higher spend per child, improved regimen building, and stronger omnichannel execution.

Major Players

- Kenvue (Johnson’s Baby)

- Laboratoires Expanscience (Mustela)

- Weleda

- Artsana Group (Chicco)

- PZ Cussons

- Beiersdorf (NIVEA Baby)

- Unilever

- Procter & Gamble

- Pierre Fabre

- Sebapharma

- Bübchen

- Sanosan

- NAÏF Care

- Biolane

- Childs Farm

Key Target Audience

- Baby skin care and hair care manufacturers

- Private label baby personal care companies

- Supermarkets and hypermarket chains

- Pharmacy and drugstore chains

- Specialty baby retail chains and e-commerce platforms

- Ingredients, packaging, and contract manufacturing companies

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

The first step involves building the market ecosystem for Europe baby care products, with specific attention to skin care and hair care. This includes mapping manufacturers, brand owners, private labels, pharmacies, grocery chains, online retailers, and regulators. The objective is to identify the variables that most directly influence category value, including birth trends, premiumization, sensitive-skin demand, retail mix, and ingredient-led differentiation.

Step 2: Market Analysis and Construction

In this phase, historical market information is compiled from public industry datasets and open market reports. The Europe market size anchor is validated against adjacent category estimates such as baby toiletries, country-level benchmarks for Germany and the UK, and category-growth indicators showing skin care as the most attractive subsegment. This step supports a bottom-up and top-down triangulation of market direction.

Step 3: Hypothesis Validation and Expert Consultation

The next phase tests market hypotheses around dominant products, route-to-market structure, pricing tiers, and demand drivers. These hypotheses are checked against public evidence from brand portfolios, retail channel trends, product-segment studies, and country demand patterns. In a full commercial study, these would be further validated through interviews with distributors, category managers, pediatric dermatology stakeholders, and baby-care brand executives.

Step 4: Research Synthesis and Final Output

The final stage consolidates the demand-side, supply-side, and competitive inputs into an actionable market view. The synthesis focuses on what matters most for business decisions: market size, growth path, dominant subsegments, competitive positioning, channel strategy, and future whitespace in skin care and hair care. The result is a market narrative designed for strategic planning, expansion assessment, portfolio prioritization, and investment screening.

- Executive Summary

- Research Methodology (Market Definitions and Scope, Assumptions and Limitations, Abbreviations, Bottom-Up Market Estimation, Top-Down Validation, Country-Level Demand Mapping, Pricing Benchmarking Framework, Brand and SKU Mapping, Channel Intelligence Framework, Consumer Cohort Analysis, Expert Interviews with Retailers/Distributors/Brands/Dermatology Stakeholders, Forecasting Model, Sensitivity Analysis)

- Definition and Scope

- Category Genesis and Evolution in Europe

- Parent Purchase Journey Across Skin and Hair Care

- Baby Personal Care Value Chain Analysis

- Industry Ecosystem and Stakeholder Map

- Demand Structure by Birth Base, Premiumization, and Household Consumption

- Role of Safety, Trust, Ingredient Transparency, and Dermatology Positioning

- Country-Level Consumption and Route-to-Market Differences

- Import Dependence, Local Manufacturing, and Private Label Penetration

- Regulatory and Claims Environment Across Baby Cosmetic Products

- By Value, 2020-2025

- By Volume, 2020-2025

- By Average Selling Price, 2020-2025

- By Branded vs Private Label, 2020-2025

- By Domestic Production vs Imports, 2020-2025

Europe Baby Skin Care Segmentation

- By Product Type (In Value %)

Baby Lotion

Baby Cream

Baby Oil

Baby Powder / Powder Alternatives

Diaper Rash Cream / Nappy Cream

Baby Wash and Bath Products

Baby Soap and Syndet Bars

Baby Sunscreen and Outdoor Protection

Baby Massage and Comfort Oils

Specialized Eczema / Sensitive-Skin Care Products - By Skin Type / Need State (In Value %)

Normal Skin Care

Sensitive Skin Care

Dry Skin Care

Atopy-Prone / Eczema-Prone Skin Care

Barrier Repair and Dermatology-Led Skin Care - By Ingredient Positioning (In Value %)

Natural / Botanical-Based

Organic Certified

Hypoallergenic

Fragrance-Free

Preservative / Paraben-Free Positioning

Vegan / Plant-Based

Dermatologist-Tested / Clinically Positioned - By Price Positioning (In Value %)

Mass Market

Mid-Premium

Premium

Organic / Clean Beauty Premium

Clinical / Dermatology Premium - By Distribution Channel (In Value %)

