Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The India Agricultural Tractor market has been experiencing robust growth driven by a surge in demand for mechanized farming equipment. Based on a recent historical assessment, the market size is valued at approximately USD ~ billion. Key drivers of this growth include the increasing demand for high-efficiency tractors, expanding agricultural mechanization, and government support in the form of subsidies and incentives. The market’s expansion is primarily attributed to the modernization of the agricultural sector and the need for greater productivity in India’s vast farming regions.

India’s dominance in the agricultural tractor market is primarily concentrated in states such as Punjab, Haryana, Uttar Pradesh, and Maharashtra, where large-scale farming and mechanization are prevalent. These regions are marked by favorable climatic conditions for agriculture, government support programs, and the presence of well-established tractor manufacturing infrastructure. The rising adoption of tractors in smaller, less mechanized regions is also contributing to India’s leadership in this market. The dominance of these regions stems from their significant contributions to India’s agricultural output and the increasing trend toward mechanized farming practices.

Market Segmentation

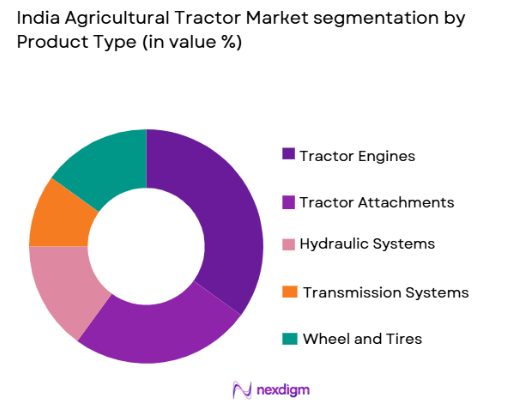

By Product Type

India Agricultural Tractor market is segmented by product type into tractor engines, tractor attachments, hydraulic systems, transmission systems, and wheel and tires. Recently, tractor engines have a dominant market share due to their critical role in the overall performance and efficiency of agricultural tractors. As tractors become more powerful, efficient, and versatile, demand for high-performance engines continues to rise, driving innovation and fueling market growth. Tractor engines are at the heart of technological advancements in tractor manufacturing, with engine power being a key factor in the decision-making process for farmers.

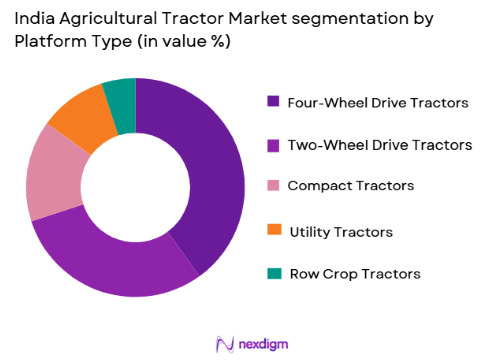

By Platform Type

India Agricultural Tractor market is segmented by platform type into two-wheel drive tractors, four-wheel drive tractors, compact tractors, utility tractors, and row crop tractors. Four-wheel drive tractors have emerged as a dominant sub-segment due to their increased power, traction, and suitability for various types of farming applications. These tractors offer enhanced maneuverability in difficult terrains, especially in regions with uneven soil and challenging topography. Their versatility in different agricultural operations, from tillage to hauling, has resulted in a greater market share for this sub-segment.

Competitive Landscape

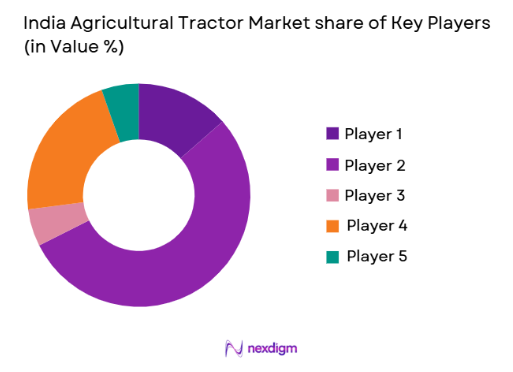

The competitive landscape of the India Agricultural Tractor market is characterized by the presence of both established players and emerging companies. The market has seen a consolidation trend with leading manufacturers like Mahindra & Mahindra and John Deere strengthening their position through mergers, partnerships, and innovation. These major players have substantial market shares due to their widespread dealer networks, diverse product portfolios, and strong brand recognition. The influence of these players drives competitive strategies focused on product innovation, customer loyalty, and strategic pricing, further intensifying market competition.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD billion) | Additional Parameter |

