Download PDF

Download PDF Download PDF

Download PDFMarket Overview

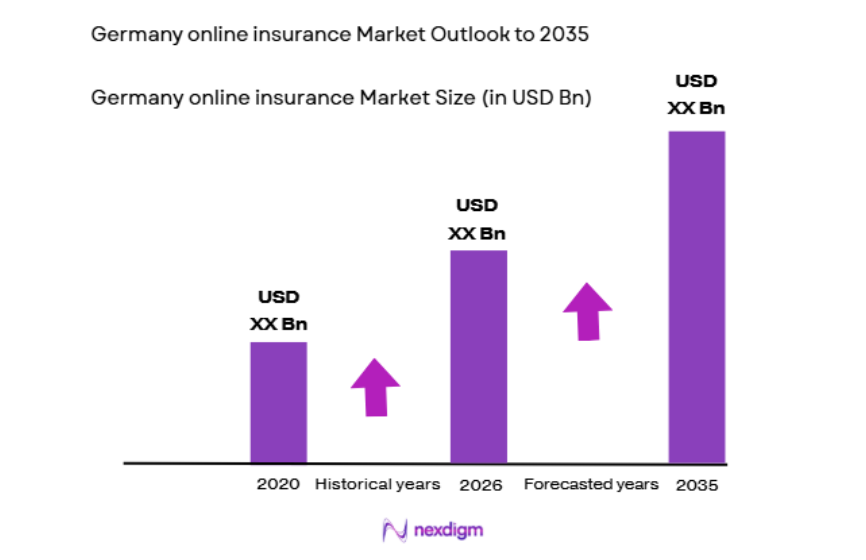

Germany online insurance market generated approximately USD ~ billion in digitally originated gross written premiums, based on a recent historical assessment of federal financial supervisory authority statistics and insurer disclosures. Growth is driven by widespread internet penetration, digital insurer platforms, and comparison portals across motor, health supplemental, and household insurance lines. Automated underwriting, electronic policy management, and online claims servicing reduce distribution costs and encourage insurers and consumers to shift toward direct digital purchase and servicing channels.

Berlin, Munich, and Hamburg dominate the Germany online insurance market due to dense insured populations, concentration of insurers and insurtech firms, and advanced digital finance ecosystems supporting seamless online policy purchase and servicing. Frankfurt contributes through financial sector employment and corporate insurance demand. Nationwide digital uptake is reinforced by strong broadband infrastructure, established comparison websites, and regulatory acceptance of electronic documentation and remote identity verification across federal states and urban centers.

Market Segmentation

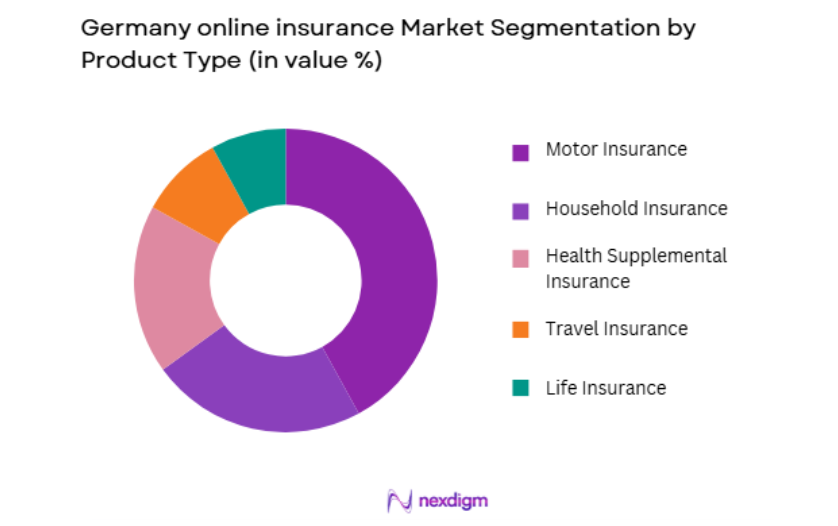

By Product Type

Germany online insurance market is segmented by product type into motor insurance, household insurance, health supplemental insurance, travel insurance, and life insurance. Recently, motor insurance has a dominant market share due to factors such as mandatory vehicle liability requirements, high vehicle ownership, and standardized policy structures suited to digital comparison and purchase. Motor insurance products are highly commoditized and easily quoted online, enabling efficient distribution through insurer websites and aggregators. Frequent renewal cycles and switching behavior reinforce digital engagement. Insurers prioritize online motor distribution because underwriting and claims data are structured and automation-friendly. Consumers increasingly prefer self-service policy management and claims reporting through digital interfaces.

