Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Germany diagnostic laboratories market demonstrates strong structural demand within the healthcare diagnostics ecosystem, supported by advanced healthcare infrastructure and extensive clinical testing utilization. Based on a recent historical assessment, the market value reached approximately USD ~ billion according to healthcare expenditure statistics and laboratory services data published by Statista and the Federal Statistical Office of Germany. Growth is driven by increasing clinical diagnostic testing volumes, expansion of molecular diagnostics, aging population healthcare needs, preventive screening programs, and integration of laboratory automation technologies across hospital networks and private diagnostic chains.

Major demand concentration exists in large metropolitan healthcare clusters including Berlin, Munich, Hamburg, Frankfurt, and Cologne, where advanced hospital systems, university medical centers, and private diagnostic networks operate extensive testing facilities. These cities host major research hospitals, biotechnology clusters, and clinical trial infrastructure that generate significant laboratory testing demand. Strong pharmaceutical research presence and well-established insurance funded healthcare systems further support laboratory service utilization, while regional diagnostic networks expand services to surrounding population centers and outpatient clinics.

Market Segmentation

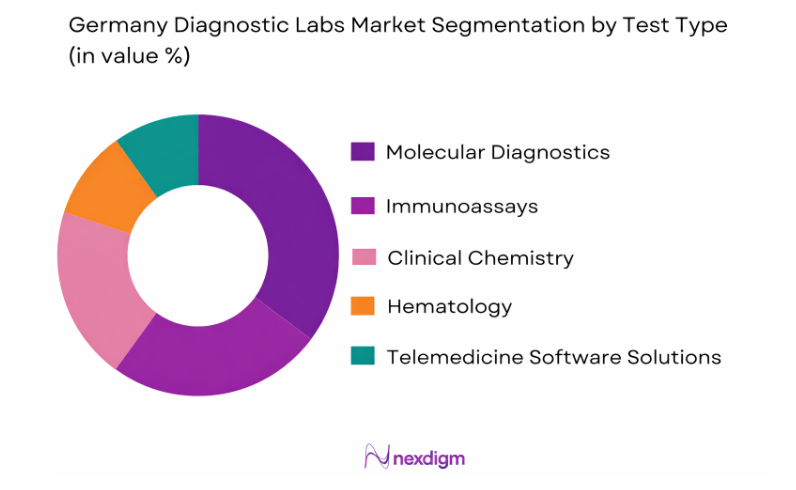

By Test Type

Germany Diagnostic Labs market is segmented by test type into clinical chemistry testing, molecular diagnostics testing, immunoassay diagnostics, hematology diagnostics, and microbiology diagnostics. Recently, clinical chemistry testing has a dominant market share due to its routine utilization across hospitals, diagnostic laboratories, and preventive health screening programs. Clinical chemistry panels including metabolic testing, lipid profiling, liver function testing, and kidney function diagnostics are widely prescribed by physicians for disease monitoring and early detection. Germany’s aging population increases demand for routine chronic disease monitoring, particularly diabetes, cardiovascular conditions, and metabolic disorders. Hospitals and outpatient diagnostic centers perform high volumes of automated clinical chemistry testing daily using high-throughput analyzers. National preventive healthcare initiatives also encourage routine diagnostic screening among adults, further driving test volumes. Additionally, clinical chemistry tests remain comparatively cost efficient and scalable within automated laboratory workflows, allowing laboratories to process large testing volumes efficiently while maintaining standardized diagnostic accuracy.

