Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The France online insurance market has grown significantly, driven by an increasing consumer shift toward digital platforms. With an expanding preference for seamless digital solutions, the market has reached a valuation of approximately USD ~ billion. This growth is propelled by advancements in technology, regulatory support, and evolving consumer behaviors that favor convenience and cost-effectiveness. The market is witnessing an increasing penetration of digital health, motor, and life insurance solutions, which further boosts its expansion.

The market’s dominance is concentrated in urban regions such as Paris, Lyon, and Marseille, where there is high internet penetration and a growing tech-savvy population. These cities benefit from strong infrastructure and widespread access to mobile devices and online platforms, which are critical drivers of digital insurance adoption. Additionally, favorable regulatory frameworks and government incentives have facilitated the rapid digitization of insurance products, further cementing France’s role as a key player in the European online insurance market.

Market Segmentation

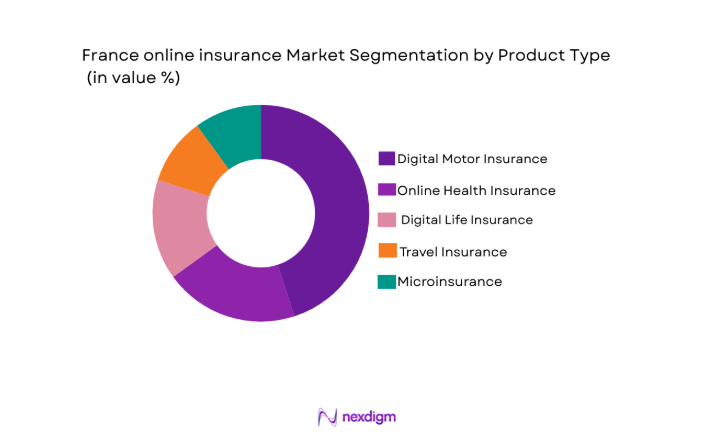

By Product Type

The France online insurance market is segmented by product type into digital motor insurance, online health insurance, digital life insurance, travel insurance, and microinsurance. Recently, digital motor insurance has seen dominant market share due to factors such as mandatory vehicle coverage requirements, high vehicle ownership rates in urban areas, and the adoption of telematics technologies. The integration of digital platforms with advanced data analytics has significantly improved customer engagement and streamlined claims processing, which has further increased consumer trust and the sector’s overall growth.

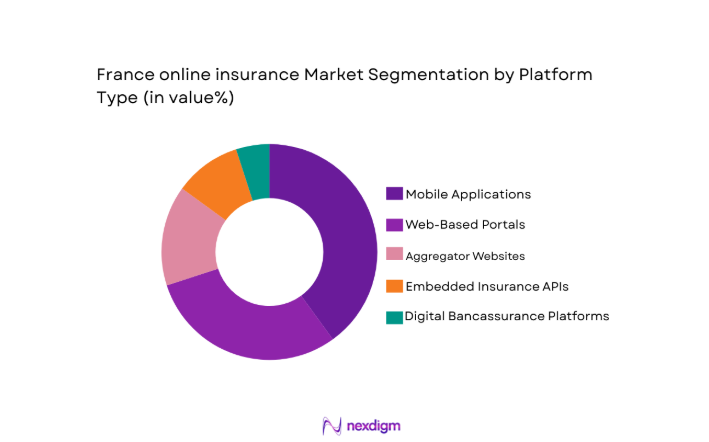

By Platform Type

The France online insurance market is segmented by platform type into web-based portals, mobile applications, aggregator websites, embedded insurance APIs, and digital bancassurance platforms. Among these, mobile applications have emerged as the dominant platform, driven by the widespread use of smartphones and the increasing preference for mobile-first services. Mobile apps provide consumers with on-the-go access to their policies, claims management, and personalized insurance offerings, which greatly enhances user experience and convenience. The mobile-first approach also enables insurers to deliver real-time updates, seamless communication, and improved customer engagement, making it a preferred choice for tech-savvy consumers in France.

