Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The France healthcare infrastructure market is valued at approximately USD ~ billion based on a recent historical assessment. The market is primarily driven by the rising demand for healthcare services due to France’s aging population, increased prevalence of chronic diseases, and advancements in medical technologies. Additionally, the government’s commitment to healthcare reforms and increased investment in the healthcare sector continue to contribute to the market’s growth. France’s advanced healthcare system and strong emphasis on improving public health drive the need for more modernized and expanded healthcare facilities.

Paris and Lyon are dominant cities in France’s healthcare infrastructure market due to their large population sizes, concentration of hospitals, and advanced healthcare facilities. Paris, being the capital, is home to several renowned hospitals and specialized healthcare centers, offering world-class services in fields like cardiology, oncology, and neurology. Lyon, with its focus on medical research and innovation, is also an important hub, especially for the biotechnology and pharmaceutical sectors. The healthcare infrastructure in these cities supports both local and international demand, making them central to the country’s healthcare landscape.

Market Segmentation

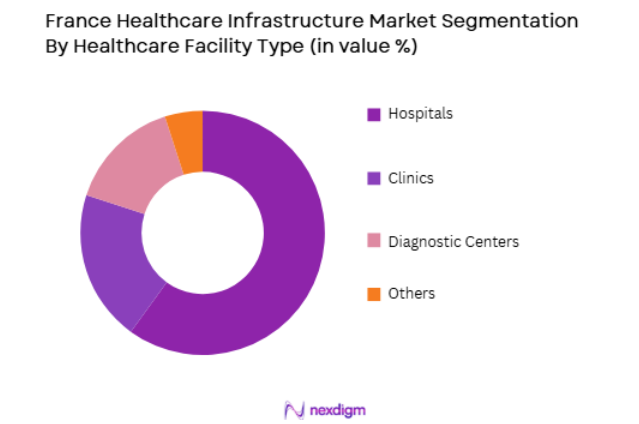

By Healthcare Facility Type

The France healthcare infrastructure market is segmented by healthcare facility type into hospitals, clinics, diagnostic centers, and others. Recently, hospitals have dominated the market share due to their comprehensive role in providing a wide range of medical services, from emergency care to complex surgeries. Hospitals in France, especially those in large cities like Paris and Lyon, are equipped with state-of-the-art medical technologies and offer specialized treatments, making them the go-to choice for patients. Additionally, public hospitals in France have a strong reputation for providing high-quality, affordable healthcare, which contributes to their dominance in the market. Moreover, the French government’s continued investment in the expansion and modernization of hospital infrastructure plays a vital role in maintaining the sector’s leadership.

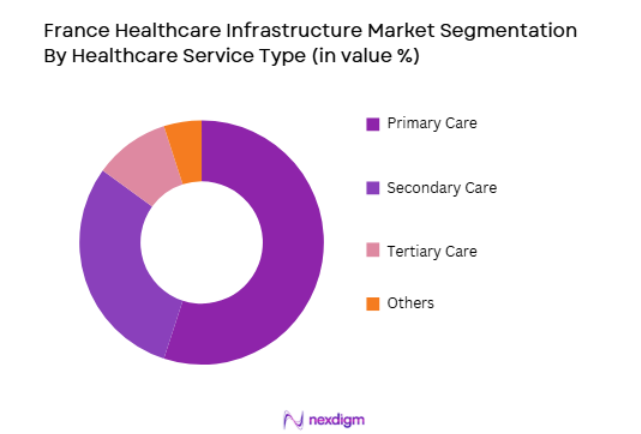

By Healthcare Service Type

The France healthcare infrastructure market is segmented by healthcare service type into primary care, secondary care, tertiary care, and others. Recently, primary care has dominated the market share due to its accessibility and the integral role it plays in France’s healthcare system. Primary care facilities, including general practitioners and family doctors, provide essential healthcare services and serve as the first point of contact for patients. The French healthcare system places a strong emphasis on primary care, with widespread availability of healthcare services across urban and rural areas. Additionally, the country’s public healthcare system ensures that primary care services remain affordable and accessible, contributing to their dominant market share.