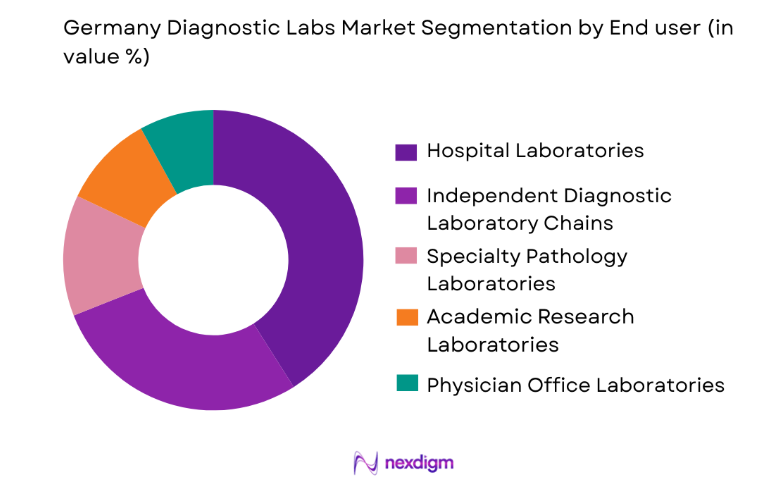

By End User

Germany Diagnostic Labs market is segmented by end user type into hospital laboratories, independent diagnostic laboratory chains, academic research laboratories, specialty pathology laboratories, and physician office laboratories. Recently, hospital laboratories have a dominant market share due to their integration with large healthcare institutions and continuous patient testing demand. Germany maintains a highly developed hospital network that performs both inpatient and outpatient diagnostics, resulting in high laboratory testing volumes. Hospital laboratories support emergency diagnostics, surgical testing requirements, and chronic disease monitoring within centralized medical systems. Advanced hospital diagnostic facilities operate automated analyzers and integrated laboratory information systems enabling efficient testing workflows. Public insurance coverage for hospital-based diagnostics also drives patient utilization. Additionally, university hospitals and tertiary care centers conduct complex testing such as genetic diagnostics and oncology biomarker testing. The strong connection between hospital treatment pathways and diagnostic testing ensures continuous demand, allowing hospital laboratories to maintain the largest share within the national diagnostic ecosystem.

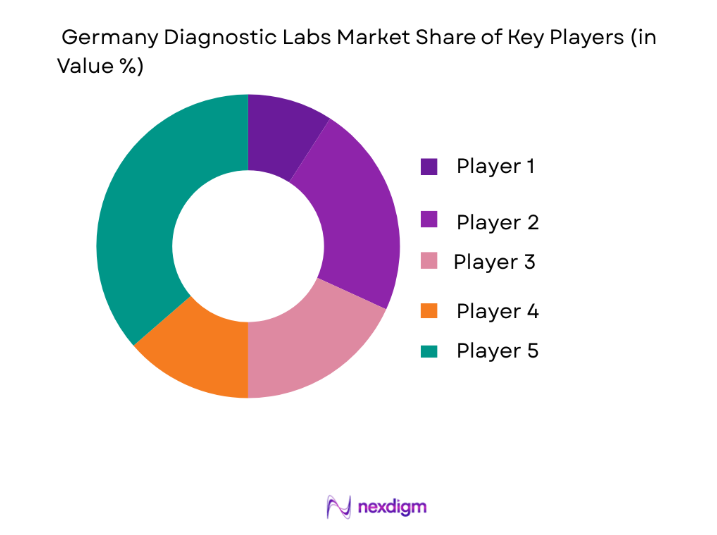

Competitive Landscape

Germany diagnostic laboratories market is moderately consolidated with large multinational diagnostics companies and national laboratory service providers dominating testing infrastructure. Major players operate high-throughput diagnostic networks supported by advanced automation, integrated data systems, and extensive hospital partnerships. Companies such as Roche Diagnostics, Siemens Healthineers, and SYNLAB maintain strong positions through technological innovation and nationwide laboratory networks. Market competition focuses on expanding molecular diagnostics capabilities, laboratory automation systems, and digital pathology platforms while strengthening hospital collaborations and regional testing centers.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Diagnostic Network Size |