| Mahindra & Mahindra | 1945 | Mumbai, India | ~ | ~ | ~ | ~ | ~ |

| John Deere | 1837 | Moline, USA | ~ | ~ | ~ | ~ | ~ |

| Escorts Group | 1948 | Faridabad, India | ~ | ~ | ~ | ~ | ~ |

| New Holland | 1895 | Turin, Italy | ~ | ~ | ~ | ~ | ~ |

| Sonalika Tractors | 1996 | Hoshiarpur, India | ~ | ~ | ~ | ~ | ~ |

India Agricultural Tractor Market Analysis

Growth Drivers

Government Subsidies

Government subsidies play a significant role in the growth of the agricultural tractor market in India. These subsidies make tractors more affordable for small-scale and marginal farmers, driving demand in rural regions. The government offers various subsidy programs to encourage mechanization in agriculture, thus supporting the purchase of tractors. This initiative has led to increased sales of tractors, especially in the rural and semi-rural areas, where mechanization is still in its nascent stages. These subsidies help farmers offset the high initial cost of purchasing agricultural tractors and ease their transition to modern farming practices. Additionally, such initiatives support farmers’ ability to scale operations and improve productivity, ultimately benefiting the entire agricultural sector.

Technological Advancements

The tractor market is witnessing a shift toward more technologically advanced models with features like GPS, auto-steering, and telematics. These advancements increase operational efficiency and precision in farming, driving the demand for high-tech tractors. As precision farming gains traction in India, tractors equipped with advanced features like automated controls and digital interfaces are becoming more desirable. Farmers are adopting such technologies to optimize fuel efficiency, reduce costs, and improve crop yields. This shift toward technology-enhanced tractors is a key growth driver, as it aligns with the growing emphasis on sustainable farming practices and maximizing output in less time.

Market Challenges

High Initial Investment Costs

One of the key challenges faced by farmers in India when purchasing agricultural tractors is the high initial investment required. Tractors, especially those equipped with advanced features, come at a premium price, which makes them unaffordable for small-scale farmers. Although government subsidies provide some financial assistance, the upfront cost remains a barrier to widespread tractor adoption in less economically developed regions. The financial constraints faced by farmers hinder the pace of mechanization, particularly among those with limited access to credit or financing options.

Climate Dependency

India’s agricultural sector is heavily reliant on the monsoon season, making tractor usage highly seasonal. During periods of drought or excessive rainfall, the demand for tractors decreases as farming activities are halted or delayed. This climate dependency poses a challenge for tractor manufacturers, as fluctuations in the agricultural calendar can lead to inconsistent demand for tractors. Additionally, poor weather conditions may lead to crop failures, further limiting farmers’ ability to invest in new machinery or adopt mechanization.

Opportunities

Adoption of Electric Tractors

The rising awareness of environmental sustainability and the need to reduce carbon emissions presents an opportunity for the adoption of electric tractors in India. With a shift toward more eco-friendly agricultural practices, electric tractors offer a cleaner, more efficient alternative to conventional diesel-powered tractors. As government regulations increasingly favor green technology, the demand for electric tractors is expected to rise. This provides an opportunity for manufacturers to innovate and develop electric tractor models that cater to the needs of Indian farmers, while also benefiting from lower operating costs and reduced carbon footprints.

Precision Farming Solutions

Precision farming techniques, including the use of automated tractors and satellite technology, offer a significant opportunity for growth in the Indian agricultural tractor market. These solutions enable farmers to optimize land use, reduce input costs, and enhance crop productivity. The integration of sensors and GPS technology in tractors allows farmers to monitor soil health, water usage, and crop performance in real-time. As the Indian government continues to promote digitization in agriculture, precision farming is poised for rapid growth, providing a significant market opportunity for tractor manufacturers to expand their product offerings.