Competitive Landscape

The competitive landscape of France’s healthcare infrastructure market is dominated by both public and private healthcare providers. The market sees significant involvement from government agencies that fund public healthcare institutions, ensuring universal access to healthcare services. The private sector, however, is becoming increasingly influential, with several private hospital chains and diagnostic centers offering specialized services to both local and international patients. Large hospital networks are expanding their reach through mergers, acquisitions, and partnerships with specialized medical centers. The French healthcare market also benefits from its strong regulatory framework, which ensures high standards of care across all levels of the healthcare system.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Additional Parameter |

| Assistance Publique-Hôpitaux de Paris | 1991 | Paris, France | ~ | ~ | ~ | ~ | ~ |

| Groupe Ramsay Santé | 1997 | Paris, France | ~ | ~ | ~ | ~ | ~ |

| Fondation de l’Assistance Publique | 1852 | Paris, France | ~ | ~ | ~ | ~ | ~ |

| Vivalto Santé | 2009 | Paris, France | ~ | ~ | ~ | ~ | ~ |

| Korian | 2003 | Paris, France | ~ | ~ | ~ | ~ | ~ |

France Healthcare Infrastructure Market Analysis

Growth Drivers

Aging Population and Rising Healthcare Demand

One of the key growth drivers for France’s healthcare infrastructure market is the aging population and the increasing demand for healthcare services. France has one of the highest proportions of elderly people in Europe, leading to a greater need for healthcare services that cater to chronic diseases, geriatric care, and long-term healthcare. The aging demographic is significantly contributing to the rising demand for specialized medical care, such as home healthcare, rehabilitation, and nursing homes. This trend is expected to persist, with healthcare providers in France focusing on expanding their services and infrastructure to meet the needs of an older population. The French government is also investing heavily in healthcare reforms that aim to improve elderly care services and increase the availability of specialized medical treatments, further driving growth in the healthcare infrastructure market. The rise in age-related health conditions, such as dementia and heart disease, requires a continuous expansion of healthcare facilities and services to address these growing demands.

Government Investment in Healthcare Infrastructure

Another major growth driver is the French government’s ongoing investment in healthcare infrastructure. The government continues to allocate substantial funding to modernize hospitals, build new healthcare facilities, and implement digital health solutions, such as telemedicine and electronic health records. This investment is intended to enhance access to healthcare services and improve the overall quality of care provided in both urban and rural areas. Furthermore, the French government’s initiatives to strengthen primary healthcare services are expected to further drive growth in the healthcare infrastructure market. In addition to expanding healthcare facilities, these investments also focus on adopting cutting-edge medical technologies to improve diagnostic and treatment capabilities. The government’s strong commitment to universal healthcare access ensures that healthcare infrastructure will continue to grow and evolve to meet the demands of the population.

Market Challenges

Rising Operational Costs

One of the key challenges facing the France healthcare infrastructure market is the rising operational costs associated with running healthcare facilities. Hospitals and clinics face significant expenses related to staffing, equipment maintenance, and medical technology upgrades. The high cost of acquiring and maintaining advanced medical equipment, such as MRI machines and robotic surgery systems, is particularly burdensome for smaller private healthcare providers and diagnostic centers. Public healthcare institutions also face increasing costs, particularly in the context of an aging population and the growing prevalence of chronic diseases, which require long-term care. Additionally, rising labor costs and the need for specialized healthcare professionals add to the financial burden of healthcare providers. This challenge is compounded by budgetary constraints in the public healthcare sector, making it difficult for some facilities to expand or modernize their infrastructure.

Regulatory and Bureaucratic Challenges

Regulatory compliance and bureaucratic challenges are also significant barriers to the growth of France’s healthcare infrastructure market. Healthcare providers in France must navigate complex regulations that govern everything from medical equipment standards to data protection and patient safety protocols. The strict regulatory environment can result in delays in the construction of new healthcare facilities and the implementation of new technologies. Moreover, healthcare providers must comply with national and EU regulations to ensure that their facilities meet the required standards, which can be time-consuming and costly. The need for continuous monitoring and auditing of healthcare services adds another layer of complexity for providers. Despite the regulatory framework being designed to ensure the highest standards of care, these compliance challenges can slow the pace of growth in the healthcare infrastructure sector.

Opportunities

Telemedicine and Digital Health Expansion

The expansion of telemedicine and digital health services presents a significant opportunity for the French healthcare infrastructure market. Telemedicine has gained traction in France in recent years, particularly following the COVID-19 pandemic, which highlighted the importance of remote healthcare services. France’s healthcare system has embraced digital health solutions, such as virtual consultations, remote monitoring, and electronic health records, to improve patient care and streamline healthcare delivery. The French government has supported the adoption of telemedicine by providing funding and regulatory frameworks that make it easier for healthcare providers to integrate digital health solutions. As telemedicine continues to evolve, it offers an opportunity to enhance access to healthcare services, particularly in rural areas where traditional healthcare infrastructure may be limited. The continued development of telehealth platforms and the integration of artificial intelligence (AI) in healthcare will further drive market growth.

