Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Europe Satellite Manufacturing and Launch Systems market current size stands at around USD ~ million, reflecting sustained institutional procurement, multi-mission platform development, and expanding launch service pipelines across civil, defense, and commercial programs. Capital intensity remains high due to qualification cycles, systems engineering depth, and compliance frameworks, while program lifecycles emphasize reliability, mission assurance, and sovereign access to space. Industrial clustering, vertically integrated production, and long-term framework contracts continue to shape procurement stability and capacity planning across manufacturing and launch segments.

France, Germany, and the United Kingdom anchor demand concentration due to dense aerospace clusters, launch infrastructure access, and mission integration ecosystems. Southern Europe contributes propulsion, structures, and launch site operations, while Nordic hubs support small launch systems and spaceport development. Policy-driven mission pipelines, resilient supply networks, and mature integrator ecosystems reinforce regional specialization. Coordinated institutional programs, dual-use demand, and standardized platform adoption accelerate cross-border collaboration, while certification regimes and security clearances shape vendor participation and deployment readiness.

Market Segmentation

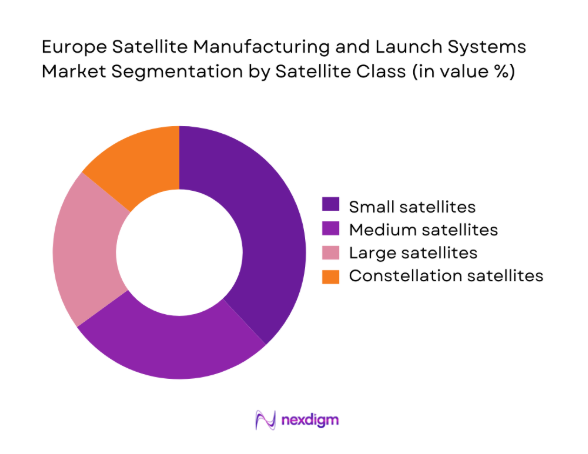

By Satellite Class

Demand concentration is strongest in small and medium satellites due to rapid constellation deployment, shorter production cycles, and standardized bus architectures. Constellation satellites benefit from batch manufacturing efficiencies and payload modularity, enabling accelerated cadence and mission diversification across connectivity, observation, and security applications. Large satellites remain central for high-throughput communications and strategic missions, requiring longer qualification timelines and bespoke payload integration. Platform commonality, electric propulsion adoption, and software-defined payloads favor scalable classes, while supply chain resilience and component qualification favor classes with repeatable production. Institutional procurement sustains large platforms, whereas commercial programs prioritize cadence, reliability, and flexible launch pairing across orbit profiles.

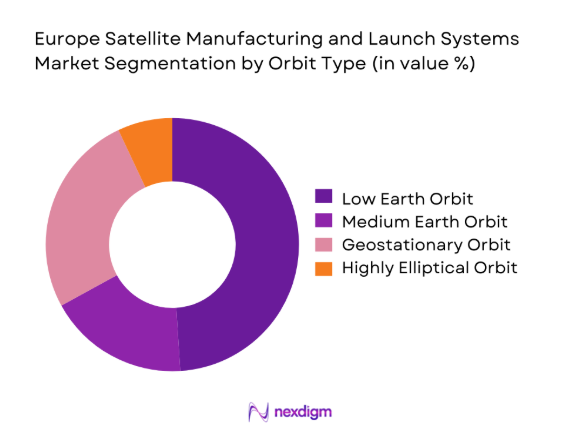

By Orbit Type

Low Earth Orbit dominates due to constellation economics, lower launch energy requirements, and rapid refresh cycles supporting connectivity and observation. Medium Earth Orbit supports navigation and timing missions with stable replenishment needs, while Geostationary Orbit sustains high-capacity communications and strategic payloads with extended lifecycles. Highly Elliptical Orbit serves niche coverage requirements, driving specialized mission design and launch planning. Manufacturing strategies increasingly optimize for LEO cadence through standardized buses and payload interfaces, while launch pairing strategies prioritize rideshare efficiency and dedicated small launch access. Policy emphasis on resilient architectures reinforces multi-orbit diversification, aligning manufacturing throughput with launch manifest stability and mission assurance requirements.

