Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, Germany’s home finance market represents outstanding residential mortgage loans totaling approximately USD ~ trillion, as reported by the Deutsche Bundesbank. The market is driven by stable household savings, strong banking sector capitalization, and long-term fixed-rate mortgage structures. Demand is supported by urban housing needs, demographic shifts, and refinancing activity within a regulated lending framework that emphasizes prudent underwriting and borrower affordability standards.

Berlin, Munich, Frankfurt, and Hamburg remain dominant urban centers within the Germany Home Finance Market due to higher property valuations, dense employment clusters, and strong rental-to-ownership transition trends. Southern Germany benefits from industrial income stability, while western regions maintain mature housing finance ecosystems. Cross-border capital flows within the European Union and strong domestic banking networks reinforce liquidity availability, supported by digital mortgage processing infrastructure and transparent regulatory supervision.

Market Segmentation

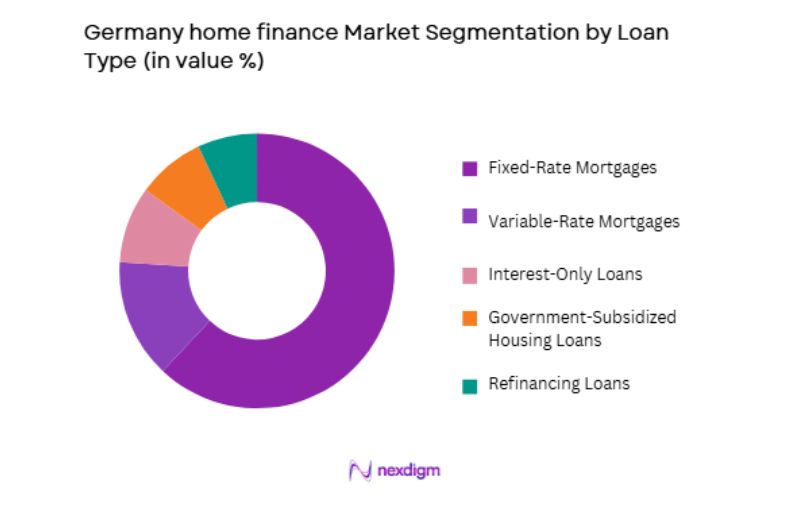

By Loan Type (In Value%)

Germany Home Finance Market is segmented by product type into Fixed-Rate Mortgages, Variable-Rate Mortgages, Interest-Only Loans, Government-Subsidized Housing Loans, and Refinancing Loans. Recently, Fixed-Rate Mortgages have a dominant market share due to factors such as borrower preference for repayment stability, long-term interest rate certainty, conservative lending standards, and strong institutional funding structures provided by German savings banks and mortgage banks, which prioritize predictable cash flows and risk mitigation within a regulated housing finance ecosystem.

By Lender Type (In Value%)

Germany Home Finance Market is segmented by product type into Private Commercial Banks, Savings Banks (Sparkassen), Cooperative Banks, Mortgage Banks, and Digital Lenders. Recently, Savings Banks (Sparkassen) have a dominant market share due to factors such as strong regional presence, public-sector backing, extensive branch networks, established customer trust, and competitive mortgage products tailored to local housing markets, supported by prudent risk assessment frameworks and long-standing retail banking relationships across Germany.

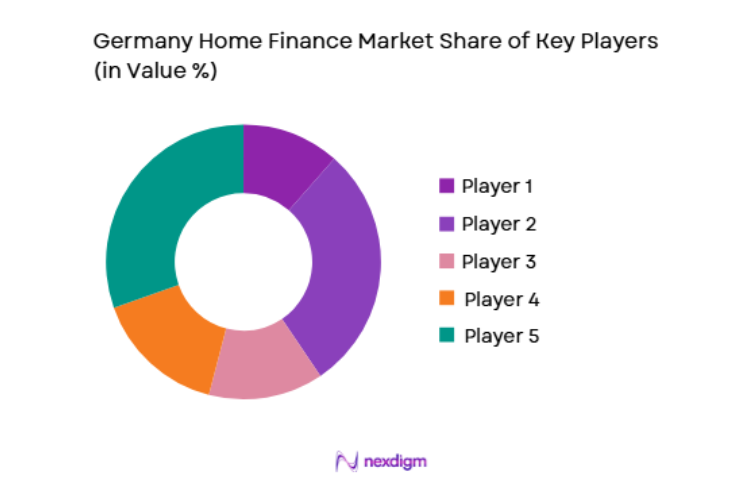

Competitive Landscape

The Germany Home Finance Market is characterized by a highly structured banking environment dominated by savings banks, cooperative institutions, and major commercial banks. Market concentration is moderate, with regional institutions holding strong customer relationships and nationwide banks leveraging digital platforms for scalability. Competition focuses on interest rate competitiveness, loan tenure flexibility, digital mortgage processing, and regulatory compliance, supported by conservative risk management practices embedded within Germany’s financial system.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD) | Mortgage Loan Book (USD) |