| Roche Diagnostics | 1896 | ~ | ~ | ~ | ~ | ~ | ~ |

| Siemens Healthineers | 1847 | ~ | ~ | ~ | ~ | ~ | ~ |

| SYNLAB Group | 1998 | ~ | ~ | ~ | ~ | ~ | ~ |

| Eurofins Scientific | 1987 | ~ | ~ | ~ | ~ | ~ | ~ |

| Sonic Healthcare | 1987 | ~ | ~ | ~ | ~ | ~ | ~ |

Germany Diagnostic Labs Market Analysis

Growth Drivers

Expansion of Preventive Healthcare Screening Programs

Preventive healthcare screening programs across Germany significantly strengthen the demand for diagnostic laboratory services as healthcare providers increasingly emphasize early disease detection and routine health monitoring within the national healthcare system. Physicians encourage individuals to undergo periodic laboratory testing for conditions such as diabetes, cardiovascular diseases, and metabolic disorders to reduce long term healthcare costs and improve patient outcomes. Public health awareness campaigns promote routine screening for cholesterol levels, blood glucose, kidney function, and cancer biomarkers, increasing laboratory test volumes nationwide. Germany’s universal healthcare coverage ensures that many diagnostic tests are reimbursed through statutory health insurance systems, encouraging patients to utilize laboratory services without significant financial barriers. Hospitals and private diagnostic networks expand their testing capabilities to handle the growing number of preventive screening procedures performed annually. Advanced automated laboratory analyzers enable diagnostic facilities to process thousands of routine tests daily with high accuracy and efficiency. The aging demographic profile within the country further contributes to testing demand because older populations require frequent monitoring for chronic disease management. Pharmaceutical companies conducting clinical trials and biomarker studies also contribute to increasing laboratory diagnostic activity within the healthcare ecosystem. As preventive medicine becomes increasingly integrated into national healthcare policy frameworks, diagnostic laboratories continue to experience strong demand for high volume testing services across hospitals, clinics, and independent laboratory networks.

Advancement of Molecular Diagnostics and Precision Medicine Technologies

Rapid technological development in molecular diagnostics and genomic testing strongly accelerates the expansion of diagnostic laboratory services across Germany as healthcare providers adopt advanced testing platforms capable of detecting diseases at the genetic and molecular level. Precision medicine initiatives require detailed laboratory analysis including next generation sequencing, polymerase chain reaction diagnostics, and biomarker identification that enable physicians to design personalized treatment plans for patients. Oncology treatment increasingly relies on molecular profiling to determine targeted therapies, significantly increasing the demand for specialized laboratory testing services. Biotechnology companies collaborate with diagnostic laboratories to develop new biomarker assays that support pharmaceutical research and clinical trial programs. Academic research hospitals and medical universities across Germany conduct extensive genomic research projects that generate substantial laboratory testing requirements. Diagnostic equipment manufacturers introduce highly automated molecular testing systems capable of delivering rapid results with improved analytical sensitivity. These technologies enable laboratories to process complex diagnostic tests efficiently while maintaining standardized clinical accuracy. National healthcare policies also support innovation in precision medicine through research funding and hospital modernization programs. As molecular diagnostics becomes a critical component of modern medical practice, diagnostic laboratories expand their capabilities to support personalized medicine and advanced disease detection across the healthcare system.

Market Challenges

High Operational Costs and Laboratory Infrastructure Investment Requirements

Diagnostic laboratories across Germany face substantial financial pressures due to the high operational costs associated with maintaining advanced laboratory infrastructure, purchasing sophisticated diagnostic equipment, and complying with strict healthcare quality regulations. Modern laboratory analyzers require significant capital investment while also demanding regular maintenance, calibration, and technical upgrades to maintain testing accuracy and reliability. Skilled laboratory technicians, pathologists, and molecular diagnostics specialists are essential for operating complex diagnostic platforms, increasing personnel expenses within diagnostic facilities. Energy consumption, laboratory consumables, reagent costs, and sample handling logistics further contribute to operational expenditures. Laboratories must also invest in digital laboratory information systems that securely manage patient data and integrate diagnostic results with hospital electronic health record systems. Quality assurance programs require laboratories to participate in proficiency testing and accreditation processes that involve additional compliance costs. Independent diagnostic laboratories particularly face financial challenges when competing with hospital laboratories that benefit from integrated healthcare infrastructure and insurance reimbursement systems. Price regulation mechanisms within healthcare reimbursement frameworks may limit the ability of laboratories to pass increased operational costs to patients or healthcare providers. As diagnostic technology continues to evolve rapidly, laboratories must constantly upgrade equipment and adopt new testing platforms to remain competitive in the healthcare market.

