Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the France Warehousing Market is valued at approximately USD ~ billion, driven by the rapid expansion of e-commerce fulfillment operations, industrial supply chains, and national logistics infrastructure development. Increasing online retail transactions require large distribution centers and automated storage systems capable of processing high parcel volumes efficiently. Investments by logistics operators and real estate developers in technologically advanced warehouses further strengthen capacity expansion across strategic logistics corridors including northern and central distribution hubs.

Major logistics activity is concentrated in metropolitan regions including Paris, Lyon, Marseille, Lille, and Bordeaux due to strong transport connectivity, dense consumer markets, and proximity to international trade routes. Paris functions as the primary logistics gateway supported by large fulfillment centers and multimodal transport infrastructure linking road, rail, and air cargo networks. Lyon and Marseille benefit from industrial manufacturing clusters and seaport access, while Lille’s strategic location near Belgium and the Netherlands supports cross-border European distribution networks.

Market Segmentation

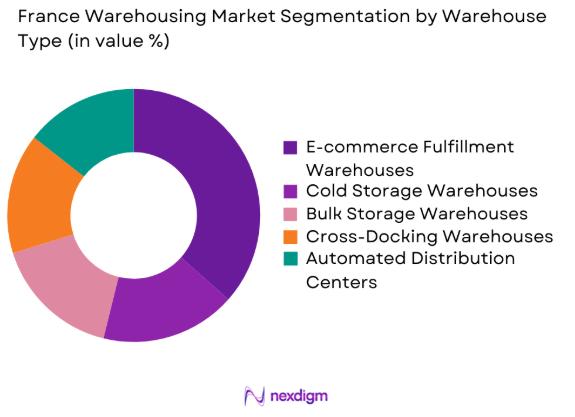

By Warehouse Type

France Warehousing Market is segmented by warehouse type into e-commerce fulfillment warehouses, cold storage warehouses, bulk storage warehouses, cross-docking warehouses, and automated distribution centers. Recently, e-commerce fulfillment warehouses have a dominant market share due to the rapid growth of digital retail platforms and consumer demand for faster delivery services across urban and suburban markets. Large online retailers and logistics providers increasingly operate high-capacity fulfillment facilities equipped with automated sorting systems, robotics-enabled inventory management, and real-time order processing technologies. These warehouses enable high-volume parcel processing and efficient last-mile distribution networks. Their strategic placement near metropolitan consumption centers improves delivery speed while reducing transportation costs. As e-commerce continues to expand, logistics companies prioritize large-scale fulfillment infrastructure investments, further strengthening the operational importance and market dominance of e-commerce fulfillment warehouses within the national warehousing ecosystem.

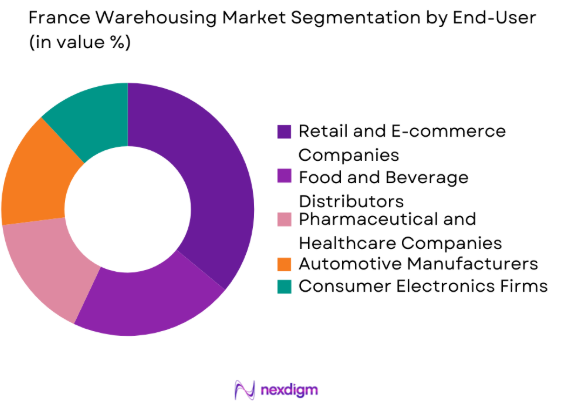

By End-User Industry

France Warehousing Market is segmented by end-user industry into retail and e-commerce companies, food and beverage distributors, pharmaceutical and healthcare companies, automotive manufacturers, and consumer electronics firms. Recently, retail and e-commerce companies have a dominant market share due to the rapid expansion of online shopping platforms and omnichannel retail distribution strategies. Large retailers require high-capacity storage facilities capable of supporting inventory management, packaging, and nationwide parcel distribution operations. Retail supply chains increasingly depend on centralized distribution hubs and regional fulfillment warehouses to support fast order processing and last-mile delivery. Growth in mobile commerce platforms and digital payment adoption further strengthens consumer participation in online retail transactions, significantly increasing warehouse storage demand. As retailers continue expanding omnichannel logistics operations, the retail and e-commerce segment remains the primary driver of warehousing capacity expansion across the national logistics infrastructure.

