Download PDF

Download PDF Download PDF

Download PDFMarket Overview

France agricultural equipment market reached USD ~ billion based on a recent historical assessment supported by European agricultural machinery industry statistics and national farm mechanization expenditure records. Demand is primarily driven by replacement of aging tractor fleets, mechanization in cereal and dairy production regions, and strong adoption of precision agriculture systems. Public subsidies for low-emission machinery and automation technologies also sustain equipment purchases across diverse farm sizes and crop types.

Dominance within the France agricultural equipment market is concentrated in regions such as Nouvelle-Aquitaine, Grand Est, and Occitanie due to large cereal, viticulture, and mixed farming operations requiring advanced machinery fleets. Strong cooperative farming structures and high mechanization intensity in these regions support equipment turnover. Western European suppliers and domestic manufacturers maintain technological leadership through established dealer networks, after-sales service infrastructure, and specialized machinery tailored to vineyards and high-value crop cultivation.

Market Segmentation

By Product Type

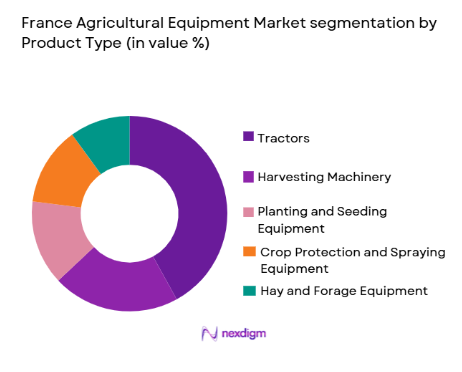

France Agricultural Equipment market is segmented by product type into tractors, harvesting machinery, planting and seeding equipment, crop protection and spraying equipment, and hay and forage equipment. Recently, tractors have a dominant market share due to factors such as broad applicability across crop types, essential role in primary field operations, strong domestic and European manufacturing presence, and continuous replacement cycles. High horsepower demand in cereal regions and compact tractor adoption in vineyards further reinforce tractor dominance, supported by subsidy programs encouraging modernization and emission-compliant machinery upgrades.

By Application

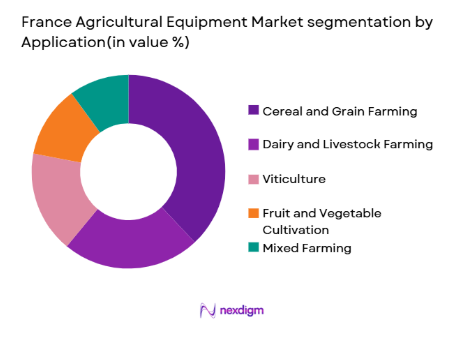

France Agricultural Equipment market is segmented by application into cereal and grain farming, dairy and livestock farming, viticulture, fruit and vegetable cultivation, and mixed farming. Recently, cereal and grain farming has a dominant market share due to extensive cultivated land area, high mechanization levels, and demand for large tractors, combines, and precision seeding equipment. Major grain-producing plains require advanced harvesting and tillage machinery, and cooperative farming structures enable capital-intensive equipment utilization, reinforcing this application’s leading position across mechanized agricultural regions.

Competitive Landscape

The France agricultural equipment market shows moderate consolidation with global manufacturers and specialized European firms competing through technology integration, dealer reach, and crop-specific machinery portfolios. Leading multinational companies maintain strong presence via local subsidiaries and distribution networks, while domestic producers focus on vineyard, tillage, and handling equipment niches. Partnerships with cooperatives and financing institutions reinforce market positioning, and innovation in precision agriculture and low-emission machinery differentiates competitive strategies across major suppliers.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD Billion) | Primary Crop Specialization |

| CLAAS | 1913 | Germany | ~ | ~ | ~ | ~ | ~ |

| John Deere | 1837 | USA | ~ | ~ | ~ | ~ | ~ |

| AGCO Corporation | 1990 | USA | ~ | ~ | ~ | ~ | ~ |

| CNH Industrial | 2013 | UK/Netherlands | ~ | ~ | ~ | ~ | ~ |

| Kuhn Group | 1828 | France | ~ | ~ | ~ | ~ | ~ |

France Agricultural Equipment Market Analysis

Growth Drivers

Agricultural Mechanization Modernization Programs:

France agricultural equipment demand is strongly influenced by national and European modernization programs promoting efficient and sustainable farming machinery. These initiatives encourage farmers to replace aging tractors and implements with advanced precision-enabled equipment that reduces fuel consumption and environmental impact. Financial incentives and low-interest financing schemes lower capital barriers for mechanization upgrades across both large and medium farms. Mechanization is particularly critical in cereal and dairy sectors where productivity depends on timely operations and scale efficiencies. Increasing labor shortages in rural areas further accelerate investment in automated machinery capable of performing multiple field tasks. Precision agriculture technologies such as GPS guidance, telematics, and variable-rate application systems are increasingly integrated into new equipment purchases. The modernization drive also supports compliance with emissions regulations, pushing adoption of low-emission engines and hybrid systems. As farms consolidate operationally through cooperatives, utilization rates of modern equipment rise, reinforcing replacement demand cycles. This systemic modernization trend sustains long-term equipment sales growth across France.

