Download PDF

Download PDFMarket Overview

The India AC Servo Drives and Motors System Market is supported by increasing industrial automation deployment across automotive manufacturing, machine tools, electronics assembly, packaging machinery, and semiconductor-related industries. The market generated nearly USD ~ million in industrial automation revenues due to expanding demand for high-precision motion control systems and smart factory integration. Growth in CNC machine installations, robotics deployment, and automated material handling systems has accelerated servo system adoption across manufacturing facilities. Increasing investments in warehouse automation, EV production infrastructure, and Industrial IoT-enabled manufacturing lines are further strengthening deployment of servo motors, servo drives, and integrated motion control solutions across India’s automation ecosystem.

Industrial hubs such as Pune, Chennai, Bengaluru, Ahmedabad, Noida, Gurugram, and Hyderabad dominate the India AC Servo Drives and Motors System Market because of their strong concentration of automotive OEMs, electronics manufacturers, semiconductor assembly operations, and machine tool industries. Southern and western India remain key adoption centers due to advanced industrial infrastructure and higher automation penetration across factories. Countries such as Japan, Germany, and China dominate the global servo system ecosystem because of their established robotics manufacturing capabilities, precision engineering expertise, and extensive deployment of smart manufacturing technologies across automotive, semiconductor, and industrial automation sectors.

Market Segmentation

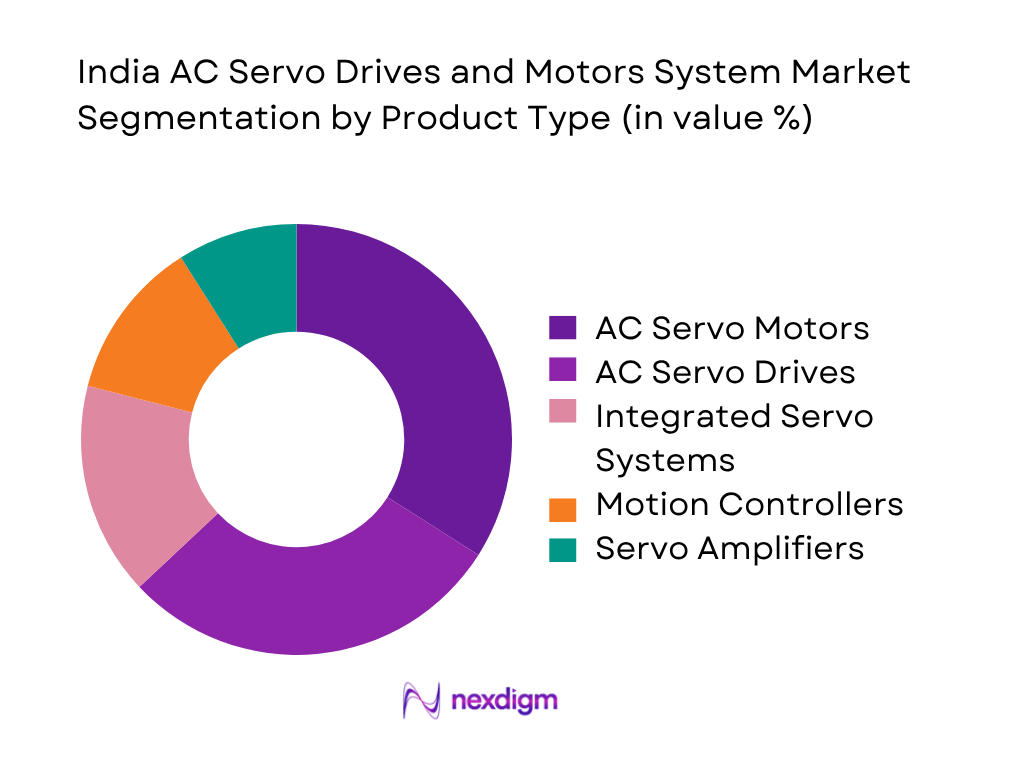

By Product Type

The India AC Servo Drives and Motors System Market is segmented by product type into AC servo motors, AC servo drives, integrated servo systems, motion controllers, and servo amplifiers. AC servo motors dominate the market because they serve as the primary motion execution component across CNC machine tools, industrial robotics, semiconductor handling systems, packaging machinery, and automated conveyor systems. Manufacturers increasingly prefer servo motors because of their superior torque control, precision positioning, high-speed synchronization capability, and energy efficiency compared to conventional induction motors. Rising deployment of robotic welding systems, pick-and-place robots, AGVs, and smart manufacturing lines across automotive and electronics industries continues to strengthen adoption of advanced servo motor systems. Additionally, increasing factory modernization initiatives and growing investments in precision engineering manufacturing facilities support continued dominance of AC servo motors within India’s industrial automation ecosystem.

