Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The France Semiconductor Manufacturing Market has experienced substantial growth, with the market size driven by the increasing demand for high-performance semiconductor chips across various sectors, particularly consumer electronics, automotive, and telecommunications. This market’s growth is fueled by technological advancements in semiconductor fabrication and government support for local semiconductor manufacturing initiatives. The market’s value is currently projected at USD ~ billion, with investments in cutting-edge technologies and infrastructure boosting production capacities and market expansion. This growth is supported by robust demand for products like mobile devices, automotive electronics, and data processing units, along with the integration of IoT devices.

The dominant players in France’s semiconductor market are located mainly in key industrial hubs such as Grenoble, Paris, and Toulouse, which have established themselves as centers of excellence in semiconductor R&D and manufacturing. These cities are home to both global semiconductor giants and local innovators, driving technological advancements and fostering collaboration within the ecosystem. France’s strategic location in Europe, along with government incentives for semiconductor production, has attracted significant investment in R&D facilities and manufacturing plants, positioning the country as a leader in Europe’s semiconductor production landscape.

Market Segmentation

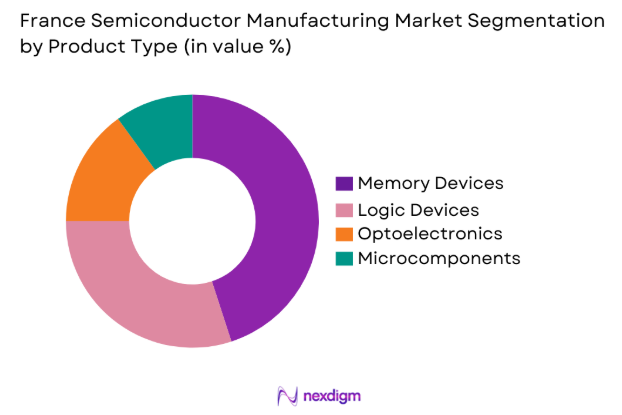

By Product Type

The France Semiconductor Manufacturing Market is segmented by product type into memory devices, logic devices, optoelectronics, and micro components. Memory devices have captured the dominant market share due to their widespread application in consumer electronics, automotive, and communication systems. These products meet the rising demand for high-performance computing, data storage, and mobile technologies, driving their increased adoption. Additionally, advancements in memory technology, such as DRAM and NAND flash, are further fueling this segment’s growth, as industries seek faster, more efficient storage solutions for both consumer and enterprise applications.

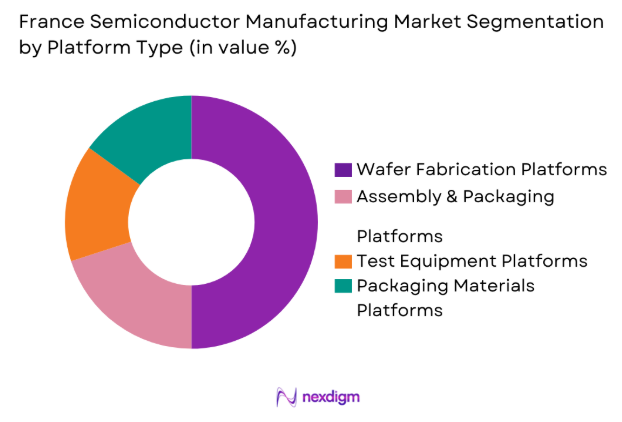

By Platform Type

The France Semiconductor Manufacturing market is also segmented by platform type into wafer fabrication platforms, assembly and packaging platforms, test equipment platforms, and packaging materials platforms. Wafer fabrication platforms hold the largest market share, owing to the increased demand for custom silicon fabrication in various sectors, including mobile phones, automotive systems, and advanced computing. As the semiconductor industry advances toward smaller, more powerful chips, wafer fabrication plays a crucial role in meeting the rising demand for miniaturized and high-performance components.

