Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Germany Courier, Express, and Parcel (CEP) market was valued at approximately USD ~ billion based on a recent historical assessment, driven by the expansion of e‑commerce, demand for rapid delivery, and increasing integration of logistics technologies such as automated sorting and real‑time tracking. The growth in consumer online shopping and rising expectations for last‑mile delivery services have propelled parcel volumes, encouraging carriers to invest in infrastructure and digital solutions to maintain efficiency.

Germany’s CEP sector exhibits pronounced activity in major logistics hubs such as Frankfurt, Munich, and Hamburg, underpinned by advanced transportation networks, central European connectivity, and strong industrial and retail bases. These cities serve as critical nodes for domestic distribution and international transit due to their proximity to key highways, airports, and rail terminals. The presence of large carrier operations and strategic hubs enhances service reliability and enables efficient handling of both domestic parcels and cross‑border flows within Europe.

Market Segmentation

By Service Type

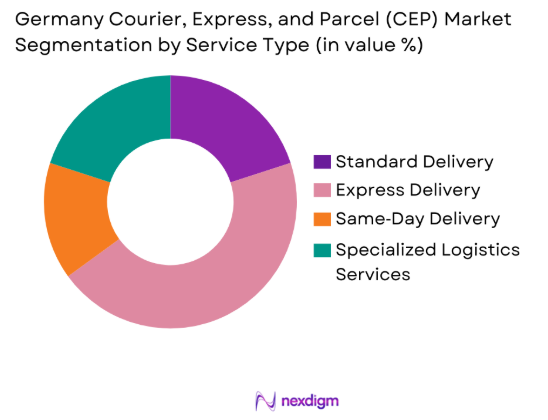

The Germany CEP market is segmented by service type into standard delivery, express delivery, same‑day delivery, and specialized logistics services. Recently, express delivery has a dominant market share due to heightened demand for fast and time‑sensitive shipments, particularly from e‑commerce platforms and business clients requiring guaranteed delivery windows. Express services benefit from premium pricing structures and extensive network investments by major carriers, making them more resilient to cost pressures and operational constraints. The preference for expedited delivery has been reinforced by consumer expectations for rapid turnarounds and competitive differentiation among logistics providers, which has driven capacity enhancements, technology uptake, and wider coverage of express offerings.

By End User Segment

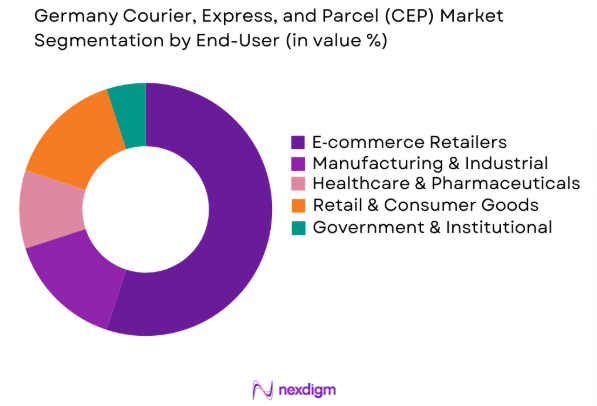

The Germany CEP market is segmented by end user into e‑commerce retailers, manufacturing and industrial enterprises, healthcare and pharmaceuticals, retail and consumer goods, and government and institutional users. Recently, e‑commerce retailers have a dominant market share due to the sustained growth in online shopping, increasing parcel volumes, and the reliance on integrated logistics for omnichannel fulfillment. E‑commerce operations depend on robust CEP networks to meet customer service levels, manage returns, and provide tracking transparency. This reliance has encouraged carriers to tailor solutions for e‑commerce volumes, optimize last‑mile delivery, and expand service options like flexible delivery windows and digital notifications, solidifying their role as preferred logistics partners.

Competitive Landscape

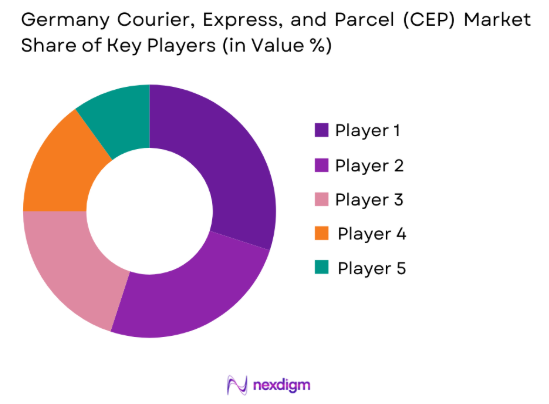

The competitive landscape of the Germany CEP market is characterized by a mix of large multinational logistics firms and regional operators, with consolidation occurring through network expansion and service diversification. Major players leverage extensive distribution networks, technological investments in automation and tracking, and scalable operations to maintain competitive positions. Intense competition and regulatory pressures have prompted partnerships and strategic alliances, especially in digital services and green logistics. Continuous innovation in delivery options and customer service capabilities shapes rivalry, while economies of scale remain a key differentiator among top carriers.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (Approx.) | Market‑Specific Metric |