Supermarkets and Hypermarkets

Pharmacies and Drugstores

Specialty Baby Stores

E-commerce Marketplaces

Brand-Owned Websites / D2C

Department Stores and General Merchandise Retailers - By Packaging Format (In Value %)

Bottles

Tubes

Pump Dispensers

Jars / Tubs

Sachets / Trial Packs

Refill Packs

Travel and On-the-Go Packs - By Country / Region Cluster (In Value %)

Germany

United Kingdom

France

Italy

Spain

Benelux

Nordics

Central and Eastern Europe

Rest of Europe

Europe Baby Skin Care Market Analysis

- Growth Drivers

Rising Demand for Sensitive-Skin and Hypoallergenic Baby Skin Care

Premiumization in Dermatology-Led and Natural Baby Care

Growth of Pharmacy and Drugstore-Led Trusted Distribution

Increasing Penetration of Organic, Fragrance-Free, and Clean-Label Formulations

E-commerce Expansion and Parent Review-Led Discovery

Higher Spend per Child in Core Skin Protection Categories

Innovation in Barrier Repair, Microbiome-Friendly, and Atopy-Oriented Products - Market Challenges

Declining Births Across Several European Markets

Ingredient Scrutiny and Claims Substantiation Complexity

Margin Pressure from Private Label and Retail Promotions

Regulatory Compliance Burden Across Formulation, Labelling, and Safety Files

Consumer Skepticism Toward Harsh Chemicals and Synthetic Fragrances

Fragmented Country Preferences in Texture, Pack Size, and Ingredient Positioning - Market Opportunities

White Space in Clinical Baby Skin Care for Eczema-Prone and Atopy-Prone Babies

Refill and Low-Plastic Packaging Formats

Premium Daily-Moisture Regimens and Gifting Bundles

D2C Subscription Models for Repeat Skin Care Essentials

Expansion of Natural and Organic Positioning in Central and Eastern Europe

Cross-Selling Through Baby Bath, Rash, and Moisture Regimes - Trends

Shift Toward Minimal-Ingredient and Fragrance-Free Formulations

Growth of Dermatologist-Tested and Pediatrician-Recommended Claims

Rising Preference for Eco-Conscious Packaging and Ecolabel Relevance

Stronger Demand for Rash Prevention and Skin Barrier Support

Premium Bundling of Lotion, Wash, Cream, and Oil Regimens - Regulatory Landscape

EU Cosmetic Product Safety and Responsible Person Requirements

Ingredient Safety Assessment and SCCS Guidance Relevance

Claims Governance for Sensitive Skin, Hypoallergenic, Natural, and Organic Positioning

Packaging, Sustainability, and Ecolabel Considerations

Country-Level Retail and Product Notification Compliance - PESTLE Analysis

- SWOT Analysis

- Porter’s Five Forces Analysis

- Stakeholder Ecosystem

- Innovation and Product Development Pipeline

- Import-Export and Sourcing Trends

- Shelf-Space and Assortment Analysis

- White Space Assessment by Country and Channel

Europe Baby Skin Care Competitive Intelligence

- Market Share of Major Players by Value

Market Share of Major Players by Volume

Market Share of Major Players by Product Type

Market Share of Major Players by Country Cluster

Brand Positioning Map - Cross Comparison Parameters (Company Overview, Product Portfolio Breadth, Sensitive-Skin / Clinical Positioning, Natural / Organic Credentials, Price Tier Presence, Pharmacy and Drugstore Reach, E-commerce Visibility, Innovation Pipeline, Manufacturing Footprint, Packaging Formats, Sustainability Positioning, Brand Trust, Promotional Strategy, Distribution Partnerships, Unique Value Proposition)

- SWOT Analysis of Major Players

- Pricing Benchmarking by SKU and Pack Size

- New Product Launch and Claims Benchmarking

- Packaging and Claims Intelligence

- Detailed Profiles of Major Companies

Johnson & Johnson

Beiersdorf (NIVEA Baby)

Laboratoires Expanscience (Mustela)

Weleda

Unilever

Procter & Gamble

PZ Cussons

Chicco (Artsana Group)

Kenvue

Pierre Fabre

Sanosan

Bübchen

Sebapharma

Biolane

NAÏF Care

Europe Baby Hair Care Segmentation

- By Product Type (In Value %)

Baby Shampoo

Baby 2-in-1 Shampoo and Body Wash

Baby Conditioner

Detangling Spray / Leave-In Care

Scalp Oil and Scalp Moisturizers

Cradle Cap Care Products

Anti-Lice / Preventive Hair Care Products

Styling and Grooming Aids for Infants and Toddlers - By Hair / Scalp Need State (In Value %)

Everyday Mild Cleansing

Sensitive Scalp Care

Dry Scalp and Moisture Care

Cradle Cap Management

Tear-Free Gentle Wash Products - By Ingredient Positioning (In Value %)

