Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Germany Agricultural Electronic Components market reached approximately USD ~ billion based on a recent historical assessment supported by German Federal Ministry of Food and Agriculture digital agriculture investment tracking and Eurostat agricultural machinery electronics data. Market expansion is driven by precision farming adoption, automation of machinery, integration of sensors and control electronics, and electrification of agricultural equipment platforms. Strong domestic electronics manufacturing capability and advanced farm mechanization infrastructure sustain consistent component demand across agricultural machinery OEM supply chains.

Dominant activity is concentrated in Germany, particularly in Bavaria, Baden-Württemberg, and Lower Saxony due to dense agricultural machinery manufacturing clusters and advanced mechanized farming ecosystems. These regions host major agricultural equipment producers and electronics suppliers, enabling strong integration of sensors, control units, and telematics modules into farm machinery. Germany leads European agricultural electronics deployment due to high-value crop cultivation, automation intensity, and established precision farming adoption supported by advanced digital infrastructure and engineering expertise.

Market Segmentation

By Product Type:

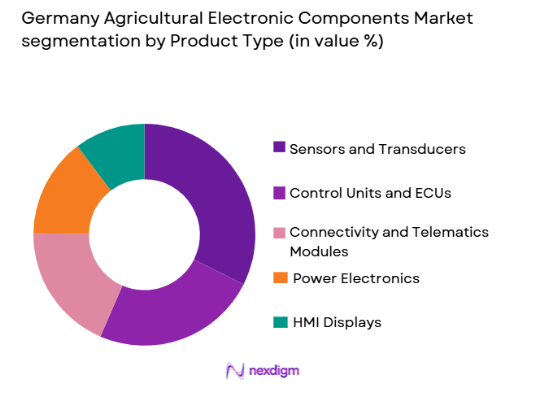

Germany Agricultural Electronic Components market is segmented by product type into sensors and transducers, control units and ECUs, connectivity and telematics modules, power electronics, and HMI displays. Recently, sensors and transducers have a dominant market share due to increasing precision agriculture adoption, automation of crop monitoring, and widespread integration of environmental, soil, and machinery sensors into agricultural equipment platforms. High demand for real-time data acquisition in farming operations, coupled with expansion of smart farming technologies and autonomous machinery development, has accelerated sensor deployment across tractors, harvesters, and crop management systems in Germany.

By Application:

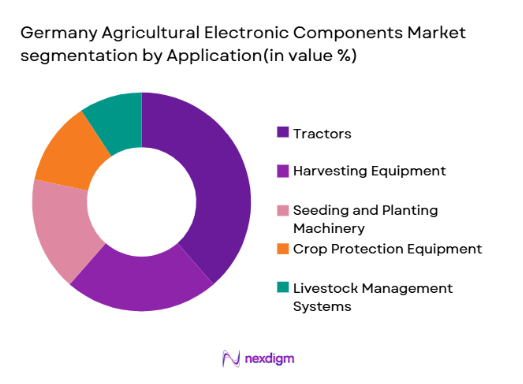

Germany Agricultural Electronic Components market is segmented by application into tractors, harvesting equipment, seeding and planting machinery, crop protection equipment, and livestock management systems. Recently, tractors have a dominant market share due to their central role in mechanized farming operations and the highest integration of electronic control systems, telematics, automation modules, and sensing technologies. Modern German tractors incorporate precision guidance, engine control electronics, implement management systems, and connectivity platforms, driving sustained demand for electronic components across both OEM manufacturing and aftermarket upgrades in agricultural operations.