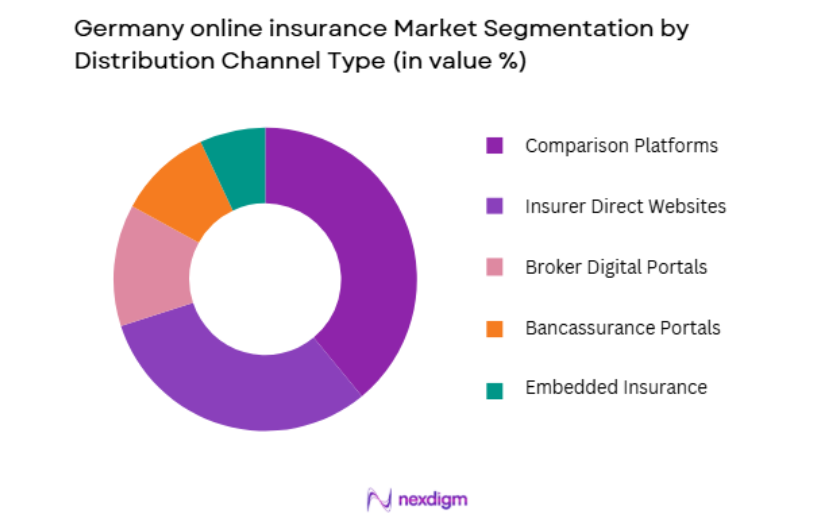

By Distribution Channel

Germany online insurance market is segmented by distribution channel into comparison platforms, insurer direct websites, broker digital portals, bancassurance portals, and embedded insurance channels. Recently, comparison platforms has a dominant market share due to factors such as strong consumer price sensitivity, well-established aggregator culture, and trust in independent comparison services. German consumers frequently use comparison portals to evaluate insurers and pricing before purchase, particularly in motor and household lines. Insurers depend on these portals for online customer acquisition and competitive visibility. Digital search behavior often directs consumers first to comparison sites rather than insurer websites. Comparison portals also support policy switching and renewal reminders.

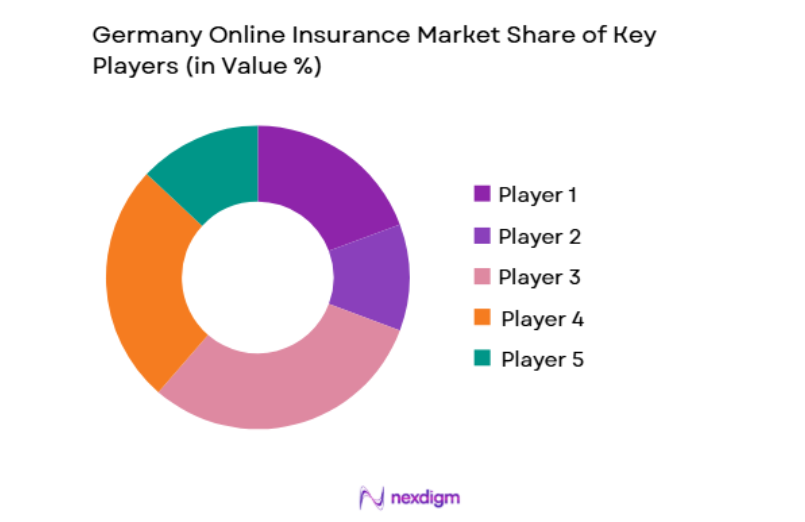

Competitive Landscape

The Germany online insurance market is moderately consolidated among large composite insurers and digital-first brands operating extensive direct online and comparison-driven distribution. Competition centers on pricing, user experience, and aggregator visibility. Traditional insurers leverage brand trust and underwriting scale, while insurtech firms focus on simplified digital products and direct acquisition. Comparison portals strongly influence customer switching and pricing dynamics across online personal insurance lines.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Online Policy Share |

