Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, Germany’s wealth management market oversees approximately USD ~ trillion in assets under management, according to data published by the Deutsche Bundesbank and the European Fund and Asset Management Association. The market is driven by a high concentration of high-net-worth individuals, strong household savings exceeding USD ~ in financial assets, and institutional demand for structured portfolio advisory services across private banking and asset management channels.

Frankfurt remains the financial nucleus of the Germany Wealth Management Market due to its role as home to the European Central Bank and major financial institutions, while Munich and Hamburg host dense clusters of private banking clients and family offices. Cross-border capital flows within the European Union further strengthen Germany’s appeal as a stable wealth preservation jurisdiction, supported by robust regulatory oversight, advanced digital banking infrastructure, and strong macroeconomic fundamentals.

Market Segmentation

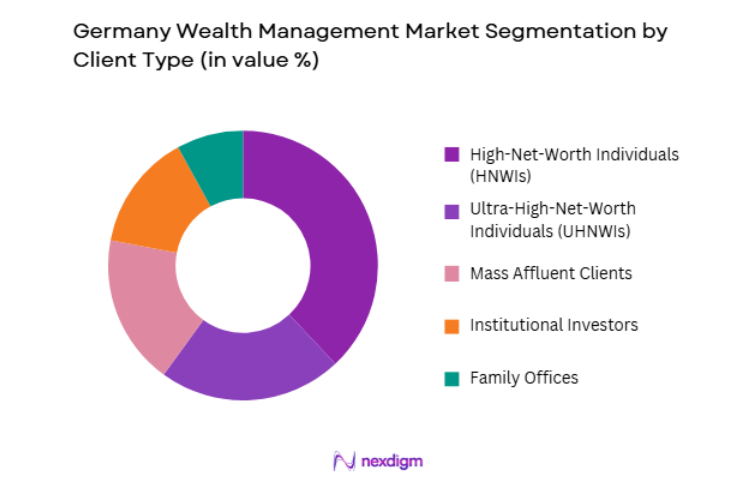

By Client Type (In Value%)

Germany Wealth Management Market is segmented by product type into High-Net-Worth Individuals (HNWIs), Ultra-High-Net-Worth Individuals (UHNWIs), Mass Affluent Clients, Institutional Investors, and Family Offices. Recently, High-Net-Worth Individuals (HNWIs) have a dominant market share due to factors such as rising private wealth accumulation, increasing intergenerational wealth transfers, diversified investment portfolios, and demand for personalized advisory services across equities, fixed income, real estate, and alternative assets, supported by strong private banking networks and structured portfolio management solutions across major German financial hubs.

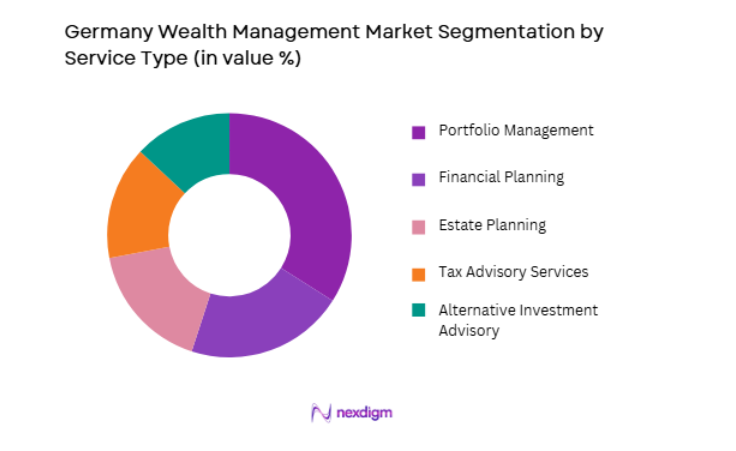

By Service Type (In Value%)

Germany Wealth Management Market is segmented by product type into Portfolio Management, Financial Planning, Estate Planning, Tax Advisory Services, and Alternative Investment Advisory. Recently, Portfolio Management has a dominant market share due to factors such as demand for diversified asset allocation strategies, risk-adjusted return optimization, discretionary mandates, regulatory compliance advisory, and integration of ESG-based investment frameworks, supported by digital platforms and structured research capabilities offered by domestic and international banking institutions operating within Germany.

Competitive Landscape

The Germany Wealth Management Market exhibits moderate consolidation, dominated by universal banks, specialized private banks, and international asset managers with strong domestic operations. Market leadership is concentrated among established institutions with diversified advisory capabilities, digital portfolio platforms, and cross-border expertise. Competition centers on personalized advisory models, ESG integration, structured product innovation, and digital wealth platforms that enhance scalability while maintaining regulatory compliance and fiduciary standards.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD) | Assets Under Management (USD) |

| Deutsche Bank Wealth Management | 1870 | Frankfurt, Germany | ~ | ~ | ~ | ~ | ~ |