Future Outlook

Over the next five years, the India Agricultural Tractor market is expected to experience continued growth driven by increasing mechanization, technological advancements, and government support. The adoption of electric and hybrid tractors, along with the integration of precision farming solutions, will reshape the market dynamics. With a focus on sustainable and efficient farming, the demand for high-performance tractors is expected to rise, particularly in emerging rural areas. Government initiatives to provide financial support and infrastructure development will further accelerate tractor adoption, contributing to the market’s expansion. Technological innovations such as autonomous tractors and AI-driven farming systems will also be key contributors to the market’s evolution.

Major Players

- Mahindra & Mahindra

- John Deere

- Escorts Group

- New Holland

- Sonalika Tractors

- Kubota

- TAFE

- CLAAS

- Yanmar

- Zetor

- Argo Tractors

- SDF Group

- SAME Deutz-Fahr

- Valtra

- Fendt

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Agricultural machinery dealers

- Large-scale agricultural farms

- Agribusiness companies

- Tractor manufacturers

- Agricultural contractors

- Financial institutions providing loans for machinery

Research Methodology

Step 1: Identification of Key Variables

The key variables influencing the India Agricultural Tractor market were identified, focusing on product types, technological advancements, regional demand, and government policies.

Step 2: Market Analysis and Construction

Data was collected from multiple primary and secondary sources, including industry reports, market surveys, and government publications, to create a comprehensive market model.

Step 3: Hypothesis Validation and Expert Consultation

Hypotheses were validated through consultations with market experts, industry analysts, and key stakeholders in the agricultural machinery sector.

Step 4: Research Synthesis and Final Output

The data was synthesized into a detailed report, offering insights into market size, trends, competitive landscape, and growth drivers.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Increasing Agricultural Mechanization

Government Subsidies and Support for Farmers

Rising Demand for High-Efficiency Tractors

Technological Advancements in Tractors

Expansion of Agricultural Land and Irrigation Systems - Market Challenges

High Initial Investment Costs

Technological Gaps in Rural Areas

Dependence on Monsoon and Climate Conditions

Government Policies and Regulations

Lack of Skilled Workforce for Advanced Technologies - Market Opportunities

Growth in Precision Farming

Emerging Demand for Electric and Autonomous Tractors

Adoption of Smart Farming Technologies - Trends

Integration of AI and IoT in Tractors

Shift Toward Sustainable and Eco-Friendly Farming Solutions

Expansion of Tractors with Autonomous Capabilities

Adoption of Hybrid and Electric Tractors

Increasing Customization and Automation in Tractors - Government Regulations & Defense Policy

Subsidy Programs for Farmers

Regulations on Emissions for Agricultural Vehicles

Policies to Promote Sustainable Farming Equipment - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Tractor Engines

Tractor Attachments

Hydraulic Systems

Transmission Systems

Wheel and Tires - By Platform Type (In Value%)

Two-Wheel Drive Tractors

Four-Wheel Drive Tractors

Compact Tractors

Utility Tractors

Row Crop Tractors - By Fitment Type (In Value%)

OEM Fitments

Aftermarket Fitments

Integrated Fitments

Modular Fitments

Custom Fitments - By EndUser Segment (In Value%)

Small-Scale Farmers

Commercial Farmers

Agricultural Cooperatives

Contractors and Service Providers

Government and Public Sector - By Procurement Channel (In Value%)

Direct Sales

Dealers/Distributors

Online Sales Platforms

Private and Government Auctions

Leasing Companies - By Material / Technology (in Value%)

Steel

Alloys

Rubber

Hydraulic Technology

Electric and Hybrid Technology

- Market structure and competitive positioning

- Market share snapshot of major players

- Cross Comparison Parameters (Engine Power, Wheel Configuration, Fitment Type, Fuel Efficiency, Price, Technological Features, Maintenance Cost, Dealer Network, After-Sales Service, Warranty)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

Mahindra & Mahindra

Tafe Tractors

Escorts Group

John Deere

Sonalika Tractors

New Holland

Kubota

Massey Ferguson

SAME Deutz-Fahr

SDF Group

CLAAS

Yanmar

Argo Tractors

Zetor

Tractors and Farm Equipment Limited

- Rural Agricultural Workforce Demand

- Government Role in Tractor Procurement

- Role of Contractors in Large-Scale Farming

- Growth in Mechanized Farming Solutions

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now