Expansion of Precision and Digital Agriculture Adoption:

The transition toward data-driven agriculture significantly stimulates demand for technologically advanced farm machinery in France. Farmers increasingly rely on precision seeding, automated spraying, and yield-monitoring harvesters to optimize input use and improve crop productivity. Integration of sensors, satellite guidance, and farm management software into equipment platforms enhances operational efficiency and decision-making accuracy. Digital connectivity allows real-time performance monitoring and predictive maintenance, reducing downtime and ownership costs. Government support for digital farming innovation and climate-smart agriculture encourages adoption of smart machinery across regions. Vineyard and specialty crop producers particularly benefit from precision robotics and compact autonomous equipment tailored to narrow-row cultivation. Equipment manufacturers invest heavily in embedded electronics and connectivity features to meet evolving farm technology expectations. Cooperative farming structures further facilitate shared use of high-technology machinery, improving affordability and penetration. The ongoing digitalization of agriculture therefore acts as a structural growth driver for advanced equipment demand.

Market Challenges

High Capital Cost of Advanced Agricultural Machinery:

Acquisition costs of modern agricultural equipment remain a significant constraint for many French farmers, particularly small and family-owned operations. Precision tractors, combines, and automated implements require substantial upfront investment despite available subsidies and financing schemes. Economic uncertainty in agricultural commodity markets reduces farmers’ willingness to undertake large capital expenditures. Seasonal income variability and long equipment payback periods further complicate purchasing decisions. Maintenance and repair costs for technologically complex machinery are also higher than for conventional equipment. Small farm sizes in certain regions limit machinery utilization rates, reducing return on investment. Equipment financing conditions may tighten during agricultural downturns, restricting credit access for farmers. Rapid technological obsolescence increases perceived investment risk, as newer digital features emerge quickly. These cost-related barriers slow replacement cycles and moderate overall equipment adoption growth across segments.

Regulatory Compliance and Environmental Standards Pressure:

Stringent European environmental regulations impose significant compliance requirements on agricultural machinery manufacturers and users in France. Emission standards necessitate advanced engine technologies and exhaust treatment systems that increase production and purchase costs. Safety and noise regulations also require additional engineering modifications and certification processes. Farmers must transition toward low-emission and precision equipment to meet sustainability targets and subsidy eligibility criteria. Compliance complexity can delay equipment approvals and market introduction timelines. Smaller domestic manufacturers face higher regulatory burden relative to multinational competitors with greater R&D resources. Environmental restrictions on chemical usage indirectly influence demand for specialized precision spraying machinery. Policy uncertainty regarding future emissions and sustainability standards complicates long-term equipment investment planning. Regulatory pressures therefore create structural challenges affecting both supply and adoption dynamics in the market.

Opportunities

Growth of Autonomous and Robotic Machinery in Specialty Crops:

France’s extensive vineyard and horticulture sectors create strong opportunities for autonomous and robotic agricultural equipment deployment. These crops require precision operations in confined spaces where compact robotic tractors and automated sprayers deliver efficiency gains. Labor shortages in vineyard management increase demand for autonomous machinery capable of performing repetitive tasks such as spraying and weeding. Technological advances in sensors, machine vision, and navigation enable safe operation in complex crop environments. Government and EU innovation funding programs support development and commercialization of agricultural robotics. Domestic manufacturers specializing in viticulture equipment can leverage this niche leadership globally. Autonomous equipment reduces chemical inputs and fuel use, aligning with sustainability goals and regulatory incentives. Early adoption by high-value crop producers accelerates market acceptance and technological refinement. The specialty crop robotics segment therefore represents a significant growth opportunity within France agricultural mechanization.

Electrification and Low-Emission Farm Equipment Transition:

Transition toward electric and hybrid agricultural machinery presents substantial opportunity in France due to environmental policies and energy transition targets. Electric tractors and implements reduce emissions, noise, and operating costs, particularly suitable for livestock farms and indoor operations. Urban-adjacent agriculture and vineyards benefit from low-noise electric equipment compatible with environmental regulations. Advances in battery capacity and charging infrastructure improve operational feasibility of electrified machinery. Government subsidies and climate funding programs incentivize adoption of zero-emission agricultural equipment. Manufacturers investing in electric drivetrains and energy-efficient systems gain competitive differentiation in sustainability-focused markets. Electrification also supports integration with renewable energy systems on farms, reducing fuel dependency. As environmental standards tighten, electrified machinery adoption is expected to expand across multiple agricultural applications. This transition provides long-term growth potential for innovative equipment suppliers in France.

