Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The German solar photovoltaic (PV) market is estimated to reach USD ~ billion based on a recent historical assessment. The market is driven by increasing demand for clean energy, government incentives for solar installations, and a strong national commitment to reduce carbon emissions. Germany’s ambitious renewable energy targets, coupled with decreasing costs for solar panels and related technologies, continue to fuel the market’s growth. The integration of solar PV into both residential and commercial energy systems also significantly contributes to market expansion.

Germany’s dominance in the solar PV market is largely attributed to the government’s long-standing commitment to renewable energy. Cities like Berlin and Munich lead the way, with significant investments in solar energy and green technologies. Moreover, Germany’s robust infrastructure, including extensive distribution networks for renewable energy, supports the widespread adoption of solar PV. The country’s policies, including the Renewable Energy Sources Act (EEG), also drive renewable energy growth, making Germany one of the largest markets for solar energy in Europe.

Market Segmentation

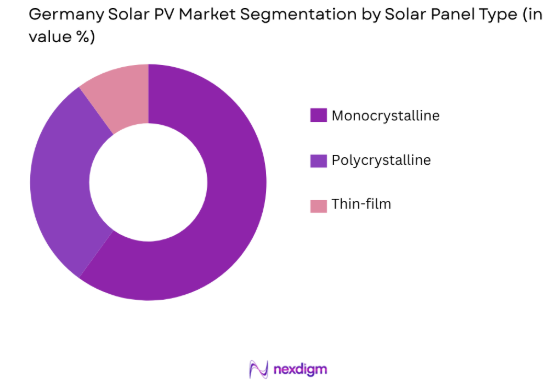

By Solar Panel Type

The German solar PV market is segmented by type of solar panel into monocrystalline, polycrystalline, and thin-film. Recently, monocrystalline solar panels have dominated the market due to their higher efficiency and longer lifespan. They are particularly suitable for residential and commercial installations where space is limited, making them the preferred choice for most solar projects. Furthermore, the decline in manufacturing costs for monocrystalline panels has made them more affordable, further bolstering their market share. The efficiency gains in monocrystalline panels, particularly in low-light conditions, have driven widespread adoption in Germany’s growing solar energy market.

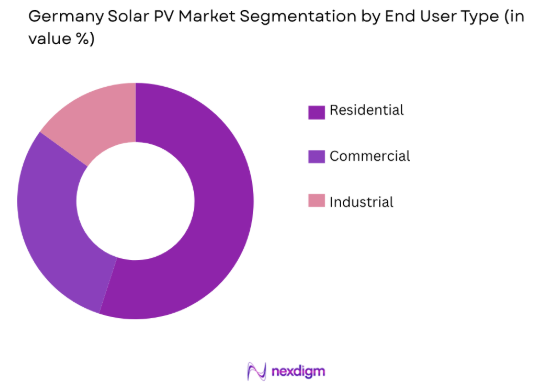

By End-User

The German solar PV market is segmented by end-user into residential, commercial, and industrial. Recently, the residential segment has been the dominant market driver due to the increasing number of homeowners adopting solar panels for self-consumption. Government incentives, such as subsidies and tax benefits, have made solar installations more affordable for residential users. The desire to reduce electricity costs, along with growing environmental concerns, has led to widespread adoption among households. This trend is supported by Germany’s ambitious energy transition goals, which encourage the installation of renewable energy systems across all sectors.

Competitive Landscape

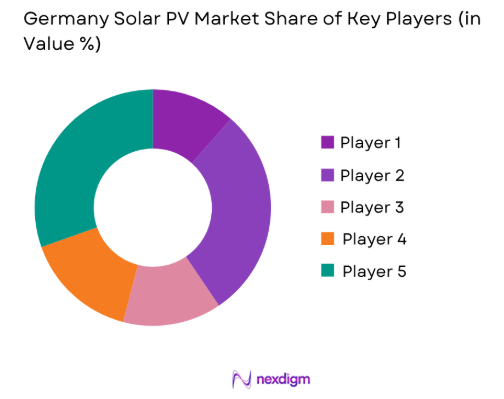

The German solar PV market is highly competitive, with a mix of international and local players dominating the industry. Leading solar manufacturers, including both large corporations and smaller niche companies, are driving innovation and pushing for cost reductions in solar panel production. The market is also characterized by strong collaboration between solar manufacturers, installers, and government entities to ensure the widespread adoption of solar technologies. Companies that provide solar energy solutions are focusing on product differentiation, such as high-efficiency panels and integrated solar energy systems, to remain competitive. Consolidation in the industry is taking place as large players acquire smaller firms to expand their market reach and technological capabilities.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Market-specific Parameter |

