Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the Germany AI Infrastructure Market reached approximately USD ~ billion, supported by rapid enterprise AI adoption, expansion of AI-optimized data centers, and national investments under the Digital Strategy and Industry 4.0 programs. Strong demand for GPU compute clusters, high-performance storage, and AI networking fabrics from automotive, manufacturing, and research sectors accelerated infrastructure spending. Hyperscale cloud providers and domestic enterprises expanded AI compute capacity across German digital infrastructure ecosystems.

Frankfurt, Berlin, and Munich dominate AI infrastructure deployment due to concentration of hyperscale data centers, AI research institutes, and industrial technology firms requiring large-scale AI compute environments. Hesse benefits from Europe’s largest internet exchange and dense cloud campuses, while Bavaria hosts automotive AI development and semiconductor research clusters. Berlin’s startup and AI innovation ecosystem drives demand for GPU cloud and AI platforms, attracting infrastructure investment across Germany’s major digital technology hubs.

Market Segmentation

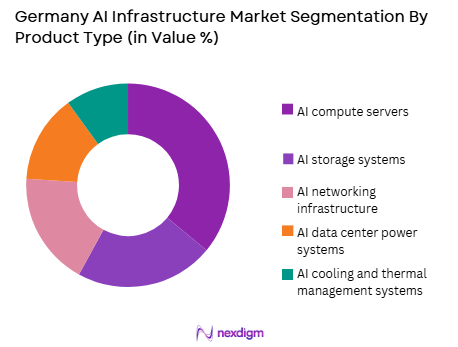

By Product Type

Germany AI Infrastructure market is segmented by product type into AI compute servers, AI storage systems, AI networking infrastructure, AI data center power systems, and AI cooling and thermal management systems. Recently, AI compute servers has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. AI compute servers dominate because enterprise and research AI workloads in Germany require high-performance GPU and accelerator clusters to support machine learning training, generative AI models, and industrial AI analytics. Automotive, manufacturing, and engineering firms invest heavily in on-premise and cloud-based AI compute capacity to enable autonomous systems and predictive manufacturing applications. Hyperscale and colocation providers deploy dense GPU server racks to support AI cloud services regionally. AI infrastructure refresh cycles are faster for compute accelerators than for storage or power systems, sustaining recurring capital expenditure. National AI strategy funding prioritizes compute capacity expansion across research centers. As AI applications remain compute-intensive, AI compute servers structurally maintain the largest share within Germany’s AI infrastructure market.

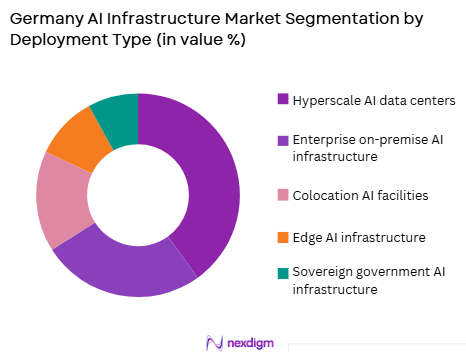

By Deployment Type

Germany AI Infrastructure market is segmented by deployment type into hyperscale AI data centers, enterprise on-premise AI infrastructure, colocation AI facilities, edge AI infrastructure, and sovereign government AI infrastructure. Recently, hyperscale AI data centers has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Hyperscale AI data centers dominate because global cloud providers continue expanding GPU-optimized AI regions in Germany to support enterprise AI adoption and European data sovereignty requirements. Frankfurt’s connectivity ecosystem and renewable energy access attract hyperscale AI campuses serving continental markets. Enterprises increasingly prefer cloud-based AI platforms over building large internal GPU clusters due to scalability and cost efficiency. Hyperscale facilities enable shared AI compute resources for multiple industries including automotive, finance, and healthcare. EU data residency policies further encourage localized AI cloud infrastructure. Rapid growth of generative AI services concentrates investment into hyperscale GPU clusters. These structural drivers sustain hyperscale AI data centers as the leading deployment segment in Germany’s AI infrastructure market.

Competitive Landscape

The Germany AI Infrastructure Market is dominated by global hyperscale cloud providers, semiconductor AI hardware firms, and European data center operators delivering GPU compute capacity and AI-optimized facilities. Domestic engineering and colocation companies support deployment of AI data center campuses across Frankfurt, Berlin, and Munich. Competition focuses on GPU density, AI cloud platforms, energy-efficient cooling, and compliance with EU data sovereignty and security standards.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | AI Infrastructure Role |