Natural / Botanical-Based

Organic Certified

Sulfate-Free / Mild Surfactant Positioning

Fragrance-Free

Hypoallergenic

Vegan / Plant-Based

Dermatologist-Tested / Clinically Positioned - By Price Positioning (In Value %)

Mass Market

Mid-Premium

Premium

Organic / Clean Beauty Premium

Clinical / Dermatology Premium - By Distribution Channel (In Value %)

Supermarkets and Hypermarkets

Pharmacies and Drugstores

Specialty Baby Stores

E-commerce Marketplaces

Brand-Owned Websites / D2C

Department Stores and General Merchandise Retailers - By Packaging Format (In Value %)

Bottles

Pump Bottles

Flip-Top Bottles

Tubes

Refill Packs

Travel and Trial Packs - By Country / Region Cluster (Birth Rate, Pharmacy Channel Strength, Premiumization, Hair Care Routine Maturity, E-commerce Penetration) (In Value %)

Germany

United Kingdom

France

Italy

Spain

Benelux

Nordics

Central and Eastern Europe

Rest of Europe

Europe Baby Hair Care Market Analysis

- Growth Drivers

Rising Preference for Tear-Free and Mild-Cleansing Hair Care Products

Expansion of Sulfate-Free, Fragrance-Free, and Sensitive-Scalp Positioning

Premiumization of Natural and Organic Baby Shampoo and Scalp Care

Stronger Online Discovery of Niche and Specialist Hair Care Brands

Increasing Demand for Cradle Cap and Scalp-Specific Solutions

Growth in Multipurpose Wash Formats for Convenience-Oriented Parents - Market Challenges

Lower Purchase Frequency Versus Baby Skin Care

High Private Label Competition in Everyday Shampoo Formats

Limited Consumer Willingness to Spend on Non-Essential Hair SKUs

Regulatory and Claims Validation Complexity

Fragmented Preferences Across Fragrance, Foam, and Texture Profiles - Market Opportunities

White Space in Sensitive-Scalp and Cradle Cap-Focused Premium Solutions

Organic Baby Hair Care Expansion in Specialist and Pharmacy Channels

Cross-Selling of Shampoo with Wash, Lotion, and Scalp Oil Regimens

Detangling, Curl-Friendly, and Toddler Hair Management Extensions

Eco-Refill and Family Pack Opportunities - Trends

Shift to Ultra-Mild Surfactants and Sulfate-Free Positioning

Growth of 2-in-1 Hair and Body Wash Formats

Increasing Fragrance-Free and Hypoallergenic Claims

Premium Scalp Care and Cradle Cap Solutions

Cleaner Label Messaging and Botanical Ingredient Storytelling - Regulatory Landscape

EU Cosmetics Safety and Product Information File Requirements

Ingredient Safety and Mild-Surfactant Positioning

Claims Governance for Tear-Free, Hypoallergenic, Sensitive Scalp, and Natural Claims

Packaging and Sustainability Compliance

Country-Level Notification and Retail Compliance Considerations - PESTLE Analysis

- SWOT Analysis

- Porter’s Five Forces Analysis

- Stakeholder Ecosystem

- Product Innovation and White Space Mapping

- Import-Export and Supply Dynamics

- Shelf-Space and Assortment Analysis

- White Space Assessment by Country and Channel

Europe Baby Hair Care Competitive Intelligence

- Market Share of Major Players by Value

Market Share of Major Players by Volume

Market Share of Major Players by Product Type

Market Share of Major Players by Country Cluster

Brand Positioning Map - Cross Comparison Parameters (Company Overview, Product Portfolio Breadth, Tear-Free / Mild Cleansing Positioning, Scalp Care Specialization, Natural / Organic Credentials, Price Tier Presence, Pharmacy and Drugstore Reach, E-commerce Visibility, Innovation Pipeline, Manufacturing Footprint, Packaging Formats, Sustainability Positioning, Brand Trust, Promotional Strategy, Distribution Partnerships, Unique Value Proposition)

- SWOT Analysis of Major Players

- Pricing Benchmarking by SKU and Pack Size

- New Product Launch and Claims Benchmarking

- Packaging and Claims Intelligence

- Detailed Profiles of Major Companies

Johnson & Johnson

Mustela

Chicco

Weleda

PZ Cussons

Unilever

Procter & Gamble

Kenvue

Sanosan

Bübchen

Sebapharma

Biolane

NAÏF Care

Beiersdorf

Pierre Fabre

- By Value, 2026-2035

- By Volume, 2026-2035

- By Average Selling Price, 2026-2035

- By Branded vs Private Label, 2026-2035

- By Domestic Production vs Imports, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now