Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The global shotgun cartridge market is valued at USD ~ million, supported by published industry sizing for worldwide shotgun ammunition. Demand is sustained by high-volume consumption in recreational shooting disciplines (trap/skeet/sporting clays), recurring hunting season pull-through, and institutional procurement for training, breaching, and crowd-management loads (including specialty less-lethal rounds). The market’s forward trajectory is anchored by a published endpoint of USD ~ million, implying steady multi-year expansion.

The market is structurally led by countries with (i) deep sport shooting infrastructure (ranges, clubs, competitions), (ii) established hunting cultures and licensing ecosystems, and (iii) large, scaled shotshell manufacturing footprints. North America remains a key demand center because of entrenched hunting and clay sports participation and strong retail distribution depth, while parts of Europe are anchored by regulated hunting traditions and competitive shooting circuits. These hubs also host major brands and contract manufacturing capacity, improving SKU availability across gauges and load types.

Market Segmentation

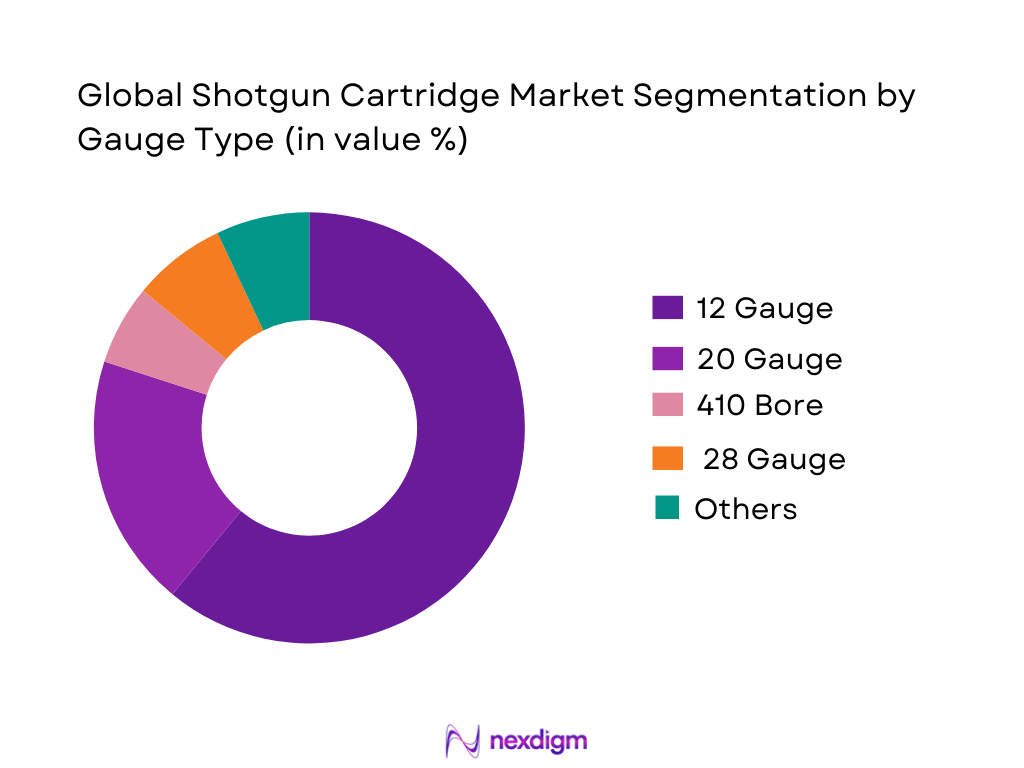

By Gauge Type

By gauge type, 12 gauge is the dominant global demand pool because it is the most versatile platform across hunting, sport shooting, and tactical/utility applications. It benefits from the broadest SKU universe (birdshot, buckshot, slugs, low-recoil, specialty wads, and purpose-built loads), enabling retailers and distributors to concentrate assortment depth and improve inventory turns. Training and institutional buyers also standardize on 12 gauge for procurement efficiency, while the global installed base of 12-gauge shotguns supports recurring aftermarket consumption. Reflecting this structural versatility and channel preference, published segment data indicates 12 gauge accounts for 60.9% of revenue in the latest year.

