Download PDF

Download PDF Download PDF

Download PDFMarket Overview

France Electric Bus market demonstrates strong development within the European clean mobility ecosystem due to aggressive decarbonization targets and government-backed public transportation modernization initiatives. Based on a recent historical assessment, the market generated approximately USD ~ billion driven by large scale procurement programs initiated by national transit authorities and municipal governments. Public transportation electrification policies encourage fleet replacements with zero emission buses across urban networks. National subsidies, European climate funding mechanisms, and battery technology improvements continue to accelerate fleet electrification projects across metropolitan transport networks.

Major metropolitan regions dominate the France Electric Bus market due to dense public transportation systems, advanced charging infrastructure deployment, and supportive regional sustainability programs. Cities such as Paris, Lyon, Marseille, and Toulouse lead adoption because local governments prioritize electrified transit fleets to reduce urban emissions and improve air quality. Large municipal transport authorities operate extensive bus networks that require high-capacity vehicles with advanced energy systems. These cities also benefit from strong industrial ecosystems including electric bus manufacturing, battery supply chains, and specialized mobility technology providers.

Market Segmentation

By Product Type

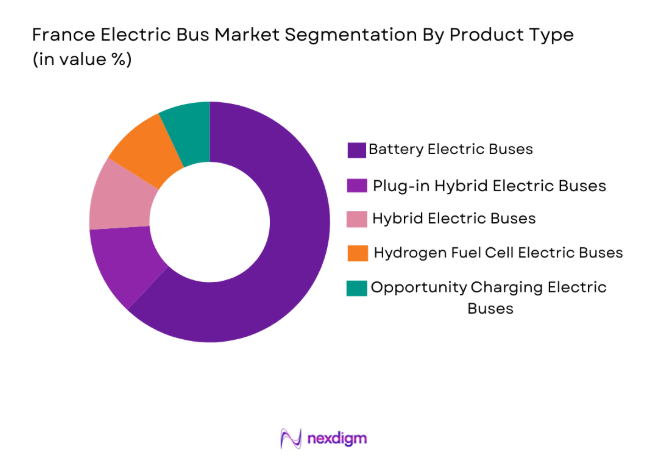

France Electric Bus market is segmented by product type into battery electric buses, plug-in hybrid electric buses, hybrid electric buses, hydrogen fuel cell electric buses, and opportunity charging electric buses. Recently, battery electric buses dominate the market due to strong government support for zero emission transport. Established charging infrastructure across urban depots supports widespread fleet adoption.

Public transit operators prefer battery electric fleets due to lower operating and maintenance costs. European climate policies also promote the replacement of diesel buses with electric alternatives. Continuous improvements in battery technology further strengthen the dominance of battery electric buses.

By Platform Type

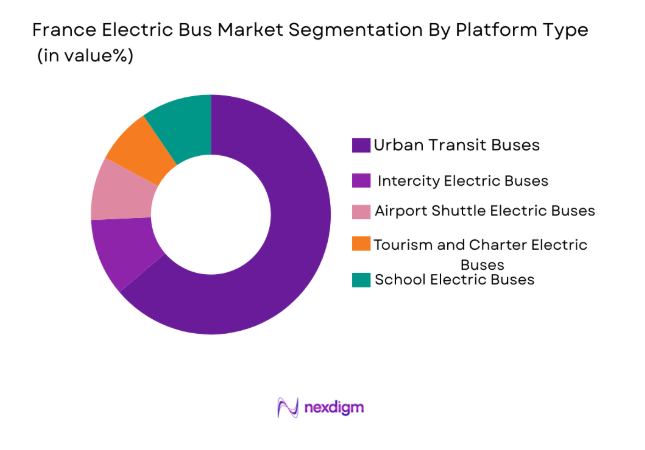

France Electric Bus market is segmented by platform type into urban transit buses, intercity electric buses, airport shuttle electric buses, tourism and charter electric buses, and school electric buses. Recently, urban transit buses dominate the market due to strong municipal electrification programs and high passenger demand in metropolitan transport networks. Urban bus routes follow predictable schedules and depot operations, making charging infrastructure easier to deploy and manage. Government funding and city level sustainability initiatives also support the rapid replacement of diesel fleets with electric urban transit buses.

