Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The France Solar EPC market is driven by the growing demand for renewable energy, with the market size expanding significantly in recent assessments. Supported by government incentives, such as tax breaks and subsidies, the market is valued in billions ~ USD. Technological advancements in solar panel efficiency and the increasing demand for sustainable energy sources are major growth contributors. With major projects in both residential and commercial segments, this sector is expected to see continuous growth, underpinned by a strategic push towards clean energy.

The dominance of urban regions like Paris, Lyon, and Marseille plays a crucial role in the market’s development. These cities benefit from robust infrastructure, favorable regulatory environments, and a high level of environmental awareness, making them key players in the adoption of solar energy. Furthermore, regional government initiatives and the large-scale integration of solar solutions in commercial and residential buildings have positioned France as a leader in solar EPC technology in Europe.

Market Segmentation

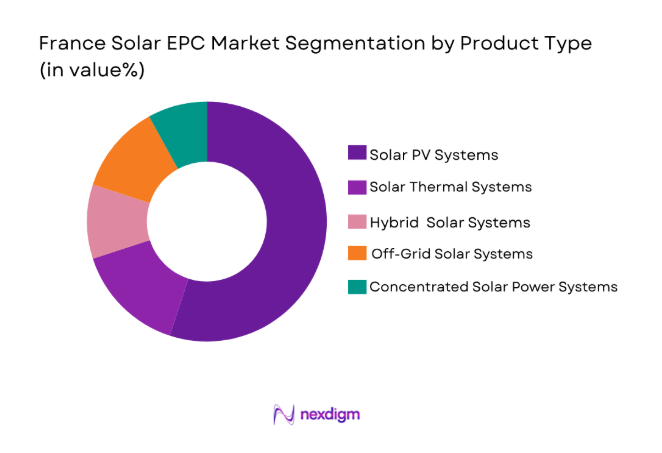

By Product Type

The France Solar EPC market is segmented by product type into Solar PV Systems, Solar Thermal Systems, Hybrid Solar Systems, Off-Grid Solar Systems, and Concentrated Solar Power Systems. Among these, Solar PV Systems dominate the market due to factors such as demand patterns, infrastructure availability, and high consumer preference for photovoltaic technology. The increasing adoption of solar PV systems across residential, commercial, and industrial sectors, combined with the lowering costs of installation and system efficiency improvements, strengthens their market share.

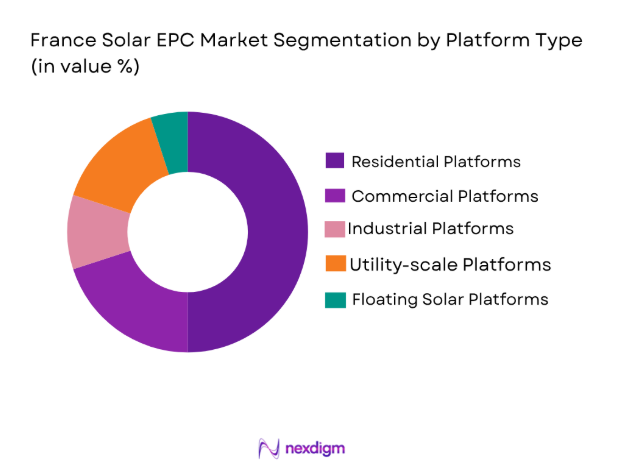

By Platform Type

The France Solar EPC market is segmented by platform type into Residential Platforms, Commercial Platforms, Industrial Platforms, Utility-Scale Platforms, and Floating Solar Platforms. Residential Platforms dominate the market, driven by government incentives, growing consumer demand for energy independence, and the rising cost of traditional electricity. The increasing affordability of solar panels and strong environmental policies have contributed to residential platforms capturing the largest share of the market.

Competitive Landscape

The competitive landscape of the France Solar EPC market reflects a mix of global players and domestic specialists that drive innovation and growth. The market is characterized by high competition, with large firms consolidating market power through strategic acquisitions and technological advancements. Major players contribute to the sector’s evolution by offering comprehensive solutions for both large-scale solar projects and residential installations.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Strategic Alliances |

