Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Germany’s cold chain logistics market is valued at approximately USD ~ billion based on a recent historical assessment supported by logistics sector datasets from Statista and Germany Trade & Invest. The market is driven by expanding pharmaceutical manufacturing, strong processed food consumption, and large-scale grocery retail distribution systems that require continuous temperature-controlled transportation and storage infrastructure. Increasing biologic medicine distribution, vaccine logistics, and frozen food supply chains also strengthen the need for advanced refrigerated warehouses, monitoring technologies, and temperature-controlled freight networks across national distribution corridors.

Major logistics activity is concentrated in metropolitan logistics hubs such as Hamburg, Berlin, Frankfurt, Munich, and Cologne due to strong transportation infrastructure and proximity to pharmaceutical manufacturing clusters and food processing industries. These cities host large cold storage facilities, multimodal freight terminals, and pharmaceutical distribution centers connected through dense highway and rail networks. Frankfurt and Hamburg dominate international temperature-controlled trade due to major air cargo hubs and maritime container terminals supporting pharmaceutical exports, seafood imports, and European cold chain distribution networks.

Market Segmentation

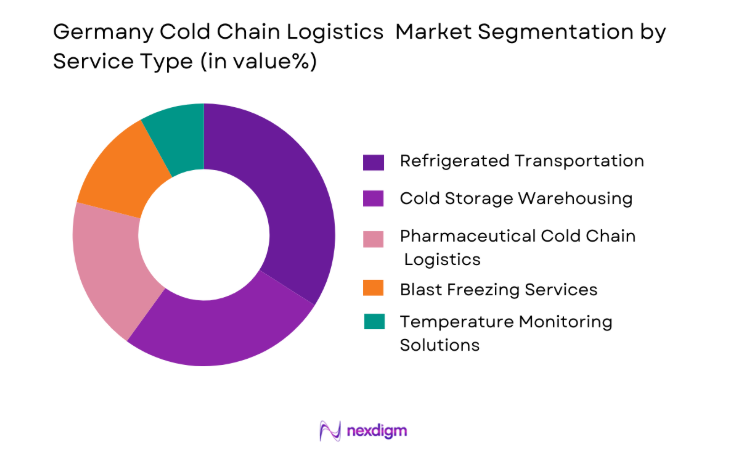

By Service Type

Germany Cold Chain Logistics market is segmented by service type into refrigerated transportation, cold storage warehousing, blast freezing services, pharmaceutical cold chain logistics, and temperature monitoring solutions. Recently, refrigerated transportation has a dominant market share due to extensive movement of temperature-sensitive goods across national supply chains linking food producers, pharmaceutical manufacturers, wholesalers, and retail supermarkets. Germany’s food retail ecosystem requires frequent distribution of dairy products, frozen meals, seafood, and fresh produce through refrigerated trucking fleets. Pharmaceutical logistics also depend on temperature-controlled transport vehicles for biologic medicines and vaccines requiring strict temperature stability during long distance distribution across Europe. The country’s strong export economy further increases refrigerated container transport through ports such as Hamburg and Bremerhaven where temperature-controlled cargo including seafood, meat, and pharmaceuticals are transported internationally. Growth of grocery delivery platforms and organized retail chains also expands last-mile refrigerated transport demand. Logistics providers therefore invest heavily in refrigerated truck fleets, telematics systems, and temperature monitoring technologies to ensure compliance with European food safety and pharmaceutical distribution regulations.