| Allianz Deutschland | 1890 | Munich | ~ | ~ | ~ | ~ | ~ |

| HUK-Coburg | 1933 | Coburg | ~ | ~ | ~ | ~ | ~ |

| AXA Deutschland | 1817 | Cologne | ~ | ~ | ~ | ~ | ~ |

| ERGO Group | 1997 | Düsseldorf | ~ | ~ | ~ | ~ | ~ |

| Getsafe | 2015 | Heidelberg | ~ | ~ | ~ | ~ | ~ |

Germany Online Insurance Market Analysis

Growth Drivers

Mature Comparison Portal Ecosystem and Price Transparency Behavior

Germany’s insurance purchasing landscape is strongly shaped by established online comparison portals that normalize digital policy shopping across motor, household, and supplemental health lines, structurally expanding online insurance distribution and competition. Consumers routinely compare multiple insurers before purchase, emphasizing price and coverage transparency and encouraging insurers to optimize digital pricing and acquisition strategies. High switching rates in commoditized lines such as motor insurance amplify renewal-driven digital engagement cycles and sustain online premium volumes. Comparison portals invest heavily in digital marketing and brand awareness, capturing consumer search intent and directing traffic to online purchase channels. Insurers align product standardization and pricing structures with portal requirements, reinforcing digital suitability. Mobile-friendly quoting and instant underwriting reduce purchase friction. Regulatory acceptance of electronic policy issuance supports fully digital transactions.

High Digital Adoption and Direct Insurer Channel Expansion

Germany exhibits high internet penetration and growing acceptance of digital financial services, enabling insurers to expand direct-to-consumer online channels that reduce distribution costs and improve customer experience across personal insurance lines. Insurers invest in automated underwriting, digital onboarding, and online claims platforms to deliver end-to-end policy lifecycle management. Direct digital brands and insurtech firms promote simplified products and self-service interfaces aligned with consumer expectations for convenience and transparency. Cost efficiencies from digital distribution enable competitive pricing and increased online conversion. Younger demographics and urban consumers increasingly prefer online purchase and servicing rather than agent interaction. Integration of telematics, property data, and behavioral analytics enhances risk assessment accuracy. Regulatory frameworks permitting remote identification and electronic documentation further support online growth. Direct digital expansion therefore materially increases scale and penetration of the Germany online insurance market.

Market Challenges

Strict Data Protection Regulation and Privacy Constraints

Germany’s stringent data protection framework under European privacy regulations imposes significant compliance obligations on insurers operating online channels, affecting data usage, analytics capabilities, and customer acquisition strategies within the online insurance market. Insurers must obtain explicit consent and maintain strict data governance for personal and behavioral information used in underwriting and marketing. Limitations on data sharing across platforms restrict advanced personalization and cross-selling initiatives. Compliance costs for digital infrastructure, cybersecurity, and documentation are substantial. Consumer privacy sensitivity reduces willingness to share data for telematics or personalized pricing programs. Insurtech firms face disproportionate regulatory burden relative to scale. Cross-border cloud and analytics arrangements require strict localization and oversight. Data protection constraints therefore slow innovation and increase operational complexity in the Germany online insurance market.

Aggregator Dependence and Price Competition Pressure

The Germany online insurance market is heavily influenced by comparison portals that control substantial customer acquisition flow, forcing insurers to compete aggressively on price and commissions to secure favorable ranking and visibility. Portal-driven price comparison commoditizes standardized insurance products, reducing differentiation and compressing margins. Insurers bear referral costs and discount pricing to remain competitive. Customer relationships may remain weak when acquisition occurs via third-party platforms, limiting retention and cross-sell opportunities. Marketing expenditure rises as insurers bid for portal placement and digital visibility. Smaller insurers struggle to sustain profitability under aggregator-driven competition. Regulatory scrutiny of portal practices can alter channel economics abruptly. Dependence on comparison platforms therefore represents a structural profitability challenge within the Germany online insurance market.

Opportunities

Embedded Insurance Integration in E-Commerce and Mobility Services

Germany’s mature digital commerce and mobility ecosystems create opportunities for embedded insurance products integrated into online transactions such as travel booking, car rental, device purchase, and parcel delivery, enabling contextual coverage purchase without separate acquisition journeys. E-commerce and service platforms seek value-added offerings that enhance customer experience and generate additional revenue streams. Insurers provide API-based microinsurance solutions embedded directly into digital platforms. Consumers benefit from convenience and relevance of contextual coverage, increasing uptake among digitally active segments. Embedded distribution expands reach beyond comparison portals into new transaction contexts. Behavioral and transactional data improve risk selection and pricing. Platform partnerships enable scalable low-cost distribution. Embedded insurance therefore represents a major growth opportunity in the Germany online insurance market.