| EDF Energy | 2000 | Paris, France | ~ | ~ | ~ | ~ | ~ |

| TotalEnergies | 1924 | Paris, France | ~ | ~ | ~ | ~ | ~ |

| Engie | 2008 | Paris, France | ~ | ~ | ~ | ~ | ~ |

| SolarEdge Technologies | 2006 | Herzliya, Israel | ~ | ~ | ~ | ~ | ~ |

| First Solar | 1999 | Arizona, USA | ~ | ~ | ~ | ~ | ~ |

France Solar EPC Market Analysis

Growth Drivers

Government Incentives

Government incentives such as tax credits, subsidies, and energy tariffs are critical drivers for the expansion of the France Solar EPC market. These incentives lower the upfront costs of solar installations, encouraging more consumers and businesses to adopt renewable energy solutions. With the French government’s commitment to a greener future, there is increasing funding allocated to support the development of solar infrastructure, reducing the financial burden of adopting solar technology. In particular, urban areas benefit from incentives that make solar energy solutions more accessible and affordable. Furthermore, the alignment of solar energy goals with France’s climate commitments strengthens the long-term vision for renewable energy adoption. As part of this, the government is establishing more favorable policies for financing solar projects, which directly supports greater investment in the sector and propels the growth of solar energy adoption across residential, commercial, and industrial segments. In addition, the government’s ambitious renewable energy targets for the coming decades encourage sustained growth within the industry, driving private-sector participation and partnerships that further promote solar energy solutions.

Technological Advancements

Technological advancements in solar power solutions, especially in solar PV systems and energy storage technologies, have bolstered the growth of the solar EPC market in France. Continuous improvements in solar cell efficiency and energy storage capabilities, along with declining costs of these technologies, make solar systems more competitive compared to traditional energy sources. As solar panels become more efficient at converting sunlight into electricity, the overall cost of generating solar energy decreases, making it a more attractive option for both commercial and residential consumers. Energy storage systems have become a crucial part of the solar energy infrastructure, enabling the storage of excess energy generated during peak production hours for use during periods of low sunlight. These advancements enhance the reliability of solar power, making it a more dependable energy source. Additionally, the development of smart grids, which allow for better integration of renewable energy into existing infrastructure, contributes significantly to market growth. As France continues to prioritize sustainability, the expansion of innovative energy storage solutions and improved grid integration techniques will foster the development of the solar EPC sector, providing both reliability and cost-efficiency for future solar projects.

Market Challenges

High Initial Investment Costs

Despite the declining cost of solar technology, the initial investment for solar energy systems remains high, especially for large-scale commercial and industrial projects. This high upfront cost can serve as a significant barrier to the adoption of solar solutions, particularly for small and medium enterprises (SMEs) that may lack the financial resources necessary to make such investments. Although financing options such as loans, leasing, and government incentives have been introduced to help mitigate the initial cost, they often still do not fully eliminate the financial challenge, particularly for projects that require extensive infrastructure and installation. The high capital investment needed for grid-tied systems, combined with the ongoing costs of maintenance and operation, may deter businesses from switching to solar energy despite the long-term savings it offers. This challenge can limit the rapid growth of solar energy adoption across various sectors, especially among organizations that are constrained by budget limitations.

Grid Integration Issues

The integration of solar power into France’s existing grid infrastructure presents another challenge for the solar EPC market. The intermittent nature of solar energy, coupled with the necessity for precise grid synchronization, requires significant upgrades to the existing power grid to accommodate renewable energy sources. While the French government has made substantial investments in grid modernization and smart grid technologies to address these challenges, the process is costly and time-consuming. Additionally, the technical complexity of managing the variable energy output from solar systems complicates the integration process. Solar power often needs to be stored or redirected, which places further pressure on grid infrastructure. Overloading the grid during times of peak solar generation, when production exceeds consumption, can lead to inefficiencies and interruptions in power supply. To address these issues, France must continue to enhance grid management capabilities and integrate advanced energy storage systems that allow solar power to be effectively used even when direct solar production is low. The ongoing grid integration challenges thus represent a key hurdle to accelerating solar energy deployment.

Opportunities

Expansion of Floating Solar Projects

One of the most promising opportunities in the France Solar EPC market is the expansion of floating solar projects. Floating solar technology, which uses bodies of water as platforms for solar panels, has gained traction due to its efficient use of space and ability to produce more energy compared to land-based systems. With France’s vast network of inland lakes, reservoirs, and coastal areas, floating solar farms provide an opportunity to harness renewable energy without competing for valuable land space. This innovative technology has the potential to address land scarcity issues while offering an environmentally friendly energy generation solution. The French government has already shown support for water-based solar energy projects, with initiatives aimed at reducing the carbon footprint of energy generation. As a result, the market for floating solar power is poised for significant growth, particularly as water-based installations help alleviate the challenge of land availability. France’s substantial investment in renewable energy infrastructure further facilitates the expansion of floating solar technology, making it a central pillar of the country’s clean energy future.

