Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The France diagnostic labs market is valued at USD ~ billion based on a recent historical assessment, with increasing demand for advanced diagnostic tools, rising prevalence of chronic diseases, and the adoption of personalized medicine driving market growth. The expansion of healthcare facilities, government investments, and advancements in technology like artificial intelligence (AI) and molecular diagnostics further fuel the market’s growth. Moreover, the French healthcare system’s emphasis on early disease detection and preventive care plays a significant role in driving the demand for diagnostic services.

Paris, Lyon, and Marseille are leading cities in France’s diagnostic labs market, driven by their strong healthcare infrastructure and concentration of hospitals, medical research centers, and universities. Paris, with its advanced healthcare ecosystem, serves as a hub for innovation and diagnostic testing. Lyon benefits from its extensive biotech and healthcare sectors, fostering technological advancements in diagnostics. Marseille’s medical tourism and proximity to southern European markets also make it a significant player in the diagnostic services industry, particularly in the diagnostic testing of rare diseases.

Market Segmentation

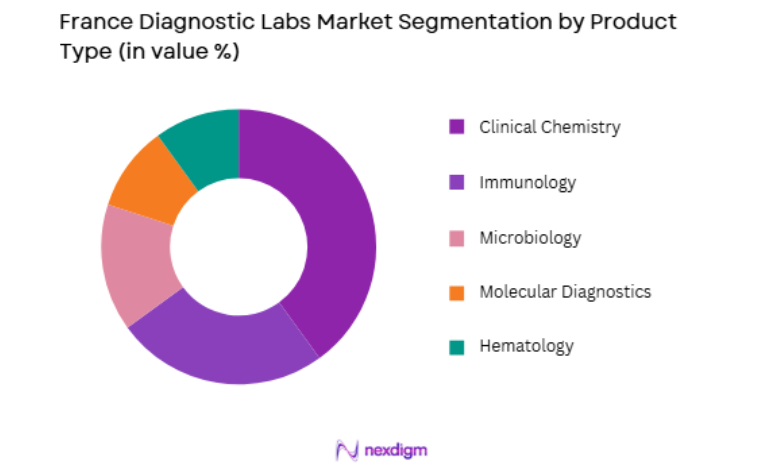

By Product Type

The France diagnostic labs market is segmented by product type into clinical chemistry, immunology, microbiology, molecular diagnostics, and hematology. Clinical chemistry holds the dominant market share due to its widespread use in disease detection, including for diabetes, cardiovascular diseases, and kidney function. The increasing prevalence of these conditions has boosted the demand for clinical chemistry diagnostics, making it a critical component in preventive healthcare. Clinical chemistry’s advanced technologies and their integration with automated systems further contribute to its dominance in the French diagnostic labs market.

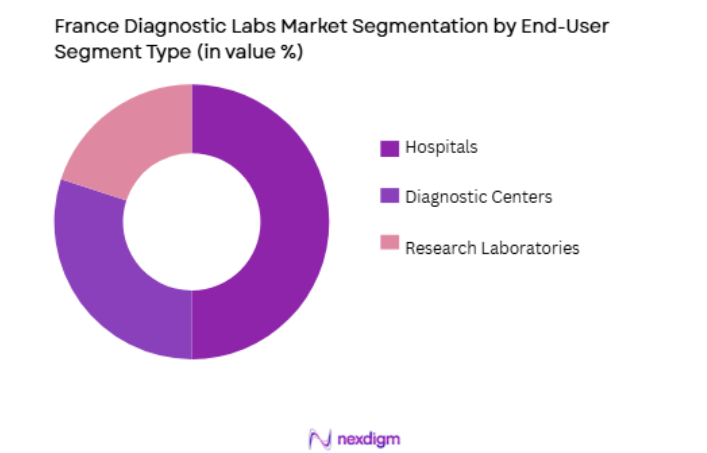

By End-User Segment

The market is segmented by end-user Segment into hospitals, diagnostic centers, and research laboratories. Hospitals currently dominate the market due to their large patient volumes and integrated diagnostic services. Hospitals in France often have in-house diagnostic labs offering a broad range of testing services, from routine blood tests to specialized diagnostics. The demand for diagnostic services in hospitals is also supported by the French healthcare system’s focus on improving patient care and reducing hospital readmission rates through early diagnosis and monitoring of diseases.