AI-Based Personalization and Usage-Based Insurance Models

Advances in artificial intelligence, telematics, and behavioral analytics enable insurers in Germany to offer personalized and usage-based insurance products aligned with individual risk profiles, enhancing differentiation in competitive online markets. Telematics-enabled motor insurance supports behavior-based pricing communicated through digital platforms. Smart home integration supports risk monitoring for household insurance. Personalized dashboards and digital engagement tools improve retention and customer experience. Data-driven underwriting enhances pricing accuracy and loss ratios. Consumers perceive value in fair pricing linked to behavior, encouraging adoption. Regulatory frameworks permitting consent-based data usage enable deployment. AI-driven personalization thus creates innovation-led growth potential for the Germany online insurance market.

Future Outlook

The Germany online insurance market is expected to expand steadily as comparison-driven purchasing and direct digital insurer platforms deepen penetration across personal insurance lines. Embedded insurance and AI-driven personalization will broaden product reach and differentiation. Regulatory frameworks supporting digital transactions will sustain online adoption. Competition will remain intense with pricing and user experience central to positioning. Technological integration will continue reshaping acquisition and servicing models.

Major Players

- Allianz Deutschland

- HUK-Coburg

- AXA Deutschland

- ERGO Group

- Getsafe

- DA Direkt

- R+V Versicherung

- DEVK Versicherung

- Zurich Deutschland

- Generali Deutschland

- CosmosDirekt

- HDI Deutschland

- Nürnberger Versicherung

- Gothaer Versicherung

- BavariaDirekt

Key Target Audience

- Insurance companies

- Digital insurers

- Insurance aggregators

- Investments and venture capitalist firms

- Government and regulatory bodies

- E-commerce platforms

- Automotive and mobility companies

- Fintech platforms

Research Methodology

Step 1: Identification of Key Variables

Key variables included digital gross written premiums, online policy share by product line, channel distribution, and consumer digital adoption. Regulatory provisions on electronic documentation and data protection were mapped. Insurer digital strategies and portal influence assessed.

Step 2: Market Analysis and Construction

Supervisory authority statistics, insurer reports, and industry data synthesized to estimate online premiums. Segmentation by product and channel derived from insurer and portal disclosures. Competitive structure assessed through digital penetration and pricing strategies.

Step 3: Hypothesis Validation and Expert Consultation

Assumptions on portal dominance, digital adoption, and personalization trends validated with insurance distribution and underwriting practitioners. Regulatory interpretations cross-checked with compliance experts. Iterative reconciliation ensured consistency.

Step 4: Research Synthesis and Final Output

Quantitative and qualitative insights integrated into structured sections aligned with outlook requirements. Tables standardized with verified data. Final narrative refined for analytical coherence and clarity.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

High digital adoption and comparison portal usage

Insurer investment in direct digital sales channels

Regulatory support for digital policy issuance and servicing - Market Challenges

Complex product structures limiting full online conversion

Strong broker channel dominance

Data privacy and compliance requirements - Market Opportunities

Usage-based and on-demand insurance products

Embedded insurance in mobility and e-commerce platforms

AI-driven underwriting and automation - Trends

Growth of digital direct insurers and insurtechs

Automation of claims and policy management - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Online Motor Insurance

Online Health Insurance

Online Life Insurance

Online Home and Liability Insurance

Online Travel Insurance - By Platform Type (In Value%)

Direct Insurer Digital Platforms

Aggregator and Comparison Portals

Mobile Insurance Applications

Broker Digital Platforms

Embedded Insurance Platforms - By Fitment Type (In Value%)

Direct-to-Consumer Online

Broker-assisted Digital

Aggregator-based Distribution

Embedded Insurance - By End User Segment (In Value%)

Individual Consumers

Small and Medium Enterprises

Young Digital-native Customers

- Market Share Analysis

- Cross Comparison Parameters (Product Type, Distribution Channel, Digital Platform Capability, Customer Segment Focus, Pricing Model, Underwriting Automation Level, Claims Processing Speed, Broker Integration Level, Data Analytics Utilization, Regulatory Compliance Capability)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Allianz Direct

Allianz Germany

AXA Germany

R+V Versicherung

HUK-COBURG

DEVK Insurance

Gothaer Insurance

Zurich Germany

ERGO Group

HDI Versicherung

Signal Iduna

Generali Deutschland

Barmenia Insurance

Debeka Insurance

LVM Versicherung

- Consumers using comparison portals for policy selection

- SMEs purchasing simple digital commercial coverage

- Young customers preferring mobile-first insurance journeys

- Self-employed professionals adopting flexible policies

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now