Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Germany Digital Health Market is projected to experience steady growth driven by substantial investments in healthcare technology, the increasing adoption of digital health solutions, and regulatory support. Based on a recent historical assessment, the market size for digital health in Germany is valued at approximately USD ~ billion, with healthcare providers and patients actively integrating electronic health records, telemedicine solutions, and mobile health applications. This market is expected to expand as digital transformation accelerates within the healthcare sector. Germany’s highly advanced healthcare system, coupled with favorable government policies, has created an environment ripe for market growth.

Dominant players in the Germany Digital Health Market are primarily located in large urban hubs such as Berlin, Munich, and Hamburg, with Berlin leading the charge as a technology hub. These cities are home to key healthcare providers, digital health startups, and technology firms that drive innovation and foster collaboration between the public and private sectors. Germany’s established infrastructure and strong regulatory frameworks for digital health create favorable conditions for sustained market dominance, positioning these cities as central to market expansion in the coming years.

Market Segmentation

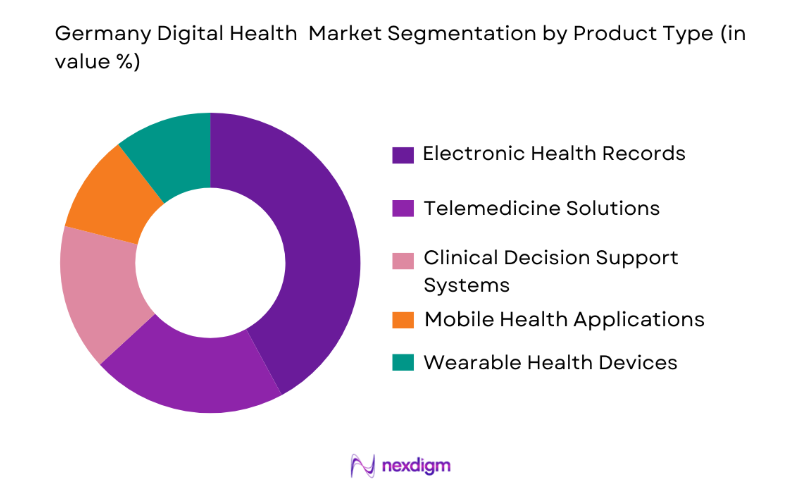

By Product Type

Germany’s digital health market is segmented by product type into electronic health records, telemedicine solutions, clinical decision support systems, mobile health applications, and wearable health devices. The dominant product type, electronic health records, has a significant market share due to increased government initiatives, widespread adoption by healthcare institutions, and rising patient data management needs. The demand for electronic health records is largely driven by the need for improved data accuracy, interoperability, and efficient healthcare delivery, which ultimately leads to better patient care outcomes.

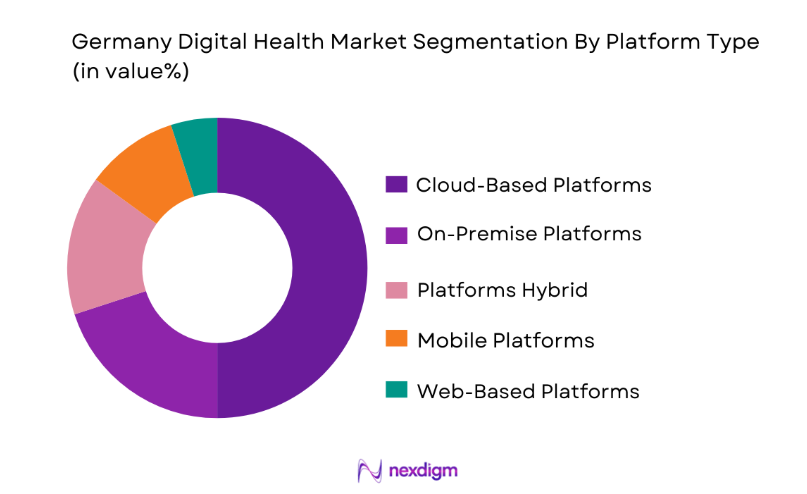

By Platform Type

The market is segmented by platform type into cloud-based platforms, on-premise platforms, hybrid platforms, mobile platforms, and web-based platforms. Cloud-based platforms dominate the Germany digital health market as they offer scalability, reduced IT infrastructure costs, and better integration across healthcare systems. The growing demand for flexible, remote access to health services, particularly in the wake of the COVID-19 pandemic, has driven the adoption of cloud platforms, making them the leading choice for healthcare providers and patients alike.