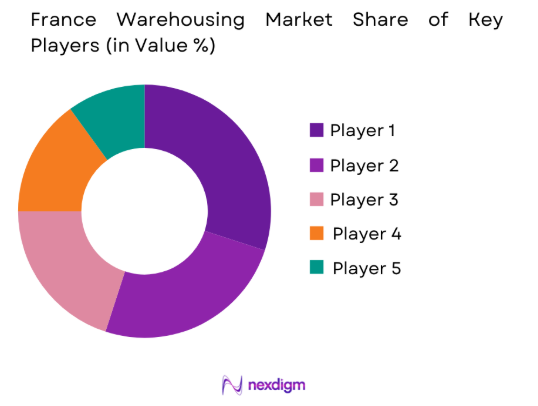

Competitive Landscape

The France Warehousing Market demonstrates moderate consolidation with several global logistics operators and industrial real estate developers controlling large warehouse portfolios across national logistics corridors. Companies focus on expanding automated distribution centers, temperature-controlled facilities, and urban fulfillment hubs to support e-commerce logistics networks. Strategic partnerships between logistics providers, property developers, and major retailers strengthen warehouse capacity expansion. Technological integration including robotics, warehouse management systems, and automated storage infrastructure further differentiates leading market participants.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Warehouse Capacity |

| Prologis | 1983 | USA | ~ | ~ | ~ | ~ | ~ |

| Segro | 1920 | UK | ~ | ~ | ~ | ~ | ~ |

| Goodman Group | 1989 | Australia | ~ | ~ | ~ | ~ | ~ |

| Geodis | 1904 | France | ~ | ~ | ~ | ~ | ~ |

| DHL Supply Chain | 1969 | Germany | ~ | ~ | ~ | ~ | ~ |

France Warehousing Market Analysis

Growth Drivers

Expansion of E-commerce Fulfillment Infrastructure and Digital Retail Supply Chains

Rapid expansion of online retail ecosystems across France significantly increases demand for advanced warehousing infrastructure capable of managing large inventory volumes and enabling rapid order fulfillment. Digital commerce platforms generate high transaction volumes involving consumer electronics, clothing, groceries, and household goods that require efficient storage and distribution networks. Logistics providers respond by developing large fulfillment centers equipped with robotics-enabled storage systems, automated parcel sorting technologies, and advanced warehouse management platforms. Retail companies increasingly adopt omnichannel distribution strategies where warehouses function as centralized inventory hubs linking online and physical retail channels. E-commerce companies also invest in regional fulfillment facilities near major population centers to shorten delivery timelines and reduce logistics costs.

Expansion of Industrial Manufacturing and Export Logistics Networks

France’s strong industrial base significantly drives warehousing demand as manufacturing companies require extensive storage facilities for raw materials, intermediate components, and finished goods within domestic and international supply chains. Automotive manufacturing clusters, aerospace producers, pharmaceutical firms, and consumer goods manufacturers rely on strategically located warehouses linking factories with distribution networks and export gateways. Industrial logistics increasingly depends on multimodal transport infrastructure integrating road freight, rail cargo, air logistics, and maritime shipping through ports such as Marseille and Le Havre. Warehouses positioned along transport corridors help manufacturers streamline inventory management and reduce supply chain lead times. Export-oriented industries also rely on distribution centers that consolidate products before international shipment, supporting efficient cargo handling and logistics coordination.