Stringent Regulatory Compliance and Diagnostic Quality Standards

Germany diagnostic laboratories operate within a highly regulated healthcare environment where strict quality standards, accreditation requirements, and medical device regulations govern laboratory operations and diagnostic testing procedures. Laboratories must comply with European Union in vitro diagnostic regulations as well as national healthcare quality frameworks that define testing protocols, safety requirements, and clinical validation standards. Accreditation bodies require laboratories to maintain standardized quality management systems, validated testing methodologies, and comprehensive documentation for all diagnostic procedures. Regulatory authorities also monitor laboratory performance through inspections and external quality assurance programs designed to ensure diagnostic reliability and patient safety. Compliance with these regulations requires significant administrative oversight and continuous training for laboratory personnel. Laboratories must maintain secure data management systems to protect patient health information while enabling secure communication with hospitals and healthcare providers. The introduction of new diagnostic technologies often requires extensive clinical validation and regulatory approval processes before laboratories can implement them within routine testing workflows. Smaller laboratories may face difficulties adapting to evolving regulatory requirements due to limited financial and technical resources. Maintaining compliance therefore represents an ongoing operational challenge for diagnostic laboratories operating within the national healthcare system.

Opportunities

Expansion of Genetic Testing and Personalized Medicine Services

The growing integration of genetic testing and personalized medicine within modern healthcare systems creates significant opportunities for diagnostic laboratories across Germany to expand specialized testing services and develop advanced molecular diagnostics capabilities. Physicians increasingly rely on genomic analysis to identify disease susceptibility, predict treatment responses, and personalize therapeutic strategies for patients with complex medical conditions. Oncology treatment in particular benefits from biomarker testing and genomic sequencing that guide targeted therapies and immunotherapy treatments. Diagnostic laboratories collaborate with pharmaceutical companies and biotechnology firms to develop companion diagnostic tests used alongside innovative drug therapies. Research hospitals and academic institutions conduct large scale genomic studies that generate demand for advanced laboratory testing infrastructure and specialized analytical expertise. Healthcare providers also utilize genetic testing for prenatal diagnostics, rare disease identification, and inherited condition screening. The expansion of direct to consumer genetic testing services further increases awareness of personalized medicine among the general population. Diagnostic laboratories capable of offering high accuracy genomic analysis therefore gain competitive advantages in the evolving healthcare diagnostics landscape. As personalized medicine becomes increasingly integrated into clinical practice, diagnostic laboratories are positioned to expand their service portfolios and develop specialized testing capabilities supporting advanced medical research and patient care.

Growth of Digital Laboratory Automation and Artificial Intelligence Diagnostics

The adoption of digital laboratory automation technologies and artificial intelligence driven diagnostics presents major growth opportunities for diagnostic laboratories operating across Germany’s healthcare ecosystem. Automated laboratory systems enable high throughput testing with minimal manual intervention, allowing laboratories to process large volumes of patient samples efficiently while reducing operational errors. Artificial intelligence algorithms assist pathologists and laboratory specialists in analyzing complex diagnostic data such as digital pathology images and genomic sequencing results. These technologies improve diagnostic accuracy and reduce the time required for clinical interpretation of laboratory results. Hospitals increasingly integrate laboratory information systems with digital health records, enabling faster communication of diagnostic results to physicians and healthcare providers. AI based analytics platforms also support predictive healthcare models by identifying patterns within laboratory data that may indicate early disease development. Diagnostic laboratories implementing digital automation technologies can significantly improve operational efficiency and reduce long term costs associated with manual laboratory workflows. Technology companies continue to introduce advanced laboratory robotics and AI driven analytical tools designed specifically for clinical diagnostics. As healthcare systems prioritize efficiency and precision medicine, laboratories adopting digital diagnostic technologies gain opportunities to enhance service capacity and clinical value within the healthcare industry.

Future Outlook

Germany diagnostic laboratories market is expected to expand steadily over the coming years as healthcare systems increasingly emphasize preventive medicine, advanced diagnostics, and personalized treatment strategies. Technological developments including molecular diagnostics, laboratory automation, and artificial intelligence supported pathology are expected to reshape testing infrastructure. Continued regulatory support for quality healthcare services and sustained healthcare expenditure will encourage modernization of diagnostic laboratories. Rising chronic disease prevalence and aging population demographics will further strengthen demand for high-volume diagnostic testing services.