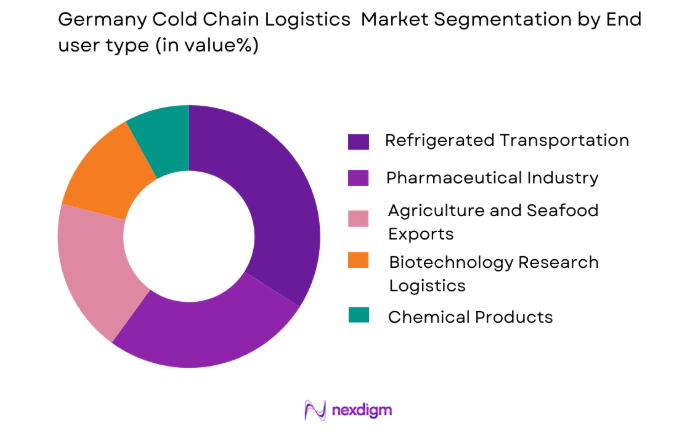

By End-Use Industry

Germany Cold Chain Logistics market is segmented by end-use industry into food and beverage industry, pharmaceutical industry, agriculture and seafood exports, chemical products, and biotechnology research logistics. Recently, the food and beverage industry has a dominant market share due to high domestic consumption of frozen foods, dairy products, processed meats, and packaged grocery items distributed through nationwide supermarket networks. Germany has one of Europe’s largest organized retail sectors with major supermarket chains operating extensive distribution systems requiring large refrigerated warehouses and truck fleets to maintain product quality during transportation. Food manufacturing companies rely heavily on cold storage infrastructure to manage inventory across national logistics hubs before supplying retailers and food service providers. Rapid growth in frozen ready-to-eat meals, dairy logistics, seafood imports, and fresh produce distribution further expands cold chain infrastructure requirements. Major food processing facilities located in Bavaria, North Rhine-Westphalia, and Lower Saxony operate integrated cold storage and distribution networks supplying supermarkets across the country. The need for continuous refrigeration throughout transportation and warehousing therefore reinforces the dominant position of the food industry within the national cold chain logistics ecosystem.

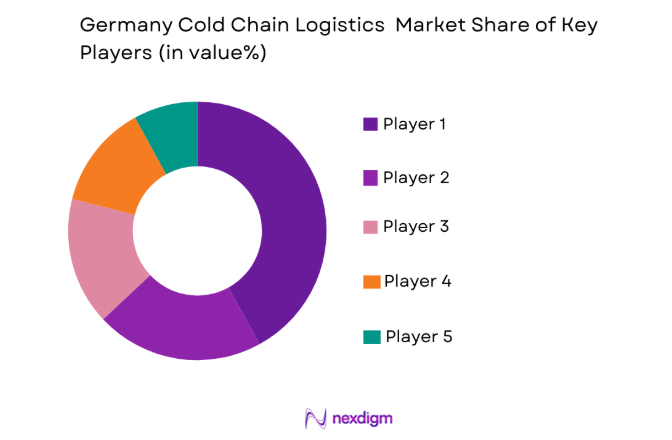

Competitive Landscape

Germany’s cold chain logistics market demonstrates moderate consolidation with a mix of global logistics companies and specialized European refrigerated transport providers. Large international logistics firms operate extensive warehousing networks and multimodal distribution systems connecting pharmaceutical manufacturers and food retailers. Advanced cold storage infrastructure, temperature monitoring technologies, and pharmaceutical distribution certifications create high entry barriers for smaller providers. Major logistics operators compete through technology adoption, network coverage, and integrated supply chain management capabilities.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Cold Storage Capacity |

| DHL Supply Chain | 1969 | Bonn, Germany | ~ | ~ | ~ | ~ | ~ |

| DB Schenker | 1872 | Essen, Germany | ~ | ~ | ~ | ~ | ~ |

| Kuehne + Nagel | 1890 | Schindellegi, Switzerland | ~ | ~ | ~ | ~ | ~ |

| Lineage Logistics | 2008 | Michigan, USA | ~ | ~ | ~ | ~ | ~ |

| Nagel Group | 1935 | Versmold, Germany | ~ | ~ | ~ | ~ | ~ |

Germany Cold Chain Logistics Market Analysis

Growth Drivers

Expansion of Pharmaceutical Biologic Medicine Distribution Networks

Germany’s pharmaceutical sector has become one of the most advanced pharmaceutical manufacturing ecosystems in Europe, generating substantial demand for highly reliable temperature-controlled logistics infrastructure capable of transporting biologic medicines, vaccines, and specialized pharmaceutical treatments across domestic and international healthcare supply chains. The production of monoclonal antibodies, gene therapies, insulin products, and specialty biologic drugs requires strict temperature management throughout transportation and storage processes to preserve therapeutic effectiveness and chemical stability. Pharmaceutical manufacturers rely heavily on validated cold chain logistics providers that maintain certified temperature conditions between production facilities, distribution centers, hospitals, and pharmacies across Germany and neighboring European markets. Advanced pharmaceutical distribution requires specialized refrigerated containers, temperature monitoring systems, and pharmaceutical grade warehouses operating under strict regulatory compliance standards mandated by European Good Distribution Practice guidelines.