Market Challenges

High Industrial Land Costs and Limited Urban Logistics Space

Warehousing development in major metropolitan regions of France faces constraints due to rising industrial land prices and limited availability of large sites near urban consumption centers. Logistics providers prefer locations close to dense markets to minimize delivery distances and reduce last-mile transportation costs. However, urban land scarcity and increasing real estate values significantly raise capital investment required to build modern warehouses. Developers compete with residential construction, commercial property projects, and infrastructure development for limited industrial land in logistics corridors near cities such as Paris and Lyon. These pressures increase both construction and operational costs, limiting expansion opportunities for smaller logistics operators. Companies therefore explore multi-story warehouses and suburban distribution hubs, although these alternatives require additional transportation infrastructure investment.

Rising Energy Consumption and Environmental Sustainability Compliance Requirements

Warehousing operations require substantial energy consumption for lighting, automated machinery, refrigeration systems, and climate-controlled environments, particularly in facilities storing pharmaceuticals and temperature-sensitive food products. Environmental regulations across France increasingly require logistics operators to meet strict sustainability standards related to building efficiency, carbon emissions, and industrial energy usage. Developers must therefore invest in energy-efficient materials, improved insulation systems, and renewable energy solutions such as rooftop solar installations. While these measures support national environmental objectives, they also increase capital costs associated with building and operating modern warehouse infrastructure. Logistics companies must implement digital monitoring platforms that track energy usage and ensure regulatory compliance. Transitioning existing warehouse facilities toward sustainable operational models therefore requires significant financial investment and technological upgrades.

Opportunities

Adoption of Automation and Robotics in Smart Warehouse Infrastructure

Integration of advanced automation technologies across warehousing operations creates significant opportunities for logistics providers seeking improved efficiency and productivity within storage and distribution facilities. Robotics-enabled storage systems, automated guided vehicles, and artificial intelligence driven warehouse management platforms accelerate order picking, inventory tracking, and product sorting compared with manual processes. Automated storage and retrieval systems also maximize vertical storage capacity while reducing handling errors and improving inventory accuracy. These technologies allow warehouses to process higher shipment volumes without proportional increases in labor resources. Logistics operators increasingly implement predictive analytics and digital simulation tools that optimize warehouse layouts and operational workflows. As supply chains become more complex and delivery expectations rise, automation technologies help warehouses sustain high operational performance and service reliability.

Development of Urban Micro Fulfillment Centers for Last-Mile Logistics

Rapid growth in urban e-commerce demand is creating opportunities for compact micro-fulfillment centers located within or near major metropolitan areas. These facilities allow logistics providers to store high-turnover consumer goods closer to end customers, reducing last-mile delivery distances and improving delivery speed. Micro-fulfillment centers often integrate robotics-enabled storage systems and automated order picking technologies that enable efficient operations within smaller warehouse spaces. Retail companies increasingly adopt these facilities as part of omnichannel distribution strategies combining online ordering with local inventory access. Strategic placement within metropolitan logistics zones improves distribution flexibility while reducing congestion across long-distance transportation networks. As consumer expectations for faster delivery continue rising, logistics providers increasingly invest in urban distribution infrastructure supporting high-frequency order fulfillment.

Future Outlook

The France Warehousing Market is expected to experience sustained expansion driven by increasing e-commerce activity, industrial supply chain modernization, and infrastructure investments across national logistics networks. Technological advancements including warehouse automation, robotics-enabled storage systems, and artificial intelligence driven inventory management will significantly improve operational productivity. Government support for logistics infrastructure and environmental sustainability initiatives will further accelerate the development of modern energy-efficient warehouses. Rising consumer demand for rapid delivery services will also strengthen investment in urban fulfillment hubs and regional distribution centers.