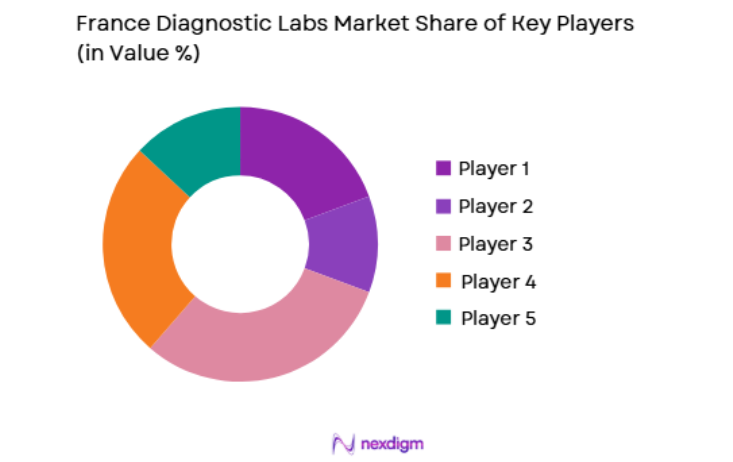

Competitive Landscape

The France diagnostic labs market is competitive, with several large players and emerging diagnostic companies innovating in molecular diagnostics, AI-based technologies, and laboratory automation. Key players in the market focus on expanding their service offerings, improving diagnostic accuracy, and enhancing operational efficiency through advanced technologies. Partnerships, mergers, and acquisitions are common strategies used by leading companies to expand their market presence and broaden their diagnostic capabilities. Government-backed initiatives promoting digital health and precision medicine also encourage market consolidation and technological innovation.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Additional Parameter |

| BioMérieux | 1963 | Marcy-l’Étoile, France | ~ | ~ | ~ | ~ | ~ |

| Siemens Healthineers | 1847 | Erlangen, Germany | ~ | ~ | ~ | ~ | ~ |

| Abbott Laboratories | 1888 | Chicago, USA | ~ | ~ | ~ | ~ | ~ |

| Thermo Fisher Scientific | 1956 | Waltham, USA | ~ | ~ | ~ | ~ | ~ |

| Roche Diagnostics | 1896 | Basel, Switzerland | ~ | ~ | ~ | ~ | ~ |

France Diagnostic Labs Market Analysis

Growth Drivers

Aging Population and Increased Prevalence of Chronic Diseases

One of the primary growth drivers for the France diagnostic labs market is the aging population and the increased prevalence of chronic diseases, such as diabetes, cardiovascular diseases, and cancer. As the population ages, the demand for diagnostic testing grows, as older adults are more prone to developing chronic conditions that require continuous monitoring and early detection. With an estimated 20% of the French population over 65 years old and the continued rise in lifestyle-related diseases, there is a growing need for reliable diagnostic solutions. Healthcare providers in France are increasingly focusing on preventive care, which includes early diagnosis and monitoring of chronic diseases, thus further driving the demand for diagnostic lab services. This shift towards preventive care aligns with government healthcare policies aimed at improving health outcomes and reducing long-term healthcare costs, reinforcing the growth of the diagnostic labs sector.

Technological Advancements and Integration of AI in Diagnostics

Another significant growth driver is the continuous technological advancements in diagnostic tools and the integration of artificial intelligence (AI) in diagnostics. The adoption of AI and machine learning technologies in diagnostic processes has led to enhanced accuracy, faster turnaround times, and more efficient workflows. In particular, molecular diagnostics, radiology, and laboratory automation have benefited from AI applications, improving diagnostic precision and supporting personalized medicine. The French healthcare system is increasingly adopting digital solutions, including telemedicine and telehealth, which require robust diagnostic capabilities. Additionally, the rise of home-based diagnostic tools, mobile health apps, and wearables is expanding the market for diagnostic tests that can be used outside traditional healthcare settings. These innovations make healthcare more accessible, enabling early detection and intervention, thus contributing to the growth of diagnostic services.

Market Challenges

Regulatory and Reimbursement Challenges

A major challenge facing the France diagnostic labs market is the complex regulatory environment and reimbursement challenges. While France has a well-established healthcare system with comprehensive reimbursement policies, the adoption of new diagnostic technologies and their integration into the public health system can be slow due to regulatory hurdles. Regulatory bodies must approve new diagnostic tests before they can be reimbursed by the national health insurance system. This process can take time, limiting the market potential for innovative diagnostic solutions. Furthermore, the evolving reimbursement landscape for diagnostics and the need for healthcare providers to navigate changing guidelines and policies pose a challenge for both new entrants and established players. Ensuring that diagnostic tests meet regulatory standards while maintaining cost-effectiveness for patients and providers is critical for market growth.

Infrastructure and Integration Challenges in Rural Areas

Another significant challenge is the lack of diagnostic infrastructure in rural areas of France. While urban areas like Paris and Lyon have advanced healthcare facilities, rural regions still struggle with limited access to diagnostic labs and healthcare professionals. This disparity in healthcare access is a major obstacle for telemedicine and remote diagnostics, as patients in rural areas may face difficulties accessing diagnostic services. Although the French government is investing in digital health solutions, there is a need for further infrastructure development in underserved areas. In addition, integrating telemedicine solutions with traditional healthcare systems in rural regions presents logistical challenges. Addressing these infrastructure gaps will be crucial for ensuring equitable access to diagnostic services across the country.

