Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The France Home Finance market has witnessed substantial growth in recent years, driven by factors such as low-interest rates, government housing incentives, and increased demand for home ownership. With a robust financial system and diverse mortgage offerings, the market has expanded significantly, providing financing solutions for a growing number of homebuyers. According to a recent assessment, the market value has reached approximately USD ~ billion in 2024, demonstrating the strong demand and investment potential within the sector.

Paris, Lyon, and Marseille are dominant players in the France Home Finance market due to their strong housing demand, urbanization, and economic activities. These cities have seen an influx of domestic and international investments, contributing to the continued rise in property prices and demand for financing solutions. The government’s support through various home ownership programs has further bolstered the market, making these areas central to the nation’s home finance activities.

Market Segmentation

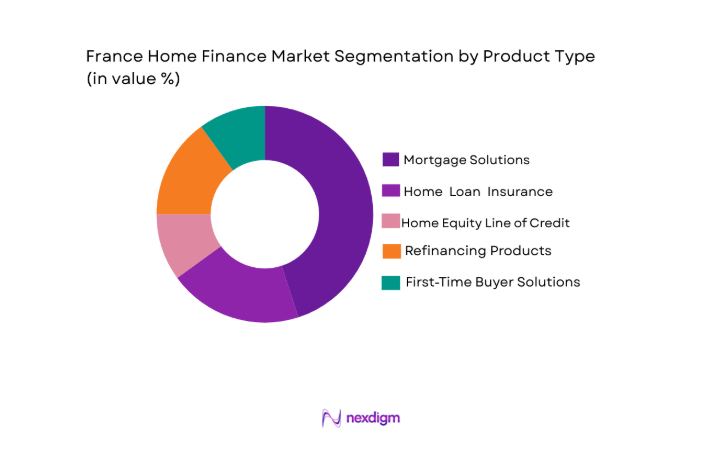

By Product Type

France Home Finance market is segmented by product type into mortgage solutions, home loan insurance, home equity lines of credit (HELOC), refinancing products, and first-time buyer solutions. Recently, mortgage solutions have had a dominant market share due to high demand driven by rising property values and favorable loan terms. Mortgage solutions continue to dominate as more homebuyers seek long-term financing options, and lenders are offering more competitive interest rates to attract borrowers. Consumer preferences for flexibility in loan repayment options, combined with the availability of government-backed financial support, have cemented the dominance of mortgage solutions in the market.

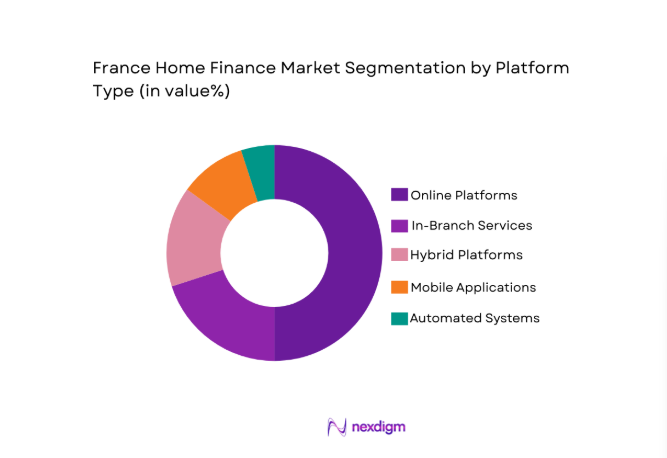

By Platform Type

The France Home Finance market is segmented by platform type into online platforms, in-branch services, hybrid platforms, mobile applications, and automated systems. Online platforms have the dominant market share, driven by the increasing preference for convenience and accessibility. With growing digitalization in the financial services sector, more consumers are opting for online platforms to compare and apply for home loans. The ease of access, user-friendly interfaces, and instant approval processes have made online platforms the preferred choice for homebuyers, pushing traditional in-branch services to a secondary position.

Competitive Landscape

The France Home Finance market is competitive, with several well-established players driving innovation in mortgage products, loan servicing, and digital transformation. Key players have consolidated their positions through strategic partnerships, technological advancements, and comprehensive customer service offerings. Major players influence market trends, and their competitive strategies focus on expanding digital offerings, improving customer experience, and offering personalized mortgage solutions.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD) | Digital Mortgage Solutions |