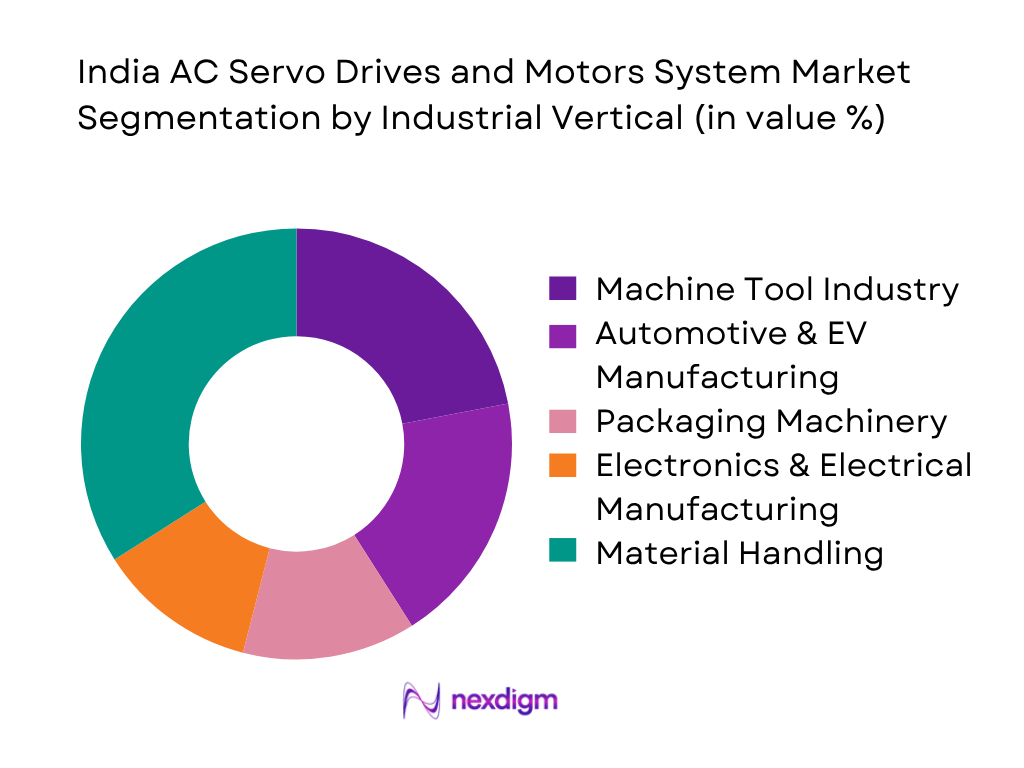

By Industrial Vertical

The India AC Servo Drives and Motors System Market is segmented by industrial vertical into machine tools, automotive and EV manufacturing, packaging machinery, electronics and electrical manufacturing, material handling, plastics and injection molding, textile, pharmaceuticals, food and beverage processing, and semiconductor manufacturing. The machine tool industry dominates because servo systems are essential for precision positioning, synchronized machining, and high-speed automated production in CNC-based operations. India’s growing domestic manufacturing of automotive components, aerospace parts, industrial equipment, and precision engineering products has accelerated deployment of CNC machines requiring advanced servo control systems. In addition, industrial automation investments across automotive and EV manufacturing facilities continue to support large-scale deployment of multi-axis servo drives and motion controllers. The increasing shift toward smart manufacturing and digitally connected factories is further expanding servo adoption across industrial machine tool applications in India.