Competitive Landscape

The competitive landscape in the France online insurance market is marked by both traditional insurers expanding their digital offerings and insurtech startups offering innovative products. Major players are focusing on technology-driven services, partnerships with fintech firms, and customer-centric solutions to gain a competitive edge. The ongoing digital transformation and evolving consumer preferences are expected to foster consolidation in the industry, with tech-driven players and traditional insurers increasingly collaborating to enhance service offerings.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD) | Additional Market Parameter |

| AXA | 1816 | Paris | ~ | ~ | ~ | ~ | ~ |

| Allianz | 1890 | Munich | ~ | ~ | ~ | ~ | ~ |

| Generali | 1831 | Trieste | ~ | ~ | ~ | ~ | ~ |

| CNP Assurances | 1959 | Paris | ~ | ~ | ~ | ~ | ~ |

| Groupama | 1900 | Paris | ~ | ~ | ~ | ~ | ~ |

France Online Insurance Market Analysis

Growth Drivers

Technological Advancements in AI and Data Analytics

The integration of AI and data analytics is rapidly transforming the France online insurance market, making it a significant growth driver. Insurers are increasingly leveraging AI to automate claims processing, enhance underwriting accuracy, and improve risk management. Data analytics is used to provide personalized offerings, helping insurers better understand consumer behavior and preferences, leading to improved customer retention and satisfaction. The ability to use data for predictive modeling has enabled companies to offer dynamic pricing models that appeal to a broader demographic. With the adoption of AI in customer service, insurers can provide faster, more efficient responses to inquiries, further boosting customer loyalty. Additionally, AI’s role in fraud detection has contributed to reducing operational costs, improving profitability for insurers. As consumers demand quicker and more accurate services, the demand for AI-driven solutions in the French insurance market is expected to continue growing.

Increasing Mobile and Internet Penetration

The rise of mobile and internet penetration in France has greatly facilitated the growth of online insurance products. With a large percentage of the population using smartphones and accessing the internet daily, consumers now expect the convenience of managing their insurance policies online. The ability to compare products, purchase policies, and file claims through mobile apps has led to greater market accessibility and convenience. As mobile usage increases, insurers are tailoring their platforms to ensure mobile compatibility, making it easier for consumers to access their services. The growth of e-commerce and digital platforms has also spurred the adoption of insurance products, as consumers are becoming more comfortable with managing financial transactions online. In addition, insurers are investing in mobile-first solutions, such as app-based claims submission and digital policy management, which are driving growth in the digital insurance space.

Market Challenges

Cybersecurity Risks and Data Privacy Concerns

As the online insurance market grows, cybersecurity risks and data privacy concerns have emerged as significant challenges. The increasing amount of personal and financial data being shared on digital platforms exposes both insurers and consumers to potential data breaches and cyber-attacks. Insurers must implement robust security measures, including encryption and multi-factor authentication, to protect sensitive information. However, even with these measures in place, consumers are often reluctant to share personal data online due to fears of identity theft and fraud. Regulatory bodies are increasing scrutiny on how insurers manage customer data, and failing to comply with these regulations could lead to fines and reputational damage. As such, insurers must strike a balance between delivering seamless online services and ensuring robust security protocols to maintain consumer trust and meet regulatory standards.

Regulatory Compliance and Fragmented Market Standards

The complex regulatory environment surrounding online insurance in France poses another challenge for the market. Insurers are required to comply with a range of national and European Union regulations governing digital insurance products, including data protection laws like the GDPR. The fragmented nature of these regulations creates compliance burdens for insurers, as they must ensure that their digital platforms meet different legal requirements across regions. Moreover, the lack of standardization in digital insurance policies can lead to confusion among consumers and slow market adoption. Insurers must continuously monitor regulatory changes and adapt their business practices to remain compliant, which can be both costly and time-consuming. This regulatory complexity can create barriers to entry for new players and hinder the overall growth of the market.

Opportunities

Expansion of Microinsurance Products

The growing demand for affordable insurance solutions presents an opportunity for the expansion of microinsurance products in the France online insurance market. Microinsurance is designed to provide coverage for low-income individuals or those with specific, limited needs. As the gig economy and freelance work continue to rise, there is an increasing demand for flexible and affordable insurance options that traditional policies cannot cater to. Insurers can capitalize on this growing demand by offering microinsurance products through digital channels. These products, often provided at lower premiums with simplified coverage, make insurance more accessible to underserved populations. Additionally, the increasing number of partnerships between insurers and fintech startups is expected to fuel the growth of microinsurance offerings, as these platforms can easily reach a wider audience and deliver cost-effective solutions.