| SMA Solar Technology | 1981 | Germany | ~ | ~ | ~ | ~ | ~ |

| First Solar | 1999 | USA | ~ | ~ | ~ | ~ | ~ |

| Canadian Solar | 2001 | Canada | ~ | ~ | ~ | ~ | ~ |

| Q CELLS | 1999 | Germany | ~ | ~ | ~ | ~ | ~ |

| Trina Solar | 1997 | China | ~ | ~ | ~ | ~ | ~ |

Germany Solar PV Market Analysis

Growth Drivers

Government Incentives and Policies

A key growth driver in the German solar PV market is the government’s supportive policy framework, which encourages the adoption of solar energy through incentives and subsidies. Germany has set ambitious renewable energy targets, aiming to achieve a significant portion of its electricity consumption from renewable sources. The Renewable Energy Sources Act (EEG), which guarantees feed-in tariffs and priority grid access for renewable energy producers, has significantly stimulated the solar PV market. Additionally, the government’s commitment to phasing out coal and nuclear energy by 2038 has further pushed the demand for solar energy as a cleaner, more sustainable alternative. Tax benefits, grants for residential solar installations, and various financial programs aimed at reducing the upfront costs of solar PV have made it more accessible to a wide range of consumers. As the government continues to prioritize renewable energy, the market is poised for long-term growth, making solar PV one of the most promising sectors within the renewable energy space.

Technological Advancements and Cost Reductions

Technological advancements in solar panel efficiency and manufacturing processes have also been crucial in driving the growth of the solar PV market in Germany. Over the past decade, the cost of producing solar panels has decreased significantly, thanks to improvements in production technologies and economies of scale. This has made solar energy more affordable for consumers, especially in the residential sector. Additionally, advances in energy storage solutions, such as lithium-ion batteries, have enabled better integration of solar energy into the grid by addressing issues related to intermittency and storage. Solar panels are also becoming more efficient, with higher energy conversion rates, making them an attractive option for homeowners and businesses with limited roof space. These technological improvements have not only made solar energy more accessible but have also enhanced the return on investment for consumers, further encouraging the adoption of solar PV systems in Germany.

Market Challenges

Intermittency and Energy Storage Challenges

One of the primary challenges facing the German solar PV market is the intermittency of solar power. Solar energy production is highly dependent on weather conditions and daylight hours, meaning that energy generation is inconsistent and can fluctuate. This intermittency issue can create challenges for grid stability, particularly during periods of low sunlight or high demand. Although Germany has made strides in energy storage solutions, such as large-scale batteries and pumped hydro storage, the cost and scalability of energy storage remain barriers. Effective and cost-efficient storage solutions are crucial for ensuring that solar energy can be stored during the day and used during the night or on cloudy days. While advances are being made, energy storage technologies are still developing, and their widespread adoption will require further investment in infrastructure and research. Overcoming these challenges is essential for the long-term success and reliability of the solar PV market in Germany.

High Initial Investment and Infrastructure Constraints

Despite the falling costs of solar technology, the high initial investment required for solar PV installations remains a significant barrier for both residential and commercial customers. While government subsidies and financial incentives help reduce the upfront costs, many consumers and businesses may still find it difficult to justify the initial expenditure. Furthermore, the installation of solar PV systems requires adequate infrastructure, including suitable roof space for residential systems and access to land for larger commercial projects. This may be particularly challenging in urban areas where space is limited. Moreover, integrating solar energy into the existing energy grid can require significant upgrades to grid infrastructure, especially in rural areas or where the grid is not fully optimized for renewable energy integration. Overcoming these infrastructural constraints and making solar PV more accessible for all consumers remains a major challenge for the market.

Opportunities

Rural and Agricultural Sector Adoption

An emerging opportunity in the German solar PV market lies in the adoption of solar energy within the rural and agricultural sectors. With a significant portion of Germany’s land area dedicated to agriculture, there is great potential for integrating solar energy into farming operations. Solar PV systems can be installed on agricultural land to generate electricity for farm operations, reducing energy costs and providing an additional income stream through the sale of excess energy to the grid. Agrivoltaics, a system that combines solar power generation with agricultural production, is an exciting development that could revolutionize land use in rural areas. This growing trend of integrating solar power with agricultural practices is gaining momentum, driven by the need for more sustainable farming solutions and greater energy independence. As farmers and rural communities seek to reduce energy expenses and minimize their environmental footprint, the demand for solar PV systems in these areas is expected to rise significantly, offering a new growth avenue for the market.