Competitive Landscape

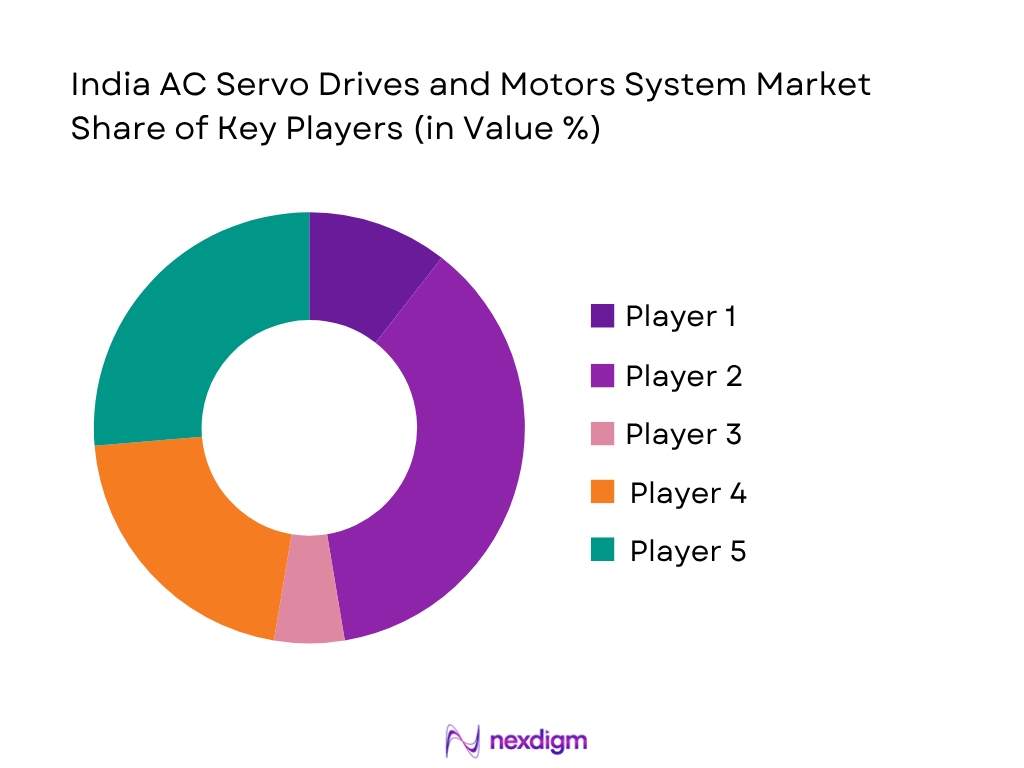

The India AC Servo Drives and Motors System Market is moderately consolidated with global industrial automation manufacturers maintaining strong dominance through advanced motion control technologies, OEM partnerships, and integrated automation platforms. Market participants are increasingly focusing on localization strategies, Industrial Ethernet integration, predictive maintenance software, and AI-enabled motion control systems to strengthen their industrial presence. Increasing investments in smart manufacturing infrastructure, robotics integration, and Industry 4.0 technologies are encouraging companies to expand engineering support centers, service networks, and manufacturing operations within India.

| Company | Establishment Year | Headquarters | Key Product Focus | Industrial Vertical Strength | Localization Capability | Industrial Ethernet Compatibility | Service & AMC Network | Innovation Focus |

| Siemens AG | 1847 | Germany | ~ | ~ | ~ | ~ | ~ | ~ |

| Mitsubishi Electric Corporation | 1921 | Japan | ~ | ~ | ~ | ~ | ~ | ~ |

| Yaskawa Electric Corporation | 1915 | Japan | ~ | ~ | ~ | ~ | ~ | ~ |

| Schneider Electric | 1836 | France | ~ | ~ | ~ | ~ | ~ | ~ |

| Delta Electronics | 1971 | Taiwan | ~ | ~ | ~ | ~ | ~ | ~ |

India AC Servo Drives and Motors System Market Analysis

Growth Drivers

Expansion of Electronics and Semiconductor Manufacturing

India’s rapid expansion in electronics and semiconductor manufacturing is significantly driving demand for AC servo drives and motors systems across precision automation environments. Domestic electronics production crossed USD 115 billion during FY2024 according to the Ministry of Electronics and Information Technology, supported by rising investments in smartphones, industrial electronics, and semiconductor packaging operations. Semiconductor manufacturing projects exceeding INR 1.26 lakh crore were approved under national semiconductor initiatives, increasing deployment of robotics, automated material handling systems, and high-precision motion control equipment. Electronics exports crossed USD 29 billion during FY2024, while mobile phone exports exceeded USD 15 billion. Servo systems are increasingly integrated into SMT assembly lines, robotic handling systems, semiconductor clean-room automation, and PCB manufacturing facilities requiring micron-level precision and synchronized motion control operations.