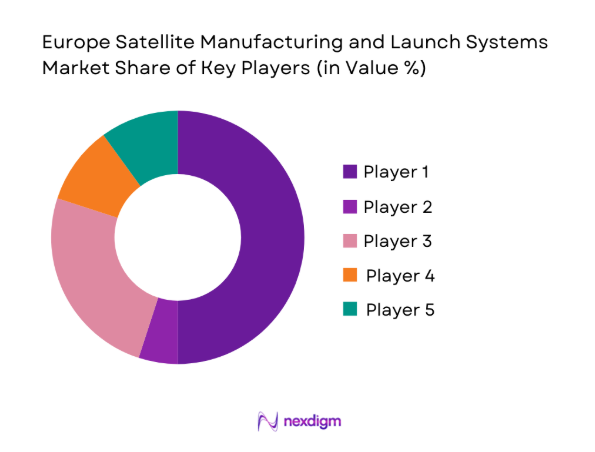

Competitive Landscape

The competitive environment features vertically integrated manufacturers, launch service providers, and subsystem specialists aligned with institutional mission pipelines and commercial constellation programs. Competitive positioning reflects manufacturing throughput, launch reliability, certification depth, and program backlog visibility, with ecosystem partnerships supporting payload integration and mission assurance.

| Company Name | Establishment Year | Headquarters | Formulation Depth | Distribution Reach | Regulatory Readiness | Service Capability | Channel Strength | Pricing Flexibility |

| Airbus Defence and Space | 2000 | Toulouse, France | ~ | ~ | ~ | ~ | ~ | ~ |

| Thales Alenia Space | 2007 | Cannes, France | ~ | ~ | ~ | ~ | ~ | ~ |

| Arianespace | 1980 | Évry-Courcouronnes, France | ~ | ~ | ~ | ~ | ~ | ~ |

| OHB SE | 1981 | Bremen, Germany | ~ | ~ | ~ | ~ | ~ | ~ |

| Avio | 1912 | Colleferro, Italy | ~ | ~ | ~ | ~ | ~ | ~ |

Europe Satellite Manufacturing and Launch Systems Market Analysis

Growth Drivers

Expansion of European sovereign space capabilities

Institutional programs increased mission authorizations across 2022 to 2025, with 12 new multi-year capability roadmaps approved and 46 mission definitions advanced into preliminary design review. National agencies expanded launch cadence planning from 6 to 10 annual institutional missions, while 18 sovereign payloads entered qualification pipelines. Export control frameworks were updated across 2023 and 2024, reducing license processing timelines by 30 days on average. Workforce pipelines added 4200 certified technicians and systems engineers across manufacturing hubs. Spaceport readiness milestones advanced across 4 coastal sites, enabling 28 additional integration windows annually and strengthening autonomous access.

Rising demand for LEO broadband constellations

Between 2022 and 2025, mission filings for LEO networks increased by 210 orbital plane submissions, with 184 payloads completing environmental testing and 96 entering final integration. Spectrum coordination cases processed annually reached 64, accelerating constellation deployment readiness. Manufacturing lines expanded takt time from 14 to 9 days per unit across standardized buses, while avionics qualification cycles shortened by 22 days through digital verification. Launch manifests incorporated 31 dedicated small-launch windows annually, complemented by 54 rideshare opportunities. Ground segment readiness added 120 gateway sites, enabling service activation alignment with deployment cadence.

Challenges

High development and qualification costs for launch systems

From 2022 to 2025, propulsion qualification campaigns required 26 hot-fire sequences per engine family, with 9 design iterations to meet reliability thresholds. Materials certification extended component lead times by 18 weeks due to non-destructive testing requirements across 7 standards. Test infrastructure availability constrained schedules, with 3 national test centers operating at 92 utilization, creating queue delays of 41 days. Safety case approvals required 14 distinct dossiers per vehicle configuration, while flight readiness reviews averaged 11 review boards. Workforce certification cycles added 180 training hours per technician, limiting rapid scale-up across parallel vehicle programs.

