Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The India Agricultural Engine market recorded a value of USD ~ billion based on a recent historical assessment of off-highway engine production and agricultural equipment demand. Market scale is driven by mechanization programs, irrigation pump deployment, and tractorization across small and mid-sized farms. Engine replacement demand and localized manufacturing expansion also contribute significantly. Rising equipment financing access and diesel engine lifecycle replacement cycles sustain consistent procurement volumes across agricultural applications nationwide.

Demand concentration is highest across northern and western agricultural belts including Punjab, Haryana, Uttar Pradesh, Maharashtra, and Gujarat, where mechanized farming intensity and irrigation density remain structurally high. Southern states such as Tamil Nadu and Karnataka also exhibit strong engine utilization due to diversified cropping and pump-based irrigation systems. Regional dominance reflects higher farm mechanization adoption, established tractor manufacturing clusters, rural credit penetration, and dense dealer service ecosystems supporting agricultural engine deployment.

Market Segmentation

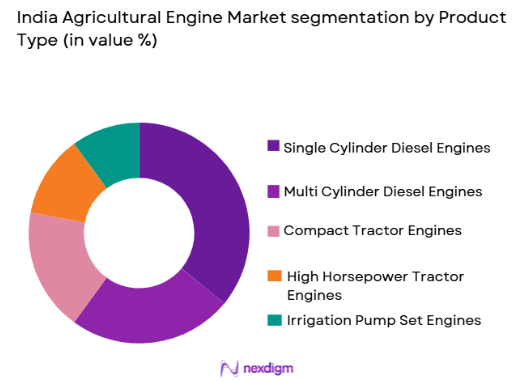

By Product Type

India Agricultural Engine market is segmented by product type into single cylinder diesel engines, multi cylinder diesel engines, compact tractor engines, high horsepower tractor engines, and irrigation pump set engines. Recently, single cylinder diesel engines has a dominant market share due to factors such as widespread irrigation pump usage, affordability for smallholder farmers, ease of maintenance, and rural service familiarity. These engines power both stationary and mobile farm applications across diverse crop systems. Their simple mechanical architecture supports long operational life under variable fuel quality conditions. Strong domestic manufacturing presence and subsidy alignment further reinforce procurement preference among small and marginal agricultural users.

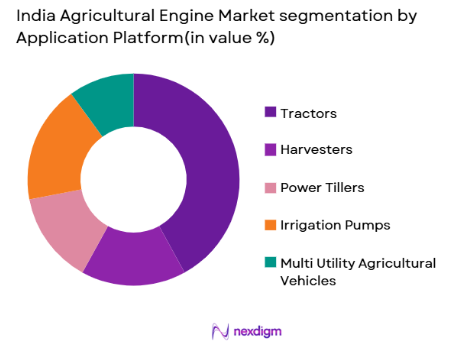

By Application

India Agricultural Engine market is segmented by application platform into tractors, harvesters, power tillers, irrigation pumps, and multi utility agricultural vehicles. Recently, tractors has a dominant market share due to factors such as multi-functional farm use, year-round utilization, rising farm mechanization, and government support programs. Tractor-mounted engines serve ploughing, hauling, sowing, and transport roles across varied terrain conditions. Expanding rural contracting services also increase tractor engine utilization intensity. Continuous horsepower upgrades and replacement cycles maintain strong procurement demand compared with seasonal equipment platforms such as harvesters and tillers.

Competitive Landscape

The India Agricultural Engine market exhibits moderate consolidation with strong domestic manufacturers complemented by multinational engine technology providers. Large players maintain competitive advantage through localized production, dealer networks, and integration with tractor OEM ecosystems. Technology differentiation centers on fuel efficiency, durability, and emission compliance capability. Regional manufacturing clusters and aftersales service infrastructure significantly influence competitive positioning. Strategic partnerships with agricultural equipment manufacturers further reinforce market presence and distribution reach across rural markets.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Engine Power Range |

| Kirloskar Oil Engines | 1946 | Pune, India | ~ | ~ | ~ | ~ | ~ |

| Mahindra Powerol | 2001 | Pune, India | ~ | ~ | ~ | ~ | ~ |

| Greaves Cotton | 1859 | Mumbai, India | ~ | ~ | ~ | ~ | ~ |

| Cummins India | 1962 | Pune, India | ~ | ~ | ~ | ~ | ~ |

| Escorts Kubota | 1944 | Faridabad, India | ~ | ~ | ~ | ~ | ~ |

India Agricultural Engine Market Analysis

Growth Drivers

Rising Farm Mechanization Across Smallholder Agriculture

Mechanization expansion across smallholder farming systems is a primary structural driver for agricultural engine demand in India. Fragmented landholdings historically limited equipment adoption, but increasing labor scarcity and wage escalation have altered cost economics in favor of mechanized solutions. Government mechanization schemes and rural financing programs have improved access to tractors, tillers, and irrigation engines among small farmers. Custom hiring centers enable shared use of engine-powered machinery, increasing utilization and replacement cycles. Expanding horticulture and commercial cropping systems require reliable mechanized operations for planting, irrigation, and post-harvest handling. Mechanization also supports climate resilience by enabling timely farm operations under uncertain rainfall conditions. Domestic manufacturing has reduced acquisition cost and improved spare parts availability across rural markets. Tractorization intensity growth across northern and central agricultural belts has accelerated engine procurement. Rising adoption of pump-based irrigation further increases stationary engine deployment. These structural shifts collectively sustain long-term growth momentum for agricultural engines.

