Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The France Agricultural Tractor & Harvester market reached approximately USD ~ billion based on a recent historical assessment, driven by replacement demand for Stage V emission compliant machinery and sustained mechanization in cereal and forage farming. Strong domestic manufacturing capacity and export oriented OEM production have reinforced equipment availability and technological penetration. Subsidy frameworks under European agricultural modernization schemes and the high average age of tractors in operation have accelerated fleet renewal across major crop producing regions.

Within the France Agricultural Tractor & Harvester market, dominance is concentrated in Western European agricultural economies led by France itself, followed by Germany and Italy due to extensive mechanized farming systems and strong OEM presence. Northern France regions such as Hauts de France and Grand Est lead equipment adoption because of large scale cereal cultivation, while western dairy belts like Brittany sustain forage harvester demand. Industrial clusters and dealership networks across these areas ensure rapid distribution and service coverage.

Market Segmentation

By Product Type:

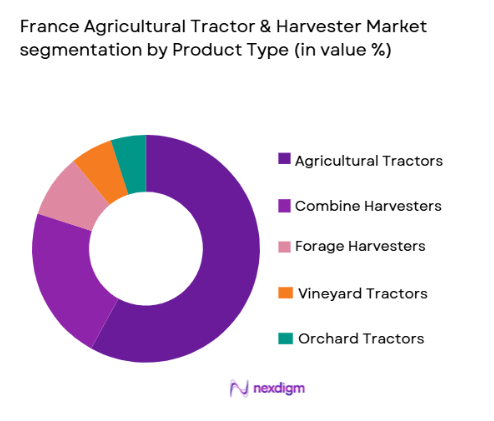

France Agricultural Tractor & Harvester market is segmented by product type into agricultural tractors, combine harvesters, forage harvesters, vineyard tractors, and orchard tractors. Recently, agricultural tractors have a dominant market share due to factors such as universal applicability across crop types, continuous replacement cycles, and extensive horsepower range suited to both arable and livestock farming. The high installed base of tractors across French farms ensures recurring demand for upgrades driven by emissions compliance and precision agriculture integration. Broad dealer networks and financing availability further strengthen tractor penetration compared with specialized harvesting equipment.

By Power Output:

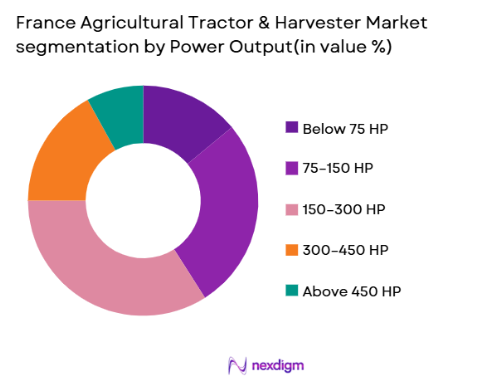

France Agricultural Tractor & Harvester market is segmented by power output into below 75 HP, 75–150 HP, 150–300 HP, 300–450 HP, and above 450 HP equipment. Recently, 150–300 HP equipment has a dominant market share due to factors such as suitability for medium to large cereal farms, compatibility with modern implements, and balanced fuel efficiency with operational capacity. This power band aligns with the average farm size expansion trend in France and supports precision agriculture technologies. Contractors and cooperatives also prefer this category for multi crop operations, reinforcing its market leadership.

Competitive Landscape

The France Agricultural Tractor & Harvester market is moderately consolidated with a mix of global agricultural machinery manufacturers and strong European specialists. Major players maintain dominance through localized production, advanced precision farming technologies, and extensive dealer networks. Brand loyalty among farmers and contractors reinforces market concentration, while mergers and portfolio expansions among European OEMs continue to shape competitive positioning.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Dealer Network Strength |

| CLAAS Group | 1913 | Germany | ~ | ~ | ~ | ~ | ~ |

| CNH Industrial | 2013 | UK | ~ | ~ | ~ | ~ | ~ |

| AGCO Corporation | 1990 | USA | ~ | ~ | ~ | ~ | ~ |

| Deere & Company | 1837 | USA | ~ | ~ | ~ | ~ | ~ |

| Kubota Corporation | 1890 | Japan | ~ | ~ | ~ | ~ | ~ |

France Agricultural Tractor & Harvester Market Analysis

Growth Drivers

Expansion of Precision Agriculture and Digital Farming Integration:

The France Agricultural Tractor & Harvester market is experiencing strong growth due to rapid adoption of precision agriculture technologies embedded within modern tractors and harvesters. Farmers across cereal producing regions are increasingly integrating GPS guidance, variable rate application, yield monitoring, and telematics to improve productivity and reduce input costs. This technological transition requires equipment upgrades, accelerating replacement cycles for older machinery fleets that lack digital capability. OEMs operating in France are embedding connectivity platforms and automation features as standard specifications, raising equipment value and encouraging adoption. Government supported modernization incentives across European agriculture are further stimulating investment in precision capable tractors and harvesting machinery. Large contractors managing multi farm operations depend on connected machinery fleets to optimize scheduling and utilization, reinforcing demand. The shift toward data driven farming also supports higher horsepower and technologically advanced harvesting platforms capable of handling large fields efficiently. Additionally, environmental compliance requirements encourage optimized input usage, which precision equipment facilitates. As French agriculture transitions toward smart farming systems, digitally enabled tractors and harvesters are becoming essential operational assets.