| DHL | 1969 | Bonn, Germany | ~ | ~ | ~ | ~ | ~ |

| DPD Group | 1977 | Asnières‑sur‑Seine, France | ~ | ~ | ~ | ~ | ~ |

| Hermes Germany | 1972 | Hamburg, Germany | ~ | ~ | ~ | ~ | ~ |

| UPS Germany | 1907 | Atlanta, US | ~ | ~ | ~ | ~ | ~ |

| FedEx Express Germany | 1971 | Memphis, US | ~ | ~ | ~ | ~ | ~ |

Germany Courier, Express, and Parcel (CEP) Market Analysis

Growth Drivers

E‑commerce Expansion and Digital Consumption

The rapid growth of e‑commerce and digital consumption has driven the Germany CEP market, as online shopping platforms generate high parcel volumes requiring robust delivery networks and advanced logistics solutions. Carriers have upgraded terminals and invested in automation to manage throughput and maintain service quality, while competition has intensified to provide flexible options such as time‑definite and same‑day delivery. Integration of data analytics and real‑time tracking enhances operational efficiency and capacity planning. Partnerships with e‑commerce marketplaces strengthen network capabilities and optimize fulfillment, reducing transit times and costs. Digital supply chain integration, sustainability initiatives like electric fleets, and workforce training programs further support service reliability, regulatory compliance, and responsiveness to evolving consumer expectations.

Urban Logistics Infrastructure and Connectivity

Germany’s well‑developed urban logistics infrastructure and connectivity have supported CEP market growth by enabling efficient parcel movement across dense metropolitan areas and major transport hubs. Investments in multimodal terminals connecting road, rail, and air freight reduce transit times and enhance network flexibility. Carriers deploy micro‑fulfillment centers and decentralized sorting facilities near cities to expedite last‑mile delivery and lower costs. Advanced traffic management and digital routing optimize delivery paths, while government-backed smart city pilots integrate real‑time data and adaptive scheduling. Public‑private initiatives expand parcel locker networks, electric and low‑emission vehicles improve sustainability, and strong EU freight links support cross‑border flows, reinforcing Germany’s role as a central European logistics hub and sustaining market resilience.

Market Challenges

Regulatory Compliance and Environmental Mandates

Strict regulatory compliance and environmental mandates create major challenges for the Germany CEP market, requiring carriers to invest in electric delivery vehicles, low‑emission logistics facilities, and greener technologies that raise capital and operational complexity. Emissions standards in urban areas force route redesigns and adoption of alternative propulsion systems, while zero‑emission zones demand technology upgrades to maintain coverage without penalties. Compliance with evolving data privacy, labor, and safety regulations adds administrative burdens and elevates workforce costs. Balancing service speed with environmental commitments impacts pricing and competitiveness, and energy price fluctuations influence strategic planning for sustainable infrastructure. Smaller carriers face difficulties matching larger players’ compliance capabilities, necessitating dedicated teams and dynamic policies to manage regulatory changes effectively.

Rising Operational Costs and Workforce Constraints

Rising operational costs and workforce constraints pose significant challenges for the Germany CEP market, as carriers contend with higher labor expenses, wage inflation, and competition for skilled logistics personnel that compress margins and limit service expansion. Driver shortages and high turnover disrupt network efficiency, increasing dependence on temporary labor solutions. Escalating fuel and energy costs further elevate delivery expenses, forcing pricing adjustments that may affect demand. Investments in automation and technology, though essential for competitiveness, require substantial capital that smaller operators struggle to secure. Maintaining consistent service across urban and rural zones, integrating advanced systems, and addressing fluctuating demand complicate workforce planning and resource allocation, while balancing costs and innovation pressures limits strategic flexibility and operational resilience.

Opportunities

Integration of Automation and AI in CEP Operations

The integration of automation and artificial intelligence in Germany’s CEP operations creates significant opportunities, allowing carriers to enhance sorting accuracy, optimize delivery routes, and reduce reliance on manual labor. Robotic sorting centers efficiently handle high parcel volumes, minimizing peak‑time bottlenecks and improving throughput. AI‑driven analytics enable demand forecasting and resource allocation, lowering delays and operational costs, while dynamic route optimization leverages real‑time data for fuel efficiency and timely deliveries. Autonomous delivery technologies and drones offer long‑term last‑mile solutions. Machine learning improves tracking accuracy and customer communication, and partnerships with tech innovators accelerate advanced system adoption. Investments in digital infrastructure support scalable, efficient operations.

Expansion of Cross‑Border and EU Intra‑Regional CEP Services

Expansion of cross‑border and intra‑EU CEP services presents significant opportunities for German carriers, leveraging Germany’s central location and robust freight networks to serve pan‑European parcel flows. Harmonized EU customs and VAT processes reduce transaction friction, improving operational efficiency. Carriers can support growing e‑commerce exports through integrated European networks, while partnerships with regional operators expand market reach with lower capital investment. Investments in cross‑border sorting hubs near ports and airports increase throughput and transit speed. Unified digital tracking platforms enhance customer experience, and tailored international offerings strengthen scalability. Aligning services with EU trade corridors fosters competitive advantage and reduces reliance on domestic demand fluctuations.