Opportunities

Expansion of Home-based and Point-of-Care Diagnostics

One of the key opportunities in the France diagnostic labs market is the expansion of home-based and point-of-care (POC) diagnostics. The increasing demand for convenient and accessible diagnostic solutions has led to the development of home testing kits and portable diagnostic devices. These solutions allow patients to monitor their health from the comfort of their homes, reducing the need for hospital visits and lowering healthcare costs. The COVID-19 pandemic has further accelerated the adoption of home-based diagnostics, particularly in areas such as COVID-19 testing and chronic disease management. With France’s strong healthcare infrastructure and growing consumer acceptance of at-home healthcare solutions, the market for home-based diagnostics is expected to expand significantly in the coming years. This shift towards POC diagnostics also creates opportunities for innovation in test accuracy, ease of use, and integration with digital health platforms, supporting market growth.

Growth in Molecular Diagnostics and Personalized Medicine

Another significant opportunity lies in the growth of molecular diagnostics and personalized medicine. The increasing focus on genomics, precision medicine, and targeted therapies is driving demand for advanced molecular diagnostic tests. France’s robust research and development sector, combined with strong government support for personalized healthcare, positions the country as a leader in molecular diagnostics. As more patients seek personalized treatment plans tailored to their genetic makeup, the demand for genetic testing and molecular diagnostics will continue to rise. The French healthcare system’s push for personalized medicine, along with advancements in next-generation sequencing and biomarker discovery, presents significant opportunities for diagnostic companies to develop and commercialize new testing solutions. These advancements will not only enhance patient outcomes but also reduce healthcare costs by ensuring more effective treatments, contributing to the overall growth of the diagnostic labs market.

Future Outlook

The future outlook for the France diagnostic labs market is promising, with continued growth expected over the next five years. The adoption of digital health solutions, including remote diagnostics and AI-driven diagnostics, will further enhance the efficiency and accuracy of diagnostic testing. Government support for healthcare innovation, coupled with rising consumer demand for preventive care and personalized medicine, will drive the market’s expansion. The market is also expected to benefit from increased investments in molecular diagnostics, point-of-care testing, and home-based diagnostic solutions. With advancements in diagnostic technology, regulatory support, and expanding access to healthcare services, the France diagnostic labs market is poised for sustained growth.

Major Players

- BioMérieux

- Siemens Healthineers

- Abbott Laboratories

- Thermo Fisher Scientific

- Roche Diagnostics

- Beckman Coulter

- Medtronic

- Becton, Dickinson and Company

- Agilent Technologies

- Philips Healthcare

- PerkinElmer

- Johnson & Johnson

- Illumina

- Abbott Diagnostics

- Labcorp

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Healthcare providers

- Diagnostic technology companies

- Biotech companies

- Research laboratories

- Medical insurance companies

Research Methodology

Step 1: Identification of Key Variables

The key variables, including diagnostic testing trends, government policies, and technological innovations, are identified through secondary research and expert consultations to drive market projections.

Step 2: Market Analysis and Construction

Market data is analyzed from reputable sources, including market reports, government publications, and industry insights, to develop a comprehensive view of the France diagnostic labs market.

Step 3: Hypothesis Validation and Expert Consultation

Insights from healthcare professionals and industry experts are used to validate market hypotheses, ensuring accuracy in understanding growth drivers, challenges, and opportunities.

Step 4: Research Synthesis and Final Output

The research findings are synthesized to create a detailed market report, providing a clear outlook on the France diagnostic labs market, including key trends, growth drivers, and market challenges.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Technological Advancements in Diagnostic Equipment

Increasing Incidences of Chronic Diseases

Government Investments in Healthcare - Market Challenges

High Operational Costs

Regulatory Compliance and Certification Challenges

Lack of Skilled Technicians - Market Opportunities

Point-of-Care Diagnostic Expansion

Demand for Personalized Diagnostics

Technological Innovations in Genetic Testing - Trends

Integration of AI in Diagnostic Systems

Shift Towards Minimally Invasive Diagnostic Procedures - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Clinical Diagnostic Labs

Pathology Diagnostic Labs

Microbiology Labs

Genetic Testing Labs

Immunoassay Labs - By Platform Type (In Value%)

Automated Diagnostic Platforms

Manual Diagnostic Platforms

Cloud-based Diagnostic Platforms

Point-of-Care Diagnostic Platforms - By Fitment Type (In Value%)

On-premise Solutions

Cloud-based Solutions

Hybrid Solutions

Integrated Solutions - By End User Segment (In Value%)

Hospitals

Private Diagnostic Centers

Public Healthcare Facilities

- Market Share Analysis

- Cross Comparison Parameters (System Type, Platform Type, Procurement Channel, End User Segment, Fitment Type, Technological Integration, Market Penetration, Service Availability, Regulatory Compliance, Data Security, Cost Efficiency)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Laboratoires Cerba

Biomérieux

Laboratoire Laborama

Laboratoires EOL

Laboratoires Elsan

Laboratoire Pasteur

Laboratoire Atlantique

Luxe Diagnostics

Eurofins Scientific

Ortho Clinical Diagnostics

Laboratoire Joly

Medica

DGLAB

Laboratoire des Champs Elysées

Laboratoire Biorad

- Hospitals Expanding Diagnostic Services

- Private Diagnostic Centers Adopting Cutting-Edge Technologies

- Public Healthcare Expanding Access to Diagnostics

- Research Institutions Innovating in Diagnostic Methods

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now