Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The India Agricultural Sensors & Telematics market has reached a market size of approximately USD ~ billion, based on a recent historical assessment. The market has been driven by the growing demand for precision agriculture, advancements in IoT, and the increasing need for real-time data analytics to improve crop yield and efficiency. The adoption of agricultural sensors and telematics systems, such as weather monitoring sensors, soil moisture sensors, and GPS systems, is on the rise, with a focus on enhancing farm management practices and reducing resource wastage. These technologies enable farmers to optimize irrigation, track livestock, monitor soil health, and predict weather patterns, contributing to overall cost reduction and enhanced productivity.

The dominant players in the market are primarily concentrated in regions with strong agricultural infrastructure, such as Maharashtra, Punjab, Uttar Pradesh, and Haryana. These states have a significant share in the agricultural production of the country, with a high adoption rate of agricultural technologies. Moreover, the influence of governmental schemes promoting smart farming solutions has encouraged widespread adoption in these regions. The increased availability of data-driven agricultural solutions and collaborations between tech firms and government agencies have made these regions the key hubs for market growth. Additionally, rising awareness among farmers about the benefits of using sensors and telematics in daily farming practices has played a vital role in driving the market’s expansion.

Market Segmentation

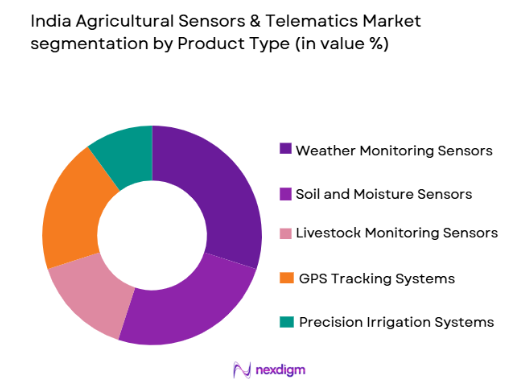

By Product Type

India Agricultural Sensors & Telematics market is segmented by product type into weather monitoring sensors, soil and moisture sensors, livestock monitoring sensors, GPS tracking systems, and precision irrigation systems. Recently, weather monitoring sensors have a dominant market share due to factors such as the increasing need for climate-resilient agriculture, which enables farmers to make data-driven decisions based on real-time weather data. The growing frequency of unpredictable weather patterns, such as droughts and floods, has emphasized the importance of precise weather data to mitigate risks. This product segment’s growing adoption is also attributed to the development of affordable, easy-to-use devices that are tailored for small-scale farmers. The government’s initiatives to boost climate-smart agriculture and the expansion of agri-tech solutions further drive the widespread use of weather monitoring sensors across regions.

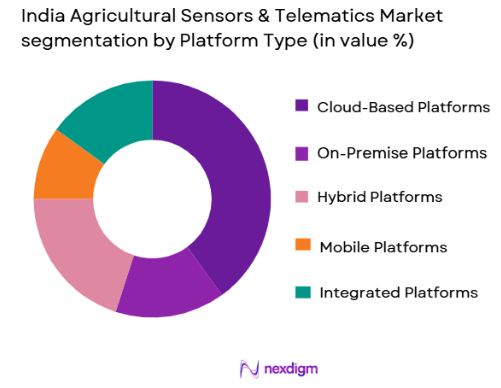

By Platform Type

India Agricultural Sensors & Telematics market is segmented by platform type into cloud-based platforms, on-premise platforms, hybrid platforms, mobile platforms, and integrated platforms. Among these, cloud-based platforms dominate the market due to their ability to offer scalable solutions and enable farmers to access data remotely. These platforms allow for the seamless integration of various sensor technologies, making them highly flexible and easy to adopt, especially for small to medium-sized farms. The increasing availability of affordable cloud computing resources and the growing number of internet users in rural areas are propelling the adoption of cloud-based platforms. Furthermore, the integration of big data and artificial intelligence into cloud platforms facilitates enhanced farm management decisions and predictive analytics, which are vital for improving farm efficiency and profitability.

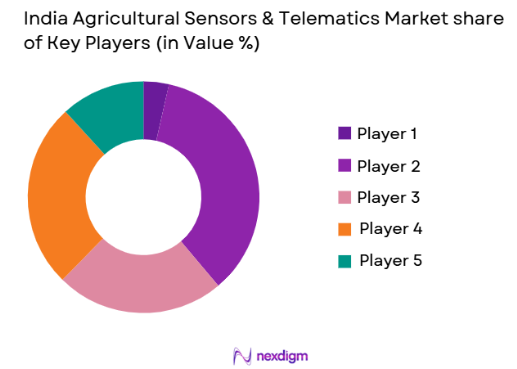

Competitive Landscape

The competitive landscape of the India Agricultural Sensors & Telematics market is highly dynamic, with both local and international players striving to gain market share through innovative product offerings and strategic partnerships. The market is experiencing a trend of consolidation, with major players collaborating with tech startups to enhance their technological capabilities and expand market reach. These collaborations are enabling the integration of advanced technologies such as AI, machine learning, and IoT into agricultural applications. Furthermore, the increasing role of government policies promoting smart agriculture is likely to fuel further competition in the coming years.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD Billion) | Additional Parameter |