Rising Industrial Automation Investments Across Manufacturing

Increasing industrial automation investments across India’s manufacturing sectors are accelerating deployment of AC servo systems in machine tools, packaging machinery, warehouse automation, and automotive production facilities. Manufacturing sector capacity utilization exceeded 74% during 2024 according to the Reserve Bank of India, encouraging factories to improve productivity through smart automation deployment. India’s automobile production crossed 28 million vehicles during FY2024, while manufacturing-related FDI inflows exceeded USD 165 billion between 2022 and 2024. Servo systems are increasingly used in robotic welding, CNC machining centers, conveyor automation, and high-speed synchronized assembly systems due to their superior positioning accuracy and operational efficiency. Rising investments in EV manufacturing plants and automated production infrastructure continue to strengthen industrial demand for advanced motion control technologies.

Market Challenges

Dependence on Imported Precision Components

The India AC Servo Drives and Motors System Market faces substantial challenges due to dependence on imported semiconductors, encoders, power electronics, and precision controllers. India’s electronic component imports exceeded USD 72 billion during FY2024, with major sourcing dependency on China, Japan, South Korea, and Taiwan. Advanced servo systems require imported IGBTs, industrial semiconductors, and digital control architectures, increasing procurement risk and operational uncertainty for Indian automation OEMs. Semiconductor supply disruptions between 2022 and 2024 also affected production schedules across CNC machinery, robotics equipment, and packaging automation systems. Currency volatility and logistics disruptions continue to impact procurement lead times and industrial automation deployment costs across India’s manufacturing ecosystem.

Shortage of Skilled Automation Workforce

The shortage of technically skilled professionals capable of operating and integrating advanced motion control systems remains a major challenge for India’s industrial automation ecosystem. India requires more than 30 million digitally skilled workers by 2026 according to the Ministry of Skill Development and Entrepreneurship, particularly across automation, robotics, and industrial electronics sectors. Increasing industrial robot deployments and smart factory installations require expertise in PLC programming, servo tuning, Industrial Ethernet integration, and predictive maintenance systems. Many SMEs and mid-sized factories continue to face operational inefficiencies because workforce skill development has not kept pace with industrial automation adoption across automotive, electronics, semiconductor, and warehouse automation industries.

Market Opportunities

Localization and Import Substitution in Industrial Automation

India’s industrial automation ecosystem presents major opportunities for localization and import substitution across servo motors, drives, motion controllers, and industrial electronics manufacturing. Manufacturing-related FDI inflows exceeded USD 17 billion during FY2024, while multiple industrial incentive schemes encouraged domestic production of automation hardware and electronics. Increasing geopolitical diversification of supply chains is encouraging global automation manufacturers to establish assembly plants, sourcing operations, and engineering centers within India. Servo localization opportunities are especially strong across machine tools, warehouse automation, packaging machinery, and textile equipment manufacturing sectors where imported automation systems currently dominate industrial deployment.

Growth of Warehouse Automation and Smart Material Handling Infrastructure

The expansion of India’s logistics, warehousing, and e-commerce sectors is creating strong demand for servo-controlled automation systems across material handling applications. India’s warehousing stock exceeded 430 million square feet during 2024 due to growth in logistics infrastructure and industrial corridor development. Modern warehouses increasingly deploy servo-integrated conveyor systems, AGVs, robotic palletizers, automated storage and retrieval systems, and high-speed sorting equipment to improve operational throughput. Servo systems play a critical role in synchronized motion control, robotic handling precision, and automated inventory movement across large-scale logistics and industrial warehouse facilities.