Competitive Landscape

The competitive landscape of the Germany Digital Health Market is marked by the consolidation of large players offering a wide range of healthcare solutions and digital platforms. Major firms, including Siemens Healthineers, SAP, and Philips Healthcare, are leading market innovation, often through strategic partnerships and acquisitions. The presence of both international giants and local startups drives competition, encouraging technological advancements and increasing accessibility to digital health solutions across Germany.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD) | Additional Parameter |

| Siemens Healthineers | 1847 | Erlangen, Germany | ~ | ~ | ~ | ~ | ~ |

| SAP | 1972 | Walldorf, Germany | ~ | ~ | ~ | ~ | ~ |

| Philips Healthcare | 1891 | Amsterdam, NL | ~ | ~ | ~ | ~ | ~ |

| GE Healthcare | 1892 | Chicago, USA | ~ | ~ | ~ | ~ | ~ |

| Medtronic | 1949 | Dublin, Ireland | ~ | ~ | ~ | ~ | ~ |

Germany Digital Health Market Analysis

Growth Drivers

Government Investments in Healthcare Digitization

Germany’s government has significantly bolstered the healthcare sector by investing in digital health technologies, creating a favorable environment for market growth. As part of its Digital Health Act, Germany has implemented reforms to ensure the integration of digital tools in healthcare settings, providing funding for electronic health records, telemedicine services, and AI applications. This government backing has encouraged healthcare providers to adopt digital solutions, ultimately streamlining workflows, improving patient care, and lowering costs. Moreover, the legal framework for reimbursing telemedicine services and other digital health tools incentivizes further adoption, particularly in rural and underserved areas. Germany’s strong regulatory support for healthcare technologies positions it as a leader in digital health transformation, further driving the market’s expansion.

Technological Advancements in HealthTech

The integration of cutting-edge technologies such as artificial intelligence, machine learning, and the Internet of Things in the healthcare sector has emerged as a primary growth driver for the digital health market in Germany. These technologies are revolutionizing diagnostic procedures, enabling better decision-making, and enhancing operational efficiencies. AI-powered solutions are being increasingly used to analyze patient data for predictive insights, while IoT-enabled devices offer continuous monitoring of vital health parameters. These innovations improve both the quality and accessibility of healthcare services, supporting the growing demand for remote monitoring, personalized medicine, and telehealth. As these technologies mature and their applications expand, Germany is poised to see further advancements in digital health that enhance both patient outcomes and healthcare system efficiency.

Market Challenges

Data Privacy and Cybersecurity Risks

One of the major challenges facing the Germany Digital Health Market is ensuring the protection of sensitive patient data in an increasingly digital healthcare environment. As digital health solutions proliferate, the risk of cyberattacks and data breaches also grows. Germany’s strict data privacy laws, such as the General Data Protection Regulation (GDPR), require healthcare providers to adhere to rigorous standards when handling patient data. However, despite these regulations, the rapid growth of digital health solutions and the interconnectedness of healthcare systems increase the vulnerability to cyber threats. As a result, healthcare providers must invest heavily in cybersecurity infrastructure, which can lead to higher operational costs and a potential slowdown in digital health adoption, particularly among smaller institutions.

Regulatory Hurdles and Slow Adoption of Digital Health Tools

Despite the strong government push for digital health adoption, regulatory hurdles remain a significant challenge in Germany. Healthcare providers are often hesitant to adopt new technologies due to complex and lengthy approval processes, particularly for telemedicine and AI-based solutions. While the German government has made strides in implementing regulations to facilitate the integration of digital health, healthcare providers still face challenges navigating through these regulations, particularly when dealing with cross-border data and international partnerships. The slow pace of regulatory approval and integration can result in delays in market entry, limiting the growth potential of innovative digital health solutions in Germany.

Opportunities

Telemedicine Expansion

The demand for telemedicine services in Germany has surged, fueled by the need for remote consultations and the convenience of accessing healthcare services from home. The German government’s reimbursement policy for telemedicine services has played a key role in encouraging healthcare providers to offer virtual consultations, particularly in rural areas. As more patients and healthcare providers embrace telemedicine, the potential for market growth is substantial, especially with the continued development of telemedicine platforms and the integration of AI-powered diagnostic tools. The expanding telemedicine infrastructure presents significant opportunities for market players to capitalize on growing consumer demand for accessible healthcare solutions.