Integration with Electric Vehicles

Another substantial opportunity in the France Solar EPC market lies in the integration of solar power with electric vehicle (EV) charging infrastructure. As the adoption of electric vehicles continues to rise across France, the demand for EV charging stations has grown correspondingly. Solar-powered EV charging stations offer a cost-effective and environmentally sustainable solution to meet this increasing demand. By combining solar power generation with EV charging infrastructure, these stations can help reduce reliance on conventional electricity sources, contributing to a cleaner, more sustainable transport sector. Moreover, the integration of solar power into EV charging networks can lower the operational costs of charging stations, making them more attractive to businesses and municipalities. The French government’s focus on advancing the use of electric vehicles, along with its commitment to reducing carbon emissions, will drive further investment in solar-powered EV charging stations. Additionally, collaborations between solar EPC providers and EV manufacturers could create synergies that result in widespread adoption of solar-integrated charging networks, presenting a valuable market opportunity for EPC companies.

Future Outlook

The France Solar EPC market is poised for continued growth over the next five years, driven by supportive government policies, technological advancements, and increasing demand for renewable energy. As solar power becomes more cost-competitive, both residential and commercial sectors are expected to adopt solar solutions at a faster pace. The growth of hybrid solar systems and energy storage technologies will play a key role in shaping the future of the market. Furthermore, regulatory support for green energy projects and the integration of electric vehicle infrastructure with solar solutions will open new avenues for market expansion.

Major Players

- EDF Energy

- TotalEnergies

- Engie

- SolarEdge Technologies

- First Solar

- SunPower Corporation

- Canadian Solar

- Trina Solar

- JA Solar

- Enphase Energy

- Fronius International

- LONGi Solar

- Vestas Wind Systems

- Siemens Gamesa

- Schneider Electric

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Residential energy consumers

- Commercial and industrial enterprises

- Renewable energy service providers

- Environmental and sustainability consultants

- Solar energy distributors

Research Methodology

Step 1: Identification of Key Variables

This step involves defining the key variables that influence the solar EPC market, including technological advancements, government policies, and consumer demand patterns.

Step 2: Market Analysis and Construction

In this step, data on market trends, growth drivers, and challenges is collected to create a comprehensive market model and structure for analysis.

Step 3: Hypothesis Validation and Expert Consultation

Expert consultations and validation of market assumptions through discussions with industry leaders ensure the accuracy of the research hypotheses.

Step 4: Research Synthesis and Final Output

The final step involves synthesizing the collected data and presenting the findings in a structured format, offering actionable insights for stakeholders.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Government Subsidies and Incentives

Technological Advancements in Solar Panel Efficiency

Rising Demand for Clean Energy - Market Challenges

High Initial Investment Cost

Regulatory and Compliance Barriers

Grid Integration Issues - Market Opportunities

Expansion of Floating Solar Projects

Advancements in Energy Storage Technologies

Increasing Adoption in Rural Areas - Trends

Rise of Hybrid Solar Solutions

Growth of Utility-Scale Solar Installations - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Solar PV Systems

Solar Thermal Systems

Hybrid Solar Systems

Off-Grid Solar Systems

Concentrated Solar Power Systems - By Platform Type (In Value%)

Residential Platforms

Commercial Platforms

Industrial Platforms

Utility-Scale Platforms

Floating Solar Platforms - By Fitment Type (In Value%)

Ground-mounted Systems

Rooftop-mounted Systems

BIPV (Building-Integrated Photovoltaics)

Floating Solar Systems - By End User Segment (In Value%)

Residential Consumers

Commercial & Industrial Entities

Government Institutions

- Market Share Analysis

- Cross Comparison Parameters (System Type, Platform Type, Procurement Channel, End User Segment, Fitment Type, Technological Integration, Regional Expansion)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

EDF Energy

TotalEnergies

Engie

SolarEdge Technologies

SMA Solar Technology

First Solar

SunPower Corporation

REC Group

Canadian Solar

Trina Solar

JA Solar

Enphase Energy

Fronius International

LONGi Solar

Vestas Wind Systems

- Residential Users Increasingly Switching to Solar

- Government Push for Clean Energy in Urban Areas

- Adoption Among Large-Scale Commercial Entities

- Integration of Solar with EV Charging Stations

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now