| Trimble | 1978 | USA | ~ | ~ | ~ | ~ | ~ |

| John Deere | 1837 | USA | ~ | ~ | ~ | ~ | ~ |

| AG Leader Technology | 1992 | USA | ~ | ~ | ~ | ~ | ~ |

| Raven Industries | 1956 | USA | ~ | ~ | ~ | ~ | ~ |

| Bosch | 1886 | Germany | ~ | ~ | ~ | ~ | ~ |

India Agricultural Sensors & Telematics Market Analysis

Growth Drivers

Technological Advancements in IoT

The increasing adoption of IoT-enabled agricultural sensors is driving market growth. IoT technology allows for the integration of sensors into various farm management systems, providing farmers with real-time data that enables them to monitor soil conditions, weather patterns, and crop health. The advancement in wireless sensor networks has made these technologies more affordable and accessible, especially for small-scale farmers. The ability to collect vast amounts of data from different farm processes allows for improved decision-making, leading to better resource utilization and higher crop yields. Furthermore, the integration of machine learning and AI into IoT systems has enhanced predictive capabilities, which aid farmers in anticipating potential issues such as pest invasions, disease outbreaks, and adverse weather events. This leads to more efficient use of pesticides, fertilizers, and water, reducing operational costs while increasing profitability. The government’s push for smart farming solutions also contributes to the growth of IoT-based systems in the Indian agricultural sector.

Government Initiatives for Smart Farming

Government schemes like the Pradhan Mantri Krishi Sinchayee Yojana (PMKSY) and the National Mission on Agricultural Extension and Technology (NMAET) have been instrumental in promoting the adoption of smart farming technologies. These initiatives offer financial support and incentives for farmers to adopt modern technologies, such as agricultural sensors and telematics systems. Government support in the form of subsidies for precision farming equipment and the promotion of digital agriculture through mobile applications is also encouraging farmers to adopt these technologies. Additionally, the government’s focus on digital infrastructure development, such as broadband connectivity and mobile networks in rural areas, is improving the reach of agricultural IoT solutions. These initiatives are creating a conducive environment for the widespread adoption of agricultural sensors and telematics systems, thereby driving market growth. As these programs continue to gain momentum, they are expected to lead to significant improvements in farming practices across the country.

Market Challenges

High Initial Cost of Technology

Despite the increasing demand for agricultural sensors and telematics, the high initial cost of implementing these technologies remains a significant barrier, especially for small-scale farmers. The cost of acquiring sensors, installation of telematics systems, and integration with existing farm management infrastructure can be prohibitive for farmers with limited capital. Although the cost of technology is gradually decreasing with advancements in manufacturing processes and economies of scale, it still represents a substantial investment. Furthermore, the lack of financing options for farmers to adopt these technologies in rural areas adds to the challenge. Many farmers are hesitant to invest in these systems due to their perceived high upfront cost and the uncertainty of returns in the short term. To overcome this challenge, the government and private players must develop affordable financing models that can ease the financial burden on farmers, making smart farming technologies more accessible to a broader audience.

Lack of Technical Expertise in Rural Areas

The adoption of agricultural sensors and telematics systems requires a certain level of technical expertise, which many farmers in rural areas lack. While urban areas are increasingly embracing digital solutions, rural regions face challenges related to the digital literacy of farmers. This lack of technical know-how hinders the effective utilization of agricultural technologies and impedes the widespread adoption of these systems. Training and capacity-building programs are essential to address this issue, but the availability of such programs is limited, and many farmers are unable to access them. As a result, even if the technologies are available, farmers may struggle to fully integrate and utilize them in their daily operations. To address this challenge, there is a need for more comprehensive training programs that focus on educating farmers about the benefits and usage of agricultural sensors and telematics systems. Additionally, collaboration with local agricultural extension services can help improve the adoption rate of these technologies.

Opportunities

Integration of AI and Machine Learning in Agricultural Sensors

The integration of AI and machine learning into agricultural sensors presents a significant opportunity for market growth. AI-powered sensors can analyze real-time data and provide predictive insights that help farmers make informed decisions. For instance, AI can predict crop diseases, pest infestations, and weather patterns, allowing farmers to take proactive measures. By leveraging machine learning algorithms, these systems can continually improve their accuracy and efficiency, offering more reliable and actionable insights over time. This integration enhances the overall value proposition of agricultural sensors and telematics systems, making them indispensable tools for modern farming. Moreover, the ability to automate decision-making based on AI analysis will significantly reduce the time and labor involved in traditional farming practices. As AI and machine learning technologies continue to evolve, their applications in agriculture will expand, leading to greater productivity, sustainability, and profitability for farmers.