Competitive Landscape

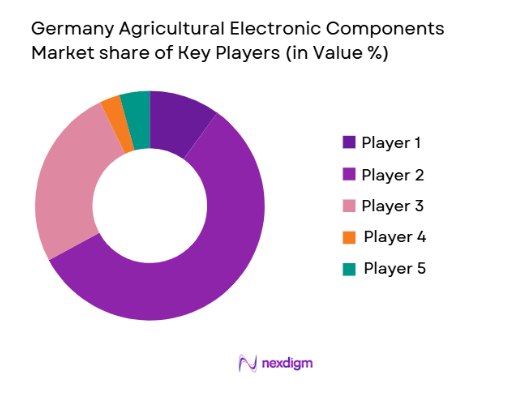

Germany Agricultural Electronic Components market is moderately consolidated, with major industrial electronics manufacturers and specialized agricultural component suppliers dominating OEM supply chains. Large automation and semiconductor firms influence technology standards and integration architectures, while mid-sized sensor and connectivity specialists supply niche agricultural solutions. Strong domestic manufacturing capability and long-term partnerships with agricultural machinery OEMs create high entry barriers and stable competitive positioning across precision farming electronics segments.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Agricultural Integration Focus |

| Bosch Rexroth AG | 2001 | Germany | ~ | ~ | ~ | ~ | ~ |

| Continental AG | 1871 | Germany | ~ | ~ | ~ | ~ | ~ |

| Infineon Technologies AG | 1999 | Germany | ~ | ~ | ~ | ~ | ~ |

| ifm electronic GmbH | 1969 | Germany | ~ | ~ | ~ | ~ | ~ |

| Phoenix Contact GmbH | 1923 | Germany | ~ | ~ | ~ | ~ | ~ |

Germany Agricultural Electronic Components Market Analysis

Growth Drivers

Advanced Precision Farming Technology Adoption:

Precision farming technology adoption in Germany has accelerated demand for agricultural electronic components across machinery platforms and farm management systems. German farms increasingly deploy sensor networks, GPS-guided machinery, and automated control electronics to optimize crop yields and resource utilization. Government-supported digital agriculture programs encourage integration of smart farming technologies into agricultural operations and equipment. Agricultural machinery OEMs incorporate advanced sensing, telematics, and control architectures to enhance operational efficiency and automation capability. High-value crop cultivation and intensive farming practices require real-time monitoring and data-driven machinery control. Strong domestic engineering expertise enables development of sophisticated agricultural electronics solutions tailored to local farming conditions. Expansion of autonomous agricultural machinery research and pilot deployment further increases electronic component integration requirements. Growing emphasis on sustainability and input optimization strengthens adoption of precision electronics across German agricultural systems. Established digital infrastructure and connectivity availability support widespread deployment of telematics-enabled farm equipment.

Agricultural Machinery Electrification and Automation:

Electrification and automation of agricultural machinery platforms significantly increase electronic component integration within German agricultural equipment manufacturing. Modern tractors, harvesters, and implements incorporate power electronics, control modules, sensors, and communication systems to enable automated operation and energy-efficient performance. Electrified drive systems and smart implement control architectures require advanced semiconductors and embedded electronics for operational management. Agricultural equipment manufacturers in Germany are transitioning toward intelligent machinery platforms with integrated electronic control networks. Automation of field operations, including steering, application control, and harvesting processes, depends on robust electronic subsystems. Demand for machine-to-machine communication and fleet management solutions drives connectivity electronics integration. Electrification initiatives aligned with emissions reduction goals accelerate development of electric and hybrid agricultural equipment. German engineering leadership in industrial automation supports rapid adoption of electronic architectures in agriculture. OEM investment in digital and autonomous machinery platforms sustains long-term growth in agricultural electronic component demand.

Market Challenges

Harsh Agricultural Operating Environment Constraints:

Agricultural machinery operates in extreme environmental conditions including vibration, moisture, dust, and temperature variability, creating durability challenges for electronic components in Germany Agricultural Electronic Components market. Components must meet high ruggedization standards and extended operational lifecycles to withstand field conditions. Failure risks increase maintenance costs and reduce reliability of precision farming systems. Designing electronics capable of sustained agricultural deployment requires specialized materials, encapsulation technologies, and testing protocols. Compliance with agricultural machinery safety and environmental regulations adds complexity to component engineering and certification processes. Continuous exposure to chemicals, soil, and mechanical stress accelerates degradation of sensors and connectors. Ensuring long-term stability of electronic performance in field machinery environments remains a major technical barrier. OEMs demand highly robust components with minimal failure rates, increasing development costs. Environmental durability requirements limit rapid adoption of consumer-grade electronics technologies in agricultural machinery systems.