Future Outlook

The India AC Servo Drives and Motors System Market is expected to witness strong expansion over the coming years due to increasing factory automation penetration, rising deployment of industrial robotics, and growing investments in semiconductor and electronics manufacturing infrastructure. Expansion of smart manufacturing facilities, warehouse automation systems, and CNC machine installations is expected to accelerate adoption of servo drives, motors, and integrated motion control platforms. Manufacturers are increasingly focusing on Industrial IoT integration, predictive maintenance software, and multi-axis intelligent motion systems to improve operational productivity and reduce downtime across industrial facilities. The market is also expected to benefit from increasing localization initiatives, expansion of EV manufacturing infrastructure, and rising automation adoption among SMEs. Growth in semiconductor assembly operations, pharmaceutical packaging automation, food processing lines, and electronics manufacturing services will continue to strengthen industrial demand for high-precision servo systems. Furthermore, increasing investments in AI-enabled motion control technologies, Industrial Ethernet communication networks, and regenerative energy-efficient servo architectures are expected to support long-term growth opportunities across India’s industrial automation ecosystem.

Major Players

- Siemens AG

- Mitsubishi Electric Corporation

- Yaskawa Electric Corporation

- ABB Ltd.

- Schneider Electric

- Rockwell Automation

- Delta Electronics

- Omron Corporation

- Panasonic Industry

- Bosch Rexroth

- Fuji Electric

- Beckhoff Automation

- Emerson Electric Co.

- Fanuc Corporation

- Nidec Corporation

Key Target Audience

- Industrial Automation OEMs

- Machine Tool Manufacturers

- Packaging Machinery Manufacturers

- Material Handling and Warehouse Automation Companies

- Automotive and EV Manufacturing Companies

- Electronics and Semiconductor Manufacturing Facilities

- Investments and Venture Capitalist Firms

- Government and Regulatory Bodies

Research Methodology

Step 1: Identification of Key Variables

The initial stage involved identifying critical variables influencing the India AC Servo Drives and Motors System Market, including industrial automation penetration, robotics deployment, CNC machine demand, warehouse automation investments, and localization trends. Extensive secondary research was conducted using industrial databases, government publications, trade statistics, and manufacturing reports to understand the market ecosystem and value chain structure.

Step 2: Market Analysis and Construction

Historical market analysis was conducted using automation deployment statistics, OEM sales data, import-export trade information, and industrial capex trends related to servo systems and motion control technologies. Market revenue estimations were derived using bottom-up calculations across industrial verticals including machine tools, automotive manufacturing, electronics, warehouse automation, and semiconductor industries.

Step 3: Hypothesis Validation and Expert Consultation

The preliminary market findings were validated through interviews with automation OEMs, servo system distributors, machine builders, industrial integrators, and manufacturing plant operators. These interactions provided operational insights regarding technology adoption, procurement trends, localization challenges, industrial demand outlook, and automation investment strategies across India’s industrial ecosystem.

Step 4: Research Synthesis and Final Output

The final stage involved consolidating qualitative and quantitative findings to develop a comprehensive assessment of the India AC Servo Drives and Motors System Market. Cross-validation was conducted using government trade statistics, automation deployment trends, industrial production data, and company disclosures to ensure consistency and reliability of market estimations, segmentation analysis, and strategic opportunity mapping.

- Executive Summary

- Research Methodology (Market Definitions and Assumptions, Abbreviations, Research Framework, Bottom-Up Market Estimation, Top-Down Validation Model, OEM-Level Revenue Benchmarking, Automation Penetration Mapping, Industrial Capex Assessment, Trade Flow and Import Dependency Analysis, Primary Interviews with Automation OEMs and System Integrators, Factory-Level Demand Assessment, Forecasting Framework, Limitations and Assumptions)