Rising Consumption of Frozen Food and Organized Retail Distribution Infrastructure

Germany’s large consumer economy and highly developed retail sector significantly increase demand for reliable cold chain logistics services capable of transporting frozen and perishable food products across extensive national distribution networks connecting manufacturers, wholesalers, supermarkets, and food service establishments. Frozen meals, dairy products, seafood, meat products, and packaged ready to eat foods require continuous refrigeration throughout transportation and storage processes to maintain quality and food safety standards required by European regulatory authorities. Organized retail chains operate nationwide supermarket networks that rely heavily on temperature controlled distribution centers and refrigerated truck fleets capable of replenishing inventory across hundreds of retail outlets every day.

Market Challenges

High Energy Costs Associated with Refrigerated Storage Infrastructure

Cold chain logistics operations require continuous refrigeration across transportation vehicles, warehouse facilities, and distribution centers, making energy consumption one of the most significant operational cost factors affecting the profitability and scalability of cold storage infrastructure across Germany’s logistics ecosystem. Refrigerated warehouses must operate powerful cooling systems capable of maintaining stable temperature ranges necessary for food safety and pharmaceutical product integrity, which leads to extremely high electricity consumption levels compared to conventional storage facilities. Rising electricity prices across European energy markets significantly increase operating costs for cold storage providers, forcing logistics companies to invest heavily in energy efficient refrigeration technologies and advanced insulation infrastructure to reduce power consumption while maintaining required temperature standards.

Complex Regulatory Compliance for Pharmaceutical Cold Chain Distribution

Pharmaceutical logistics operations require extremely strict regulatory compliance frameworks governing the storage and transportation of temperature sensitive medicines, vaccines, and biologic drugs across national and international healthcare supply chains. Cold chain logistics providers operating within pharmaceutical distribution networks must comply with European Union Good Distribution Practice guidelines which require validated temperature controlled transportation systems capable of continuously monitoring environmental conditions during product handling and transit. Pharmaceutical warehouses must maintain detailed documentation, temperature monitoring records, and certified storage environments that guarantee product stability throughout the distribution process. Logistics providers must also undergo frequent regulatory audits conducted by healthcare authorities to ensure adherence to pharmaceutical quality standards and transportation protocols required for handling sensitive medical products.

Opportunities

Expansion of Automated Cold Storage Warehousing Technologies

Logistics companies across Germany increasingly invest in highly automated refrigerated warehouses designed to improve operational efficiency while supporting growing demand for temperature controlled distribution services across food and pharmaceutical supply chains. Automated cold storage facilities utilize robotics enabled pallet handling systems, automated storage retrieval systems, and advanced warehouse management software capable of managing extremely large inventory volumes while minimizing human intervention inside refrigerated environments. Automation technologies reduce operational costs by improving warehouse productivity, optimizing inventory movement, and reducing labor requirements associated with manual cold storage operations.

Growth of Temperature Controlled Pharmaceutical Clinical Trial Logistics

Germany hosts one of Europe’s largest pharmaceutical research and biotechnology ecosystems, creating substantial demand for specialized cold chain logistics services capable of supporting pharmaceutical clinical trials and biomedical research supply chains across hospitals, laboratories, and research institutions. Clinical trial materials including biologic compounds, blood samples, vaccines, and laboratory reagents require extremely strict temperature management throughout transportation and storage processes to maintain scientific validity and product stability. Research institutions and pharmaceutical companies increasingly depend on specialized cold chain logistics providers capable of delivering validated transport systems designed specifically for biomedical research distribution networks.

Future Outlook

Germany’s cold chain logistics market is expected to expand steadily as pharmaceutical manufacturing, food distribution, and biotechnology research continue generating strong demand for temperature controlled logistics infrastructure. Increasing automation within refrigerated warehouses and integration of IoT-based monitoring systems will enhance operational efficiency across logistics networks. Government regulations supporting food safety and pharmaceutical distribution standards will further encourage investment in advanced cold storage facilities. Growth of online grocery retail and pharmaceutical exports will also expand refrigerated transportation demand across European trade corridors.