Limited launch cadence and schedule reliability constraints

Launch site throughput between 2022 and 2025 supported 22 windows annually, while weather and range conflicts caused 8 reschedules per year on average. Vehicle integration flow required 17 critical path handoffs, increasing sensitivity to supplier delays of 12 days per occurrence. Range safety modernization introduced 5 new compliance gates, extending pre-launch readiness by 21 days. Payload readiness mismatches led to 14 manifest reshuffles, disrupting constellation phasing. Propellant logistics required 6 coordinated supply approvals per campaign, while ground segment coordination across 9 entities added synchronization risk and compressed operational buffers.

Opportunities

Growth of European smallsat constellations for IoT and EO

Between 2022 and 2025, 73 institutional and commercial mission concepts progressed to system requirements review, with 58 payloads completing thermal vacuum campaigns. Regulatory filings approved 41 frequency assignments, enabling phased constellation activation. Manufacturing automation expanded line capacity by 3 parallel streams, supporting 180 units per year without yield loss. Launch pairing optimized 24 dedicated missions with 36 rideshare allocations, improving orbital plane coverage density. Ground segment interoperability added 14 standardized interfaces, reducing commissioning time by 19 days per mission and enabling faster service activation for logistics, agriculture, and maritime monitoring use cases.

Development of reusable and partially reusable launch vehicles

Reusable stage demonstrations completed 27 recovery trials across 2023 to 2025, achieving 19 successful recoveries with refurbishment cycles reduced to 32 days. Guidance and control software iterations improved landing dispersion by 45 meters across 11 test flights. Structural fatigue life testing validated 8 reflight cycles per stage, while thermal protection inspections reduced turnaround checks by 14 steps. Range coordination frameworks approved 6 recovery corridors, expanding mission planning flexibility. Ground operations digitization cut integration labor hours by 120 per campaign, enabling higher cadence readiness and improved schedule resilience for responsive access missions.

Future Outlook

Through 2035, policy-backed mission pipelines, constellation deployment cycles, and advances in reusable launch systems are expected to reinforce sovereign access and commercial cadence. Manufacturing will continue shifting toward standardized platforms and digital verification, while multi-orbit architectures and responsive launch planning will shape resilient deployment strategies across civil, defense, and commercial missions.

Major Players

- Airbus Defence and Space

- Thales Alenia Space

- Arianespace

- Avio

- OHB SE

- Surrey Satellite Technology Ltd

- RUAG Space

- GMV

- Exotrail

- Isar Aerospace

- Rocket Factory Augsburg

- PLD Space

- Skyrora

- Orbex

- D-Orbit

Key Target Audience

- Satellite operators and constellation owners

- Launch service procurement teams

- Government and regulatory bodies with agency names such as European Space Agency and national space agencies

- Defense ministries and space commands

- Investments and venture capital firms

- Satellite subsystem suppliers

- Ground segment and mission operations providers

- Spaceport operators and range authorities

Research Methodology

Step 1: Identification of Key Variables

Key variables were defined across satellite classes, orbit profiles, mission types, launch vehicle configurations, integration workflows, and regulatory gates. Demand drivers, qualification cycles, and supply chain constraints were mapped to operational milestones. Institutional mission pipelines and commercial constellation phasing informed variable prioritization.

Step 2: Market Analysis and Construction

Manufacturing throughput, integration cadence, and launch manifest capacity were constructed using operational indicators from 2024 and 2025. Scenario frameworks aligned production takt times with launch window availability and regulatory readiness. Sensitivity testing assessed impacts of test infrastructure utilization and range coordination constraints.