Exporting Solar Technology and Expertise

Another opportunity for the German solar PV market lies in the export of solar technology and expertise to other countries, particularly in emerging markets. Germany is a global leader in solar PV technology, with a strong track record of innovation in the production of high-efficiency solar panels, energy storage solutions, and smart grid systems. As countries around the world seek to transition to renewable energy, there is increasing demand for German-made solar technologies and solutions. Exporting solar panels, components, and systems to regions with growing energy needs, such as Africa, the Middle East, and Southeast Asia, presents a significant growth opportunity. Additionally, Germany’s expertise in grid management and energy storage solutions can be leveraged to support international solar projects. With Germany’s established reputation as a pioneer in renewable energy technologies, there is a strong potential for German companies to expand their reach in global markets, strengthening the country’s position as a major player in the global solar PV industry.

Future Outlook

The German solar PV market is expected to continue its strong growth trajectory in the next five years, driven by government support, technological advancements, and increasing demand for clean energy. As the country moves towards its renewable energy targets, solar PV will play a critical role in achieving these goals. Technological developments, such as improvements in energy storage, solar panel efficiency, and integration with the smart grid, will further accelerate market growth. Additionally, Germany’s growing interest in exporting solar technology and integrating renewable energy into agricultural sectors will provide further opportunities for expansion. With a strong policy framework and commitment to decarbonization, the solar PV market in Germany is poised for continued success.

Major Players

- SMA Solar Technology

- First Solar

- Canadian Solar

- Q CELLS

- Trina Solar

- SunPower Corporation

- Vestas

- Enphase Energy

- JinkoSolar

- Longi Solar

- REC Group

- Sharp Solar

- RWE Renewables

- Sunrun

- Solarpower Europe

Key Target Audience

- Government and regulatory bodies

- Renewable energy companies

- Investment firms and venture capitalists

- Energy infrastructure developers

- Manufacturing and industrial companies

- Research institutions

- International energy suppliers

Research Methodology

Step 1: Identification of Key Variables

Key market variables such as government policies, technological advancements, and grid integration challenges were identified and analyzed.

Step 2: Market Analysis and Construction

Data was collected from industry reports, government energy policies, and market surveys to estimate the market size, trends, and forecasts for solar PV in Germany.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts, including government officials, solar manufacturers, and energy companies, validated assumptions, trends, and key growth drivers.

Step 4: Research Synthesis and Final Output

The data was synthesized into a comprehensive report that covers market size, segmentation, growth drivers, challenges, and opportunities for stakeholders in the German solar PV market.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Government subsidies and incentives

Technological advancements in solar PV systems

Increasing awareness and adoption of renewable energy

Declining costs of solar panels and installations - Market Challenges

High initial capital investment

Regulatory and policy uncertainties

Interconnection and grid integration issues

Weather and geographical limitations - Market Opportunities

Expansion of solar PV in rural areas

Partnerships for innovation in energy storage

Rising demand for decentralized energy generation - Trends

Rising adoption of residential solar installations

Growth in the integration of solar PV with energy storage - Government Regulations

Renewable Energy Sources Act (EEG)

Feed-in Tariff (FiT) programs

Net metering regulations

Incentives for residential and commercial solar installations - SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Utility-Scale Solar PV Systems

Residential Solar PV Systems

Commercial Solar PV Systems

Rooftop Solar PV Systems

Off-Grid Solar PV Systems - By Platform Type (In Value%)

Onshore Solar PV Platforms

Offshore Solar PV Platforms

Floating Solar PV Platforms

Hybrid Solar PV Platforms - By Fitment Type (In Value%)

Fixed Tilt Solar PV Systems

Tracking Solar PV Systems

Rooftop Solar PV Systems

Ground-Mounted Solar PV Systems - By End User Segment (In Value%)

Residential Users

Commercial Users

Industrial Users

Government and Public Sector

- Market Share Analysis

- Cross Comparison Parameters (System Type, Platform Type, End-User Segment, Technology, Cost Structure, Regulatory Compliance, Fitment Type)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

First Solar

SMA Solar Technology

SunPower

Trina Solar

JA Solar Technology

LONGi Solar

Risen Energy

REC Solar

Canadian Solar

Jinko Solar

Hanwha Q CELLS

BayWa r.e.

Siemens Gamesa

Enphase Energy

LG Electronics

- Residential users’ increasing interest in energy independence

- Commercial and industrial users seeking to reduce energy costs

- Government and public sector initiatives for clean energy adoption

- Energy storage systems’ role in solar PV adoption

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now