Accelerated Replacement of Aging Machinery Fleet under Emission Standards:

A significant portion of the France Agricultural Tractor & Harvester installed base consists of equipment exceeding typical operational life cycles, creating strong replacement demand. Implementation of stringent Stage V emission regulations for non road agricultural machinery has rendered older tractors and harvesters less compliant and less efficient. Farmers are incentivized to replace legacy equipment with modern low emission models offering improved fuel economy and performance. Government subsidy programs tied to environmental compliance and modernization have reduced capital barriers for equipment renewal. OEMs are launching updated tractor and harvester ranges specifically engineered for emissions standards, stimulating purchase activity. The economic benefits of lower fuel consumption and reduced maintenance costs further justify replacement investments for farmers and contractors. Financing programs and leasing structures offered by manufacturers and cooperatives also facilitate fleet upgrades. Mechanization intensity in French agriculture ensures continuous equipment utilization, increasing wear and accelerating renewal cycles. Consequently, emissions driven replacement demand remains a core structural growth factor for the market.

Market Challenges

High Capital Cost and Financing Constraints for Advanced Machinery:

Modern tractors and harvesting equipment incorporating precision agriculture technologies, automation systems, and emissions compliant powertrains involve substantially higher acquisition costs than legacy machinery. Many small and medium sized farms in France operate under tight profit margins influenced by commodity price volatility and input cost fluctuations, limiting capital expenditure capacity. Although subsidies exist, upfront investment requirements remain significant, particularly for high horsepower tractors and self propelled harvesters. Financing access varies across regions and farm sizes, creating unequal adoption rates for advanced machinery. Contractors and cooperatives mitigate this barrier, yet ownership costs remain prohibitive for independent farmers. Additionally, rapid technological evolution increases perceived obsolescence risk, discouraging large purchases. Maintenance and software subscription costs associated with digital equipment further increase lifetime ownership expenses. Economic uncertainty and fluctuating agricultural income streams can delay equipment replacement decisions. These financial constraints collectively slow penetration of advanced tractors and harvesters across parts of the market.

Seasonal Utilization and Low Asset Turnover in Specialized Harvesters:

Harvesting machinery such as combines and forage harvesters experience highly seasonal operational cycles aligned with crop harvesting periods in France. Outside these limited seasonal windows, equipment remains idle, reducing annual utilization rates and lowering return on investment for owners. This challenge is particularly pronounced for specialized machinery serving single crop segments like vineyards or forage harvesting. Farmers often rely on contractors rather than direct ownership to mitigate underutilization risk, restricting market expansion. High maintenance requirements for idle equipment further increase lifecycle costs. Storage, insurance, and depreciation expenses accumulate even during non operational periods, affecting profitability. Weather variability can compress harvesting windows, intensifying usage spikes followed by prolonged inactivity. The economics of ownership therefore favor large contractors or cooperatives rather than individual farmers. As a result, purchase volumes for harvesters remain sensitive to utilization economics and seasonal demand variability.

Opportunities

Electrification and Hybridization of Agricultural Powertrains:

The transition toward low emission and energy efficient agricultural machinery presents a major opportunity in the France Agricultural Tractor & Harvester market. Development of hybrid and fully electric tractor platforms aligns with European decarbonization policies and sustainability objectives in agriculture. Electrified drivetrains can significantly reduce fuel consumption, emissions, and operating noise, particularly valuable for vineyard and livestock farming environments. Government incentives for sustainable machinery adoption can accelerate commercialization of these technologies. Advances in battery density and charging infrastructure are gradually improving feasibility for medium power tractors used in regional farming operations. OEM investment in electric prototypes and hybrid harvesters is increasing across European manufacturers. Farmers seeking long term operating cost reductions may adopt electrified machinery despite higher upfront costs. Urban proximity farming and specialty crop sectors offer early adoption niches. Over time, electrification can reshape equipment design, maintenance structures, and energy supply chains within agricultural mechanization.

Growth of Contractor Based Mechanization and Shared Equipment Models:

Expansion of agricultural contractor services and cooperative machinery ownership models creates a strong opportunity for the France Agricultural Tractor & Harvester market. Many French farms prefer outsourcing harvesting and heavy mechanization tasks to specialized contractors equipped with high capacity modern machinery. This trend enables efficient utilization of expensive tractors and harvesters across multiple farms, improving asset productivity. Contractors typically invest in technologically advanced equipment fleets to maintain competitive service offerings, supporting high value equipment demand. Cooperative ownership schemes also allow smaller farms to access modern machinery without full ownership costs. Digital fleet management tools enable scheduling and sharing across members, improving equipment utilization rates. Manufacturers benefit from bulk sales to contractors and cooperatives rather than fragmented individual purchases. As farm consolidation and labor shortages continue, service based mechanization demand is expected to expand. This structural shift supports sustained growth in high performance tractors and harvesters.