Future Outlook

The Germany CEP market is expected to continue its structural growth trajectory supported by sustained e‑commerce demand, technological innovation, and expanding last‑mile delivery solutions. Investments in automation, AI, and green logistics will shape operational models, enabling carriers to improve efficiency and service quality. Regulatory support for low‑emission zones and sustainable infrastructure will drive adoption of electric fleets and low‑impact delivery methods. Increasing cross‑border parcel flows within Europe present avenues for network expansion, while customer expectations for faster, transparent logistics will drive service differentiation. Continued enhancements in digital platforms and intermodal connectivity will ensure resilience and competitiveness in the broader European logistics landscape.

Major Players

- Deutsche Post DHL Group

- DPD Germany

- Hermes Germany

- GLS Germany

- UPS Germany

- FedEx Germany

- TNT Express Germany

- Amazon Logistics Germany

- Hellmann Worldwide Logistics

- Kuehne + Nagel Germany

- DB Schenker Germany

- GO! Express & Logistics

- SPEED Courier Service GmbH

- Steinfurth & Co GmbH

Key Target Audience

- Logistics and transportation companies

- E‑commerce retailers with delivery needs

- Investment and venture capitalist firms

- Retail and consumer goods enterprises

- Manufacturing and industrial conglomerates

- Healthcare and pharmaceutical distributors

- Government and regulatory bodies

- Regional delivery service providers

Research Methodology

Step 1: Identification of Key Variables

This step involves identifying crucial market variables including service types, delivery modes, end‑user segments, and competitive landscape factors that define the CEP market structure and its performance metrics.

Step 2: Market Analysis and Construction

Market analysis is conducted through data aggregation from industry reports, revenue figures, shipment volumes, and trend indicators to build a comprehensive view of Germany’s CEP market dynamics and segmentation.

Step 3: Hypothesis Validation and Expert Consultation

Hypotheses about key drivers, challenges, and opportunities are validated through interviews with industry experts, logistics professionals, and regional CEP operators to ensure alignment with practical market insights.

Step 4: Research Synthesis and Final Output

The final step integrates quantitative data, expert feedback, and industry trends into a coherent report, synthesizing findings and presenting structured conclusions about market size, forecasts, and strategic implications.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising E-commerce Penetration in Germany

Advanced Urban Logistics Infrastructure

Increasing Demand for Rapid Delivery Services - Market Challenges

Regulatory Compliance and Environmental Constraints

Rising Operational Costs and Labor Shortages

Technological Integration Across Multiple Platforms - Market Opportunities

Expansion of Green and Electric Delivery Fleets

Integration of AI and IoT in CEP Operations

Regional Expansion of Cross-border Parcel Networks - Trends

Automation in Sorting and Last-Mile Delivery

Growth of Contactless and Digital Payment Solutions

Urban Micro-Fulfillment Centers Expansion - Government Regulations

- SWOT Analysis of Key Competitors

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Parcel Delivery Systems

Express Courier Solutions

Same-Day Delivery Services

E-commerce Logistics Platforms

Cold Chain Parcel Systems - By Platform Type (In Value%)

Road Transport

Air Freight

Rail Freight

Urban Micro-Delivery Vehicles

Automated Sorting Hubs - By Fitment Type (In Value%)

On-demand Delivery

Subscription-based Logistics

Integrated Delivery Networks

Third-party Logistics Outsourcing

Hybrid Delivery Solutions - By End User Segment (In Value%)

E-commerce Retailers

Food & Beverage Companies

Pharmaceutical and Healthcare Providers

Manufacturing & Industrial Enterprises

Government Agencies - By Procurement Channel (In Value%)

Direct Corporate Contracts

Third-party Logistics Providers

Government Tenders

Digital Marketplace Platforms

Regional Distribution Networks

- Market Share Analysis

- Cross Comparison Parameters (System Type, Platform Type, Procurement Channel, End User Segment, Fitment Type, Delivery Speed Tier, Automation Level, Urban vs Rural Coverage, Technology Integration, Cold Chain Capability)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

DHL Express Germany

DPD Germany

Hermes Germany

GLS Germany

UPS Germany

FedEx Germany

TNT Express Germany

Amazon Logistics Germany

Go! Express & Logistics

Schumacher Cargo Logistics

Hellmann Worldwide Logistics

Kuehne + Nagel Germany

DB Schenker Germany

Royal Mail Germany Operations

Chronopost Germany

- E-commerce retailers’ reliance on CEP services for timely deliveries

- Food and beverage companies prioritizing temperature-sensitive shipments

- Healthcare providers increasing demand for reliable courier networks

- Government agencies coordinating emergency logistics and document delivery

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now