Download PDF

Download PDF Download PDF

Download PDFMarket Overview

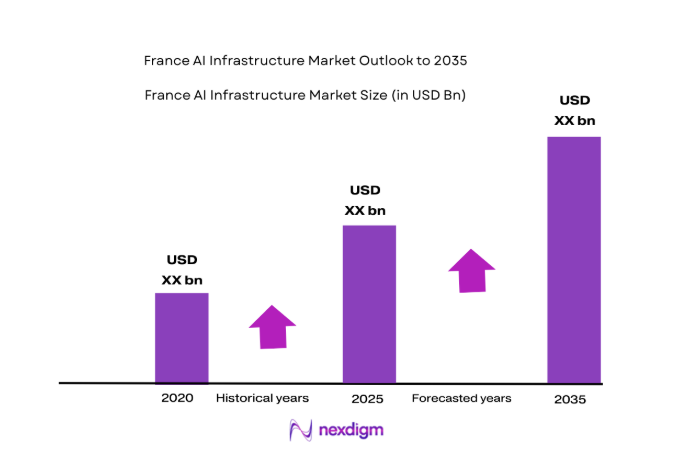

France AI infrastructure market reached approximately USD ~ billion based on a recent historical assessment, reflecting sustained expansion of high-performance computing clusters, hyperscale cloud regions, and sovereign data center deployments across the country. Growth is primarily driven by national artificial intelligence strategy funding, enterprise generative AI adoption, and rapid expansion of GPU-accelerated compute environments. Large-scale investments in energy-efficient AI data centers and liquid-cooled supercomputing facilities further strengthened infrastructure capacity supporting research, defense, and industrial AI workloads.

Paris dominates the France AI infrastructure market due to concentration of hyperscale cloud regions, financial institutions, and government digital agencies requiring sovereign compute environments and high-security data hosting. Île-de-France also benefits from dense fiber connectivity, skilled AI engineering workforce, and proximity to national research laboratories and supercomputing centers. Marseille and Lyon are emerging secondary hubs supported by submarine cable landings, industrial clusters, and regional digital infrastructure programs enabling distributed AI compute deployment.

Market Segmentation

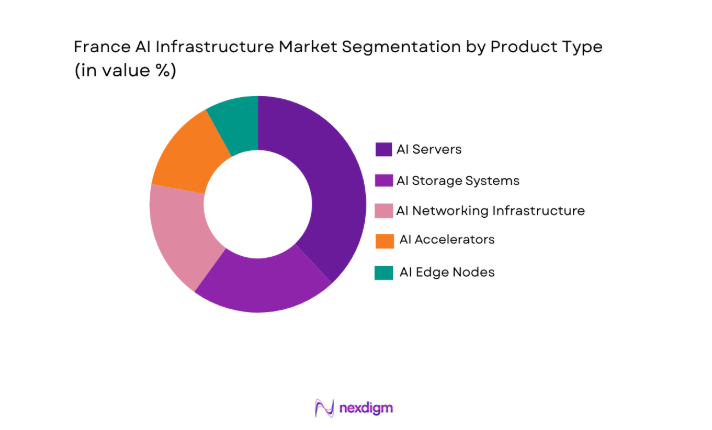

By Product Type

France AI Infrastructure market is segmented by product type into AI servers, AI storage systems, AI networking infrastructure, AI accelerators, and AI edge nodes. Recently, AI servers have a dominant market share due to factors such as hyperscale deployment demand, enterprise generative AI workloads, and rapid GPU-dense rack adoption across sovereign cloud and supercomputing facilities. National AI programs and enterprise modernization initiatives prioritize high-performance compute clusters, driving large procurement volumes and infrastructure standardization. Server-centric architecture also anchors integrated AI stacks, reinforcing its leading position.