Expansion of Irrigation Infrastructure and Pump Engine Deployment

Expansion of irrigation infrastructure significantly drives demand for agricultural engines powering pump sets across groundwater and surface irrigation systems. Irrigation intensity growth enables multi-cropping and higher productivity, increasing reliance on engine-driven water extraction technologies. Diesel pump engines remain essential in regions with unreliable grid power or remote field locations lacking electrification. Government irrigation schemes and watershed programs expand cultivated command areas requiring pump equipment installation. Replacement cycles remain high due to continuous seasonal operation and exposure to harsh field conditions. Farmers prefer robust diesel engines capable of operating with variable fuel quality and minimal maintenance support. Regional groundwater irrigation dominance across western and northern states sustains large stationary engine populations. Expansion of micro-irrigation adoption also requires engine-powered water pressurization systems. Rising demand for assured irrigation amid climate variability reinforces engine procurement. These infrastructure and agronomic factors collectively sustain strong agricultural engine market expansion.

Market Challenges

Price Sensitivity and Capital Constraints Among Small Farmers

Agricultural engine adoption in India is strongly influenced by affordability constraints faced by small and marginal farmers who represent the majority of agricultural holdings. Limited disposable income and volatile farm earnings create high sensitivity to upfront equipment cost. Even subsidized mechanization schemes often require co-payment beyond the financial capacity of many farmers. Access to institutional credit remains uneven across regions, restricting mechanization investment potential. Informal financing channels carry high interest burdens, discouraging engine procurement. Farmers frequently defer replacement of aging engines due to cost pressures, extending lifecycle beyond optimal efficiency. Seasonal cash flows linked to crop harvest cycles further constrain purchasing decisions. Price competition among manufacturers compresses margins and limits technological upgrades. Low cost imports and informal refurbishing markets also disrupt formal engine sales. These structural financial barriers continue to challenge agricultural engine market penetration.

Emission Compliance Transition and Technology Cost Pressures

Implementation of stricter emission norms for off-highway diesel engines increases design complexity and manufacturing cost across agricultural engine platforms. Compliance requires advanced fuel injection systems, improved combustion efficiency, and emission control components. These technology upgrades raise engine price levels beyond affordability thresholds of price-sensitive agricultural users. Smaller manufacturers face capital constraints in adopting emission-compliant production technologies. Supply chain adaptation for compliant components also increases production cost volatility. Farmers often prioritize durability and repairability over emission performance, creating adoption resistance. Transition timelines require parallel production of legacy and compliant engines, raising operational burden. Regulatory uncertainty and phased implementation complicate product planning for manufacturers. Dealer networks require training and diagnostic capability upgrades for compliant engines. These technological and regulatory cost pressures present significant challenges to agricultural engine market growth.

Opportunities

Adoption of Fuel Efficient and Low Emission Agricultural Engines

toward fuel efficient and low emission agricultural engines presents a major technological opportunity in the India Agricultural Engine market. Rising diesel cost sensitivity among farmers increases demand for engines delivering lower fuel consumption per operational hour. Manufacturers are investing in optimized combustion design and electronic fuel systems to improve efficiency. Emission-compliant engines also support policy alignment with environmental sustainability goals in agriculture. Improved fuel economy reduces lifetime operating cost, strengthening value proposition despite higher upfront price. Government incentives for cleaner agricultural technologies can accelerate adoption across mechanization programs. Export potential also increases for manufacturers producing compliant engines aligned with global standards. Precision farming equipment integration further benefits from efficient engine performance characteristics. Dealer networks can leverage efficiency savings messaging to promote upgrades. These efficiency and environmental factors create long-term growth opportunities.

Growth of Custom Hiring and Agricultural Service Mechanization Models

Expansion of custom hiring and farm mechanization service models offers substantial opportunity for agricultural engine demand growth. Smallholder farmers increasingly access mechanized operations through rental service providers rather than direct equipment ownership. Service operators maintain fleets of tractors, tillers, and pump engines with high utilization intensity. Higher operating hours accelerate engine wear and replacement cycles compared with individual farm ownership. Government promotion of custom hiring centers supports rural mechanization accessibility. Service providers prefer durable engines with lower downtime to maximize asset productivity. Fleet-based procurement creates bulk purchasing demand for manufacturers. Mechanization service entrepreneurship is expanding across rural regions with rising labor shortages. Digital platforms enabling farm equipment rental further stimulate mechanization service penetration. These structural shifts toward shared mechanization models significantly expand agricultural engine market opportunity.