Medical Tourism and International Patient Care

Medical tourism presents another major opportunity for Spain’s healthcare infrastructure market. France is already a well-known destination for international patients seeking high-quality medical care, particularly in specialized fields such as oncology, cardiology, and orthopedics. With its world-class hospitals, renowned healthcare professionals, and advanced medical technologies, France is well-positioned to attract medical tourists from around the world. The government’s support for medical tourism and the ongoing improvement of healthcare facilities will likely increase the number of international patients seeking treatment in France. As global demand for affordable, high-quality healthcare services grows, France’s medical tourism sector is expected to expand. Healthcare providers offering specialized services to international patients will further contribute to the growth of the healthcare infrastructure market in the coming years.

Future Outlook

The future outlook for France’s healthcare infrastructure market is strong, with steady growth expected over the next five years. The aging population, increasing demand for healthcare services, and government investments in healthcare infrastructure will continue to drive market expansion. Technological advancements, particularly in telemedicine and digital health, will also play a key role in transforming the healthcare landscape. The government’s commitment to improving healthcare access, especially in rural areas, will create further opportunities for infrastructure development. Additionally, France’s growing medical tourism sector will further bolster the market, with the country expected to remain a top destination for international patients seeking specialized treatments.

Major Players

- AssistancePublique-Hôpitaux de Paris

- Groupe Ramsay Santé

- Fondation de l’Assistance Publique

- Vivalto Santé

- Korian

- Pôle Santé République

- CHU de Bordeaux

- Clinique des Cèdres

- Fondation Santé des Etudiants de France

- Hôpital Foch

- Groupe Médipôle

- Hôpital de la Pitié-Salpêtrière

- Clinique Saint-Jean

- Hôpital Saint-Louis

- GHL Santé

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Healthcare providers

- Hospitals and clinics

- Pharmaceutical companies

- Medical device manufacturers

- Insurance providers

- Medical research organizations

Research Methodology

Step 1: Identification of Key Variables

The research identifies key market variables such as healthcare demand, government investment, regulatory frameworks, and technological advancements that influence the growth of healthcare infrastructure.

Step 2: Market Analysis and Construction

Data is collected from credible sources and analyzed using statistical models to construct a comprehensive market forecast, focusing on the healthcare infrastructure sector in France.

Step 3: Hypothesis Validation and Expert Consultation

Hypotheses regarding market trends and drivers are validated through expert consultations with healthcare professionals and industry stakeholders.

Step 4: Research Synthesis and Final Output

The final report synthesizes the collected data and insights, presenting a comprehensive analysis of the France healthcare infrastructure market.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Government Investments in Healthcare Infrastructure

Technological Advancements in Healthcare Systems

Aging Population Driving Healthcare Demand - Market Challenges

High Operational Costs

Regulatory Barriers and Compliance Costs

Unequal Healthcare Access Across Regions - Market Opportunities

Adoption of Smart Healthcare Solutions

Government Initiatives for Rural Healthcare

Telemedicine Expansion - Trends

Integration of Artificial Intelligence in Healthcare

Shift Towards Value-based Care - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Hospital Infrastructure

Primary Care Facilities

Emergency Medical Services

Outpatient Care Centers

Specialized Healthcare Facilities - By Platform Type (In Value%)

Digital Health Platforms

Hospital Management Systems

Electronic Health Records (EHR) Platforms

Telemedicine Platforms

Integrated Healthcare Platforms - By Fitment Type (In Value%)

On-premise Solutions

Cloud-based Solutions

Hybrid Solutions

Modular Solutions - By End User Segment (In Value%)

Public Healthcare Sector

Private Healthcare Sector

Healthcare Service Providers

- Market Share Analysis

- Cross Comparison Parameters (System Type, Platform Type, Procurement Channel, End User Segment, Fitment Type, Technological Integration, Service Availability)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Siemens Healthineers

GE Healthcare

Philips Healthcare

Medtronic

Roche Diagnostics

Schneider Electric

Cerner Corporation

Abbott Laboratories

Stryker Corporation

Becton Dickinson

Johnson & Johnson

Fujifilm Healthcare

Thermo Fisher Scientific

Zebra Technologies

Honeywell Life Sciences

- Public Healthcare Providers Adopting Modern Infrastructure

- Private Healthcare Expanding Healthcare Networks

- Government Role in Regulating Healthcare Systems

- Healthcare Service Providers Leveraging Digital Tools

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now