| Commerzbank Private Banking | 1870 | Frankfurt, Germany | ~ | ~ | ~ | ~ | ~ |

| UBS Europe SE | 1862 | Frankfurt, Germany | ~ | ~ | ~ | ~ | ~ |

| Allianz Global Investors | 1890 | Munich, Germany | ~ | ~ | ~ | ~ | ~ |

| DWS Group | 1956 | Frankfurt, Germany | ~ | ~ | ~ | ~ | ~ |

Germany Wealth Management Market Analysis

Growth Drivers

Expansion of High-Net-Worth Population and Intergenerational Wealth Transfer

Germany’s steady accumulation of private wealth, supported by industrial strength and export-driven corporate profitability, has significantly expanded the high-net-worth population requiring advanced financial advisory services. The increasing number of entrepreneurs, corporate executives, and inheritors of family-owned enterprises is creating substantial demand for structured wealth preservation strategies. Intergenerational asset transfer is accelerating as aging business founders transition ownership to successors, necessitating estate planning, tax optimization, and diversified asset management frameworks. Wealth managers are responding with tailored discretionary mandates and multi-asset strategies designed to protect capital while generating stable returns. The presence of established private banking infrastructure allows institutions to scale services while maintaining personalized advisory relationships. Cross-border diversification within the European Union further enhances portfolio resilience for affluent clients. Regulatory transparency and investor protection standards reinforce trust in institutional advisory channels. Growing financial literacy and demand for sustainable investment strategies also stimulate portfolio expansion into ESG-aligned assets. Together, these structural dynamics provide a long-term foundation for sustained demand in Germany’s wealth management ecosystem.

Digital Transformation and ESG-Oriented Investment Integration

The rapid adoption of digital advisory platforms and data-driven portfolio management tools is reshaping the competitive dynamics of Germany’s wealth management landscape. Financial institutions are deploying artificial intelligence-based analytics, automated rebalancing systems, and client portals that improve transparency and operational efficiency. Digital onboarding and hybrid advisory models enable wealth managers to expand access to affluent and mass affluent clients without compromising regulatory compliance. Concurrently, ESG integration has transitioned from a niche offering to a core portfolio construction principle, driven by regulatory frameworks and strong investor demand for sustainable assets. Asset managers are incorporating climate risk analytics, impact measurement tools, and sustainability scoring into core advisory propositions. This dual transformation enhances scalability, reduces operational costs, and aligns portfolios with evolving investor expectations. Germany’s regulatory framework encourages sustainable finance disclosures, increasing institutional credibility. Technological modernization also strengthens risk monitoring and reporting standards. Collectively, digital innovation and ESG integration serve as powerful catalysts accelerating structural evolution across the market.

Market Challenges

Stringent Regulatory Compliance and Reporting Requirements

Germany’s wealth management industry operates within a highly regulated financial environment shaped by European Union directives and domestic supervisory oversight. Compliance with MiFID II, anti-money laundering directives, and data protection regulations significantly increases operational complexity for private banks and asset managers. Extensive reporting obligations demand sophisticated compliance infrastructure and continuous system upgrades. Smaller advisory firms face disproportionate cost burdens associated with regulatory adherence. Complex cross-border investment structures require meticulous documentation and disclosure. Regulatory scrutiny also limits flexibility in product structuring and advisory compensation models. Ongoing updates to sustainability disclosure standards create additional administrative requirements. Compliance-driven cost pressures may constrain profitability margins across mid-sized firms. The need for highly skilled compliance professionals intensifies competition for specialized talent. These structural constraints present a persistent operational challenge within Germany’s wealth management ecosystem.

Market Volatility and Low-Yield Investment Environment

Germany’s wealth management market is exposed to macroeconomic fluctuations, global interest rate cycles, and geopolitical uncertainties that influence asset valuations. Periods of low interest rates compress fixed income returns, reducing portfolio income generation for conservative investors. Equity market volatility affects short-term portfolio performance and client sentiment, increasing advisory pressure. Currency fluctuations impact cross-border allocations within diversified portfolios. Heightened inflationary pressures alter asset allocation strategies and risk tolerance frameworks. Wealth managers must balance capital preservation objectives with return expectations in uncertain economic cycles. Diversification into alternative assets introduces liquidity considerations and complexity in valuation models. Risk management systems require continuous recalibration to adapt to changing market conditions. Client demand for downside protection intensifies during economic downturns. These interconnected factors create structural performance management challenges for advisory institutions operating in Germany.

Opportunities

Expansion of Digital Wealth Platforms for Mass Affluent Segment

Germany’s mass affluent population represents a significant growth avenue for scalable digital wealth management solutions that bridge traditional advisory and robo-advisory models. Hybrid platforms combining algorithm-driven asset allocation with human advisory oversight can deliver cost-efficient yet personalized portfolio services. Increasing digital adoption among younger investors supports expansion into new demographic segments. Wealth managers can leverage advanced analytics to tailor risk profiles and investment preferences more precisely. Subscription-based advisory models enhance recurring revenue streams. Digital platforms enable efficient cross-selling of insurance, tax planning, and retirement products. Integration with open banking infrastructure strengthens data-driven financial planning. Enhanced cybersecurity measures increase client trust in digital channels. Regulatory support for fintech innovation encourages collaboration between banks and technology firms. This convergence of digital capability and demographic demand presents substantial structural opportunity.

