Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the France car finance market reached approximately USD 215 billion in outstanding automotive credit value according to Banque de France consumer credit statistics and the European Automobile Manufacturers Association. The market is driven by high vehicle ownership demand, strong penetration of leasing and loan-based purchasing models, and increasing integration of financing solutions within dealership networks. Financial institutions, captive automotive finance companies, and digital lending platforms collectively support vehicle purchases through structured installment financing and flexible leasing contracts for consumers and corporate fleet buyers.

Paris, Lyon, Marseille, Toulouse, and Lille dominate the France car finance ecosystem because of their high vehicle ownership density, large dealership networks, and strong presence of financial institutions offering consumer credit services. Urban regions host the headquarters of major automotive banks and leasing firms, enabling rapid financing approvals and integrated dealership lending systems. Strong economic activity, higher disposable income levels, and the concentration of automotive retail infrastructure contribute to the dominance of these metropolitan markets in vehicle financing adoption.

Market Segmentation

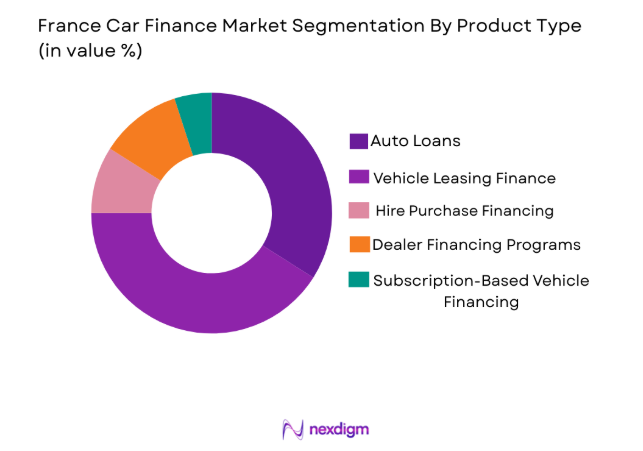

By Product Type

France car finance market is segmented by product type into auto loans, vehicle leasing finance, hire purchase financing, dealer financing programs, and subscription-based vehicle financing. Recently, vehicle leasing finance has a dominant market share due to factors such as consumer preference for lower upfront costs, flexible contract terms, strong brand-backed leasing programs from automakers, and tax advantages for corporate fleet operators. Leasing solutions allow drivers to access newer vehicles without full ownership commitment, which aligns with evolving mobility trends and technology upgrades. Corporate fleet managers also favor leasing structures because they simplify vehicle replacement cycles and reduce long-term depreciation risk. Automotive manufacturers actively promote leasing through captive finance divisions, strengthening its market position.

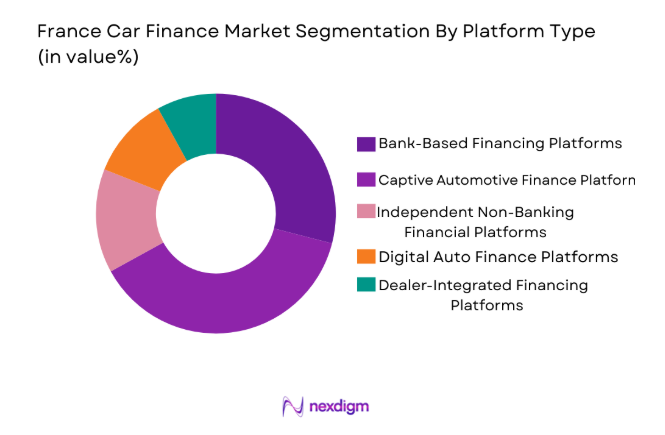

By Platform Type

France car finance market is sermented by platform type into bank-based financing platforms, captive automotive finance platforms, independent non-banking financial platforms, digital auto finance platforms, and dealer-integrated financing platforms. Recently, captive automotive finance platforms have a dominant market share due to their strong partnerships with vehicle manufacturers and dealership networks across France. These platforms offer competitive financing packages bundled directly with vehicle purchases, simplifying the transaction process for consumers. Automakers provide attractive interest structures and loyalty incentives through captive lenders, encouraging customers to finance vehicles through affiliated institutions. Their deep integration within dealership sales channels significantly accelerates loan approvals and increases financing penetration.