Future Outlook

France agricultural equipment market is expected to expand steadily over the next five years driven by mechanization renewal cycles, digital agriculture integration, and sustainability policies. Adoption of precision, autonomous, and low-emission machinery will accelerate as farms modernize operations and comply with environmental regulations. Continued government incentives and cooperative farming structures will support capital investment in advanced equipment. Specialty crop mechanization and electrified machinery segments are likely to record faster growth, while replacement demand sustains overall market stability.

Major Players

- CLAAS

- John Deere

- AGCO Corporation

- CNH Industrial

- Kuhn Group

- Same Deutz-Fahr

- Kubota Corporation

- Manitou Group

- Pellenc Group

- Grégoire-Besson

- Carré SAS

- Monosem

- Sulky Burel

- Maschio Gaspardo

- Hardy Sprayers

Key Target Audience

- Agricultural equipment manufacturers

- Farm machinery distributors and dealers

- Agricultural cooperatives

- Large commercial farming enterprises

- Precision agriculture technology providers

- Investments and venture capitalist firms

- Government and regulatory bodies

- Agricultural financing institutions

Research Methodology

Step 1: Identification of Key Variables

Comprehensive variables influencing France agricultural equipment demand were identified, including mechanization levels, crop patterns, subsidy programs, technology adoption rates, and farm structure characteristics. Data sources included agricultural statistics, industry associations, and machinery registration records.

Step 2: Market Analysis and Construction

Market size and segmentation were constructed using equipment sales data, trade statistics, and mechanization indicators across product and application categories. Regional agricultural production and machinery utilization patterns were analyzed to determine segment shares and competitive structure.

Step 3: Hypothesis Validation and Expert Consultation

Preliminary estimates and structural assumptions were validated through consultations with agricultural machinery experts, distributors, and cooperative procurement specialists. Industry reports and policy frameworks were cross-checked to ensure consistency with mechanization and sustainability trends.

Step 4: Research Synthesis and Final Output

Validated data and insights were synthesized into structured market analysis covering segmentation, competition, drivers, challenges, and opportunities. Quantitative estimates and qualitative assessments were integrated to produce a comprehensive France agricultural equipment market outlook.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Strong mechanization demand in high-value crop regions

Expansion of precision agriculture adoption

Government incentives for sustainable farming equipment

Labor shortages driving automation uptake

Replacement demand for aging machinery fleets - Market Challenges

High acquisition cost of advanced machinery

Fragmented farm structure limiting scale adoption

Regulatory emissions compliance costs

Seasonal utilization affecting ROI

Dependence on imported components - Market Opportunities

Growth in autonomous vineyard machinery

Electrification of compact farm equipment

Digital farm management integration - Trends

Rapid adoption of GPS-guided tractors

Integration of telematics and fleet analytics

Shift toward low-emission machinery

Robotic solutions for specialty crops

Data-driven variable rate technologies - Government Regulations & Defense Policy

EU agricultural machinery safety standards enforcement

Subsidies for low-emission farm equipment

Digital agriculture funding programs - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Tractors and Power Units

Harvesting Machinery

Planting and Seeding Equipment

Crop Protection and Spraying Systems

Hay and Forage Equipment - By Platform Type (In Value%)

Wheeled Self-Propelled Equipment

Tracked Agricultural Machines

Mounted and Trailed Implements

Autonomous Robotic Platforms

Aerial Agricultural Systems - By Fitment Type (In Value%)

OEM Integrated Systems

Aftermarket Attachments

Retrofit Precision Kits

Modular Add-On Units

Fully Integrated Smart Equipment - By EndUser Segment (In Value%)

Large Commercial Farms

Family-Owned Medium Farms

Agricultural Cooperatives

Viticulture and Specialty Crop Growers

Agricultural Contractors - By Procurement Channel (In Value%)

Direct Manufacturer Sales

Authorized Dealer Networks

Agricultural Cooperatives Procurement

Government and Subsidy Programs

Online and Digital Marketplaces - By Material / Technology (in Value %)

Precision GPS and Guidance Systems

ISOBUS-Compatible Electronics

Lightweight Composite Structures

Electric and Hybrid Powertrains

IoT-Enabled Smart Sensors

- Market structure and competitive positioning

- Market share snapshot of major players

- CrossComparison Parameters (Product Portfolio Breadth, Technology Integration Level, Horsepower Range Coverage, Precision Agriculture Capability, Dealer Network Strength, AfterSales Service Depth, Localization in France, Sustainability Compliance, Pricing Tier Positioning, Innovation and R&D Intensity)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

CLAAS

AGCO Corporation

John Deere

CNH Industrial

Kubota Corporation

Same Deutz-Fahr

Kuhn Group

Grégoire-Besson

Manitou Group

Pellenc Group

Carré SAS

Monosem

Sulky Burel

Maschio Gaspardo

Hardy Sprayers

- Large cereal farms prioritizing high-horsepower tractors

- Vineyards demanding compact autonomous machines

- Cooperatives pooling machinery investments

- Contractors driving high-utilization equipment demand

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now