| Deutsche Bank | 1870 | Frankfurt, Germany | ~ | ~ | ~ | ~ | ~ |

| Commerzbank | 1870 | Frankfurt, Germany | ~ | ~ | ~ | ~ | ~ |

| KfW Bankengruppe | 1948 | Frankfurt, Germany | ~ | ~ | ~ | ~ | ~ |

| DZ Bank | 2001 | Frankfurt, Germany | ~ | ~ | ~ | ~ | ~ |

| Sparkassen-Finanzgruppe | 1900 | Berlin, Germany | ~ | ~ | ~ | ~ | ~ |

Germany Home Finance Market Analysis

Growth Drivers

Urbanization and Housing Demand in Major Metropolitan Regions

Germany’s sustained urban concentration in cities such as Berlin, Munich, and Frankfurt continues to drive structural demand for residential mortgage financing as employment opportunities, education infrastructure, and industrial growth remain concentrated in metropolitan corridors. Rising property valuations in urban districts increase the absolute financing requirement per transaction, thereby expanding total mortgage volumes even in periods of moderate transaction activity. Stable labor markets and comparatively low unemployment levels support borrower creditworthiness and enhance repayment capacity, reinforcing lender confidence. Long-term fixed-rate structures provide predictability to households planning property acquisition in high-cost urban environments. Strong rental markets also encourage tenants to transition toward ownership, particularly in economically resilient regions. Infrastructure development projects and public transportation investments enhance peripheral housing demand, expanding financed property areas. Conservative underwriting standards ensure controlled risk exposure while maintaining credit expansion. Germany’s savings-oriented financial culture supports down payment accumulation, facilitating mortgage qualification. Together, these metropolitan demand drivers provide consistent structural support to the home finance ecosystem.

Stable Long-Term Fixed Interest Rate Framework and Conservative Lending Standards

Germany’s home finance structure is distinguished by long-term fixed-rate mortgage contracts that often extend beyond ten years, offering borrowers repayment certainty and shielding them from short-term interest rate volatility. This structural characteristic enhances household financial planning stability and reduces default risk, contributing to overall banking sector resilience. Conservative loan-to-value ratios and rigorous credit assessment procedures strengthen asset quality within mortgage portfolios. Institutional investors favor German covered bonds, or Pfandbriefe, which provide stable funding channels for mortgage lenders. Strong capital adequacy ratios across major banks enable sustained credit provision even during macroeconomic fluctuations. Regulatory supervision by BaFin reinforces prudent risk management and transparency in lending practices. Refinancing cycles remain orderly due to structured amortization profiles embedded in loan contracts. Borrower confidence in stable repayment conditions sustains demand across income segments. This conservative yet scalable framework remains a foundational growth engine for the Germany Home Finance Market.

Market Challenges

Interest Rate Volatility and Borrower Affordability Constraints

Germany’s home finance market faces challenges associated with shifts in European monetary policy that influence benchmark lending rates and refinancing costs. Rising interest rates increase monthly repayment obligations for new borrowers and reduce overall loan eligibility under affordability calculations. Higher financing costs may suppress transaction volumes in high-priced urban property markets. First-time buyers face increased entry barriers when combined with elevated property valuations. Lenders must recalibrate credit scoring models to incorporate macroeconomic uncertainty and income sensitivity analysis. Refinancing activity may decline when existing borrowers hold lower fixed-rate contracts, limiting new loan origination growth. Banks must manage interest rate risk exposure across long-duration fixed portfolios. Housing demand elasticity becomes more sensitive to monetary policy changes. Investor appetite for mortgage-backed instruments may fluctuate under changing yield environments. These factors collectively create cyclical pressure on loan origination volumes and margin stability.

Regulatory Capital Requirements and Prudential Oversight Complexity

Germany’s home finance market operates under stringent European Union banking regulations that require robust capital buffers and detailed risk reporting standards. Basel III and related supervisory frameworks impose capital allocation requirements that influence lending capacity and profitability. Enhanced stress testing procedures require banks to model adverse housing price scenarios and macroeconomic shocks. Compliance with consumer protection standards increases administrative processes within mortgage approval workflows. Smaller regional institutions may face disproportionate compliance costs relative to scale. Ongoing digital security requirements add investment obligations in cybersecurity infrastructure. Data privacy regulations necessitate secure borrower data management systems. Reporting transparency expectations increase operational overhead. Regulatory evolution related to sustainable housing finance adds further disclosure complexity. These structural compliance factors raise cost bases while limiting aggressive credit expansion strategies.

Opportunities

Expansion of Green and Energy-Efficient Mortgage Financing Programs

Germany’s commitment to climate neutrality creates significant opportunities for green mortgage products that finance energy-efficient housing and renovation projects. Government-backed incentives and subsidies encourage borrowers to upgrade insulation, heating systems, and renewable energy installations. Financial institutions can structure preferential loan rates linked to energy performance certification standards. Demand for sustainable housing increases among environmentally conscious homeowners. Banks can collaborate with public development institutions to co-finance eco-friendly housing initiatives. Integration of environmental risk assessment into property valuation strengthens long-term asset resilience. Green covered bonds attract institutional capital aligned with sustainability mandates. Enhanced reporting transparency supports investor confidence in environmentally aligned portfolios. Digital monitoring of energy efficiency metrics improves loan performance evaluation. This transition toward sustainable housing finance presents scalable growth potential within regulatory frameworks.