| NVIDIA | 1993 | USA | ~ | ~ | ~ | ~ | ~ |

| Intel | 1968 | USA | ~ | ~ | ~ | ~ | ~ |

| AMD | 1969 | USA | ~ | ~ | ~ | ~ | ~ |

| Amazon Web Services | 2006 | USA | ~ | ~ | ~ | ~ | ~ |

| Equinix | 1998 | USA | ~ | ~ | ~ | ~ | ~ |

Germany AI Infrastructure Market Analysis

Growth Drivers

Industrial AI Adoption Across Manufacturing and Automotive Sectors

Germany’s strong industrial base in automotive, machinery, and advanced manufacturing is rapidly integrating artificial intelligence into production, design, and operational optimization processes, driving substantial demand for AI infrastructure. Industrial AI applications such as predictive maintenance, computer vision quality inspection, digital twins, and autonomous robotics require high-performance compute clusters and large-scale data processing environments. Automotive firms developing autonomous driving and intelligent mobility platforms invest heavily in AI training infrastructure and simulation compute capacity. Manufacturing companies deploy AI analytics and real-time optimization systems requiring scalable GPU servers and high-speed networking fabrics. Industry 4.0 initiatives encourage digital transformation across factories, increasing demand for localized and cloud-based AI infrastructure. Research collaborations between industry and Fraunhofer institutes expand AI compute capacity in applied industrial environments. Industrial datasets generated by sensors and machines require AI storage and processing infrastructure at scale. German enterprises increasingly adopt AI cloud platforms to accelerate innovation cycles. These sector-specific AI adoption patterns structurally drive sustained expansion of Germany’s AI infrastructure market.

Expansion of European AI Sovereignty and Cloud Infrastructure Programs

European Union and German national strategies emphasizing AI sovereignty and data independence are accelerating deployment of domestic AI infrastructure across hyperscale and sovereign cloud environments. Initiatives supporting European AI capabilities incentivize investment into localized GPU data centers and trusted AI cloud platforms within Germany. Data sovereignty regulations require sensitive industrial and public-sector AI workloads to be processed within EU jurisdictions, stimulating domestic infrastructure expansion. Sovereign AI cloud programs encourage collaboration between European cloud providers and semiconductor firms to build independent AI compute ecosystems. Public funding supports AI research supercomputers and national AI compute clusters across German research institutions. Enterprises in regulated sectors increasingly prefer sovereign AI infrastructure compliant with EU standards. Regional AI data center expansion also supports cross-border European AI collaboration networks. Germany’s central position in European digital infrastructure strengthens its role as a continental AI compute hub. These policy-driven investments significantly accelerate AI infrastructure deployment across Germany.

Market Challenges

High Energy Demand and Cooling Requirements of AI Compute Clusters

AI infrastructure deployment in Germany faces major challenges due to extremely high energy consumption and thermal management requirements of dense GPU and accelerator clusters. AI training workloads require power-intensive servers operating continuously at high utilization, increasing electricity demand within data centers. Germany’s relatively high energy costs affect operational economics of AI compute infrastructure compared to other regions. Advanced liquid cooling and thermal management systems increase capital expenditure for AI-optimized data centers. Grid capacity constraints and energy approval processes can delay large AI data center construction projects. Sustainability and carbon reduction requirements impose additional investment in renewable energy sourcing and efficiency technologies. Heat dissipation challenges limit achievable compute density in certain facilities. Environmental regulations governing industrial energy use further influence infrastructure deployment decisions. These combined energy and cooling constraints restrict rapid scaling of AI infrastructure capacity in Germany.

Dependence on Imported AI Semiconductor Hardware Supply Chains

Germany’s AI infrastructure ecosystem relies heavily on imported semiconductor hardware such as GPUs, accelerators, and AI processors, creating supply chain vulnerabilities and deployment uncertainties. Global shortages or geopolitical restrictions affecting advanced AI chips can directly constrain infrastructure expansion within Germany. Limited domestic production of advanced AI accelerators reduces national control over critical AI compute components. Long procurement cycles and high costs for AI hardware impact infrastructure investment planning for enterprises and cloud providers. Export controls and technology restrictions may affect access to cutting-edge AI processors. Dependence on foreign semiconductor ecosystems also affects upgrade cycles and technology availability timelines. European semiconductor initiatives are still developing domestic AI hardware capabilities. Infrastructure operators face pricing volatility for GPU systems due to global demand fluctuations. These supply chain dependencies represent structural challenges for Germany’s AI infrastructure growth trajectory.

Opportunities

Development of AI Supercomputing and National Compute Clusters

Germany has significant opportunities to expand AI supercomputing infrastructure and national AI compute clusters to support research, industry, and public sector AI innovation. Government-funded AI supercomputers and high-performance computing centers can provide shared GPU resources for enterprises and startups lacking large internal infrastructure. National AI compute platforms support development of large language models and industrial AI applications domestically. Integration of AI supercomputing with research institutions strengthens Germany’s AI innovation ecosystem. Public-private partnerships can accelerate deployment of large-scale AI compute clusters. Shared AI infrastructure improves accessibility and competitiveness of German AI companies globally. EU funding programs for digital infrastructure further support national AI compute expansion. Supercomputing facilities also anchor regional AI ecosystems and talent development. This national AI compute infrastructure pathway offers substantial growth potential within Germany’s AI infrastructure market.

