Download PDF

Download PDF Download PDF

Download PDFMarket Overview

India’s advanced materials market demonstrates strong industrial relevance, with a recent historical assessment valuing the market at approximately USD ~ based on consolidated industrial production data and manufacturing output statistics published by national manufacturing authorities and international trade databases. Demand is driven by expanding aerospace engineering programs, semiconductor manufacturing, renewable energy equipment production, automotive lightweighting technologies, and high-performance industrial infrastructure materials used across power generation, electronics fabrication, and chemical processing sectors.

Dominance within the market is strongly associated with large industrial manufacturing clusters located in Bengaluru, Hyderabad, Chennai, Pune, Ahmedabad, and Mumbai where aerospace engineering firms, semiconductor research centers, automotive production facilities, and advanced chemical manufacturing ecosystems operate. These cities host dense networks of research laboratories, industrial parks, and technology startups developing composites, ceramics, advanced polymers, and electronic materials that support high-performance manufacturing supply chains serving domestic industrial demand and global export markets.

Market Segmentation

By Product Type

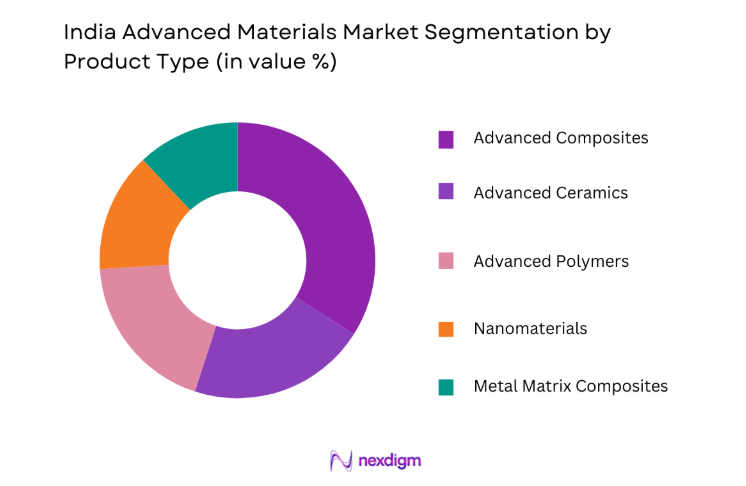

India Advanced Materials Market is segmented by product type into advanced composites, advanced ceramics, advanced polymers, nanomaterials, and metal matrix composites. Recently, advanced composites have a dominant market share due to strong demand from aerospace manufacturing, automotive lightweighting technologies, and wind turbine blade production across renewable energy infrastructure projects. Composite materials provide high strength-to-weight ratios, corrosion resistance, and structural durability that significantly improve performance in aviation components, defense equipment, and electric vehicle structures. Domestic aerospace programs, wind energy installations, and automotive component manufacturers increasingly rely on carbon fiber reinforced composites and glass fiber composites for structural engineering applications, strengthening the dominant demand position of advanced composite materials within India’s evolving advanced materials manufacturing ecosystem.

By End-Use Industry

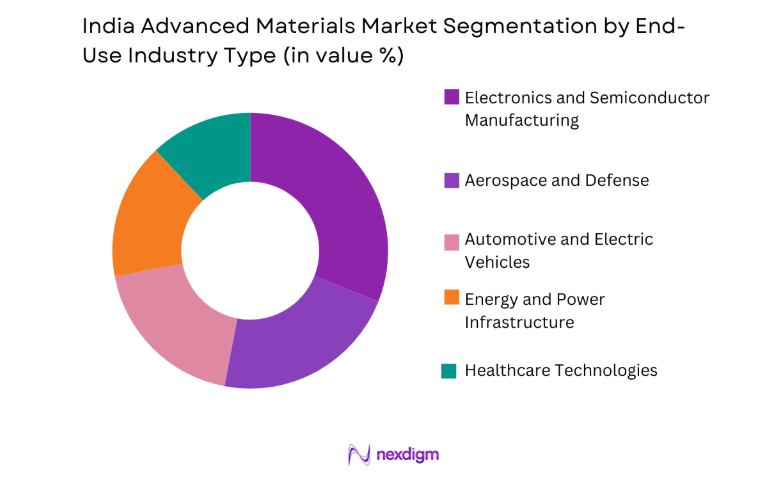

India Advanced Materials Market is segmented by end-use industry into aerospace and defense, electronics and semiconductor manufacturing, automotive and electric vehicles, energy and power infrastructure, and healthcare technologies. Recently, electronics and semiconductor manufacturing has a dominant market share due to the rapid expansion of semiconductor fabrication facilities, electronics component manufacturing clusters, and government supported semiconductor production programs. Advanced materials such as silicon wafers, gallium nitride substrates, specialty ceramics, and nano engineered conductive materials are essential for integrated circuit fabrication and high performance electronics. Increasing domestic smartphone assembly, semiconductor packaging units, and consumer electronics manufacturing plants significantly increase the consumption of advanced materials across semiconductor and electronic component supply chains.