Competitive Landscape

The France car finance market is moderately consolidated with several large financial institutions and manufacturer-backed captive finance companies controlling a significant portion of vehicle lending activity. Major automotive finance subsidiaries benefit from strong dealership integration and brand loyalty, while commercial banks and fintech lenders compete by offering flexible digital credit services. Competitive dynamics increasingly revolve around digital loan approvals, electric vehicle financing programs, and partnerships between automakers and financial institutions that streamline vehicle purchase financing.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Automotive Finance Model |

| BNP Paribas Personal Finance | 1953 | Paris, France | ~ | ~ | ~ | ~ | ~ |

| Crédit Agricole Consumer Finance | 1951 | Paris, France | ~ | ~ | ~ | ~ | ~ |

| RCI Banque | 1924 | Paris, France | ~ | ~ | ~ | ~ | ~ |

| Santander Consumer Finance France | 1987 | Madrid, Spain | ~ | ~ | ~ | ~ | ~ |

| ALD Automotive | 1946 | Paris, France | ~ | ~ | ~ | ~ | ~ |

France Car Finance Market Analysis

Growth Drivers

Rising Vehicle Leasing Adoption Among Consumers and Corporate Fleets:

The increasing popularity of vehicle leasing among both individual consumers and corporate fleet operators is significantly driving growth in the France car finance market. Leasing arrangements allow drivers to access newer vehicles with lower upfront costs while spreading payments over predictable monthly installments. Businesses increasingly rely on leasing structures because they simplify fleet management and allow periodic upgrades without the long-term depreciation risks associated with ownership. Automotive manufacturers actively promote leasing programs through captive finance divisions integrated within dealership networks across France. This integration streamlines the vehicle purchasing process because customers can arrange financing simultaneously with vehicle selection. Consumers are also attracted to leasing because contracts often include maintenance services and flexible upgrade options at the end of the lease term. The growth of electric vehicles further strengthens leasing demand because consumers prefer financing options that allow them to switch to newer battery technologies more frequently. Financial institutions and automotive finance subsidiaries have developed digital platforms that accelerate leasing approvals and reduce documentation complexity. As urban mobility patterns evolve and consumers prioritize flexibility over ownership, leasing continues to expand rapidly as a preferred vehicle financing structure.

Expansion of Digital Auto Financing Platforms Across Automotive Retail Networks:

The rapid digitization of automotive financing services is transforming how vehicle loans and leasing agreements are processed throughout France. Financial institutions increasingly deploy digital platforms that allow customers to complete credit applications, documentation, and approvals entirely online. These platforms integrate advanced credit scoring algorithms and automated underwriting systems that significantly reduce approval times compared with traditional lending models. Consumers benefit from improved transparency because digital tools provide instant loan simulations and financing comparisons across different lenders. Automotive dealerships also integrate digital financing portals directly into their sales platforms, enabling customers to secure financing during the vehicle purchase process without visiting banks separately. Fintech companies are entering the automotive lending ecosystem with specialized platforms that provide real-time credit decisions and personalized loan offers. Digital onboarding technologies reduce operational costs for lenders while improving customer experience and accessibility. The increasing adoption of mobile banking and online credit services further accelerates the transition toward digital vehicle financing solutions. As financial institutions continue investing in advanced lending technologies, digital platforms are expected to play an increasingly central role in automotive finance distribution across the country.

Market Challenges

Strict Consumer Credit Regulations and Compliance Requirements in European Financial Markets:

Regulatory oversight within the European financial system imposes strict compliance obligations on institutions offering vehicle financing services in France. Financial regulators require lenders to maintain rigorous credit risk assessment procedures before approving consumer loans, which can limit financing accessibility for certain customer segments. Compliance with consumer protection frameworks and transparency requirements also increases administrative complexity for financial institutions and captive automotive finance providers. Lenders must conduct thorough affordability assessments and verify borrower income stability before issuing vehicle loans or leasing agreements. These compliance measures protect consumers from excessive debt exposure but may slow loan approval timelines and reduce financing penetration in certain markets. Regulatory agencies also require detailed disclosure of interest rates, contract terms, and associated fees to ensure transparency in consumer lending. Financial institutions must invest heavily in regulatory reporting infrastructure and compliance monitoring systems to maintain adherence to evolving policies. European data protection regulations further influence automotive finance platforms by requiring secure handling of personal financial information during credit assessments. As financial oversight continues evolving across European markets, lenders operating in France must constantly adapt their systems and procedures to remain compliant.