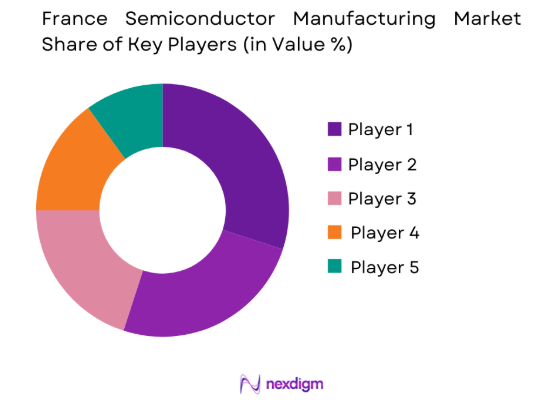

Competitive Landscape

The competitive landscape in the France Semiconductor Manufacturing Market is characterized by a mix of global players and local innovators. Major players have been actively expanding their production capabilities and adopting innovative technologies, while the market has seen increasing consolidation, especially in the wafer fabrication and memory sectors. These companies are focused on strategic investments in research and development, collaborations, and acquisitions to maintain their competitive edge and meet the growing demand for semiconductor components. With Europe pushing for technological autonomy, France has emerged as a key player in the semiconductor sector.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD) | Additional Market-Specific Parameter |

| STMicroelectronics | 1987 | Geneva, Switzerland | ~ | ~ | ~ | ~ | ~ |

| Soitec | 1992 | Bernin, France | ~ | ~ | ~ | ~ | ~ |

| GlobalFoundries | 2009 | Malta, USA | ~ | ~ | ~ | ~ | ~ |

| NXP Semiconductors | 1953 | Eindhoven, Netherlands | ~ | ~ | ~ | ~ | ~ |

| Infineon Technologies | 1999 | Neubiberg, Germany | ~ | ~ | ~ | ~ | ~ |

France Semiconductor Manufacturing Market Analysis

Growth Drivers

Increased Demand for Consumer Electronics

The rapid growth in demand for consumer electronics, driven by technological advancements and the rise of smart devices, is a major growth driver for the semiconductor market. Devices such as smartphones, wearables, and home automation systems rely heavily on high-performance semiconductor components, increasing the demand for more efficient and advanced chips. As consumer preferences shift toward mobile computing and interconnected devices, the French semiconductor market benefits from this trend. This demand is fostering growing investments in research and development, with a focus on producing smaller, faster, and more energy-efficient semiconductor products to meet the needs of modern electronics and smart technologies.

Technological Advancements in Semiconductor Fabrication

Technological advancements in semiconductor fabrication, such as smaller process nodes and the adoption of new materials, are fueling significant market growth. These innovations allow the production of more powerful chips at lower costs, driving demand for advanced electronics and high-performance computing systems. As companies aim to meet consumer and industry needs for faster data processing, lower power consumption, and smaller chip sizes, improvements in fabrication technology are essential for continued market expansion. The shift toward 5nm and 3nm semiconductor technologies is setting new industry standards, with France playing a key role in advancing these technologies and contributing to the global semiconductor landscape.

Market Challenges

High Capital Investment in Semiconductor Manufacturing

The semiconductor manufacturing process demands significant capital investment, especially for the purchase and upkeep of advanced equipment used in wafer fabrication and testing. Establishing new fabrication plants and upgrading existing facilities involves high costs, posing a challenge for smaller manufacturers. This capital-intensive nature creates a barrier to entry for new players, limiting competition and potentially slowing the adoption of new technologies. Additionally, the increasing complexity of semiconductor production makes it difficult to maintain high-quality standards while controlling costs. For the French semiconductor industry, overcoming these financial and operational challenges is crucial to sustaining growth and innovation in an increasingly competitive global market.

Supply Chain Disruptions in Raw Materials

The French semiconductor industry faces significant challenges related to the global supply chain for raw materials such as rare earth metals and semiconductor-grade silicon. Disruptions caused by geopolitical tensions, natural disasters, or trade restrictions have led to material shortages, increased costs, and production delays. These issues are especially problematic for the semiconductor sector, which relies on precise materials to manufacture high-performance components. To address these challenges, the industry must focus on strategic sourcing and diversifying suppliers to ensure a stable flow of materials. Tackling these supply chain issues is crucial for maintaining the efficiency and competitiveness of France’s semiconductor manufacturing sector.

Opportunities

Expansion of Automotive Semiconductor Applications

The growing integration of semiconductor components in automotive applications presents a valuable opportunity for the French semiconductor market. The automotive industry is increasingly adopting advanced semiconductor technologies, especially for electric vehicles (EVs), autonomous driving systems, and in-vehicle entertainment. As the demand for EVs and connected cars rises, the need for more semiconductor chips in automotive systems, including sensors, controllers, and communication devices, intensifies. This trend offers France a prime opportunity to enhance its semiconductor manufacturing capabilities to meet the evolving needs of the automotive sector. By capitalizing on this opportunity, France can strengthen its position in the global semiconductor market while supporting the growth of smart and electric vehicles.