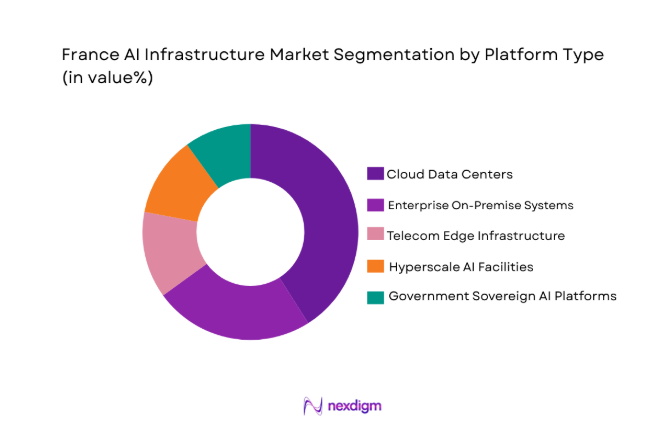

By Platform Type

France AI Infrastructure market is segmented by platform type into cloud data centers, enterprise on-premise systems, telecom edge infrastructure, hyperscale AI facilities, and government sovereign AI platforms. Recently, cloud data centers have a dominant market share due to factors such as scalable AI workload hosting, sovereign cloud adoption, and multi-tenant GPU cluster availability for enterprises and public sector agencies. Hyperscale operators and national cloud initiatives centralize compute resources, enabling cost efficiency and elastic deployment models preferred by organizations transitioning to AI-driven operations.

Competitive Landscape

France AI infrastructure market exhibits moderate consolidation with a mix of global hardware vendors, national digital infrastructure providers, and sovereign cloud operators shaping competitive intensity. Large technology firms dominate high-performance compute and accelerator supply, while domestic engineering and data center specialists maintain influence in sovereign and regulated deployments. Strategic partnerships between cloud providers, telecom operators, and energy-efficient infrastructure firms define procurement ecosystems and long-term infrastructure investments.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Sovereign AI Capability |

| Atos | 1997 | France | ~ | ~ | ~ | ~ | ~ |

| OVHcloud | 1999 | France | ~ | ~ | ~ | ~ | ~ |

| Orange Business | 2006 | France | ~ | ~ | ~ | ~ | ~ |

| Schneider Electric | 1836 | France | ~ | ~ | ~ | ~ | ~ |

| Capgemini | 1967 | France | ~ | ~ | ~ | ~ | ~ |

France AI infrastructure Market Analysis

Growth Drivers

National AI Sovereignty and Strategic Compute Investments

France AI infrastructure expansion is strongly driven by national strategic objectives to establish sovereign artificial intelligence capabilities and reduce dependence on foreign cloud and semiconductor ecosystems, resulting in sustained public and private investments into domestic high-performance computing clusters and sovereign data center environments. Government backed AI programs channel funding into supercomputing facilities, trusted cloud platforms, and secure data hosting architectures that comply with European data sovereignty regulations, stimulating procurement of GPU dense servers, advanced cooling systems, and secure networking infrastructure across defense, research, and public administration sectors. The emphasis on technological independence encourages domestic manufacturing partnerships, national cloud initiatives, and local infrastructure engineering ecosystems, creating stable long-term demand for AI compute platforms within France and the broader European digital sovereignty framework. Sovereign compute policies also drive modernization of legacy government IT environments toward AI-ready architectures capable of supporting large language models, predictive analytics systems, and national data platforms requiring controlled processing environments. Public sector digital transformation programs further reinforce demand by mandating trusted infrastructure hosting for sensitive citizen data, healthcare records, and critical industrial information, increasing adoption of certified domestic AI infrastructure providers. National supercomputing initiatives and European collaborative HPC programs strengthen domestic AI infrastructure supply chains through procurement frameworks prioritizing local engineering capability and energy-efficient compute design. Industrial policy alignment between AI strategy, semiconductor initiatives, and energy transition programs ensures coordinated infrastructure expansion across research, defense, manufacturing, and digital services sectors, sustaining long-term capacity growth. The combined effect of sovereignty requirements, funding stability, and regulatory alignment creates predictable infrastructure investment cycles that support domestic vendors and hyperscale deployments within national borders.