- Definition and Scope

- Evolution of Industrial Automation and Motion Control in India

- Industry Ecosystem and Stakeholder Mapping

- Servo System Architecture Overview

- Supply Chain and Value Chain Analysis

- Raw Material and Semiconductor Component Dependency

- Growth Drivers

Expansion of Electronics and Semiconductor Manufacturing

Rising Industrial Automation Investments Across Manufacturing

Growth in CNC Machine Tool Deployments

Expansion of Warehouse Automation and Material Handling Systems

Increasing Robotics Adoption Across Factories - Market Challenges

Dependence on Imported Precision Components

Shortage of Skilled Automation Workforce

Semiconductor Supply Chain Constraints

High Initial Capital Investment for Automation Systems - Market Opportunities

Localization and Import Substitution in Industrial Automation

Expansion of Smart Factory Infrastructure

Growth in SME Automation Adoption

Increasing Demand for AI-Enabled Motion Control

Growth of Automated Warehousing and Logistics Infrastructure - Market Trends

Shift Towards Multi-Axis Intelligent Servo Systems

Integration of Industrial IoT and Predictive Maintenance

Rising Adoption of EtherCAT and PROFINET Networks

Compact Integrated Servo System Development

Energy-Efficient Regenerative Servo Technologies - Government Regulations

BIS and IEC Compliance Standards

Industrial Safety and Motion Control Standards

Localization and Manufacturing Incentives

Energy Efficiency and Industrial Automation Policies - Porter’s Five Forces Analysis

- Pricing Analysis

- Competition Ecosystem

- Factory Automation Penetration Mapping

- Machine Builder Ecosystem Analysis

- By Revenue, 2020-2025

- By Volume Shipment, 2020-2025

- By Average Selling Price, 2020-2025

- By Installed Base of Servo Systems, 2020-2025

- By Product Type (in Revenue %)

Torque Density

Precision Level

Encoder Resolution

Energy Efficiency

Motion Synchronization Capability - By Motor Type (in Revenue %)

Rotary Servo Motors

Linear Servo Motors

Brushless AC Servo Motors

Synchronous Servo Motors

Direct Drive Servo Motors - By Drive Type (in Revenue %)

Single-Axis Drive Adoption

Multi-Axis Synchronization

Industrial Ethernet Compatibility

Digital Control Capability

Response Time Efficiency - By Voltage Range (in Revenue %)

Load Handling Capacity

Industrial Compatibility

Power Consumption

Operational Stability - By Power Capacity (in Revenue %)

Below 1 kW

1–5 kW

5–15 kW

Above 15 kW - By Communication Protocol (in Revenue %)

EtherCAT Integration

PROFINET Adoption

Modbus Connectivity

EtherNet/IP Compatibility

CC-Link IE Usage - By Application (in Revenue %)

Precision Positioning Requirement

Cycle Time Optimization

Automation Intensity

Robotics Integration

Machine Throughput Efficiency - By Industrial Vertical (in Revenue %)

Material Handling

Machine Tool Industry

Packaging Machinery

Plastics and Injection Molding

Textile Industry

Pharmaceuticals

Food and Beverage Processing

HVAC Systems - By End User Type (in Revenue %)

OEM and Machine Builder Penetration

Factory Automation Maturity

Retrofit Adoption

Production Scale

System Integration Requirement - By Distribution Channel (in Revenue %)

Direct Sales Penetration

Authorized Distributor Reach

System Integrator Contribution

Industrial E-Commerce Penetration

Dealer Network Density - By Region (in Revenue %)

North India

South India

West India

East India

- Market Share Analysis of Major Players on the Basis of Revenue and Shipment Volume

- Cross Comparison Parameters (Company Overview, Product Portfolio Breadth, Servo Precision Capability, Industrial Vertical Presence, OEM Partnerships, Localization Capability, Communication Protocol Compatibility, Installed Base Strength, Manufacturing Footprint, Service and AMC Network, Distribution Reach, Motion Controller Integration, Pricing Positioning, Energy Efficiency Features, Innovation Pipeline, Strategic Collaborations)

- Competitive Benchmarking Matrix

- SWOT Analysis of Major Players

- Pricing Analysis by Power Rating and Torque Category

- Detailed Profiles of Major Companies

Siemens AG

Mitsubishi Electric Corporation

Yaskawa Electric Corporation

ABB Ltd.

Schneider Electric

Rockwell Automation

Delta Electronics

Omron Corporation

Panasonic Industry

Bosch Rexroth

Fuji Electric

Beckhoff Automation

Emerson Electric Co.

Fanuc Corporation

Nidec Corporation

- Industrial Procurement and Vendor Selection Analysis

- Factory Automation Budget Allocation Analysis

- Machine Builder Purchasing Behaviour

- Operational Pain Point Assessment

- Automation ROI and Productivity Analysis

- Industry-Wise Motion Control Adoption Mapping

- By Revenue, 2026-2032

- By Volume Shipment, 2026-2032

- By Average Selling Price, 2026-2032

- By Installed Base Growth, 2026-2032

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now