Interest Rate Volatility Affecting Consumer Borrowing Capacity for Vehicle Purchases:

Fluctuations in interest rates significantly influence the affordability of automotive financing products in France. When lending rates increase, monthly installment payments for vehicle loans and leases also rise, which can discourage consumers from purchasing new vehicles through financing arrangements. Higher financing costs can reduce demand for premium vehicles and push consumers toward used vehicles or lower-priced models. Financial institutions must carefully balance loan pricing strategies to remain competitive while maintaining profitability under changing monetary conditions. Automotive manufacturers sometimes respond by offering subsidized financing programs through captive lenders to maintain vehicle sales momentum. However, sustained interest rate increases may still reduce overall credit demand in the automotive sector. Corporate fleet operators may also delay vehicle replacement cycles when financing costs become significantly higher. This environment creates uncertainty for automotive lenders and dealerships that depend heavily on financed vehicle purchases. Financial institutions must continuously adjust credit policies and risk management strategies to adapt to evolving monetary conditions while sustaining automotive lending volumes.

Opportunities

Rapid Expansion of Electric Vehicle Financing Programs Across France:

The accelerating transition toward electric vehicles presents a significant opportunity for automotive finance providers operating in France. Electric vehicle adoption is supported by government incentives, environmental policies, and growing consumer awareness of sustainable mobility solutions. Financing companies can develop specialized loan and leasing products designed specifically for electric vehicles, including flexible battery upgrade options and maintenance packages. Captive automotive lenders associated with electric vehicle manufacturers often introduce attractive financing packages to stimulate early adoption among consumers. Financial institutions also collaborate with dealerships to create bundled financing solutions that include charging infrastructure installation and service contracts. As electric vehicle technologies evolve rapidly, financing solutions that allow drivers to upgrade vehicles frequently become particularly attractive. Digital financing platforms further simplify the approval process for electric vehicle loans, improving accessibility for first-time EV buyers. Financial institutions that develop tailored credit solutions for electric vehicles will gain a competitive advantage in the expanding sustainable mobility ecosystem.

Integration of Fintech Technologies in Automotive Lending Ecosystems:

The emergence of fintech-driven lending platforms creates substantial opportunities for innovation within the France car finance market. Fintech companies deploy advanced analytics, machine learning algorithms, and alternative credit scoring models to evaluate borrower risk more accurately. These technologies enable lenders to approve loans faster and extend financing to consumer segments that traditional banks may previously have rejected. Digital verification tools allow customers to upload documents and complete credit assessments entirely online without visiting financial institutions physically. Fintech platforms also enable automotive dealerships to integrate real-time credit approvals directly into their sales workflows. Enhanced data analytics improve loan portfolio management and allow lenders to personalize financing offers based on customer behavior patterns. These technologies significantly reduce administrative costs and processing time while improving customer satisfaction. As fintech firms continue collaborating with automotive manufacturers and financial institutions, technological

Future Outlook

The France car finance market is expected to evolve steadily over the next five years as digital lending technologies, electric vehicle financing programs, and integrated dealership credit platforms expand across the automotive sector. Financial institutions are investing heavily in digital credit assessment systems and automated loan approval processes. Government support for sustainable transportation will also encourage financing packages tailored for electric vehicles. As mobility patterns continue shifting toward flexible ownership models, leasing and subscription financing structures are projected to expand significantly across the country.

Major Players

- BNP Paribas Personal Finance

- Crédit Agricole Consumer Finance

- Société Générale Equipment Finance

- Crédit Mutuel Leasing

- La Banque Postale Consumer Finance

- RCI Banque

- PSA Finance

- Volkswagen Financial Services France

- Toyota Financial Services France

- Mercedes-Benz Financial Services France

- BMW Financial Services France

- Santander Consumer Finance France

- ALD Automotive

- Arval BNP Paribas

- CGI Finance

Key Target Audience

- Automotive manufacturers

- Automotive dealerships and distribution networks

- Vehicle leasing companies

- Fleet management service providers

- Investments and venture capitalist firms

- Government and regulatory bodies

- Commercial banks and lending institutions

- Automotive technology solution providers

Research Methodology

Step 1: Identification of Key Variables

Researchers identify key variables influencing the France car finance market including vehicle sales trends, consumer credit penetration, leasing adoption, and regulatory frameworks affecting automotive lending. These variables establish the foundational framework for analyzing automotive financing demand.