Semiconductor Supply Chain Volatility:

Global semiconductor supply chain disruptions significantly impact availability and pricing of agricultural electronic components in Germany Agricultural Electronic Components market. Agricultural machinery electronics depend on automotive-grade semiconductors, sensors, and microcontrollers subject to cyclical shortages and geopolitical supply risks. Component lead times and procurement uncertainty disrupt OEM production schedules and machinery manufacturing output. Dependence on specialized semiconductor fabrication and packaging capabilities outside Germany increases vulnerability to global market fluctuations. Price volatility in chips and electronic materials elevates production costs for agricultural electronics suppliers. Supply chain instability complicates long-term procurement planning for machinery manufacturers and component vendors. Agricultural electronics often compete with automotive and industrial sectors for semiconductor allocation priority. Limited local semiconductor manufacturing capacity restricts supply resilience in agricultural electronics. Ongoing geopolitical and trade dynamics continue to affect semiconductor availability for German agricultural equipment production.

Opportunities

Autonomous Agricultural Machinery Electronics Development:

Development of autonomous agricultural machinery in Germany Agricultural Electronic Components market creates substantial demand for advanced sensing, computing, and control electronics. Autonomous tractors, robotic harvesters, and intelligent implements require sophisticated sensor fusion, perception systems, and embedded control architectures. Integration of artificial intelligence and machine vision technologies into farm equipment drives high-value electronic component adoption. German agricultural machinery manufacturers actively invest in autonomous platform research and pilot deployment programs. Advanced electronics enable self-navigation, obstacle detection, crop recognition, and automated task execution in farming operations. Demand for high-performance processing units and sensor arrays increases with autonomous capability expansion. Agricultural robotics adoption accelerates electronics content per machine and raises system complexity. Collaboration between agricultural equipment OEMs and electronics suppliers supports innovation in autonomous systems. Germany’s strong automation and robotics ecosystem provides a technological foundation for growth in autonomous agricultural electronics.

Localized Manufacturing and Supply Chain Resilience Initiatives:

Strengthening localized manufacturing of agricultural electronic components in Germany Agricultural Electronic Components market presents significant opportunity for supply chain resilience and technology leadership. European initiatives promoting semiconductor and electronics manufacturing independence encourage domestic production capacity expansion. Localization reduces dependency on global supply chains and mitigates semiconductor shortages impacting agricultural machinery production. German electronics firms can develop specialized agricultural-grade components tailored to regional machinery requirements. Closer collaboration between component manufacturers and agricultural OEMs enhances product customization and integration efficiency. Domestic production supports faster innovation cycles and shorter lead times for agricultural electronics. Government industrial policy promoting advanced manufacturing strengthens investment in electronics fabrication and assembly. Localization initiatives align with strategic autonomy goals in critical industrial technologies. Expansion of regional electronics ecosystems enables long-term growth and stability in agricultural electronic component supply for German agriculture.

Future Outlook

Germany Agricultural Electronic Components market is expected to experience steady expansion over the next five years driven by automation, electrification, and precision agriculture technology adoption. Integration of autonomous machinery electronics and AI-enabled sensing systems will increase component intensity per agricultural machine. Regulatory emphasis on sustainable and efficient farming practices will further accelerate digital agriculture deployment. Continued OEM innovation and localized electronics manufacturing initiatives are likely to strengthen market growth and technological advancement across German agricultural equipment sectors.

Major Players

- Bosch Rexroth AG

- Continental AG

- Infineon Technologies AG

- ifm electronic GmbH

- Phoenix Contact GmbH

- WAGO GmbH & Co. KG

- Balluff GmbH

- Turck Holding GmbH

- Beckhoff Automation GmbH & Co. KG

- Festo SE & Co. KG

- Kostal Industrie Elektrik GmbH

- Liebherr Electronics and Drives GmbH

- Hella GmbH & Co. KGaA

- Siemens AG

- Epec Oy

Key Target Audience

- Agricultural machinery manufacturers

- Agricultural electronicscomponent suppliers

- Precision farming technology providers

- Farm automation solution integrators

- Agricultural equipment distributors

- Semiconductor and sensor manufacturers

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

Market variables including agricultural machinery production, electronics integration rates, precision farming adoption, and component supply chains were identified through industry datasets, government agricultural technology programs, and manufacturing statistics.