Enterprise Generative AI Adoption and Hyperscale Cloud Expansion

Rapid enterprise adoption of generative artificial intelligence applications across finance, manufacturing, retail, and public services sectors significantly accelerates demand for scalable AI compute environments, driving hyperscale cloud region expansion and GPU-accelerated data center deployments throughout France. Organizations integrating large language models, computer vision analytics, and predictive automation systems require high-density compute clusters and high-bandwidth networking fabrics capable of supporting model training and inference workloads at scale, increasing procurement of AI-optimized servers, storage, and networking infrastructure. Cloud providers respond by expanding regional data center capacity and sovereign cloud offerings tailored to regulatory compliance and low-latency processing requirements, reinforcing centralized AI infrastructure investment. Enterprise migration toward cloud-hosted AI platforms reduces barriers to adoption while creating sustained demand for shared GPU clusters and managed AI infrastructure services delivered through hyperscale operators. The integration of AI capabilities into enterprise software platforms, industrial automation systems, and digital customer interfaces multiplies compute intensity across sectors, further strengthening infrastructure consumption patterns. Hyperscale operators deploy advanced cooling, energy optimization, and modular data center architectures to support continuous AI workload growth while maintaining operational efficiency and regulatory compliance. Strategic partnerships between enterprises and cloud providers also accelerate deployment of dedicated AI infrastructure zones and private cloud AI environments supporting secure workloads. As generative AI transitions from experimentation to core operational capability across industries, hyperscale infrastructure expansion remains a structural driver of the France AI infrastructure market.

Market Challenges

High Capital Intensity and Energy Constraints in AI Data Center Expansion

The France AI infrastructure market faces significant barriers associated with the exceptionally high capital expenditure required to deploy GPU-dense data centers, advanced cooling systems, high-capacity power distribution networks, and secure sovereign hosting facilities capable of supporting modern artificial intelligence workloads. AI data centers demand substantially greater electrical power density than conventional computing facilities due to accelerator-rich server architectures, leading to increased infrastructure cost, longer construction timelines, and dependence on stable grid connectivity and renewable energy integration. National energy transition policies and carbon reduction commitments impose additional constraints on infrastructure operators, requiring energy-efficient design, low-carbon electricity sourcing, and thermal optimization technologies that further elevate upfront investment requirements. Limited availability of suitable land parcels with grid capacity, fiber connectivity, and environmental clearance slows expansion of large-scale AI facilities in metropolitan regions where demand is highest. Rising electricity costs and regulatory scrutiny of energy-intensive computing facilities create operational risk and financial uncertainty for infrastructure providers planning long-term AI capacity expansion. Cooling requirements for high-performance accelerators necessitate liquid cooling or immersion technologies that involve complex engineering integration and increased maintenance costs compared with traditional air-cooled data centers. Financing challenges emerge for smaller domestic infrastructure firms lacking capital scale to compete with global hyperscale operators capable of deploying multi-billion-dollar AI campuses. These capital and energy constraints collectively limit speed of infrastructure rollout and intensify competitive advantage of large multinational providers within the France AI infrastructure market.

Dependence on Imported Advanced Semiconductors and Accelerator Supply Chains

France AI infrastructure development remains structurally dependent on imported high-performance GPUs, AI accelerators, and advanced semiconductor components primarily manufactured outside Europe, creating supply chain vulnerability, procurement uncertainty, and pricing volatility for domestic infrastructure operators. Global concentration of advanced semiconductor fabrication capacity exposes infrastructure deployment timelines to geopolitical tensions, export controls, and production constraints affecting availability of cutting-edge AI chips required for training and inference workloads. Domestic AI infrastructure providers must compete with hyperscale cloud operators and international technology firms for limited accelerator supply, often facing extended lead times and cost premiums that delay deployment of compute clusters and supercomputing facilities. Limited European semiconductor manufacturing capability restricts local sourcing options and reduces bargaining power in procurement negotiations, particularly for emerging accelerator architectures optimized for generative AI models. Technology lifecycle acceleration in AI hardware further intensifies dependency, as infrastructure providers must continuously upgrade systems to remain performance competitive, increasing exposure to external semiconductor supply fluctuations. Integration challenges arise when combining imported accelerators with locally engineered servers and cooling systems, requiring specialized design adaptation and technical expertise. Policy initiatives supporting European semiconductor sovereignty remain in early stages and have not yet translated into large-scale domestic accelerator production capable of meeting infrastructure demand. This structural reliance on external semiconductor ecosystems constrains strategic autonomy and introduces persistent risk into long-term France AI infrastructure expansion planning.