Competitive Landscape

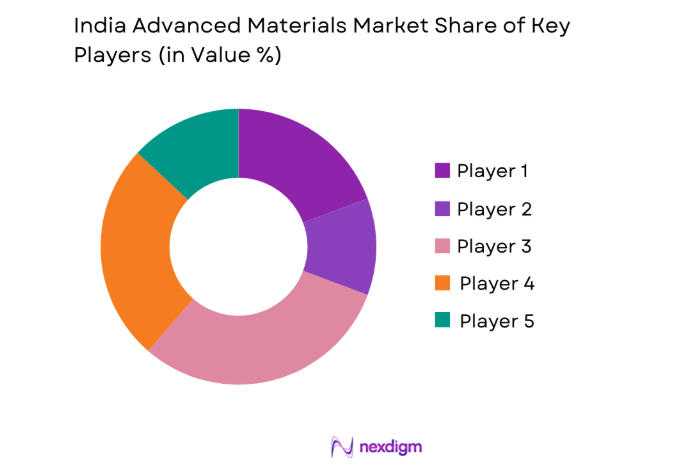

The India Advanced Materials Market exhibits a moderately consolidated structure where multinational specialty material producers operate alongside domestic advanced material manufacturers and research-driven technology companies. Global corporations maintain technological leadership in high-performance composites, specialty ceramics, semiconductor materials, and advanced polymers while domestic companies expand manufacturing capacities supported by national industrial policies encouraging local production of high value engineering materials. Strategic collaborations between research institutes, aerospace manufacturers, and electronics companies accelerate innovation across nanomaterials, semiconductor substrates, and lightweight structural composites.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Advanced Materials Capability |

| Tata Advanced Materials | 1990 | Bengaluru | ~ | ~ | ~ | ~ | ~ |

| Reliance Industries Advanced Materials | 1973 | Mumbai | ~ | ~ | ~ | ~ | ~ |

| 3M India | 1987 | Bengaluru | ~ | ~ | ~ | ~ | ~ |

| Saint Gobain India | 1996 | Chennai | ~ | ~ | ~ | ~ | ~ |

| Hindalco Industries | 1958 | Mumbai | ~ | ~ | ~ | ~ | ~ |

India Advanced Materials Market Analysis

Growth Drivers

Expansion of Semiconductor Manufacturing and Electronics Production Infrastructure

Rapid expansion of semiconductor manufacturing facilities and electronics production clusters significantly increases demand for advanced materials used in wafer fabrication packaging technologies and high performance electronic components across domestic manufacturing ecosystems. Semiconductor fabrication plants require specialized materials including ultra pure silicon wafers gallium nitride substrates advanced ceramics and nano engineered conductive materials that enable high precision electronic component production. Government initiatives supporting semiconductor manufacturing investments encourage global technology companies to establish fabrication facilities that depend heavily on advanced materials supply chains. Consumer electronics production including smartphones telecommunications equipment and digital infrastructure hardware also requires advanced polymers thermal interface materials and specialty ceramics. Domestic electronics manufacturing expansion strengthens demand for high performance materials used in printed circuit boards semiconductor packaging and electronic heat management technologies. Industrial automation robotics and artificial intelligence computing systems further increase consumption of semiconductor materials and specialty electronic substrates used in high performance processors and sensors. Supply chain localization strategies adopted by electronics manufacturers increase the need for domestic advanced materials production capabilities capable of supporting semiconductor manufacturing infrastructure. These developments collectively position advanced materials as a foundational industrial input supporting India’s expanding electronics and semiconductor manufacturing ecosystem.

Rapid Growth of Renewable Energy Infrastructure and Electric Vehicle Manufacturing

Accelerating deployment of renewable energy infrastructure and electric vehicle manufacturing significantly increases industrial demand for advanced materials capable of improving efficiency durability and performance across modern energy technologies. Wind turbine blades require high strength composite materials capable of maintaining structural stability under continuous aerodynamic stress and environmental exposure. Solar photovoltaic modules incorporate advanced semiconductor materials engineered glass substrates and specialty coatings designed to enhance electricity generation efficiency and operational lifespan. Electric vehicle manufacturing increasingly depends on lightweight composite materials high performance battery materials and thermal management ceramics that support energy efficient transportation technologies. Automotive manufacturers adopt aluminum composites carbon fiber reinforced materials and advanced polymers to reduce vehicle weight and improve energy efficiency in electric mobility systems. Battery technologies used in electric vehicles and energy storage systems require advanced nanomaterials engineered cathode materials and electrolyte polymers capable of delivering higher energy density and longer lifecycle performance. Renewable energy infrastructure including grid scale battery storage power electronics and smart grid technologies also utilizes advanced semiconductor materials designed to manage high voltage electricity flows efficiently. These structural industrial transitions collectively generate strong demand for advanced materials supporting India’s energy transition and electric mobility ecosystem.