Competitive Landscape

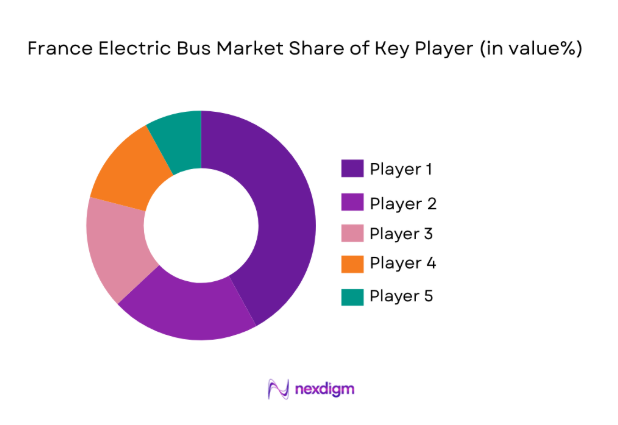

The France Electric Bus market demonstrates moderate consolidation with a combination of established European bus manufacturers and emerging global electric mobility companies competing for public transit contracts. Government procurement programs strongly influence competitive positioning because municipal transport authorities typically award large multi-year fleet electrification contracts. Companies with strong battery technology integration, charging infrastructure partnerships, and advanced vehicle platforms maintain competitive advantages. European manufacturers dominate urban fleet supply while global electric mobility firms increasingly expand presence through technology partnerships and localized manufacturing strategies.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Fleet Electrification Capability |

| BYD Europe | 1995 | Shenzhen China | ~ | ~ | ~~ | ~ | ~ |

| Solaris Bus & Coach | 1996 | Poland | ~ | ~ | ~ | ~ | ~ |

| Iveco Bus | 1975 | France | ~ | ~ | ~ | ~ | ~ |

| Volvo Buses | 1928 | Sweden | ~ | ~ | ~ | ~ | ~ |

| Mercedes Benz Buses | 1895 | Germany | ~ | ~ | ~ | ~ | ~ |

France Electric Bus Market Analysis

Growth Drivers

Expansion of Renewable Energy Integration Across National Grid Infrastructure:

France is undergoing a significant transformation in its electricity generation landscape as renewable energy sources such as solar and wind power increasingly contribute to the national electricity supply. Renewable energy expansion has created a strong requirement for flexible energy storage systems capable of balancing variable electricity generation and maintaining grid stability during fluctuating supply conditions. Utility operators and energy developers are investing in large scale battery energy storage installations that allow excess renewable electricity to be stored during periods of high generation and released during peak demand periods when renewable output declines. Grid scale battery systems also help electricity network operators maintain frequency stability and manage voltage fluctuations across transmission networks that experience irregular renewable power injection. Energy storage infrastructure plays a central role in supporting France’s national energy transition strategies which aim to reduce dependence on conventional fossil fuel power generation while expanding renewable energy capacity. Renewable energy developers frequently integrate battery storage into solar and wind projects to enhance operational reliability and improve electricity delivery to the national grid. Battery energy storage also enables improved energy arbitrage opportunities by allowing operators to store electricity during periods of low demand and release it when market electricity prices increase. Government policy frameworks supporting decarbonization and clean energy development further strengthen investment in grid scale battery storage infrastructure across several regions. The continuous deployment of renewable generation facilities across the national electricity system ensures that battery energy storage solutions remain essential for maintaining stable electricity supply while supporting the long term transition toward low carbon energy infrastructure.