Development of 5G Networks

The rollout of 5G networks represents a significant growth opportunity for the French semiconductor manufacturing market. As 5G technology requires advanced semiconductor chips for infrastructure, mobile devices, and IoT applications, the demand for these components is set to increase. France’s investments in 5G infrastructure and its focus on maintaining technological leadership in Europe will drive this demand. This expansion in 5G technology not only fuels growth in mobile communication systems but also fosters new opportunities in sectors like healthcare, smart cities, and industrial automation. These advancements position the French semiconductor market for continued growth and innovation, ensuring its role as a key player in the global semiconductor industry.

Future Outlook

Over the next five years, the France Semiconductor Manufacturing Market is expected to experience continued growth, driven by innovations in semiconductor fabrication, the increasing demand for consumer electronics, and the expansion of automotive and telecommunications sectors. France is poised to benefit from ongoing investments in 5G infrastructure and the growing adoption of electric vehicles, both of which will require advanced semiconductor components. Government initiatives and industry collaborations will further accelerate technological developments, ensuring that France remains a key player in the global semiconductor market.

Major Players

- STMicroelectronics

- Soitec

- GlobalFoundries

- NXP Semiconductors

- Infineon Technologies

- Texas Instruments

- Intel Corporation

- Micron Technology

- Qualcomm

- Broadcom

- Renesas Electronics

- ON Semiconductor

- Analog Devices

- TSMC

- ASML

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Automotive manufacturers

- Consumer electronics manufacturers

- Semiconductor foundries

- Mobile device manufacturers

- Telecom companies

- Research and development centers

Research Methodology

Step 1: Identification of Key Variables

The initial step involves identifying the key factors that influence the semiconductor market, including technology trends, industry growth drivers, and consumer demand.

Step 2: Market Analysis and Construction

This step includes analyzing historical data, current market trends, and future forecasts to construct a comprehensive understanding of the semiconductor market in France.

Step 3: Hypothesis Validation and Expert Consultation

This step validates initial hypotheses and assumptions through consultation with industry experts, market leaders, and technology specialists.

Step 4: Research Synthesis and Final Output

The final output is synthesized by combining market insights, expert opinions, and data-driven analyses to produce a detailed report on the France Semiconductor Manufacturing Market.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Increased Consumer Electronics Demand

Technological Advancements in Semiconductor Fabrication

Rising Automotive Electronics Integration - Market Challenges

High Capital Investment in Manufacturing Facilities

Supply Chain Disruptions in Raw Materials

Technological Complexity and R&D Costs - Market Opportunities

Expansion of Automotive Semiconductor Applications

Growing Demand for 5G Networks and Infrastructure

Emerging AI and Machine Learning Applications in Semiconductors - Trends

Miniaturization and Advanced Packaging Techniques

Increase in Semiconductor Recycling

Development of Eco-friendly Semiconductor Materials - Government Regulations

- SWOT Analysis of Key Competitors

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Semiconductor Foundries

Memory Devices

Logic Devices

Optoelectronics

Microcomponents - By Platform Type (In Value%)

Wafer Fabrication Platforms

Assembly & Packaging Platforms

Test Equipment Platforms

Fabless Semiconductor Platforms

Packaging Materials Platforms - By Fitment Type (In Value%)

On-premise Solutions

Cloud-based Solutions

Modular Solutions

Integrated Solutions

Hybrid Solutions - By End User Segment (In Value%)

Consumer Electronics

Automotive & Transport

Telecommunications

Healthcare

Industrial Applications - By Procurement Channel (In Value%)

Direct Procurement

Retail Distributors

E-commerce Platforms

Third-party Distributors

OEM Procurement

- Market Share Analysis

- Cross Comparison Parameters (System Type, Platform Type, Procurement Channel, End User Segment, Fitment Type, Market Share, Technology Focus, Revenue, Geographic Reach, Product Lifecycle Stage)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

STMicroelectronics

Renesas Electronics

NXP Semiconductors

Soitec

GlobalFoundries

Intel Corporation

TSMC

Micron Technology

Qualcomm

Broadcom

Infineon Technologies

Texas Instruments

Analog Devices

ON Semiconductor

AMD

- Consumer Electronics Industry Growth

- Automotive Sector Demand for Smart Chips

- Telecommunications Industry Shift Towards 5G

- Healthcare Industry’s Adoption of Semiconductors

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now