Rise of Precision Agriculture in Developing Markets

Precision agriculture is rapidly gaining traction in developing markets like India due to the increasing demand for sustainable farming practices. Precision agriculture utilizes advanced technologies, such as sensors, GPS, and remote sensing, to optimize farming operations and reduce resource usage. This approach allows farmers to use fertilizers, pesticides, and water more efficiently, minimizing waste and environmental impact. The rise of precision agriculture in India is being driven by several factors, including the growing need to address food security concerns, improve yield per acre, and mitigate the effects of climate change. Additionally, the government’s push for sustainable farming practices and the increasing availability of affordable precision agriculture solutions are encouraging farmers to adopt these technologies. The growing awareness of the benefits of precision farming is expected to lead to a significant increase in the adoption of agricultural sensors and telematics systems, opening up new growth opportunities for market players.

Future Outlook

The India Agricultural Sensors & Telematics market is poised for significant growth over the next five years, driven by advancements in IoT, AI, and machine learning technologies. Increased government support for smart farming and sustainable agriculture practices will continue to boost adoption rates, especially in rural areas. Technological innovations will lead to more affordable and efficient solutions, making agricultural sensors and telematics systems accessible to a broader base of farmers. The market is also expected to see a rise in the adoption of cloud-based platforms and mobile applications, enhancing data accessibility and decision-making capabilities for farmers. Additionally, growing awareness about the environmental impact of traditional farming methods and the need for sustainable practices will further drive market demand. With these trends in mind, the market is set to experience a period of rapid technological advancements and increased investments, positioning India as a key player in the global agricultural technology landscape.

Major Players

- Trimble

- John Deere

- AG Leader Technology

- Raven Industries

- Bosch

- Hexagon Agriculture

- CNH Industrial

- Topcon Positioning Systems

- Yara International

- Caterpillar

- Case IH

- Kubota Corporation

- Mahindra & Mahindra

- ZedX Inc.

- Deere & Company

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Agricultural equipment manufacturers

- Agri-tech startups

- Technology solution providers

- Retailers of farm equipment

- Large-scale farms

- Precision agriculture service providers

Research Methodology

Step 1: Identification of Key Variables

The first step involves identifying key market variables such as product types, technology trends, consumer preferences, and regional dynamics that drive the market.

Step 2: Market Analysis and Construction

This step includes the analysis of historical market data and construction of the market model based on factors such as market trends, growth rates, and key drivers.

Step 3: Hypothesis Validation and Expert Consultation

In this phase, expert consultations and surveys are conducted to validate the market hypotheses and ensure that all assumptions align with real-world data.

Step 4: Research Synthesis and Final Output

The final output synthesizes all findings from market analysis, expert feedback, and data verification to generate actionable insights for the report.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising Adoption of Precision Agriculture

Government Support for Smart Farming Technologies

Technological Advancements in IoT and Sensors

Growing Demand for Sustainable Farming Solutions

Increase in Agricultural Automation - Market Challenges

High Initial Investment for Implementation

Lack of Technical Skills in Rural Areas

Limited Connectivity in Remote Areas

Data Security and Privacy Concerns

Inconsistent Standards for Agricultural Data - Market Opportunities

Expansion of IoT Integration in Agriculture

Partnerships with Tech Startups for Innovation

Rising Demand for Data-Driven Decision Making - Trends

Growing Use of Autonomous Agricultural Machinery

Integration of AI and Machine Learning in Farm Management

Focus on Sustainable and Eco-Friendly Farming Practices

Increased Connectivity with Rural Farming Communities

Rise of Digital Platforms for Farm-to-Market Solutions - Government Regulations & Defense Policy

Support for Digital Transformation in Agriculture

Regulations on Precision Farming Practices

Policies for Data Sharing and Standardization - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Precision Agriculture Sensors

Telematics and Fleet Management Systems

Soil and Moisture Sensors

Livestock Monitoring Sensors

Weather Monitoring Systems - By Platform Type (In Value%)

Cloud-Based Platforms

On-Premise Platforms

Hybrid Platforms

Mobile Platforms

Integrated Platforms - By Fitment Type (In Value%)

Standalone Systems

Embedded Systems

Hybrid Systems

Modular Systems

Integrated Systems - By EndUser Segment (In Value%)

Farmers and Agricultural Cooperatives

Agricultural Equipment Manufacturers

Agriculture Technology Providers

Research and Development Institutes

Government Agencies - By Procurement Channel (In Value%)

Direct Procurement

Third-Party Distributors

Online Bidding Platforms

Government Tenders

Private Sector Procurement - By Material / Technology (In Value%)

Wireless Communication Technology

IoT-based Sensors

Satellite and GPS Technology

Machine Learning and AI Integration

Big Data Analytics

- Market structure and competitive positioning

- Market share snapshot of major players

- Cross Comparison Parameters (System Type, Platform Type, Procurement Channel, EndUser Segment, Fitment Type, Material/Technology, Growth Drivers, Challenges, Opportunities, Trends)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

Trimble

John Deere

Ag Leader Technology

AG Leader Technology

Monsanto

Raven Industries

Topcon Positioning Systems

Hexagon Agriculture

Deere & Company

DigiFarm

Trelleborg

Yokogawa Electric Corporation

Kubota Corporation

Sick AG

MapShots, Inc.

- Farmers’ Increasing Need for Real-Time Data

- Government Agencies Driving Regulatory Changes

- Agri-Tech Startups Enhancing Innovation

- Research Institutions Promoting Sustainable Solutions

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now