Major Players

- Roche Diagnostics

- Siemens Healthineers

- SYNLAB Group

- Eurofins Scientific

- Sonic Healthcare

- Limbach Gruppe

- AmedesGroup

- LADR Laboratory Group

- MedicoverDiagnostics

- CerbaHealthCare

- BioscientiaHealthcare

- Labor Berlin

- IMD Berlin

- MVZ Labor Dr. Limbach

- SynlabMVZ Leinfelden-Echterdingen

Key Target Audience

- Pharmaceutical and biotechnology companies

- Hospital and healthcare system operators

- Diagnostic laboratory service providers

- Medical device manufacturers

- Investments and venture capitalist firms

- Government and regulatory bodies

- Healthcare insurance providers

- Private healthcare infrastructure investors

Research Methodology

Step 1: Identification of Key Variables

The research begins by identifying major market variables including diagnostic testing volume, laboratory infrastructure capacity, technology adoption rates, and healthcare expenditure patterns. Key indicators affecting diagnostic laboratory demand are evaluated through healthcare databases, regulatory publications, and hospital service utilization data.

Step 2: Market Analysis and Construction

Market size and segmentation are constructed through analysis of diagnostic service revenues, laboratory testing volumes, and healthcare utilization statistics. Public healthcare expenditure reports, diagnostic equipment sales data, and laboratory service provider financial disclosures are integrated to establish market structure.

Step 3: Hypothesis Validation and Expert Consultation

Preliminary findings are validated through consultation with laboratory professionals, diagnostic equipment manufacturers, healthcare administrators, and biotechnology researchers. Expert feedback ensures the research framework accurately reflects operational realities within the diagnostic laboratory industry.

Step 4: Research Synthesis and Final Output

The final stage integrates quantitative healthcare data with qualitative industry insights to produce a comprehensive assessment of the diagnostic laboratories market. Analytical models are used to evaluate structural trends, technological developments, and competitive dynamics influencing future market development.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Rising Demand for Early Disease Detection and Preventive Diagnostics

Expansion of Private Diagnostic Laboratory Networks

Growing Adoption of Molecular and Genetic Testing Technologies - Market Challenges

High Operational Costs for Advanced Laboratory Infrastructure

Regulatory Compliance and Quality Certification Requirements

Shortage of Skilled Laboratory Technologists - Market Opportunities

Expansion of Precision Medicine and Genetic Testing Services

Integration of Artificial Intelligence in Laboratory Diagnostics

Growth of Home-Based and Remote Diagnostic Testing - Trends

Automation of Laboratory Workflows and Digital Pathology Adoption

Increasing Utilization of Next Generation Sequencing Diagnostics

Expansion of Integrated Laboratory Information Management Systems - Government Regulations

- SWOT Analysis of Key Competitors

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Clinical Chemistry Testing Systems

Immunoassay Diagnostic Systems

Molecular Diagnostic Systems

Hematology Diagnostic Systems

Microbiology Testing Systems - By Platform Type (In Value%)

Central Laboratory Diagnostic Platforms

Point-of-Care Diagnostic Platforms

Automated High-Throughput Laboratory Platforms

Integrated Laboratory Information Systems Platforms

Cloud-Enabled Diagnostic Data Platforms - By Fitment Type (In Value%)

Standalone Laboratory Testing Systems

Integrated Hospital Laboratory Systems

Modular Diagnostic Laboratory Systems

Portable Diagnostic Testing Units

Networked Laboratory Automation Systems - By EndUser Segment (In Value%)

Public Hospital Laboratories

Private Diagnostic Laboratory Chains

Academic and Research Laboratories

Specialized Pathology Laboratories

Primary Care Diagnostic Centers - By Procurement Channel (In Value%)

Direct Procurement from Diagnostic Manufacturers

Hospital Group Procurement Contracts

Government Healthcare Procurement Programs

- Market Share Analysis

- Cross Comparison Parameters (Diagnostic Test Portfolio, Automation Capability, Laboratory Network Coverage, Pricing Strategy, Technology Integration)

SWOT Analysis of Key Competitors

Pricing & Procurement Analysis

Key Players - Roche Diagnostics

Siemens Healthineers

SYNLAB Group

Limbach Gruppe

Eurofins Scientific

Amedes Group

BIOSCIENTIA Healthcare

Cerba HealthCare

Sonic Healthcare Germany

Labor Berlin

MVZ Labor Dr. Limbach

Synlab MVZ Leinfelden-Echterdingen

LADR Laboratory Group

Medicover Diagnostics

IMD Berlin

- Hospitals Increasing Investment in Integrated Laboratory Infrastructure

- Private Diagnostic Chains Expanding High Throughput Testing Capacity

- Research Institutes Driving Advanced Genomic and Molecular Diagnostics

- Primary Care Providers Increasing Use of Preventive Laboratory Screening

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now