Digital Health Insurance Adoption

The growing emphasis on health and wellness, especially post-pandemic, presents a significant opportunity for digital health insurance products. Consumers are increasingly turning to online platforms to manage their health and wellness needs, including obtaining health insurance coverage. The digital health insurance sector in France is expected to benefit from the rise of telemedicine, wearables, and digital health monitoring tools, which allow consumers to actively manage their health while interacting with their insurance providers. Insurers are also leveraging technology to offer personalized health plans based on individual health data, enabling more targeted and efficient coverage. As consumers become more health-conscious and demand more flexible, digitally-driven health insurance products, the digital health insurance market is poised for significant growth. The expansion of these products will help insurers capture a larger share of the market, particularly as they align with consumer preferences for more personalized and accessible health solutions.

Future Outlook

The future outlook for the France online insurance market is promising, driven by ongoing technological advancements and favorable regulatory conditions. As consumers increasingly demand digital-first insurance solutions, insurers are expected to continue investing in AI, big data, and mobile platforms to enhance user experiences. The growing popularity of microinsurance and digital health products further supports long-term market expansion. Additionally, continued collaboration between traditional insurers and insurtech firms will spur innovation and create more diverse offerings, ensuring that the market remains dynamic and competitive.

Major Players

- AXA

- Allianz

- Generali

- CNP Assurances

- Groupama

- La Parisienne Assurances

- Maif

- Swiss Life France

- Macif

- MMA

- AIG

- Zurich Insurance Group

- Lemonade

- Direct Assurance

- Boursorama

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Insurance companies

- Digital platforms and aggregators

- Mobile app developers

- Telecom service providers

- Financial technology companies

- Consumer goods companies

Research Methodology

Step 1: Identification of Key Variables

Identify the main variables influencing the market, including technological trends, consumer behavior, and regulatory policies.

Step 2: Market Analysis and Construction

Analyze data from primary and secondary sources to construct a comprehensive view of the market landscape.

Step 3: Hypothesis Validation and Expert Consultation

Validate the findings through expert interviews and industry consultations to ensure the reliability of the data.

Step 4: Research Synthesis and Final Output

Synthesize all collected data and insights into a final report, ensuring all market factors are addressed comprehensively.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Increasing Smartphone Penetration

Growing Preference for Digital Services

Government Regulations Promoting Digital Adoption

Rising Demand for Personalized Insurance Products

Increasing Financial Literacy among Consumers - Market Challenges

Cybersecurity and Data Privacy Concerns

Regulatory Compliance and Fragmentation

Customer Trust Issues in Digital Platforms

Intense Competition from Traditional Insurers

Technological Integration Challenges - Market Opportunities

Growth in the Microinsurance Sector

Collaborations with Fintech and Insurtech Startups

Expansion of AI-Driven Insurance Models - Trends

Rise of On-Demand Insurance Models

Personalization of Insurance Products via Data Analytics

Integration of AI for Automated Claims Processing

Growing Popularity of Digital Wallets for Insurance Payments

Increased Investment in Customer Experience Technology - Government Regulations & Defense Policy

Data Protection and Privacy Regulations

Regulation of Insurtech Platforms

Government Incentives for Digital Transformation in Insurance - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Digital Motor Insurance

Online Health Insurance

Digital Life Insurance

Travel Insurance

Microinsurance - By Platform Type (In Value%)

Web-Based Portals

Mobile Applications

Aggregator Websites

Embedded Insurance APIs

Digital Bancassurance Platforms - By Fitment Type (In Value%)

Direct-to-Consumer Solutions

Third-Party Aggregator Solutions

Insurance-as-a-Service Platforms

Mobile App-Based Solutions

B2B2C Insurance Integration - By End User Segment (In Value%)

Individual Consumers

Small & Medium Enterprises (SMEs)

Large Enterprises

Government & Public Sector

Insurance Brokers & Intermediaries - By Procurement Channel (In Value%)

Direct Procurement

Third-Party Aggregators

Bancassurance Partnerships

Online Marketplaces

Brokerage Services

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (System Type, Platform Type, Procurement Channel, End User Segment, Fitment Type)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

AXA

Allianz

Generali

CNP Assurances

Groupama

Mutuelle de Poitiers

Maif

La Parisienne Assurances

L’olivier Assurance

Swiss Life France

Macif

MMA

AIG

Zurich Insurance Group

Lemonade

- Increasing Shift towards Online Insurance Platforms by Millennials

- Need for Real-Time Claims Processing in Health Insurance

- Demand for Comprehensive Travel Insurance Solutions

- Rising Popularity of Digital Motor Insurance Solutions

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now