| Société Générale | 1864 | Paris, France | ~ | ~ | ~ | ~ | ~ |

| Crédit Agricole | 1894 | Montrouge, France | ~ | ~ | ~ | ~ | ~ |

| BNP Paribas | 1848 | Paris, France | ~ | ~ | ~ | ~ | ~ |

| La Banque Postale | 2006 | Paris, France | ~ | ~ | ~ | ~ | ~ |

| LCL (Le Crédit Lyonnais) | 1863 | Lyon, France | ~ | ~ | ~ | ~ | ~ |

France Home Finance Market Analysis

Growth Drivers

Increasing Demand for Home Ownership

The rising desire for homeownership, especially among millennials and first-time buyers, is one of the major growth drivers in the France Home Finance market. This demand is being fueled by low-interest rates, attractive loan terms, and government initiatives to make homeownership more accessible. France’s strong economic performance and rising property values also contribute to the increasing affordability of home loans, thereby stimulating demand for financing. Homebuyers are looking for flexible mortgage products with low down payments and competitive interest rates, and these preferences are further driving the expansion of the home finance market. Additionally, consumer confidence in the economy and low unemployment rates continue to push the demand for home financing higher. The demographic shift, with younger individuals increasingly preferring to buy homes, further augments the growth of this segment. Government-backed programs have provided further assistance, increasing homeownership opportunities and accelerating demand for financial products such as home loans and equity lines.

Expansion of Digital Mortgage Platforms

The shift toward digital platforms is another key driver of growth in the France Home Finance market. With the digital transformation of financial services, more homebuyers are now opting for online mortgage solutions, which offer convenience, ease of use, and faster processing times. Digital mortgage platforms provide users with access to a wide range of home financing options, allowing consumers to compare rates, submit applications, and track loan progress all from their smartphones or computers. This technology-driven shift has significantly disrupted the traditional banking and financial sector. The adoption of AI-powered solutions and automation is improving the efficiency of home loan origination, approval processes, and customer service. As more homebuyers become comfortable with digital solutions, the market is expected to continue its growth. Fintech companies are also entering the space, offering innovative mortgage solutions and personalized financing options to attract customers. As a result, the demand for digital mortgage services is expected to expand rapidly, providing a strong growth trajectory for the France Home Finance market.

Market Challenges

Rising Interest Rates

Rising interest rates present a significant challenge for the France Home Finance market, as they can make borrowing more expensive and reduce affordability for potential homebuyers. Increased rates result in higher monthly mortgage payments, making homeownership less accessible for many consumers. This trend can slow down the pace of home loan approvals and reduce consumer demand, especially in an environment where property prices are rising. Furthermore, homeowners with existing variable-rate mortgages may face increased financial pressure as their loan repayments rise, which could lead to higher default rates and lower consumer confidence. This challenge could have a long-term impact on the overall growth of the market, as it may discourage people from entering the housing market or refinancing their homes. In addition to affecting homebuyers, rising interest rates can also deter investors and developers from taking out loans for new residential projects, which could further limit the availability of homes. Financial institutions and lenders must adapt their strategies to counter these challenges, such as offering fixed-rate loans or creating alternative financing solutions to mitigate the impact of higher interest rates.

Regulatory Complexity

Navigating the complex regulatory environment in France’s home finance market is another significant challenge. Financial institutions and mortgage providers must comply with numerous regulations, including those related to lending practices, consumer protection, and tax policies. These regulations are subject to change and can vary by region, requiring companies to stay updated and adjust their practices accordingly. Furthermore, regulatory requirements such as the implementation of strict mortgage affordability tests and lending limits can restrict the ability of borrowers to access home loans, limiting the overall market potential. Additionally, stringent anti-money laundering (AML) and know-your-customer (KYC) regulations add operational costs and complexity for financial institutions, which can lead to delays in loan approval processes and a reduction in customer satisfaction. For lenders, these regulations may also result in increased compliance costs and fines for non-compliance. Navigating this regulatory landscape requires significant investment in legal and compliance resources, as well as technological systems to ensure that all regulatory standards are met efficiently.

Opportunities

Green Financing for Sustainable Homes

Green financing represents a significant opportunity for the France Home Finance market, as the demand for energy-efficient and environmentally sustainable homes increases. With growing awareness of climate change and the environmental impact of construction, both homebuyers and developers are increasingly looking for financing options that support sustainable building practices. The French government’s commitment to sustainability, including offering incentives and tax credits for energy-efficient homes, has created a favorable environment for green mortgages. Lenders and financial institutions that offer green home loans or energy-efficient home financing products stand to gain a competitive edge in the market. This trend is expected to continue as more consumers prioritize sustainability in their home-buying decisions. Green financing also aligns with the European Union’s broader environmental goals and supports the growing trend toward eco-friendly living. Furthermore, green mortgages often come with lower interest rates or better terms, making them an attractive option for buyers. Financial institutions that focus on green loans are positioning themselves as environmentally responsible, which can enhance their brand image and attract a wider customer base.

