Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The India Agricultural Transmission & Gearbox market is valued at approximately USD ~ billion, with substantial contributions from advanced mechanization trends, government incentives for modern agriculture, and the ongoing shift toward automation. Demand for efficient and durable transmission systems has driven market growth, particularly as the agriculture sector increasingly integrates sophisticated machinery. As rural and semi-urban regions continue to expand mechanization initiatives, the sector is expected to see a steady rise in agricultural equipment demand. The market is also fueled by advancements in gearbox technologies, with improvements in fuel efficiency, performance, and adaptability being pivotal drivers.

India’s dominant agricultural regions, including Punjab, Haryana, and Uttar Pradesh, have witnessed substantial growth in the adoption of modern farming equipment. These regions lead in mechanization due to favorable soil conditions, government subsidies, and a high proportion of mechanized farms. The success of agricultural reforms, coupled with state-driven schemes, has prompted rapid infrastructure development and boosted demand for advanced transmission and gearbox systems. These areas continue to shape the market, benefiting from strong policy support and agricultural growth programs.

Market Segmentation

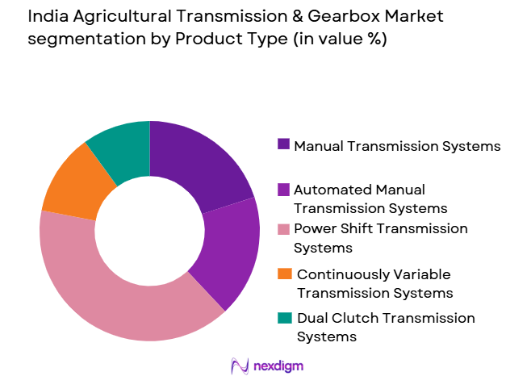

By Product Type

The India Agricultural Transmission & Gearbox market is segmented by product type into manual transmission systems, automated manual transmission systems, power shift transmission systems, continuously variable transmission (CVT) systems, and dual clutch transmission systems. The power shift transmission systems sub-segment currently dominates the market share due to their exceptional efficiency in energy transfer, smoother gear shifting, and ability to handle a wide range of agricultural tasks. The demand for power shift transmission systems is further propelled by their durability and the rise of technologically advanced farm machinery.

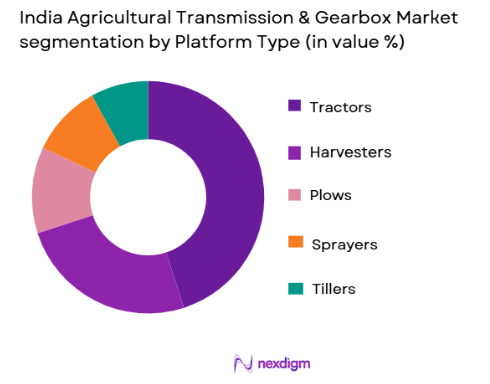

By Platform Type

The India Agricultural Transmission & Gearbox market is also segmented by platform type, including tractors, harvesters, plows, sprayers, and tillers. Tractors hold a dominant position due to their central role in agricultural operations. With rising demand for high-horsepower, energy-efficient tractors equipped with advanced transmission systems, the segment’s growth is sustained by government policies aimed at supporting mechanized farming. Furthermore, tractor adoption is bolstered by the increasing focus on crop productivity, where robust and reliable transmission systems are essential for optimizing performance.

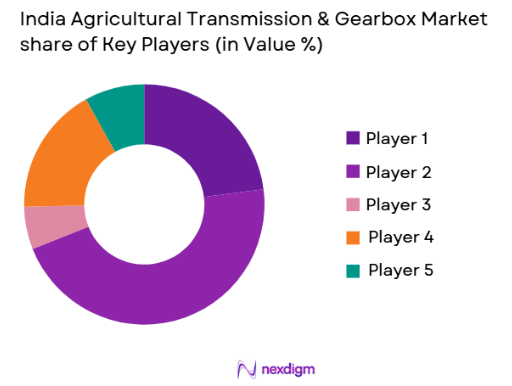

Competitive Landscape

The competitive landscape of the India Agricultural Transmission & Gearbox market is shaped by consolidation, technological advancements, and the entry of global players alongside established local manufacturers. Key players continue to dominate the market by leveraging robust distribution networks, efficient production processes, and innovation. As companies collaborate with OEMs and government bodies to expand market reach, the competitive dynamics are expected to shift towards players with integrated offerings in automation and IoT-enabled systems.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD Billion) | Additional Parameter |