AI and Big Data Integration

The integration of AI and big data analytics in the German healthcare system presents another key opportunity for digital health market expansion. AI solutions, combined with large-scale data analysis, offer healthcare providers the ability to deliver personalized treatments, predict health outcomes, and enhance diagnostic accuracy. Germany’s strong commitment to AI research and development in healthcare positions it as a leader in this field, creating opportunities for innovation and the development of new healthcare technologies. As the adoption of AI-driven healthcare tools increases, the demand for big data analytics platforms and AI solutions in digital health will continue to grow, opening up avenues for both startups and established players to thrive in this market.

Future Outlook

The future outlook for the Germany Digital Health Market over the next five years appears promising, with steady growth projected due to technological advancements and ongoing regulatory support. As the demand for remote healthcare services, telemedicine, and AI-driven solutions increases, market players are expected to capitalize on emerging opportunities in these sectors. Furthermore, government investments in healthcare digitization and the expansion of digital health infrastructure will provide a solid foundation for long-term market growth. The integration of big data analytics, AI, and IoT in healthcare is set to enhance patient care, reduce costs, and streamline healthcare operations, fueling the market’s progress.

Major Players

- Siemens Healthineers

- SAP

- Philips Healthcare

- GE Healthcare

- Medtronic

- Cerner Corporation

- Allscripts Healthcare Solutions

- IBM Watson Health

- Optum

- Honeywell Life Care Solutions

- Dell Technologies

- Bosch Healthcare Solutions

- Abbott Laboratories

- Oracle

- Google Health

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Hospitals and healthcare providers

- Pharmaceutical companies

- Insurance companies

- Medical device manufacturers

- Healthcare IT service providers

- Healthcare-focused NGOs

Research Methodology

Step 1: Identification of Key Variables

In this step, key variables such as market size, growth rate, and market trends are identified based on available data and industry insights.

Step 2: Market Analysis and Construction

Market analysis is performed by segmenting the data, identifying key players, and understanding the demand and supply dynamics in the digital health sector.

Step 3: Hypothesis Validation and Expert Consultation

Hypotheses formed during the market analysis are validated through consultation with industry experts and key stakeholders in the healthcare and technology sectors.

Step 4: Research Synthesis and Final Output

After collecting and validating data, the final research findings are synthesized and presented in a comprehensive market report, ready for dissemination.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Increased Government Investments in Digital Healthcare

Rising Demand for Remote Healthcare Solutions

Technological Advancements in AI and Big Data - Market Challenges

Cybersecurity Concerns

Regulatory Hurdles in Data Privacy

High Initial Investment for Healthcare Providers - Market Opportunities

Expansion of Telemedicine Services

Integration of AI and Machine Learning in Healthcare

Growth of Mobile Health Applications - Trends

Rise in Use of Artificial Intelligence in Healthcare

Increased Adoption of Mobile Health Devices

Integration of IoT in Healthcare Monitoring - Government Regulations

Data Protection and Privacy Regulations

Government Funding and Grants for Digital Health

Telemedicine Regulatory Policies

- By Market Value, 2020, 2025

- By Installed Units, 2020, 2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Electronic Health Records

Telemedicine Solutions

Clinical Decision Support Systems

Mobile Health Applications

Wearable Health Devices - By Platform Type (In Value%)

Cloud-Based Platforms

On-Premise Platforms

Hybrid Platforms

Mobile Platforms

Web-Based Platforms - By Fitment Type (In Value%)

On-Premise Solutions

Cloud-Based Solutions

Hybrid Solutions

Modular Solutions

Integrated Solutions - By End User Segment (In Value%)

Hospitals

Healthcare Providers

Government Health Agencies

Insurance Companies

- Market Share Analysis

- Cross Comparison Parameters (System Type, Platform Type, End User Segment, Procurement Channel, Fitment Type)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Porter’s Five Forces

- Key Players

Siemens Healthineers

SAP

Philips Healthcare

GE Healthcare

Cerner Corporation

Allscripts Healthcare Solutions

Medtronic

IBM Watson Health

Huawei Technologies

Vodafone Group

Vodacom

DXC Technology

Optum

Intel Corporation

Amazon Web Services

- Increasing Demand from Healthcare Providers for Digital Solutions

- Adoption of Telemedicine by Insurance Companies

- Growing Role of Government Health Agencies in Digital Health

- Rise in Mobile Health Applications among Pharmaceutical Companies

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now