Opportunities

Development of Sovereign European AI Cloud and Trusted Compute Platforms

France AI infrastructure market holds substantial growth potential through expansion of sovereign European artificial intelligence cloud platforms designed to provide secure, regulation-compliant compute environments for government agencies, defense organizations, healthcare systems, and regulated enterprises requiring controlled data processing within national and European jurisdictional boundaries. Increasing enforcement of data protection regulations and digital sovereignty policies encourages migration of sensitive workloads toward trusted domestic infrastructure providers offering certified hosting, secure networking, and sovereign AI processing frameworks. National cloud initiatives and collaborative European infrastructure programs create opportunities for domestic operators to deploy large-scale AI compute clusters tailored to sovereignty compliance and privacy-preserving architecture requirements. Demand for trusted AI environments supporting public sector analytics, healthcare diagnostics, and critical infrastructure monitoring expands procurement of secure data centers and sovereign GPU clusters. European industrial alliances and funding mechanisms facilitate joint development of sovereign AI platforms integrating domestic hardware engineering, cloud orchestration, and cybersecurity technologies. Enterprises in finance, energy, and manufacturing sectors increasingly prefer sovereign AI hosting to mitigate regulatory risk and cross-border data transfer constraints. Sovereign cloud adoption also stimulates localized AI ecosystem growth including data services, AI model hosting, and secure analytics platforms anchored on domestic infrastructure. As digital sovereignty becomes a structural policy priority across Europe, France positioned with strong public funding and domestic infrastructure capability stands to expand sovereign AI cloud deployment significantly.

AI Infrastructure for Industrial Automation, Robotics, and Edge Intelligence Deployment

Expanding integration of artificial intelligence into industrial automation systems, robotics platforms, logistics optimization networks, and smart manufacturing environments creates substantial opportunity for distributed AI infrastructure deployment across factories, transportation hubs, and energy systems throughout France. Industrial enterprises adopting predictive maintenance analytics, autonomous robotics control, and real-time process optimization require localized edge AI compute nodes capable of low-latency data processing and machine learning inference within operational environments. Industry digitalization programs and smart factory initiatives stimulate demand for ruggedized AI servers, industrial edge accelerators, and private AI networks integrated with production systems. Telecommunications operators and industrial technology vendors collaborate to deploy edge AI infrastructure supporting connected machinery, autonomous vehicles, and intelligent supply chain platforms. The convergence of industrial IoT and AI analytics expands infrastructure requirements beyond centralized data centers into distributed compute architectures embedded across industrial ecosystems. Energy, transportation, and logistics sectors adopt AI-enabled monitoring and optimization systems requiring resilient local processing infrastructure. National manufacturing modernization strategies and Industry 4.0 programs reinforce investment in AI-enabled production systems anchored by edge compute infrastructure. As industrial sectors transition toward autonomous and data-driven operations, distributed AI infrastructure deployment emerges as a major growth opportunity within the France AI infrastructure market.

Future Outlook

France AI infrastructure market is expected to experience sustained expansion over the next five years supported by sovereign cloud programs, hyperscale data center construction, and enterprise generative AI adoption. Continued public funding for national supercomputing and trusted AI platforms will accelerate domestic infrastructure capacity. Advances in liquid cooling, energy-efficient accelerators, and modular AI data centers will improve scalability and sustainability. Growing industrial AI deployment and edge computing integration will further diversify infrastructure demand across regions and sectors.

Major Players

- Atos

- OVHcloud

- Orange Business

- Schneider Electric

- Capgemini

- Thales

- Dassault Systèmes

- Eviden

- Nvidia

- Intel

- AMD

- HPE

- Dell Technologies

- Lenov

- Cisco

Key Target Audience

- Hyperscale cloud providers

- Telecommunications operators

- Government and regulatory bodies

- Defense and security agencies

- Large enterprises

- Industrial automation companies

- Investments and venture capitalist firms

- Data center developers

Research Methodology

Step 1: Identification of Key Variables

Critical variables including AI compute capacity, data center deployment, accelerator adoption, and sovereign cloud investment were identified through secondary research across government policy papers, infrastructure reports, and industry databases. Market boundaries and technology scope were defined based on AI infrastructure components and deployment models across France.