Edge AI Infrastructure for Industrial and Smart City Applications

Germany’s advanced industrial and urban infrastructure creates opportunities for distributed edge AI infrastructure supporting real-time analytics and autonomous systems. Manufacturing plants, logistics networks, and smart city platforms require localized AI processing close to data sources for latency-sensitive applications. Edge AI infrastructure complements centralized hyperscale AI data centers by enabling on-site inference and analytics. Industrial IoT deployments generate continuous data streams requiring edge processing capacity. Autonomous vehicles and intelligent transportation systems depend on distributed AI compute environments. Municipal digitalization programs encourage smart infrastructure and urban AI services. Telecommunications 5G networks support deployment of edge AI nodes nationwide. Integration of edge and cloud AI architectures expands infrastructure demand. Distributed industrial AI ecosystems therefore present significant opportunities for Germany’s AI infrastructure expansion.

Future Outlook

Germany’s AI infrastructure market is expected to expand strongly over the next five years driven by industrial AI adoption, sovereign AI programs, and hyperscale GPU data center growth. AI supercomputing clusters and edge AI deployment across manufacturing and cities will shape infrastructure expansion. Energy-efficient cooling and renewable-powered AI data centers will gain importance. EU digital sovereignty policies and industrial AI demand will sustain investment momentum nationwide.

Major Players

- NVIDIA

- Intel

- AMD

- Amazon Web Services

- Equinix

- Microsoft

- IBM

- Oracle

- Atos

- Deutsche Telekom

- OVHcloud

- SAP

- Hewlett Packard Enterprise

- Dell Technologies

Key Target Audience

- Automotive and manufacturing companies

- Cloud service providers

- Data center operators

- AI software and platform companies

- Telecommunications companies

- Investments and venture capitalist firms

- Government and regulatory bodies

- Industrial automation companies

Research Methodology

Step 1: Identification of Key Variables

AI infrastructure components including GPU compute, storage, networking, power, cooling, and deployment models were identified through AI hardware market data, data center capacity statistics, and European digital infrastructure policy frameworks. Industrial AI demand drivers across manufacturing, automotive, and research sectors were mapped to infrastructure requirements.

Step 2: Market Analysis and Construction

Market size and segmentation were constructed using AI data center capacity additions, GPU deployment estimates, and enterprise AI infrastructure spending across Germany. Infrastructure component ratios and deployment patterns were synthesized to derive segment shares and overall market structure.

Step 3: Hypothesis Validation and Expert Consultation

Market assumptions regarding hyperscale dominance, compute infrastructure share, and industrial AI demand were validated through AI infrastructure engineers, data center operators, and industrial digitalization experts. Cross-verification ensured alignment with Germany’s AI deployment trends.

Step 4: Research Synthesis and Final Output

Validated quantitative and qualitative inputs were integrated into a structured AI infrastructure market model covering segmentation, drivers, challenges, and opportunities. Competitive landscape and outlook were derived from AI adoption trajectories and infrastructure investment plans across Germany.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Industrial AI adoption across automotive and manufacturing sectors

Expansion of sovereign and regulated AI cloud infrastructure

Rising demand for generative AI and HPC compute capacity - Market Challenges

Power density and cooling constraints in high-performance AI clusters

Data sovereignty and compliance requirements for AI workloads

Shortage of specialized AI infrastructure engineering talent - Market Opportunities

AI infrastructure for autonomous mobility and Industry 4.0

Federated and sovereign AI cloud deployments in Europe

Next-generation energy-efficient AI data centers - Trends

Shift toward GPU and accelerator-dense AI data centers

Adoption of liquid cooling for high-density AI racks

Integration of AI workloads across edge and cloud - Government regulations

European AI Act and compliance frameworks

Data sovereignty and industrial data governance rules

Energy efficiency and green data center regulations - SWOT analysis

- Porters Five forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

AI compute servers

AI storage and data pipeline systems

High-speed AI networking infrastructure

AI accelerator and GPU clusters

AI data center cooling and power systems - By Platform Type (In Value%)

Hyperscale AI cloud data centers

Enterprise AI private infrastructure

Edge AI compute facilities

Research and HPC AI clusters

Sovereign AI cloud platforms - By Fitment Type (In Value%)

Greenfield AI data center builds

Brownfield AI infrastructure upgrades

Modular AI pod deployments

On-premise AI cluster installations

Hybrid distributed AI integrations - By End User Segment (In Value%)

Cloud and AI service providers

Automotive and manufacturing firms

Financial and enterprise technology firms

Research institutions and universities

Government and defense agencies - By Procurement Channel (In Value%)

Direct OEM procurement

Systems integrator deployment contracts

Cloud provider infrastructure sourcing

Public sector procurement programs

HPC consortium procurement

- Market Share Analysis

- Cross Comparison Parameters (AI Compute Density, Accelerator Integration, Cooling Architecture, Network Throughput, Sovereign Compliance, Energy Efficiency, Scalability, Latency Performance, Automation Level, Interconnect Technology)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

NVIDIA

AMD

Intel

Atos

Siemens

SAP

T-Systems

Deutsche Telekom

OVHcloud

IBM

Hewlett Packard Enterprise

Dell Technologies

Lenovo

Supermicro

Fujitsu

- Automotive OEMs deploying AI training and simulation clusters

- Manufacturers integrating AI for predictive and autonomous operations

- Cloud providers expanding regulated AI regions

- Research institutions scaling HPC and AI compute capacity

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now