By Application / End-Use

By application, the largest volume-consumption engine is hunting & sport shooting, because these channels generate repeat purchase behavior driven by seasonality (hunting) and high round-count training/competition cycles (clay sports). Hunters typically purchase multiple load types (upland, waterfowl, turkey) with different shot materials and payload profiles, while competitive shooters consume high-throughput target loads as part of routine practice, league play, and events. These use-cases also have strong retail visibility (sporting goods, specialty firearms retailers, and large distributor networks), enabling frequent replenishment and broad SKU access. Publicly available segmentation indicates hunting & sport shooting represents 48% of demand in the latest year within one openly published market split.

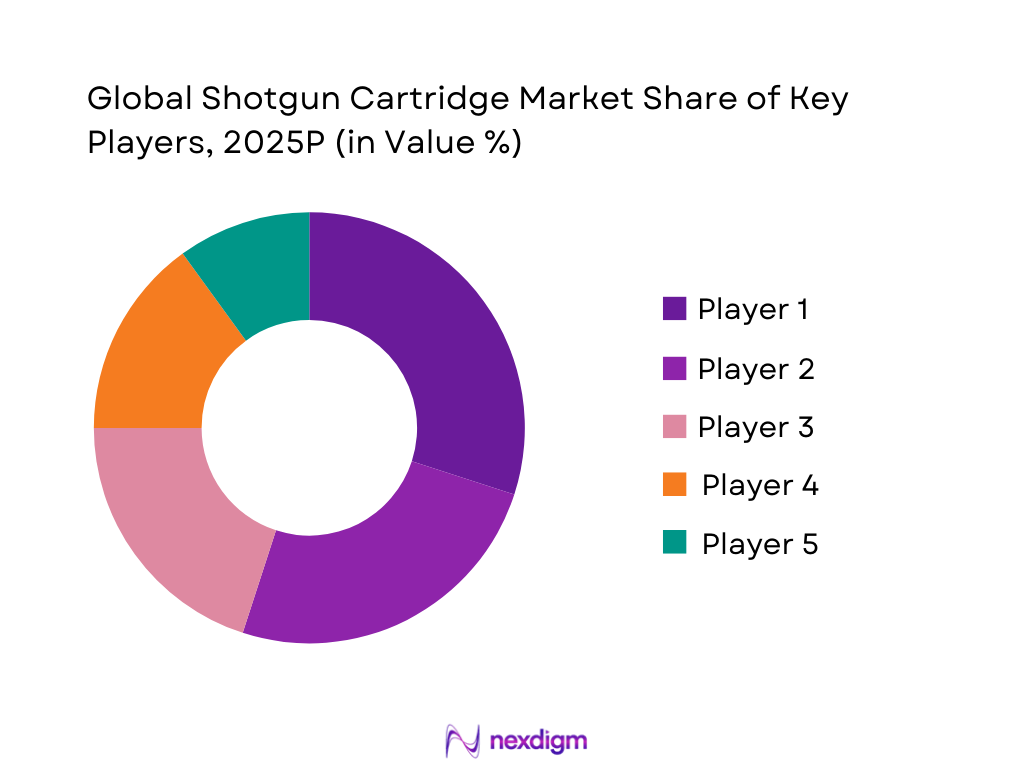

Competitive Landscape

The global shotgun cartridge market is brand- and channel-concentrated, with a set of long-established ammunition producers controlling broad SKU catalogs across gauges and load types, plus regionally strong challengers that win via distributor relationships, contract manufacturing, and specialty performance loads (non-toxic, low-recoil, premium hunting, and operational less-lethal). Consolidation is also shaped by manufacturing scale, certification/standards alignment, and the ability to serve both civilian and institutional buyers reliably across cycles.