Rising Demand for Grid Stability and Energy Infrastructure Modernization:

The increasing complexity of electricity distribution networks across France is driving strong demand for advanced battery energy storage technologies that can support grid modernization initiatives and improve overall electricity reliability. As electricity consumption patterns evolve with increasing electrification of transportation, industrial systems, and residential energy applications, grid operators require more sophisticated infrastructure capable of managing dynamic energy flows across multiple distribution networks. Battery energy storage systems provide grid operators with flexible tools that help manage peak electricity demand, stabilize voltage fluctuations, and support frequency regulation across interconnected electricity networks. Modern electricity grids must accommodate increasing renewable power generation alongside traditional power plants, which creates operational challenges that require advanced storage technologies to ensure balanced electricity supply and demand conditions. Battery storage installations allow energy operators to quickly respond to sudden electricity demand spikes and unexpected fluctuations in renewable energy generation. National electricity infrastructure programs focusing on smart grid deployment and digital energy management platforms further support the integration of battery storage systems into modern electricity networks. Advanced monitoring technologies allow energy storage operators to optimize system performance while maintaining efficient energy distribution across the grid. Continuous modernization of electricity infrastructure combined with increasing electrification across transportation and industrial sectors further accelerates the need for large scale battery energy storage installations throughout the national electricity network.

Market Challenges

High Capital Investment Requirements for Large Scale Energy Storage Infrastructure:

The deployment of battery energy storage systems requires substantial capital investment due to the high cost of advanced battery technologies, system integration equipment, and supporting electrical infrastructure required for grid connectivity. Utility scale energy storage projects typically require large financial commitments from energy developers and electricity operators before installations can become operational. Battery systems must be integrated with advanced power electronics, monitoring technologies, and safety systems that ensure reliable performance within electricity distribution networks. These technological requirements significantly increase the total cost of energy storage infrastructure development compared with conventional electricity generation technologies. Financial investors often require clear long term revenue mechanisms and regulatory support before committing capital to large energy storage installations. Electricity markets must also establish pricing frameworks that reward energy storage operators for providing grid services such as frequency regulation, load balancing, and reserve capacity. In some cases the financial returns from energy storage projects remain uncertain due to evolving electricity market structures and regulatory frameworks governing energy storage participation. Project developers must also allocate resources for site preparation, grid connection infrastructure, and regulatory compliance before construction of battery storage facilities can begin. Large scale battery installations require specialized engineering expertise and advanced safety systems that ensure operational reliability across electricity distribution networks. Despite growing interest in energy storage technologies, the high capital cost associated with battery energy storage infrastructure continues to represent a major barrier for widespread deployment across certain energy markets.

Supply Chain Dependency on Critical Battery Materials and Global Manufacturing Networks:

Battery energy storage technologies rely heavily on critical raw materials such as lithium, cobalt, nickel, and graphite that are sourced from global mining operations and processed through complex international supply chains. The availability and pricing of these materials significantly influence the overall cost structure of battery energy storage systems used in grid infrastructure projects. Fluctuations in raw material prices can increase manufacturing costs for battery technology providers and affect the economic feasibility of large scale energy storage installations. Many battery materials are concentrated within limited geographic regions, which creates potential supply chain vulnerabilities for energy storage developers operating in different global markets. Energy storage manufacturers must manage complex logistics networks that transport raw materials to battery production facilities before finished storage systems are delivered to project developers and energy utilities. Geopolitical developments, trade policies, and transportation disruptions can influence the availability of critical battery components required for large energy storage projects. Battery manufacturers also face growing regulatory expectations regarding responsible sourcing of raw materials and environmental sustainability standards for battery production. Recycling infrastructure for end of life batteries remains under development in many regions, which creates additional challenges related to long term material supply and environmental compliance. Energy companies and battery manufacturers are increasingly exploring alternative battery chemistries and recycling technologies that may reduce dependence on critical raw materials while strengthening supply chain resilience for energy storage systems.