Growth in Sustainable and Impact Investment Mandates

Sustainable investing continues to gain momentum within Germany’s wealth management market as clients increasingly prioritize environmental and social responsibility alongside financial returns. Regulatory alignment with European sustainability frameworks strengthens transparency and standardization across ESG investment products. Asset managers can expand thematic funds targeting renewable energy, green infrastructure, and social impact initiatives. Institutional and private clients alike demonstrate willingness to allocate capital toward measurable sustainability outcomes. Integration of climate scenario analysis into portfolio construction enhances long-term risk management. Customized impact reporting differentiates advisory services in a competitive landscape. Collaboration with sustainable finance research institutions deepens analytical capabilities. Growing corporate disclosure requirements improve ESG data quality and comparability. Germany’s industrial leadership in renewable technologies further supports thematic investment growth. This evolving sustainability paradigm offers long-term differentiation and revenue expansion potential.

Future Outlook

Over the next five years, the Germany Wealth Management Market is expected to experience steady structural expansion supported by digitalization, demographic shifts, and regulatory clarity in sustainable finance. Increased adoption of hybrid advisory platforms will improve scalability across affluent client segments. ESG integration and alternative asset allocation are likely to deepen portfolio diversification trends. Stable macroeconomic fundamentals and continued wealth accumulation are anticipated to sustain advisory demand across major financial centers.

Major Players

- Deutsche Bank Wealth Management

- Commerzbank Private Banking

- Allianz Global Investors

- DWS Group

- Berenberg

- Bankhaus Metzler

- Hauck Aufhäuser Lampe

- ODDO BHF

- BayernLB Private Banking

- DZ BANK Private Banking

- Landesbank Baden-Württemberg

- Helaba Private Banking

- LBBW Asset Management

- Union Investment

- Universal-Investment

Key Target Audience

- UBS Europe SE

- BNP Paribas Wealth Management Germany

- J.P. Morgan Private Bank Germany

- Goldman Sachs Bank Europe SE

- HSBC Germany

- BlackRock Germany

- Amundi Deutschland

Research Methodology

Step 1: Identification of Key Variables

Key variables including assets under management, client demographics, regulatory framework, service segmentation, and technological integration were identified through secondary financial databases and supervisory publications. Macroeconomic indicators and wealth distribution data were incorporated to define structural market parameters.

Step 2: Market Analysis and Construction

Market sizing was constructed using official financial disclosures, central bank statistics, and asset management association data. Segmentation was developed by mapping advisory services, client categories, and institutional structures across Germany’s financial ecosystem.

Step 3: Hypothesis Validation and Expert Consultation

Industry assumptions were validated through consultation with financial analysts, portfolio managers, and regulatory specialists. Cross-verification ensured consistency between reported financial metrics and institutional disclosures.

Step 4: Research Synthesis and Final Output

Findings were synthesized into a structured analytical framework integrating quantitative data and qualitative insights. Final outputs were reviewed for coherence, regulatory alignment, and factual accuracy before consolidation into the report.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Large pool of private financial assets and savings culture

Expansion of private banking and advisory networks

Increasing demand for diversified global investments - Market Challenges

Conservative investor preference for low-risk assets

Regulatory compliance and reporting requirements

Fee pressure from digital wealth platforms - Market Opportunities

Growth in ESG and sustainable investment mandates

Digital wealth solutions for mass affluent clients

Intergenerational wealth transfer advisory services - Trends

Integration of digital reporting and portfolio analytics

Rising allocation to alternative and private market assets - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Discretionary Portfolio Management

Advisory and Financial Planning

Private Banking Services

Alternative Investment Advisory

Retirement and Pension Advisory - By Platform Type (In Value%)

Private Bank Wealth Platforms

Universal Bank Wealth Divisions

Independent Financial Advisory Firms

Digital Wealth and Robo-advisory Platforms

Securities Brokerage Wealth Platforms - By Fitment Type (In Value%)

Onshore Wealth Management

Offshore Wealth Structuring

Hybrid Advisory Models

Fully Digital Wealth Solutions - By End User Segment (In Value%)

High Net Worth Individuals

Ultra High Net Worth Individuals

Mass Affluent Investors

- Market Share Analysis

- Cross Comparison Parameters (Client Segment Focus, Asset Class Coverage, Advisory Model, Digital Platform Capability, Pricing Structure, Relationship Management Depth, ESG Integration Capability, Alternative Investment Access, Portfolio Customization Level, Cross-border Structuring Expertise)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Deutsche Bank Wealth Management

Commerzbank Wealth Management

DZ Bank Private Banking

Berenberg Bank

Hauck Aufhäuser Lampe

ODDO BHF Wealth Management

UBS Germany Wealth Management

Julius Baer Germany

HSBC Trinkaus & Burkhardt

BNP Paribas Wealth Management Germany

DekaBank Private Banking

Helaba Wealth Management

Santander Private Banking Germany

MM Warburg & CO

HypoVereinsbank Wealth Management

- Affluent families seeking structured succession planning

- Entrepreneurs diversifying beyond domestic assets

- Mass affluent investors adopting managed portfolios

- Family offices formalizing governance frameworks

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now