Major Players

- Prologis

- Segro

- Goodman Group

- GLP Europe

- Panattoni Europe

- Argan

- Logicor

- WDP

- Geodis

- DHL Supply Chain

- Kuehne + Nagel

- DB Schenker

- XPO Logistics

- ID Logistics

- FM Logistic

Key Target Audience

- Logistics infrastructure investors

- Industrial real estate developers

- E-commerce companies

- Third partylogisticsproviders

- Manufacturing companies

- Food and pharmaceutical distributors

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

Key market variables including warehouse capacity, logistics infrastructure development, industrial output, and e-commerce transaction volumes are identified through secondary research. These variables establish the structural foundation for understanding demand patterns within the France Warehousing Market.

Step 2: Market Analysis and Construction

Industry data from logistics operators, industrial real estate developers, and government trade databases are analyzed to construct market size estimates and segmentation structures. Cross-validation with industry publications and supply chain reports ensures data reliability.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts including logistics executives, warehouse developers, and supply chain analysts provide insights validating key assumptions regarding market drivers, technological adoption trends, and infrastructure expansion across the warehousing ecosystem.

Step 4: Research Synthesis and Final Output

All research findings are consolidated into a structured analytical framework integrating quantitative data with qualitative industry insights, producing a comprehensive assessment of the France Warehousing Market and its long-term development trajectory.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expansion of E-commerce Fulfillment and Omnichannel Retail Distribution

Rising Demand for Temperature Controlled Logistics Infrastructure

Growth of Industrial Manufacturing and Export Oriented Supply Chains - Market Challenges

High Industrial Land Costs in Major Logistics Corridors

Complex Zoning Regulations and Infrastructure Approval Procedures

Rising Energy Consumption and Sustainability Compliance Requirements - Market Opportunities

Expansion of Automated Smart Warehousing Technologies

Development of Urban Micro Fulfillment Centers Near Major Cities

Growth of Sustainable Green Warehousing Infrastructure - Trends

Adoption of Robotics and Artificial Intelligence in Warehouse Operations

Integration of Real Time Inventory Tracking and IoT Monitoring Systems

Expansion of Multi Client Shared Warehousing Facilities - Government Regulations

- SWOT Analysis of Key Competitors

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Automated Storage and Retrieval Systems Warehouses

Temperature Controlled Warehouses

Bulk Storage Warehouses

Cross Docking Warehouses

E-commerce Fulfillment Warehouses - By Platform Type (In Value%)

Standalone Warehousing Facilities

Integrated Logistics Parks

Urban Micro Fulfillment Centers

Port Centric Warehousing Facilities

Rail Linked Warehousing Hubs - By Fitment Type (In Value%)

Automated Warehousing Systems

Semi Automated Warehousing Systems

Manual Warehousing Operations

IoT Enabled Smart Warehouses

Robotics Integrated Warehouses - By End User Segment (In Value%)

E-commerce Retailers

Food and Beverage Companies

Pharmaceutical and Healthcare Firms

Automotive Manufacturers

Consumer Electronics Companies - By Procurement Channel (In Value%)

Direct Leasing from Warehouse Operators

Third Party Logistics Service Contracts

Government and Municipal Storage Contracts

Private Logistics Partnerships

Industrial Real Estate Developers

- Market Share Analysis

- Cross Comparison Parameters (Warehouse Capacity, Automation Level, Geographic Coverage, End User Industry Focus, Temperature Control Capability, Warehouse Floor Area, Storage Density, Technology Integration Level, Distribution Network Connectivity, Sustainability Certification)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Prologis

GLP Europe

Segro

Goodman Group

Logicor

WDP

Panattoni Europe

ID Logistics

FM Logistic

DHL Supply Chain

Kuehne + Nagel

DB Schenker

Geodis

XPO Logistics

Argan

- Rapid expansion of e-commerce retailers requiring large fulfillment warehouses

- Increasing pharmaceutical distribution demanding certified storage facilities

- Automotive manufacturers expanding component storage and logistics hubs

- Food retailers investing in cold storage and distribution warehouses

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now