| Mahindra & Mahindra | 1945 | Mumbai, India | ~ | ~ | ~ | ~ | ~ |

| John Deere | 1837 | Moline, USA | ~ | ~ | ~ | ~ | ~ |

| Escorts Group | 1945 | Faridabad, India | ~ | ~ | ~ | ~ | ~ |

| Kubota Corporation | 1890 | Osaka, Japan | ~ | ~ | ~ | ~ | ~ |

| New Holland Agriculture | 1895 | Turin, Italy | ~ | ~ | ~ | ~ | ~ |

India Agricultural Transmission & Gearbox Market Analysis

Growth Drivers

Government Support for Agricultural Mechanization

Government initiatives play a crucial role in promoting mechanized farming by providing subsidies, grants, and low-interest loans to farmers for purchasing modern equipment. These policies aim to increase agricultural productivity and reduce labor dependence by facilitating the adoption of advanced transmission and gearbox systems. With the government’s continued push for sustainable farming practices, these financial incentives are expected to further drive market growth, especially in rural and semi-urban regions. The mechanization of agriculture aligns with India’s broader agricultural reforms, ensuring long-term stability and growth in the sector.

Technological Advancements in Transmission Systems

The rapid evolution of agricultural machinery, driven by advancements in gearbox technology, has significantly impacted the India Agricultural Transmission & Gearbox market. As manufacturers focus on improving the durability, fuel efficiency, and adaptability of transmission systems, modern farm equipment increasingly incorporates innovations such as power shift and continuously variable transmission systems. These technologies offer better energy transfer, higher productivity, and reduced operational costs. The demand for such systems continues to rise as more farmers invest in sophisticated machines designed to enhance performance and productivity.

Market Challenges

High Cost of Advanced Transmission Systems

One of the primary barriers to widespread adoption of advanced transmission systems in India’s agricultural sector is the high upfront cost associated with acquiring sophisticated machinery. Small-scale farmers, who dominate the rural landscape, often face financial constraints and are unable to afford high-end systems, resulting in a slow rate of adoption. While government schemes attempt to mitigate this challenge, the cost remains a significant hurdle, particularly for farmers operating with limited capital. This has created a disparity in the adoption of new technologies between large agricultural enterprises and smallholder farmers, limiting market growth in certain regions.

Lack of Skilled Workforce for Modern Equipment

As agricultural machinery becomes more technologically advanced, the lack of skilled technicians and operators trained to manage modern equipment poses a significant challenge. Transmission and gearbox systems require specialized knowledge for installation, operation, and maintenance. The shortage of trained personnel, especially in rural areas, hinders the efficient functioning of agricultural machinery and increases downtime. As a result, farmers often revert to outdated, less efficient systems, which diminishes the overall market potential for advanced transmission technologies.

Opportunities

Integration of IoT in Agricultural Equipment

The integration of Internet of Things (IoT) technology into agricultural equipment presents significant opportunities for the growth of the India Agricultural Transmission & Gearbox market. IoT-enabled devices can monitor system performance, detect faults, and optimize the operation of transmission systems, providing real-time data for maintenance and improving the overall efficiency of farming operations. The adoption of IoT in agriculture is accelerating due to the benefits of predictive maintenance, real-time monitoring, and enhanced operational performance. As the demand for connected, smart farming solutions grows, the market for advanced transmission systems is expected to expand significantly.

Rising Demand for Sustainable Farming Practices

There is an increasing demand for sustainable farming practices, driven by environmental concerns and the need for resource efficiency. This trend has led to greater adoption of advanced transmission and gearbox technologies that improve fuel efficiency, reduce emissions, and enhance the overall sustainability of agricultural operations. The growing preference for eco-friendly farming solutions is encouraging the development of low-emission, energy-efficient machinery. This shift towards sustainability presents an opportunity for transmission system manufacturers to develop and offer environmentally conscious solutions that cater to the evolving needs of modern agriculture.

Future Outlook

Over the next five years, the India Agricultural Transmission & Gearbox market is expected to experience steady growth, driven by technological advancements, government support for mechanization, and increasing demand for smart farming solutions. As the government continues to incentivize the adoption of advanced machinery, the market will witness more widespread use of power shift and continuously variable transmission systems. Additionally, the growth of IoT-enabled devices and smart agriculture systems will further propel the demand for modern transmission technologies. With rising focus on sustainability and productivity, India’s agricultural sector is well-positioned to embrace the next generation of mechanized solutions.