Step 2: Market Analysis and Construction

Market analysts evaluate financial institution reports, automotive sales statistics, banking credit databases, and mobility trends to construct the market structure. Data triangulation is used to validate lending volumes and financing adoption patterns across automotive sectors.

Step 3: Hypothesis Validation and Expert Consultation

Industry specialists including automotive lenders, dealership executives, and financial analysts validate the research assumptions. Their insights help confirm the accuracy of financing trends, digital lending adoption, and emerging electric vehicle financing strategies.

Step 4: Research Synthesis and Final Output

Collected data is synthesized using statistical modeling and financial trend analysis to produce a comprehensive market assessment. Final outputs integrate macroeconomic indicators, financial sector insights, and automotive industry developments to ensure research reliability.

- Executive Summary

- France car finance Market Research Methodology

(Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expansion of vehicle leasing and subscription financing models across France

Increasing consumer preference for flexible payment financing structures

Growing adoption of digital lending platforms within automotive financing ecosystems - Market Challenges

Strict credit risk regulations impacting consumer lending approvals

Rising interest rate environment affecting vehicle financing affordability

Complex compliance requirements under European financial regulatory frameworks - Market Opportunities

Expansion of digital auto financing platforms for faster loan approvals

Growing demand for electric vehicle financing packages

Partnerships between fintech platforms and automotive dealerships - Trends

Increasing penetration of online vehicle financing applications

Integration of AI-based credit scoring in automotive lending

Growth of subscription-based vehicle ownership models

Expansion of used vehicle financing services

Rising collaboration between OEMs and financial institutions - Government Regulations & Defense Policy

EU consumer credit regulatory framework influencing vehicle financing

Environmental regulations encouraging electric vehicle financing incentives

Financial supervision policies by French banking authorities - SWOT Analysis

Stakeholder and Ecosystem Analysis - Porter’s Five Forces Analysis

Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Auto Loans

Vehicle Leasing Finance

Hire Purchase Financing

Dealer Financing Programs

Subscription-Based Vehicle Financing - By Platform Type (In Value%)

Bank-Based Financing Platforms

Captive Automotive Finance Platforms

Independent Non-Banking Financial Platforms

Digital Auto Finance Platforms

Dealer-Integrated Financing Platforms - By Fitment Type (In Value%)

New Vehicle Financing

Used Vehicle Financing

Refinancing Programs

Balloon Payment Financing

Flexible Payment Financing - By EndUser Segment (In Value%)

Individual Consumers

Corporate Fleet Operators

SME Business Vehicle Buyers

Vehicle Rental Companies

Government and Public Sector Fleets - By Procurement Channel (In Value%)

Dealership Financing

Direct Bank Financing

Online Auto Finance Platforms

Broker-Based Financing

OEM Captive Finance Channels - By Material / Technology (in Value %)

Digital Loan Processing Systems

AI-Based Credit Assessment Platforms

Blockchain-Based Loan Verification Systems

Telematics-Integrated Leasing Platforms

Automated Risk Analytics Systems

- Market structure and competitive positioning

Market share snapshot of major players - CrossComparison Parameters (Financing Model, Loan Tenure Options, Interest Rate Structures, Digital Application Capability, Dealer Network Integration)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

BNP Paribas Personal Finance

Crédit Agricole Consumer Finance

Société Générale Equipment Finance

Crédit Mutuel Leasing

La Banque Postale Consumer Finance

RCI Banque

PSA Finance

Volkswagen Financial Services France

Toyota Financial Services France

Mercedes-Benz Financial Services France

BMW Financial Services France

Santander Consumer Finance France

ALD Automotive

Arval BNP Paribas

CGI Finance

- Increasing consumer adoption of financing solutions for personal vehicle purchases

- Corporate fleet operators relying on leasing models for cost optimization

- SME businesses utilizing structured financing for commercial vehicle acquisition

- Rental and mobility service providers expanding financed fleet procurement

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-203

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now