Digital Mortgage Processing and Fintech Collaboration Models

The increasing adoption of digital mortgage application platforms offers operational efficiency improvements across origination, underwriting, and documentation processes. Online verification systems reduce processing time and enhance borrower convenience. Fintech partnerships enable automated credit scoring, digital identity verification, and electronic contract management. Remote advisory services expand geographic reach beyond branch-based distribution models. Data analytics improve risk profiling and personalized product offerings. Digital ecosystems facilitate integration with property valuation databases and notary services. Cost efficiencies achieved through automation support competitive interest pricing. Younger borrower segments show strong preference for seamless digital experiences. Secure cloud infrastructure enhances scalability and compliance reporting. The convergence of traditional banking expertise and fintech innovation presents a transformative opportunity within Germany’s home finance landscape.

Future Outlook

Over the next five years, the Germany Home Finance Market is expected to maintain structural stability supported by conservative lending standards and gradual digital transformation. Green housing initiatives and energy-efficient mortgage programs are anticipated to expand lending categories. Regulatory oversight will continue to ensure prudential stability while encouraging sustainable finance integration. Demand in metropolitan regions and digital mortgage adoption are likely to shape competitive differentiation and long-term market resilience.

Major Players

- Deutsche Bank

- Commerzbank

- Sparkassen-Finanzgruppe

- DZ Bank

- KfW Bankengruppe

- ING-DiBa

- HypoVereinsbank

- Landesbank Baden-Württemberg

- BayernLB

- Deutsche Pfandbriefbank

- Aareal Bank

- Münchener Hypothekenbank

- Berlin Hyp

- BHW Bausparkasse

- Wüstenrot Bausparkasse

Key Target Audience

- Residential mortgage borrowers

- First-time home buyers

- Property refinancing customers

- Real estate developers

- Housing cooperatives

- Institutional property investors

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

Key variables including outstanding mortgage volumes, lender categories, loan structures, and regulatory parameters were identified using central bank publications and financial disclosures. Macroeconomic housing indicators and demographic data were incorporated to define the structural scope of analysis.

Step 2: Market Analysis and Construction

Market size was constructed using official Bundesbank mortgage statistics and institutional financial reports. Segmentation was developed by mapping loan types and lender categories within Germany’s regulated banking ecosystem.

Step 3: Hypothesis Validation and Expert Consultation

Assumptions were validated through consultation with banking analysts, housing finance specialists, and regulatory professionals. Cross-verification ensured consistency between reported loan books and supervisory data.

Step 4: Research Synthesis and Final Output

Quantitative findings and qualitative insights were synthesized into a structured analytical framework. Final outputs were reviewed for factual accuracy, regulatory alignment, and logical coherence prior to report consolidation.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Low Interest Rate Environment Supporting Borrowing Demand

Urban Housing Demand in Major German Cities

Government Incentives for Energy Efficient Housing Finance - Market Challenges

Stringent Lending Regulations and Credit Assessment Norms

Rising Property Prices Impacting Affordability

Macroeconomic Uncertainty Affecting Borrower Confidence - Market Opportunities

Expansion of Green Mortgage Financing Products

Digital Mortgage Processing and Automation

Cross Border Lending within the European Union - Trends

Adoption of End to End Digital Mortgage Journeys

Increasing Demand for Sustainable and Energy Efficient Home Financing - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Residential Mortgage Loans

Home Equity Loans

Building Society Savings Contracts

Refinancing and Remortgage Products

Government Subsidized Housing Loans - By Platform Type (In Value%)

Branch Based Lending

Online Direct Lending Platforms

Mortgage Broker Networks

Mobile Banking Applications

Fintech Aggregator Platforms - By Fitment Type (In Value%)

Fixed Interest Rate Loans

Variable Interest Rate Loans

Hybrid Rate Mortgage Products

Balloon Payment Structures - By End User Segment (In Value%)

First Time Home Buyers

Property Investors

Self Employed Borrowers

- Market Share Analysis

- Cross Comparison Parameters (Interest Rate Structure, Loan Tenure, Loan to Value Ratio, Processing Time, Digital Integration Level)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Deutsche Bank AG

Commerzbank AG

DZ Bank AG

KfW Bankengruppe

ING DiBa AG

HypoVereinsbank

Sparkassen Finanzgruppe

Volksbanken Raiffeisenbanken

Santander Consumer Bank AG

Bausparkasse Schwabisch Hall

Wustenrot Bausparkasse

Postbank AG

Berlin Hyp AG

Aareal Bank AG

DSL Bank

- Rising Preference for Long Term Fixed Rate Mortgages among Households

- Growing Participation of Institutional Investors in Residential Real Estate

- Increasing Demand for Flexible Repayment Options among Self Employed Borrowers

- Higher Credit Scrutiny for First Time Buyers

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now