Market Challenges

High Capital Requirements for Advanced Materials Manufacturing Infrastructure

Establishing advanced materials manufacturing facilities requires substantial capital investment due to the sophisticated equipment research infrastructure and specialized production processes required for engineering high performance materials. Semiconductor substrate manufacturing ceramic processing composite fabrication and nanomaterial production require precision controlled manufacturing environments and expensive industrial equipment. Companies entering advanced materials production must invest heavily in research laboratories materials testing facilities and quality assurance systems to ensure product performance reliability. These capital intensive requirements create high entry barriers that limit participation of smaller manufacturing companies within the advanced materials supply chain. Industrial scale manufacturing of composites ceramics and semiconductor materials also requires advanced process automation and environmental control systems that significantly increase operational costs. Many domestic companies rely on imported equipment and technology licensing agreements that further increase capital expenditure during facility development phases. Financial risk associated with long development cycles and uncertain demand for emerging materials technologies also discourages large scale investment in advanced materials production. These structural cost barriers continue to challenge domestic manufacturers attempting to scale advanced materials production capacities across India’s industrial manufacturing ecosystem.

Limited Domestic Supply Chains for Specialized Raw Materials and Processing Technologies

The advanced materials industry relies on highly specialized raw materials chemical precursors and precision manufacturing technologies that are not always available through domestic supply chains. Semiconductor materials high purity metals specialty polymers and nano engineered compounds often require international sourcing due to limited domestic extraction and refining capabilities. Dependence on imported raw materials increases supply chain vulnerabilities when global trade disruptions affect material availability or pricing stability. Advanced materials manufacturing also requires proprietary processing technologies developed through extensive research and engineering expertise held by a limited number of global companies. Domestic manufacturers may face difficulties accessing specialized manufacturing knowledge or intellectual property necessary for producing high performance materials. Limited availability of advanced processing equipment and technical expertise further constrains large scale domestic production of specialty materials used in aerospace electronics and semiconductor manufacturing. These technological and supply chain limitations restrict rapid expansion of domestic advanced materials manufacturing capabilities. Overcoming these constraints requires long term investments in research infrastructure technology transfer programs and domestic supply chain development across the advanced materials ecosystem.

Opportunities

Development of Domestic Semiconductor and Electronics Supply Chain Ecosystems

Expansion of domestic semiconductor fabrication facilities and electronics manufacturing clusters creates substantial opportunities for advanced materials manufacturers capable of supplying specialized materials required for electronic component production. Semiconductor fabrication plants depend on ultra pure silicon wafers gallium nitride substrates advanced ceramics and high precision nanomaterials essential for integrated circuit manufacturing. Government supported semiconductor production programs encourage local sourcing of materials used in wafer fabrication packaging and electronic component assembly operations. Electronics manufacturers also require advanced polymers conductive nanomaterials and thermal management materials designed to support high performance computing systems telecommunications infrastructure and consumer electronics devices. Establishing domestic production capabilities for semiconductor grade materials can significantly reduce dependence on imported electronic materials while strengthening national technology supply chains. Research collaborations between universities technology institutes and manufacturing companies accelerate innovation in semiconductor materials engineering and nano scale electronic materials development. Emerging industries including artificial intelligence computing quantum electronics and high speed telecommunications networks further increase demand for specialized electronic materials. These developments create long term growth opportunities for advanced materials companies supplying semiconductor and electronics manufacturing ecosystems within India.

Expansion of Aerospace Manufacturing and Defense Technology Programs

Growth of domestic aerospace manufacturing capabilities and defense technology development programs significantly expands demand for advanced materials capable of meeting stringent engineering performance requirements. Aerospace structures require lightweight composite materials high temperature ceramics and advanced metal alloys capable of maintaining structural integrity under extreme operational conditions. Domestic aircraft manufacturing programs and defense equipment development initiatives increase industrial consumption of advanced structural materials used in aircraft fuselages propulsion systems and electronic defense equipment. Defense modernization programs also require advanced materials used in radar systems satellite components and unmanned aerial vehicle technologies supporting national security infrastructure. Aerospace research institutions collaborate with materials engineering companies to develop high performance composites and nano engineered coatings designed for aviation and space applications. Increasing participation of private aerospace manufacturing companies further strengthens demand for advanced materials used in aircraft assembly component manufacturing and defense equipment engineering. Export opportunities for aerospace components manufactured using advanced materials also encourage domestic manufacturers to expand material engineering capabilities. These developments create sustained opportunities for advanced materials companies participating in aerospace manufacturing and defense technology supply chains.