| Company | Est. Year | HQ | Core Shotshell Brands / Labels | Gauge Breadth Focus | Manufacturing Footprint Signal | Primary Demand Focus | Channel Strength | Differentiation Lever |

| Olin (Winchester Ammunition) | 1892 | USA | ~ | ~ | ~ | ~ | ~ | ~ |

| Fiocchi Munizioni | 1876 | Lecco, Italy | ~ | ~ | ~ | ~ | ~ | ~ |

| CBC Global Ammunition (CBC/Magtech group) | 1926 | Brazil | ~ | ~ | ~ | ~ | ~ | ~ |

| Remington (ammunition/brand ecosystem) | 1816 | USA | ~ | ~ | ~ | ~ | ~ | ~ |

| NobelSport (NobelSport Italia) | — | Italy | ~ | ~ | ~ | ~ | ~ | ~ |

Global Shotgun Cartridge Market Analysis

Growth Drivers

Firearms License Base

The global shotgun cartridge market is structurally supported by a large and legally expanding firearms license base in major consumption economies. In the United States, the FBI National Instant Criminal Background Check System recorded 28,097,205 firearm background checks, indicating sustained legal acquisition activity tied directly to ammunition consumption for training, sport shooting, and hunting. In Europe, the United Kingdom reported 495,798 active shotgun certificates and 147,364 firearm certificates, reflecting a stable licensed user base that requires recurring cartridge replenishment. Canada reported 2,425,627 licensed firearms holders, reinforcing North America’s dominance in lawful shotgun ownership. These licensed users operate within high-income economies: the World Bank reports GDP per capita of USD 84,534 for the US, USD 53,246 for the UK, and USD 54,966 for Canada, enabling discretionary spending on sporting ammunition and seasonal hunting cartridges. This licensed ecosystem directly underpins recurring cartridge demand across civilian, sporting, and institutional use.

Hunting Participation

Hunting participation remains a critical consumption driver for shotgun cartridges due to seasonal intensity and repeated ammunition usage. In the United States, the U.S. Fish & Wildlife Service reports 14,101,000 licensed hunters, with small-game and upland bird hunting relying predominantly on shotgun cartridges. In Canada, federal data shows 1,309,000 resident hunters, with waterfowl and small-game categories accounting for high shotshell usage per hunting season. In Europe, Germany alone records 384,000 licensed hunters, supported by long-standing hunting traditions regulated under federal hunting law. These activities are supported by strong rural and outdoor economies: the World Bank reports USD 28.7 trillion GDP for the United States and USD 4.5 trillion GDP for Germany, sustaining land access, hunting clubs, and ammunition retail ecosystems. The repetitive and seasonal nature of hunting directly translates into consistent cartridge consumption across global markets.

Market Challenges

Lead Bans

Lead ammunition restrictions present a structural challenge to the shotgun cartridge market by forcing material substitution, regulatory compliance, and firearm compatibility adjustments. The European Chemicals Agency estimates 1,000,000 birds are affected annually by lead poisoning from ammunition residues, prompting strict regulatory action. The EU ban prohibits lead shot usage in wetlands and within 100 meters of such areas, significantly impacting traditional hunting cartridges. The agency further estimates lead ammunition contributes to over 20,000 tonnes of lead emissions annually, intensifying enforcement pressure. These regulatory actions affect manufacturers’ production processes, certification requirements, and distribution eligibility. While demand persists, compliance costs increase across supply chains. The challenge is amplified in regulated high-income regions, where the IMF reports EUR 16.6 trillion GDP for the European Union, meaning policy enforcement capacity is strong and persistent rather than temporary.

Regulatory Fragmentation

Regulatory fragmentation across countries creates compliance complexity for global shotgun cartridge manufacturers and distributors. Firearms and ammunition laws vary significantly: the United States regulates under federal and state statutes, while Europe operates under country-specific firearms acts alongside EU-level chemical rules. For example, the UK mandates police-issued certificates for every shotgun owner, while Germany requires federal hunting licenses combined with regional firearm registration. Japan permits shotgun ownership under one of the world’s strictest licensing regimes, resulting in extremely controlled ammunition distribution. According to the World Bank, over 65 percent of global GDP is generated in countries with independently administered firearms laws, increasing compliance variation. This fragmentation complicates cross-border trade, SKU standardization, and inventory planning. Manufacturers must customize cartridge offerings and packaging per jurisdiction, increasing operational complexity without reducing underlying demand.