Major Players

- Mahindra & Mahindra

- John Deere

- Escorts Group

- Kubota Corporation

- New Holland Agriculture

- TAFE Motors

- SDF Group

- Massey Ferguson

- Bharat Earth Movers Limited

- AGCO Corporation

- ZF Friedrichshafen AG

- Valtra

- JCB

- Case IH

- CNH Industrial

Key Target Audience

- Government and regulatory bodies

- Agricultural equipment manufacturers

- Agricultural machinery distributors

- Financial institutions and lending organizations

- Farmers and agricultural cooperatives

- Investment and venture capital firms

- Rural development agencies

- OEMs (Original Equipment Manufacturers)

Research Methodology

Step 1: Identification of Key Variables

Identify the key market drivers, challenges, opportunities, and growth patterns that influence the India Agricultural Transmission & Gearbox market.

Step 2: Market Analysis and Construction

Analyze historical data and current market trends to construct the market size, segmentation, and growth patterns.

Step 3: Hypothesis Validation and Expert Consultation

Validate market hypotheses through expert consultations, interviews with industry professionals, and secondary research.

Step 4: Research Synthesis and Final Output

Synthesize research findings into a final comprehensive market report, including all necessary insights, forecasts, and recommendations.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising Demand for Advanced Agricultural Equipment

Government Support for Agricultural Mechanization

Technological Advancements in Transmission Systems

Increasing Focus on Fuel Efficiency

Shift Toward Automation in Agriculture - Market Challenges

High Cost of Advanced Transmission Systems

Lack of Skilled Workforce for New Technologies

Complexities in Maintaining Advanced Gearbox Systems

Limited Awareness Among Small-Scale Farmers

Regulatory Constraints in Certain Regions - Market Opportunities

Technological Innovation in Transmission Systems

Increase in Export Demand for Agricultural Machinery

Government Incentives for Sustainable Agriculture Practices - Trends

Integration of IoT in Agricultural Transmission Systems

Growing Adoption of Hybrid and Electric Systems

Shift Toward Precision Agriculture Technologies

Miniaturization of Gearboxes for Compact Tractors

Rise of Smart Sensors in Agricultural Equipment - Government Regulations & Defense Policy

Incentives for Agricultural Modernization

Energy Efficiency Standards for Agricultural Equipment

Regulations on Emissions and Sustainability Practices - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Manual Transmission Systems

Automated Manual Transmission Systems

Power Shift Transmission Systems

Continuously Variable Transmission (CVT) Systems

Dual Clutch Transmission Systems - By Platform Type (In Value%)

Tractors

Harvesters

Plows

Sprayers

Tillers - By Fitment Type (In Value%)

OEM (Original Equipment Manufacturer) Fitment

Aftermarket Fitment

Hybrid Fitment

Custom Fitment

Retrofit Solutions - By EndUser Segment (In Value%)

Farm Equipment Manufacturers

Agricultural Cooperatives

Independent Farmers

Agricultural Service Providers

Government & Regulatory Bodies - By Procurement Channel (In Value%)

Direct Procurement

Dealer/Distributor Channels

Online Platforms

Government Tenders

OEM Partnerships - By Material / Technology (in Value%)

Steel Components

Alloy Materials

Electronics and Automation

Hydraulic Systems

Smart Agricultural Systems

- Market structure and competitive positioning

- Market share snapshot of major players

- Cross Comparison Parameters (System Type, Platform Type, Procurement Channel, End User Segment, Fitment Type, Material/Technology, Geographic Reach, Product Portfolio, Customer Support, Innovation)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

Mahindra & Mahindra

Sonalika Tractors

John Deere

Escorts Group

Kubota Corporation

New Holland Agriculture

SDF Group

Tafe Motors

Massey Ferguson

Bharat Earth Movers Limited

Sisu Diesel

ZF Friedrichshafen AG

AGCO Corporation

BorgWarner Inc.

Valeo SA

- Demand for Customizable Agricultural Machinery

- Increasing Investment in Precision Agriculture

- Shift Toward High-Torque Transmission Solutions

- Growing Interest in Automated Equipment

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now