Future Outlook

The India Advanced Materials Market is expected to experience sustained industrial expansion driven by rapid growth in semiconductor manufacturing renewable energy infrastructure electric vehicle production and aerospace engineering industries. Technological advancements in nanomaterials advanced composites and semiconductor materials will significantly enhance the performance of modern industrial systems. Government initiatives promoting domestic manufacturing innovation and industrial research are likely to strengthen local production capabilities for advanced engineering materials. Increasing collaboration between technology companies research institutions and manufacturing firms will further accelerate the development of next generation advanced materials across multiple industrial sectors.

Major Players

- Tata Advanced Materials

- Reliance Industries

- Hindalco Industries

- 3M India

- Saint Gobain India

- BASF India

- Solvay

- Toray Industries

- Mitsubishi Chemical Group

- Hexcel Corporation

- Covestro

- Arkema

- Huntsman Corporation

- SGL Carbon

- Morgan Advanced Materials

Key Target Audience

- Aerospace manufacturing companies

- Semiconductor manufacturing firms

- Automotive and electric vehicle manufacturers

- Renewable energy equipment manufacturers

- Investments and venture capitalist firms

- Government and regulatory bodies

- Industrial materials manufacturers

Research Methodology

Step 1: Identification of Key Variables

Primary variables including advanced materials production capacity industrial demand drivers manufacturing clusters and material technology adoption across aerospace electronics and energy sectors are identified using industrial databases trade statistics and manufacturing policy reports.

Step 2: Market Analysis and Construction

Supply chain analysis industrial output statistics advanced materials consumption patterns and technology adoption trends are examined to construct the overall structure of the India Advanced Materials Market and its industrial ecosystem.

Step 3: Hypothesis Validation and Expert Consultation

Findings are validated through consultation with materials scientists semiconductor engineers aerospace manufacturers and industrial technology experts who provide insights into technological developments manufacturing demand and supply chain trends.

Step 4: Research Synthesis and Final Output

All validated insights industrial statistics and technological assessments are synthesized into a comprehensive market framework describing market structure segmentation competitive landscape and long term growth potential.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Expansion of Aerospace and Defense Manufacturing Programs

Increasing Demand for Lightweight Materials in Automotive Electrification

Growing Semiconductor and Electronics Manufacturing Ecosystem - Market Challenges

High Production Costs and Complex Manufacturing Processes

Limited Domestic Supply Chains for Specialized Raw Materials

Technology Transfer Restrictions and Intellectual Property Barriers - Market Opportunities

Expansion of Renewable Energy Infrastructure Requiring High Performance Materials

Rising Adoption of Nanomaterials in Electronics and Medical Applications

Growth of Electric Vehicle Manufacturing Demanding Lightweight Structural Materials - Trends

Increasing Integration of Nanotechnology in Industrial Materials Engineering

Growing Use of Advanced Composites in Aerospace Structural Components - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Advanced Composite Materials

High Performance Polymers

Advanced Ceramics

Nanomaterials

Metal Matrix Composites - By Platform Type (In Value%)

Aerospace Platforms

Automotive Platforms

Energy & Power Platforms

Electronics & Semiconductor Platforms - By Fitment Type (In Value%)

Structural Components

Thermal Protection Systems

Electronic Components

Industrial Equipment Components - By End User Segment (In Value%)

Aerospace and Defense Industry

Automotive and Transportation Industry

Energy and Industrial Manufacturing

- Market Share Analysis

- Cross Comparison Parameters (Material Type, Application Sector, Manufacturing Technology, Performance Characteristics, Supply Chain Integration, Pricing Structure, Innovation Capability)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Reliance Industries Limited

Tata Advanced Materials Limited

Aditya Birla Advanced Materials

Hindustan Aeronautics Limited

BASF India

3M India

Solvay Speciality Polymers India

Hexcel Corporation

Toray Industries

Huntsman Corporation

DuPont

Dow Inc

Saint Gobain India

SGL Carbon SE

Teijin Limited

- Aerospace Manufacturers Increasing Use of Lightweight Composite Materials

- Automotive OEMs Adopting Advanced Materials for Electric Vehicle Efficiency

- Energy Companies Utilizing Advanced Materials in High Temperature Industrial Systems

- Electronics Manufacturers Deploying Nanomaterials in Semiconductor Devices

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now