Step 2: Market Analysis and Construction

Market size and segmentation were constructed using agricultural machinery electronics content estimates, OEM production volumes, component pricing benchmarks, and technology adoption levels across German farming sectors.

Step 3: Hypothesis Validation and Expert Consultation

Assumptions and market structure were validated through consultation with agricultural equipment engineers, electronics suppliers, and precision farming technology specialists across Germany’s agricultural machinery ecosystem.

Step 4: Research Synthesis and Final Output

All quantitative and qualitative insights were synthesized into coherent market modeling, ensuring alignment with agricultural mechanization trends, electronics integration evolution, and German agricultural technology policies.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expansion of precision agriculture adoption across German farms

Automation demand in high-value crop cultivation

Electrification of agricultural machinery platforms

Government support for digital farming technologies

Integration of IoT connectivity in farm equipment - Market Challenges

High certification and compliance requirements for agri-electronics

Harsh operating environments affecting component durability

Complex integration with legacy machinery platforms

Supply chain volatility in semiconductor components

Cost sensitivity among small and mid-scale farms - Market Opportunities

Development of autonomous farming electronics architectures

Localized manufacturing of rugged agricultural electronics

Advanced sensor fusion systems for smart farming - Trends

Shift toward data-driven farm management electronics

Adoption of ISOBUS-compliant control systems

Miniaturization of agricultural sensing components

Growth of edge computing in farm machinery

Integration of AI-enabled control modules - Government Regulations & Defense Policy

EU machinery and electronic safety directives compliance

German digital agriculture funding frameworks

Environmental and emissions monitoring mandates - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Precision farming control units

Sensor modules and transducers

Power electronics and controllers

Connectivity and telematics modules

Display and HMI components - By Platform Type (In Value%)

Tractors and power units

Harvesting equipment

Seeding and planting machinery

Crop protection equipment

Livestock management systems - By Fitment Type (In Value%)

OEM integrated electronics

Retrofit electronic kits

Modular add-on systems

Embedded control assemblies

Aftermarket replacement electronics - By EndUser Segment (In Value%)

Large commercial farms

Medium-scale family farms

Agricultural contractors

Agri-equipment OEMs

Research and pilot farms - By Procurement Channel (In Value%)

Direct OEM supply contracts

Authorized agricultural dealers

Industrial electronics distributors

Online B2B procurement platforms

System integrator partnerships - By Material / Technology (in Value %)

Silicon-based semiconductors

Printed circuit assemblies

MEMS sensing technology

Wireless communication chipsets

Ruggedized encapsulation materials

- Market structure and competitive positioning

- Market share snapshot of major players

- CrossComparison Parameters (Product Portfolio Breadth, Agricultural Application Coverage, Integration Capability, Ruggedization Standards, OEM Partnerships, Innovation in Precision Electronics, Manufacturing Localization, Cost Competitiveness, Aftermarket Support, Compliance Certifications)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

Bosch Rexroth AG

Continental AG

Infineon Technologies AG

Hella GmbH and Co. KGaA

Siemens AG

Phoenix Contact GmbH and Co. KG

WAGO GmbH and Co. KG

Balluff GmbH

ifm electronic GmbH

Turck Holding GmbH

Liebherr Electronics and Drives GmbH

Festo SE and Co. KG

Beckhoff Automation GmbH and Co. KG

Kostal Industrie Elektrik GmbH

Epec Oy

- Large farms prioritizing integrated precision electronics systems

- Contractors investing in retrofit automation modules

- OEMs embedding proprietary electronic architectures

- Research farms piloting advanced sensing and control electronics

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now