Future Outlook

The France Agricultural Tractor & Harvester market is expected to expand steadily over the next five years driven by precision farming adoption, emissions compliant machinery replacement, and contractor led mechanization. Electrified powertrains, automation, and digital fleet management will shape product innovation. Policy support for sustainable agriculture and modernization subsidies will continue encouraging equipment upgrades. Demand from large cereal farms and cooperative mechanization models will reinforce market stability.

Major Players

- CLAAS Group

- CNH Industrial

- AGCO Corporation

- Deere & Company

- Kubota Corporation

- SDF Group

- Argo Tractors

- Kuhn Group

- Kverneland Group

- Manitou Group

- Fendt

- Massey Ferguson

- New Holland Agriculture

- Deutz Fahr

- Same Tractors

Key Target Audience

- Agricultural machinery manufacturers

- Farm equipment distributors and dealers

- Agricultural cooperatives

- Large scale farming enterprises

- Agricultural contractors and service providers

- Investments and venture capitalist firms

- Government and regulatory bodies

- Precision agriculture technology providers

Research Methodology

Step 1: Identification of Key Variables

Key market variables including machinery sales volume, installed fleet age, emission regulations, subsidy structures, and mechanization intensity were identified through industry databases and agricultural policy documentation. Regional cropping patterns and farm size distribution were mapped to equipment demand categories.

Step 2: Market Analysis and Construction

Market size and segmentation were constructed using equipment registration statistics, manufacturer shipment data, and trade association reports. Power output and product category shares were derived from sales mix patterns and mechanization usage across French agricultural regions.

Step 3: Hypothesis Validation and Expert Consultation

Findings were validated through consultations with agricultural machinery distributors, contractors, and farm cooperatives. OEM product managers and service providers provided insights into replacement cycles, technology adoption, and regional equipment demand dynamics.

Step 4: Research Synthesis and Final Output

All quantitative and qualitative insights were synthesized into structured market analysis. Cross verification ensured consistency between demand drivers, segmentation, and competitive landscape to produce a comprehensive France Agricultural Tractor & Harvester market assessment.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Mechanization demand in large scale cereal cultivation regions

Replacement cycle acceleration due to emissions compliant equipment

Labor shortages driving adoption of high capacity harvesters

Expansion of precision agriculture practices

Government supported modernization incentives - Market Challenges

High acquisition costs of advanced harvesting machinery

Fragmented farm structure in certain regions

Compliance costs with stringent EU emissions norms

Seasonal utilization affecting ROI for farmers

Supply chain disruptions in components and electronics - Market Opportunities

Electrified and hybrid tractor platforms for specialty farming

Autonomous harvesting solutions for labor constrained operations

Digital service and predictive maintenance offerings - Trends

Integration of smart guidance and auto steering systems

Growth in contractor owned high horsepower machinery fleets

Adoption of telematics based fleet optimization

Specialized machinery for vineyards and orchards

Shift toward low emission powertrain technologies - Government Regulations & Defense Policy

EU Stage V emission standards for non road mobile machinery

Common Agricultural Policy subsidies for farm modernization

French road homologation and safety certification for tractors - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Utility Tractors

Row Crop Tractors

Combine Harvesters

Forage Harvesters

Vineyard and Orchard Tractors - By Platform Type (In Value%)

Wheeled Tractors

Tracked Tractors

Self Propelled Harvesters

Mounted Harvesters

Trailed Harvesters - By Fitment Type (In Value%)

Front Mounted Implements

Rear Mounted Implements

Mid Mount Configurations

Integrated Harvester Headers

Quick Coupler Systems - By EndUser Segment (In Value%)

Cereal and Grain Farms

Dairy and Livestock Farms

Vineyard and Orchard Farms

Agricultural Contractors

Cooperative Farming Groups - By Procurement Channel (In Value%)

Authorized Dealership Networks

Direct OEM Sales

Agricultural Cooperatives

Equipment Leasing Providers

Online Machinery Platforms - By Material / Technology (in Value %)

Stage V Diesel Powertrains

Hybrid Electric Drives

Precision GPS Guidance Systems

Telematics and Fleet Management

Advanced Header Automation

- Market structure and competitive positioning

- Market share snapshot of major players

- CrossComparison Parameters (Engine Horsepower Range, Harvesting Capacity, Automation Level, Emissions Compliance Tier, Fuel Type, Transmission Type, Precision Farming Integration, Attachment Compatibility, Lifecycle Cost, AfterSales Network)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

CLAAS Group

CNH Industrial

AGCO Corporation

John Deere

Kubota Corporation

SDF Group

Argo Tractors

Kuhn Group

Manitou Group

Kverneland Group

Fendt

Massey Ferguson

New Holland Agriculture

Deutz Fahr

Same Tractors

- Large grain producers prioritizing high capacity combines

- Contractors expanding multi farm harvesting services

- Vineyard operators demanding compact specialized tractors

- Cooperatives enabling shared machinery ownership models

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now