Opportunities

Eco-Friendly Ammunition

Eco-friendly shotgun cartridges represent a strong opportunity as environmental regulation converts compliance into recurring demand. The European Chemicals Agency estimates that restricting lead ammunition could prevent approximately 630,000 tonnes of cumulative lead emissions, accelerating the shift toward steel, bismuth, and tungsten cartridges. Wetlands protection rules now require hunters to carry non-lead cartridges in large parts of Europe, immediately expanding the addressable base for compliant shotshells. High-income consumer markets support this transition: the World Bank reports household final consumption expenditure of USD 18.1 trillion in the US and USD 2.3 trillion in Germany, enabling adoption of higher-specification eco-compliant ammunition without reducing participation. As hunting and shooting activities continue under stricter rules, eco-friendly cartridges transition from niche alternatives to standard-issue products, structurally expanding this segment.

Premium Sport Cartridges

Premium sport cartridges are gaining traction due to rising participation in organized shooting sports and the concentration of disposable income in developed markets. The International Shooting Sport Federation reports over 160 national federations, supporting structured training and competition environments where high-performance cartridges are preferred. In the United States, the Bureau of Economic Analysis reports USD 1.1 trillion in recreational services output, indicating sustained spending capacity for performance-oriented sporting goods. Similarly, Europe’s strong club-based shooting culture benefits from EUR 10.6 trillion in household consumption expenditure, as reported by Eurostat. Competitive shooters demand consistency, recoil management, and pattern precision, driving repeat purchases of premium cartridges. This segment benefits from existing participation levels rather than new adoption, making it a durable growth opportunity supported by current macroeconomic strength.

Future Outlook

Over the next planning cycle, the shotgun cartridge market is expected to advance on three reinforcing vectors: (1) sustained participation in clay sports and organized range activity, (2) product premiumization in hunting loads (performance payloads, wad innovations, tighter QC), and (3) regulatory-driven substitution (especially lead-free and lower-environmental-impact configurations where mandated). At the same time, manufacturers are likely to invest in capacity resilience, component supply assurance (primers, powders, shot materials), and SKU rationalization to protect margins while maintaining channel service levels. Published forward sizing points to continued growth to USD ~ million.

Major Players

- Olin (Winchester Ammunition)

- Fiocchi Munizioni

- CBC Global Ammunition (CBC / Magtech group)

- Remington

- Federal (Vista Outdoor/brand ecosystem)

- Hornady

- Sellier & Bellot

- NobelSport Italia

- RIO Ammunition

- Baschieri & Pellagri

- Eley

- Gamebore

- Kent Cartridge

- Sterling Ammunition

- PPU (Prvi Partizan)

Key Target Audience

- Ammunition manufacturers & contract loaders (shotshell lines)

- Component suppliers (shot materials, wads, primers, powders, hulls)

- National & regional distributors / importers (bulk procurement and private label)

- Sporting goods retail chains & specialty firearms retailers

- Shooting range operators & clay sports venues (league/event procurement)

- Hunting & outdoor organizations / procurement groups (seasonal bulk demand)

- Investments and venture capitalist firms (platform rollups, specialty ammo, manufacturing automation)

- Government and regulatory bodies (ATF – USA; CIP member proof/regulatory bodies in Europe; national environment agencies governing lead/non-lead shot rules)

Research Methodology

Step 1: Identification of Key Variables

We construct the market ecosystem map covering ammunition OEMs, contract loaders, component suppliers, distributors/importers, retail, and institutional channels. We define variables such as gauge mix, load-type mix, channel cadence, and regulatory constraints that influence demand and SKU strategy.

Step 2: Market Analysis and Construction

We compile historical market signals (revenue directionality, product mix evolution, and region demand centers) and align them with published market sizing endpoints. We structure segmentation under consistent taxonomies (gauge and application/end-use) to avoid double counting across civilian and institutional channels.

Step 3: Hypothesis Validation and Expert Consultation

We validate demand drivers, channel mix, and procurement behaviors via expert interviews (manufacturers, distributors, range operators, and institutional buyers). This step is used to reconcile taxonomy differences (e.g., “civilian vs sport” splits) and to confirm dominant sub-segments.

Step 4: Research Synthesis and Final Output

We triangulate findings across public market datasets, company disclosures, and channel interviews to finalize sizing narrative, segment dominance logic, and competitive benchmarking. The deliverable is then QA-checked for taxonomy consistency and source traceability.