Opportunities

Expansion of Hybrid Renewable Energy and Battery Storage Infrastructure Projects:

Hybrid energy infrastructure projects that combine renewable power generation with integrated battery storage systems are creating major opportunities for energy developers and technology providers operating in the battery energy storage ecosystem. Renewable power plants increasingly incorporate battery storage systems that allow electricity generated from solar and wind facilities to be stored and delivered during periods when generation declines or electricity demand increases. Hybrid renewable storage projects enable energy developers to maximize electricity output from renewable installations while ensuring consistent energy delivery to electricity distribution networks. Battery energy storage systems also allow renewable energy facilities to participate more effectively in electricity markets by storing excess generation during low demand periods and releasing stored electricity when market prices increase. Hybrid energy infrastructure improves overall energy system efficiency while reducing curtailment of renewable electricity generation during periods of surplus production. Governments supporting energy transition strategies frequently encourage the development of integrated renewable and storage infrastructure through supportive policy frameworks and infrastructure investment programs. Hybrid renewable storage projects can also strengthen grid resilience by providing backup electricity supply during unexpected power disruptions or extreme weather events that affect traditional electricity generation infrastructure. Continued expansion of renewable power generation across several regions ensures that hybrid renewable energy storage projects will remain a major opportunity within the battery energy storage industry.

Development of Smart Grid Technologies and Digital Energy Management Systems:

Advanced digital technologies and smart grid infrastructure are creating significant opportunities for battery energy storage systems to become central components of modern electricity management networks. Smart grids incorporate digital monitoring technologies, automated control systems, and advanced data analytics platforms that allow electricity operators to monitor energy flows across transmission and distribution networks in real time. Battery energy storage systems integrated into smart grid platforms can automatically respond to fluctuations in electricity demand and generation conditions while supporting efficient energy distribution across electricity networks. Digital energy management systems allow electricity operators to optimize battery charging and discharging cycles in order to maximize system efficiency and extend battery lifecycle performance. Smart grid technologies also enable distributed energy resources such as rooftop solar systems, microgrids, and community energy projects to interact more effectively with centralized electricity infrastructure. Battery storage systems play a critical role in enabling these distributed energy networks by providing flexible energy balancing capabilities that support stable electricity supply. As digital energy infrastructure continues to expand across modern electricity systems, battery energy storage technologies will increasingly serve as essential components that enhance grid flexibility, improve operational efficiency, and strengthen overall electricity network reliability.

Future Outlook

The France Electric Bus market is expected to expand steadily as public transportation electrification becomes central to national climate strategies and urban sustainability initiatives. Government funding programs and European environmental policies will continue to support fleet replacement programs across metropolitan transit networks. Advancements in battery technology, hydrogen mobility, and charging infrastructure will improve operational efficiency for transit operators. Increasing urbanization and sustainable mobility planning will further strengthen long term demand for electric buses across the national transportation ecosystem.

Major Players

- Solaris Bus & Coach

- Iveco Bus

- Volvo Buses

- Mercedes Benz Buses

- MAN Truck & Bus

- Irizar e-Mobility

- VDL Bus & Coach

- Yutong Bus

- Wrightbus

- CaetanoBus

- Temsa

- Alstom Mobility

- Heuliez Bus

- Proterra

Key Target Audience

- Public transportation authorities

- Electric bus manufacturers

- Battery technology companies

- Charging infrastructure providers

- Energy utilities

- Investments and venture capitalist firms

- Urban mobility infrastructure developers

Research Methodology

Step 1: Identification of Key Variables

Key variables such as vehicle electrification trends, transit fleet replacement rates, charging infrastructure development, and policy incentives are identified. These variables help define the boundaries of the France Electric Bus market and guide the analytical framework used during research.