Step 3: Hypothesis Validation and Expert Consultation

Hypotheses on cadence scalability, reusability readiness, and platform standardization were validated through expert workshops with systems engineers, mission planners, and compliance leads. Iterative reviews refined assumptions on qualification bottlenecks, workforce readiness, and supply chain resilience across propulsion and avionics.

Step 4: Research Synthesis and Final Output

Findings were synthesized into integrated manufacturing–launch system pathways aligned to multi-orbit deployment strategies. Cross-functional insights were consolidated to ensure coherence between regulatory readiness, operational cadence, and mission assurance. Final outputs emphasize actionable pathways for scalable production and reliable launch access.

- Executive Summary

- Research Methodology (Market Definitions and satellite manufacturing and launch system taxonomy, OEM and launch service provider primary interviews, ESA and national space agency procurement analysis, Launch cadence and manifest tracking, Satellite production capacity and backlog assessment, Regulatory and export control review, Competitive intelligence from financial filings and contracts)

- Definition and Scope

- Market evolution

- Mission and application pathways

- Ecosystem structure

- Supply chain and industrial base structure

- Regulatory environment

- Growth Drivers

Expansion of European sovereign space capabilities

Rising demand for LEO broadband constellations

Increased Earth observation programs for climate and security

Public funding through ESA and national space programs

Commercialization of small satellite missions

Growth of in-orbit services and responsive launch demand - Challenges

High development and qualification costs for launch systems

Limited launch cadence and schedule reliability constraints

Dependence on public funding cycles and political priorities

Supply chain bottlenecks in propulsion and avionics

Export control and ITAR-related compliance burdens

Competition from non-European launch providers - Opportunities

Growth of European smallsat constellations for IoT and EO

Development of reusable and partially reusable launch vehicles

Expansion of commercial rideshare and dedicated small launch services

Public-private partnerships for sovereign launch access

Emergence of in-orbit servicing and manufacturing missions

Increased defense-driven demand for resilient space architectures - Trends

Shift toward LEO constellations and mass satellite production

Investments in reusable launch technologies

Vertical integration by satellite OEMs and launch providers

Standardization of satellite platforms and buses

Increased use of electric propulsion and advanced materials

Digitalization of manufacturing and mission operations - Government Regulations

- SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Value, 2020–2025

- By Shipment Volume, 2020–2025

- By Active Systems, 2020–2025

- By Unit Economics, 2020–2025

- By Satellite Class (in Value %)

Small satellites

Medium satellites

Large satellites

Constellation satellites - By Orbit Type (in Value %)

Low Earth Orbit

Medium Earth Orbit

Geostationary Orbit

Highly Elliptical Orbit - By Application (in Value %)

Earth observation

Telecommunications and broadband

Navigation and timing

Science and exploration

Defense and security - By Launch Vehicle Type (in Value %)

Small launch vehicles

Medium-lift launch vehicles

Heavy-lift launch vehicles

Rideshare launch services - By End User (in Value %)

Government and defense

Commercial operators

Scientific and research institutions - By Country (in Value %)

France

Germany

United Kingdom

Italy

Spain

- Market structure and competitive positioning

- Market share snapshot of major players

- Cross Comparison Parameters (launch success rate, manufacturing throughput, payload capacity range, cost per kilogram to orbit, reusability maturity, program backlog, geographic footprint, government contract exposure)

- SWOT Analysis of Key Players

- Pricing and Commercial Model Benchmarketing

- Detailed Profiles of Major Companies

Airbus Defence and Space

Thales Alenia Space

Arianespace

Avio

OHB SE

Surrey Satellite Technology Ltd

RUAG Space

GMV

Exotrail

Isar Aerospace

Rocket Factory Augsburg

PLD Space

Skyrora

Orbex

D-Orbit

- Demand and utilization drivers

- Procurement and tender dynamics

- Buying criteria and vendor selection

- Budget allocation and financing preferences

- Implementation barriers and risk factors

- Post-purchase service expectations

- By Value, 2026–2035

- By Shipment Volume, 2026–2035

- By Active Systems, 2026–2035

- By Unit Economics, 2026–2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now