Major Players

- DHL Supply Chain

- DB Schenker

- Kuehne + Nagel

- Lineage Logistics

- Americold Logistics

- Nagel Group

- DachserLogistics

- Rhenus Logistics

- NewColdAdvanced Cold Logistics

- NordfrostGmbH

- FrigologixGroup

- Maersk Logistics

- XPO Logistics

- TIP Group Refrigerated Logistics

- GEFCO Logistics

Key Target Audience

- Food manufacturing companies

- Pharmaceutical manufacturers

- Biotechnology companies

- Refrigeratedlogisticsproviders

- Cold storage infrastructure developers

- Investments and venture capitalist firms

- Government and regulatory bodies

- Grocery retail chains

Research Methodology

Step 1: Identification of Key Variables

Key market variables including cold storage capacity, refrigerated transport volume, pharmaceutical logistics demand, and food distribution infrastructure were identified. Industry databases, government logistics reports, and supply chain datasets were examined to determine factors influencing market size and operational dynamics.

Step 2: Market Analysis and Construction

The market model was constructed using secondary datasets from logistics industry publications, transportation statistics, and pharmaceutical distribution reports. Cold chain infrastructure capacity, freight movement patterns, and warehouse expansion trends were analyzed to develop a structured industry framework.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts including logistics operators, supply chain analysts, and pharmaceutical distribution specialists were consulted to validate market assumptions. Operational insights regarding warehouse capacity utilization, distribution networks, and regulatory compliance were incorporated to refine analytical conclusions.

Step 4: Research Synthesis and Final Output

All datasets and analytical findings were consolidated into a structured market assessment covering infrastructure development, logistics demand patterns, competitive landscape dynamics, and future investment opportunities within Germany’s temperature controlled logistics ecosystem.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expansion of Pharmaceutical and Biologic Drug Distribution

Growth of Frozen and Processed Food Consumption

Increasing Export of Temperature Sensitive Agricultural Products - Market Challenges

High Energy Costs for Refrigeration Infrastructure

Complex Regulatory Compliance for Pharmaceutical Logistics

Infrastructure Constraints in Long Distance Refrigerated Transport - Market Opportunities

Adoption of IoT Enabled Temperature Monitoring Systems

Expansion of Pharmaceutical Cold Chain Clinical Trial Logistics

Development of Sustainable Energy Efficient Refrigeration Facilities - Trends

Integration of Digital Temperature Monitoring Platforms

Expansion of Automated Cold Storage Warehouses

Growth of Sustainable Refrigeration Technologies - Government Regulations

- SWOT Analysis of Key Competitors

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Refrigerated Transportation Systems

Temperature Controlled Warehousing Systems

Cold Storage Distribution Systems

Pharmaceutical Grade Cold Chain Systems

Integrated Cold Chain Monitoring Systems - By Platform Type (In Value%)

Road Based Refrigerated Logistics

Rail Refrigerated Freight Systems

Air Cargo Cold Chain Platforms

Maritime Refrigerated Container Logistics

Integrated Multimodal Cold Chain Networks - By Fitment Type (In Value%)

Standalone Refrigerated Transport Units

Integrated Cold Storage Facilities

Modular Cold Chain Infrastructure

Mobile Refrigerated Containers

Hybrid Cold Chain Distribution Systems - By EndUser Segment (In Value%)

Food Processing Companies

Pharmaceutical Manufacturers

Biotechnology and Life Sciences Firms

Retail Supermarket Chains

Agricultural Exporters - By Procurement Channel (In Value%)

Direct Logistics Provider Contracts

Third Party Logistics Partnerships

Government and Public Sector Procurement

- Market Share Analysis

- CrossComparison Parameters(Service Portfolio, Cold Storage Capacity, Geographic Distribution Network, Temperature Monitoring Technology, Pharmaceutical Logistics Certification)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Porter’s Five Forces

- Key Players

DHL Supply Chain

DB Schenker

Kuehne + Nagel

Maersk Logistics

Lineage Logistics

Americold Logistics

Nagel Group

Dachser Logistics

Rhenus Logistics

NewCold Advanced Cold Logistics

Nordfrost GmbH

TIP Group Refrigerated Logistics

GEFCO Logistics

XPO Logistics

- Pharmaceutical companies increasingly require validated temperature controlled logistics for biologic medicines

- Food retailers depend on reliable refrigerated distribution to maintain product quality and safety

- Biotechnology firms rely on specialized cold chain logistics for clinical research and vaccine distribution

- Agricultural exporters utilize refrigerated logistics for perishable produce shipments

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now