Step 2: Market Analysis and Construction

Primary and secondary research sources including transport authorities, industry publications, government mobility programs, and corporate financial reports are analyzed. Market sizing models combine fleet deployment data with procurement programs to construct a comprehensive market structure.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts including electric mobility engineers, transit operators, and policy specialists validate key assumptions. Interviews and expert consultations refine technology adoption trends, procurement strategies, and infrastructure investment patterns across the electric bus ecosystem.

Step 4: Research Synthesis and Final Output

All validated insights are integrated into a structured market intelligence framework. Quantitative market estimates and qualitative insights are synthesized to produce a detailed analysis of the France Electric Bus market including competitive positioning and long term growth dynamics.

- Executive Summary

- Research Methodology

(Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Government decarbonization targets accelerating public transit electrification

Expansion of urban low emission zones encouraging zero emission bus adoption

National and EU funding programs supporting electric public transportation

Rapid improvements in battery efficiency and charging infrastructure

Growing municipal investments in sustainable urban mobility systems - Market Challenges

High upfront procurement costs for electric buses compared with diesel fleets

Charging infrastructure deployment challenges in dense urban depots

Battery replacement and lifecycle cost management concerns

Grid capacity limitations in large metropolitan transit depots

Operational adjustments required for fleet electrification planning - Market Opportunities

Integration of electric buses with renewable energy powered charging infrastructure

Expansion of hydrogen fuel cell buses for long distance transit routes

Growth of smart fleet management platforms for electric public transport - Trends

Expansion of overnight depot charging infrastructure across French cities

Increasing adoption of articulated electric buses for high passenger capacity routes

Development of battery swapping and fast opportunity charging systems

Partnerships between transit agencies and energy providers for charging solutions

Integration of telematics and predictive maintenance in electric bus fleets - Government Regulations & Defense Policy

National clean mobility policies promoting zero emission public transport fleets

European Union climate directives supporting urban transport electrification

Public procurement regulations prioritizing low emission transport systems - SWOT Analysis

Stakeholder and Ecosystem Analysis - Porter’s Five Forces Analysis

Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Battery Electric Buses

Plug-in Hybrid Electric Buses

Fuel Cell Electric Buses

Hybrid Electric Buses

Opportunity Charging Electric Buses - By Platform Type (In Value%)

Urban Transit Buses

Intercity Electric Buses

School Electric Buses

Airport Shuttle Electric Buses

Tourism and Charter Electric Buses - By Fitment Type (In Value%)

OEM Factory Integrated Systems

Retrofit Electrification Systems

Modular Electric Drivetrain Systems

Depot Charging Configurations

Opportunity Charging Configurations - By EndUser Segment (In Value%)

Public Transit Authorities

Municipal Transport Agencies

Private Transit Operators

Airport Transportation Operators

Tourism and Charter Bus Operators - By Procurement Channel (In Value%)

Government Public Tenders

Direct Procurement from Manufacturers

Public Private Partnership Procurement

Leasing and Fleet Financing Programs

Transport Authority Framework Agreements - By Material / Technology (in Value %)

Lithium-ion Battery Systems

Solid State Battery Technology

Hydrogen Fuel Cell Systems

Advanced Power Electronics Systems

Regenerative Braking Energy Systems

- Market structure and competitive positioning

Market share snapshot of major players

CrossComparison Parameters (Battery Capacity, Driving Range, Charging Technology, Vehicle Length, Passenger Capacity) - SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

BYD Europe

Solaris Bus & Coach

Alstom Mobility

Iveco Bus

Volvo Buses

Mercedes Benz eCitaro

MAN Truck & Bus

VDL Bus & Coach

Irizar e-mobility

Yutong Bus

Heuliez Bus

Wrightbus

CaetanoBus

Temsa

Proterra

- Public transit authorities expanding zero emission fleets to comply with national climate policies

- Municipal governments prioritizing electric buses for urban air quality improvement programs

- Private transit operators adopting electric buses to reduce long term fuel expenses

- Airport and tourism operators introducing electric shuttle fleets for sustainable transportation

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now