Increasing Demand for First-Time Homebuyer Solutions

The demand for first-time homebuyer solutions presents a substantial opportunity for the France Home Finance market. As more young individuals enter the workforce and seek to establish themselves financially, many are turning to homeownership as an investment and personal milestone. First-time buyers are often looking for lower down payment requirements, flexible repayment options, and lower interest rates, which have created an opportunity for lenders to tailor their products to this segment. Government programs designed to assist first-time homebuyers, such as down payment assistance and tax incentives, have further encouraged this demographic to enter the housing market. In response, financial institutions are introducing specialized products, such as first-time buyer mortgages, which offer more favorable terms and a smoother approval process. As this trend continues, home financing providers that cater specifically to first-time buyers are likely to see strong growth. Furthermore, the growth of digital mortgage platforms, which offer convenient and accessible mortgage options, is expected to further support the expansion of this segment.

Future Outlook

The future outlook for the France Home Finance market is promising, with continued growth expected in the coming years. As the demand for home ownership remains strong, driven by favorable interest rates, government initiatives, and a growing population, the market is poised to expand. Technological advancements, such as AI-powered mortgage platforms and automated underwriting systems, will continue to drive efficiency and enhance the customer experience. Additionally, regulatory support for green financing and sustainable homeownership will provide new opportunities for lenders. Consumer demand for flexible and affordable financing options is expected to increase, and the shift towards digital platforms will continue to shape the future of home finance in France.

Major Players

- Société Générale

- Crédit Agricole

- BNP Paribas

- La Banque Postale

- LCL (Le Crédit Lyonnais)

- Caisse d’Épargne

- Banque Populaire

- Crédit Mutuel

- HSBC France

- BRED Banque Populaire

- ING France

- AXA Banque

- Lloyds Bank France

- Cofidis

- Sarenza

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Financial institutions and banks

- Real estate developers

- Property investors

- Homebuyers

- Mortgage brokers and advisors

- Sustainable housing companies

Research Methodology

Step 1: Identification of Key Variables

Key variables such as economic trends, interest rates, regulatory factors, and technological developments are identified and analyzed.

Step 2: Market Analysis and Construction

Comprehensive market analysis is performed using both primary and secondary research methods to construct an accurate market overview.

Step 3: Hypothesis Validation and Expert Consultation

Expert consultations are conducted to validate hypotheses and refine market assumptions based on industry insights.

Step 4: Research Synthesis and Final Output

The final research output is synthesized, incorporating all relevant data and analysis to deliver a comprehensive market report.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Increase in First-Time Homebuyers

Government Incentives for Homebuyers

Technological Advancements in Mortgage Processing

Rising Property Values and Demand for Financing

Expansion of Online and Digital Platforms - Market Challenges

Rising Interest Rates and Economic Uncertainty

Complex Regulatory Landscape

High Debt Levels Among Borrowers

Slow Adoption of Fintech Solutions

Limited Financial Literacy Among Borrowers - Market Opportunities

Expansion of Green Financing for Sustainable Homes

Adoption of AI for Personalized Loan Offers

Partnerships Between Tech Firms and Financial Institutions - Trends

Integration of Mobile Apps in Mortgage Services

Rise of Digital-Only Mortgage Providers

Increased Use of AI in Mortgage Risk Assessment

Shift Toward Sustainable and Energy-Efficient Homes

Rise of Homeowner Insurance Bundling - Government Regulations & Defense Policy

Government Subsidies for First-Time Homebuyers

Regulation of Digital Financial Services

Energy-Efficiency Financing Requirements - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Mortgage Solutions

Home Loan Insurance

Home Equity Line of Credit (HELOC)

Refinancing Products

First-Time Buyer Solutions - By Platform Type (In Value%)

Online Platforms

In-Branch Services

Hybrid Platforms

Mobile Applications

Automated Systems - By Fitment Type (In Value%)

Individual Buyers

Home Renovation Financing

Property Developers

Refinancing Clients

Real Estate Investment Trusts (REITs) - By EndUser Segment (In Value%)

Homeowners

Renters Looking to Purchase

First-Time Homebuyers

Investors

Mortgage Brokers and Advisors - By Procurement Channel (In Value%)

Direct Borrowing

Financial Institutions

Government Subsidy Programs

Online Comparison Platforms

Private Lenders - By Material / Technology (in Value%)

Blockchain-Enabled Mortgage Platforms

Artificial Intelligence in Credit Scoring

Cloud-Based Mortgage Solutions

Digital Verification Technologies

Mobile Payment Systems

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (System Type, Platform Type, Procurement Channel, End User Segment, Fitment Type, Technology Adoption, Loan Terms, Interest Rates)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Société Générale

Crédit Agricole

BNP Paribas

La Banque Postale

LCL (Le Crédit Lyonnais)

Caisse d’Épargne

Banque Populaire

Crédit Mutuel

HSBC France

BRED Banque Populaire

ING France

AXA Banque

Lloyds Bank France

Cofidis

Sarenza

- Increasing Demand for First-Time Buyer Solutions

- Rise in Home Renovation and Financing

- Focus on Digital Platforms by Younger Generations

- Growth of Mortgage Brokers and Advisory Services

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now