Future Outlook

The India Agricultural Engine market is expected to experience steady expansion driven by sustained mechanization adoption, irrigation growth, and rural equipment financing penetration. Technological transition toward fuel-efficient and emission-compliant engines will reshape product portfolios. Increasing custom hiring models and higher horsepower equipment adoption will further strengthen demand. Localization of engine manufacturing and policy support for farm productivity will reinforce long-term growth momentum across agricultural mechanization ecosystems.

Major Players

- Kirloskar Oil Engines

- Mahindra Powerol

- Greaves Cotton

- Cummins India

- Escorts Kubota

- Tata Motors Industrial Engines

- Ashok Leyland Engines

- Sonalika International Tractors Engines Division

- HMT Machine Tools Engines

- VE Commercial Vehicles Powertrain

- Yanmar India

- Kubota Agricultural Engines India

- Perkins India

- Deutz Engines India

- Honda India Power Products

Key Target Audience

- Agricultural equipment manufacturers

- Tractor OEM companies

- Irrigation pump manufacturers

- Agricultural machinery distributors

- Farm mechanization service providers

- Rural financing institutions

- Government and regulatory bodies

- Investments and venture capitalist firms

Research Methodology

Step 1: Identification of Key Variables

Key variables including agricultural mechanization rates, tractor population, irrigation pump penetration, engine replacement cycles, and rural financing access were identified to define market structure and demand drivers.

Step 2: Market Analysis and Construction

Supply-side production data and demand-side agricultural equipment deployment indicators were synthesized to construct market size, segmentation structure, and competitive positioning across engine categories and platforms.

Step 3: Hypothesis Validation and Expert Consultation

Industry expert inputs from manufacturers, distributors, and agricultural mechanization specialists validated assumptions regarding adoption patterns, technology transition, and regional demand concentration dynamics.

Step 4: Research Synthesis and Final Output

All quantitative and qualitative insights were integrated into a structured analytical framework to produce final market sizing, segmentation distribution, competitive analysis, and forward-looking outlook assessment.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Mechanization growth in small and mid sized farms

Rising demand for higher horsepower tractors

Expansion of irrigation infrastructure

Government subsidy support for farm equipment

Replacement demand for aging diesel engines - Market Challenges

Price sensitivity among small farmers

Fragmented rural distribution networks

Emission compliance cost pressures

Seasonal demand volatility

Dependence on monsoon driven farm income - Market Opportunities

Adoption of fuel efficient and low emission engines

Growth in custom hiring agricultural services

Expansion of agri mechanization schemes - Trends

Shift toward higher horsepower mechanization

Integration of electronic fuel systems

Demand for durable low maintenance engines

Growth of aftermarket engine replacement

Localization of engine manufacturing - Government Regulations & Defense Policy

Bharat Stage emission norms for off road engines

Farm mechanization subsidy programs

Rural equipment financing initiatives

SWOT Analysis

Stakeholder and Ecosystem Analysis

Porter’s Five Forces Analysis

Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Single Cylinder Diesel Engines

Multi Cylinder Diesel Engines

Compact Tractor Engines

High Horsepower Tractor Engines

Irrigation Pump Set Engines - By Platform Type (In Value%)

Tractors

Harvesters

Power Tillers

Irrigation Pumps

Multi Utility Agricultural Vehicles - By Fitment Type (In Value%)

OEM Integrated Engines

Aftermarket Replacement Engines

Retrofit Engine Kits

Stationary Engine Installations

Mobile Equipment Engines - By EndUser Segment (In Value%)

Smallholder Farmers

Commercial Farming Enterprises

Agricultural Contractors

Cooperative Farming Societies

Government and Rural Agencies - By Procurement Channel (In Value%)

OEM Direct Procurement

Authorized Dealer Networks

Rural Distribution Retailers

Government Subsidy Programs

Aftermarket Distributors - By Material / Technology (in Value %)

Mechanical Fuel Injection Engines

Electronic Fuel Injection Engines

Turbocharged Diesel Engines

Emission Compliant Engines

Alternative Fuel Compatible Engines

- Market structure and competitive positioning

- Market share snapshot of major players

- Cross Comparison Parameters (Engine Power Range, Fuel Efficiency, Emission Compliance Level, Durability Lifecycle, OEM Integration Capability, Price Positioning, Distribution Reach, Aftermarket Support, Technology Integration, Manufacturing Localization)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

Kirloskar Oil Engines

Mahindra Powerol

Greaves Cotton

Cummins India

Escorts Kubota

Tata Motors Industrial Engines

Ashok Leyland Engines

Sonalika International Tractors Engines Division

HMT Machine Tools Engines

VE Commercial Vehicles Powertrain

Briggs and Stratton India

Yanmar India

Kubota Agricultural Engines India

Perkins India

Deutz Engines India

- Smallholder farmers prioritizing affordability and reliability

- Commercial farms adopting high horsepower engines

- Contractors driving utilization intensive demand

- Government programs influencing equipment adoption

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now