Step 2: Market Analysis and Construction

Market structure was constructed by mapping supply chains covering semiconductor vendors, server manufacturers, cloud providers, and infrastructure operators. Capacity additions, procurement patterns, and deployment trends were analyzed to estimate market size and segmentation distribution for France AI infrastructure.

Step 3: Hypothesis Validation and Expert Consultation

Preliminary findings were validated through expert insights from infrastructure engineers, cloud architects, and AI deployment specialists. Industry consultations ensured accuracy of technology trends, adoption drivers, and investment patterns across sovereign, enterprise, and hyperscale infrastructure environments.

Step 4: Research Synthesis and Final Output

Validated data and qualitative insights were synthesized into a structured analytical framework covering market dynamics, segmentation, competition, and outlook. Final outputs were aligned with France AI infrastructure market scope and standardized research methodology protocols.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

National AI sovereignty and strategic compute investments

Expansion of hyperscale and sovereign cloud infrastructure

Rising enterprise adoption of generative AI workloads

Public funding for AI research supercomputing facilities

Growth of edge AI deployments in telecom and industry - Market Challenges

High capital intensity of AI data center infrastructure

Power availability and grid constraints for large facilities

Dependence on imported advanced semiconductors

Cooling and energy efficiency requirements

Skills shortage in AI infrastructure engineering - Market Opportunities

Development of sovereign AI cloud and compute platforms

AI infrastructure for industrial automation and robotics

Green AI data centers using low carbon energy - Trends

Shift toward GPU dense and accelerator rich architectures

Adoption of liquid cooling in AI data centers

Rise of edge AI infrastructure for 5G and IoT

Integration of AI supercomputing in research clusters

Partnerships between cloud providers and telecom operators - Government Regulations & Defense Policy

EU AI Act compliance and trusted AI infrastructure standards

National sovereignty policies for sensitive data hosting

Public funding programs for AI compute and research facilities - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

AI Compute Servers

AI Storage and Data Fabric Systems

AI Networking and Interconnect Infrastructure

Edge AI Infrastructure Nodes

AI Accelerators and Processing Units - By Platform Type (In Value%)

Cloud Data Center AI Infrastructure

Enterprise On Premise AI Infrastructure

Telecom Edge AI Infrastructure

Hyperscale AI Supercomputing Facilities

Sovereign and Government AI Infrastructure - By Fitment Type (In Value%)

Greenfield AI Data Center Deployments

Brownfield AI Infrastructure Upgrades

Modular AI Infrastructure Systems

Integrated AI Infrastructure Stacks

Colocation Based AI Infrastructure - By End User Segment (In Value%)

Cloud and Hyperscale Providers

Government and Public Sector Agencies

Telecommunications Operators

Large Enterprises and Industrial Groups

Research and Academic Institutions - By Procurement Channel (In Value%)

Direct OEM Procurement

System Integrator Led Procurement

Government Tender and Framework Contracts

Cloud Marketplace Procurement

Colocation and Managed Infrastructure Contracts - By Material / Technology (in Value %)

GPU and Accelerator Based Systems

High Performance CPU AI Systems

Silicon Photonics Interconnect Technology

Advanced Cooling and Thermal Systems

AI Optimized Storage and Memory Technology

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (Compute Performance Density, Energy Efficiency, Cooling Technology, Accelerator Integration, Network Bandwidth, Scalability Architecture, Deployment Model Flexibility, Sovereignty Compliance, Total Cost of Ownership)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Atos

OVHcloud

Orange Business

Thales

Schneider Electric

Capgemini

Dassault Systèmes

Eviden

Nvidia

Intel

AMD

HPE

Dell Technologies

Lenovo

Cisco

- Cloud providers expanding sovereign AI regions within France

- Government agencies investing in national AI compute capacity

- Telecom operators deploying edge AI for 5G services

- Industrial enterprises adopting on premise AI infrastructure

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now