- Executive Summary

- Research Methodology (Market Definitions and Assumptions, Ammunition Classification Logic, Gauge–Load Compatibility Framework, Terminal Ballistics Benchmarking, Demand-Side Consumption Modeling, Supply-Side Capacity Mapping, Primary Interviews with Cartridge OEMs, Distributors, Shooting Federations and Hunting Associations, Trade Flow and Import Licensing Mapping, Limitations and Forward Assumptions)

- Definition and Scope

- Industry Evolution and Technology Progression

- Timeline of Shotgun Cartridge Design and Material Innovations

- Industry Business Cycle and Demand Seasonality

- End-to-End Value Chain Analysis

- Raw Material Ecosystem (Shot Metals, Hulls, Primers, Propellants, Wads)

- Manufacturing and Assembly Process Flow

- Growth Drivers (firearms license base, hunting participation, sport shooting infrastructure)

- Market Challenges (lead bans, regulatory fragmentation, logistics constraints)

- Opportunities (eco-friendly ammunition, premium sport cartridges)

- Technology and Product Trends (low-recoil, pattern optimization, biodegradable components)

- Regulatory and Compliance Landscape (CIP, SAAMI, environmental directives)

- SWOT Analysis

- Stakeholder Ecosystem

- Porter’s Five Forces Analysis

- Competitive Intensity Mapping

- By Value, 2019-2025P

- By Volume (Cartridge Consumption), 2019-2025P

- By Gauge Type (In Value %)

12 Gauge

• Standard chamber

• Magnum chamber

• Super magnum chamber

20 Gauge

• Youth and training use

• Lightweight hunting loads

410 Bore

• Recreational shooting

• Small game and pest control

28 Gauge

• Upland hunting

• Competitive niche shooting

Others

• 10 Gauge

• Regional legacy gauges - By Load Configuration (In Value %)

Light Load

• Training and practice loads

• Youth and beginner loads

Standard Load

• All-round hunting

• Recreational shooting

Heavy / Magnum Load

• Long-range hunting

• High-impact applications - By Shot Material (In Value %)

Lead Shot

Steel Shot

Bismuth Shot

Tungsten-Based Shot

Hybrid and Composite Shot - By Shot Size (In Value %)

Fine Shot (No. 7 to No. 9)

Medium Shot (No. 4 to No. 6)

Large Shot (No. 1 to No. 3)

Buckshot

Slug - By Application (In Value %)

Hunting

Sports Shooting

Law Enforcement & Security

Military & Training

Pest and Wildlife Control - By Cartridge Construction (In Value %)

Hull Type

• Plastic hull

• Paper hull

• Metal-base reinforced hull

Wad Type

• Plastic wad

• Fiber wad

• Biodegradable wad

Primer Type

• Boxer primer

• Proprietary primer systems - By Distribution Channel (In Value %)

Authorized Firearms Retailers

Sporting Goods Chains

Government and Institutional Procurement

Shooting Clubs and Ranges

Online Licensed Platforms - By Geography, (In Value %)

North America

Europe

Asia Pacific

Latin America

(Top 3 Countries in each region)

- Market Share of Major Players, 2019-2025P (Value and Volume)

- Cross Comparison Parameters (Gauge Coverage Breadth, Shot Material Portfolio, Ballistic Consistency, Production Capacity, Environmental Compliance Readiness, Distribution Reach, Pricing Tier Coverage, Innovation Pipeline, Shot Size Range Coverage, Load Configuration Diversity, Cartridge Construction Quality, Regulatory & Certification Compliance, Manufacturing Automation Level, Supply Chain Resilience, Institutional & Government Contract Capability, Brand Equity & End-User Loyalty)

- Competitive Positioning Matrix

- Pricing Analysis by Gauge and Application

- Detailed Profiles of Major Companies

Vista Outdoor

Olin Corporation

FN Herstal

Nammo

CBC Global Ammunition

B&P Ammunition

Cheddite

Eley Hawk

NobelSport

Sellier & Bellot

Baschieri & Pellagri

Rio Ammunition

Gamebore

Kent Cartridge

Lyalvale Express

- Consumption Patterns by End User

- Purchase Frequency and Stockpiling Behavior

- Compliance and Licensing Requirements

- Pain Point and Performance Expectation Analysis

- Brand Loyalty and Switching Behavior

- By Value, 2026-2035

- By Volume (Cartridge Consumption), 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now