Market Outlook to 2035")

Market Outlook to 2035") Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the India Battery Energy Storage System (BESS) market reached approximately USD ~ billion in total project value, supported by government-backed grid-scale storage tenders and rising renewable energy integration. The market is primarily driven by large-scale solar and wind additions exceeding USD ~ billion in annual renewable investments, alongside Production Linked Incentive allocations of USD ~ billion for advanced chemistry cell manufacturing announced by the Government of India.

Major demand centers include Gujarat, Maharashtra, Rajasthan, Tamil Nadu, and Karnataka, where renewable installations and industrial electricity consumption are concentrated. These states host large solar parks, data centers, and manufacturing clusters, creating high demand for grid stabilization and backup solutions. Delhi NCR and Hyderabad are also emerging hubs due to rapid data center expansion and increasing commercial and industrial investments in captive and hybrid energy storage systems.

Market Segmentation

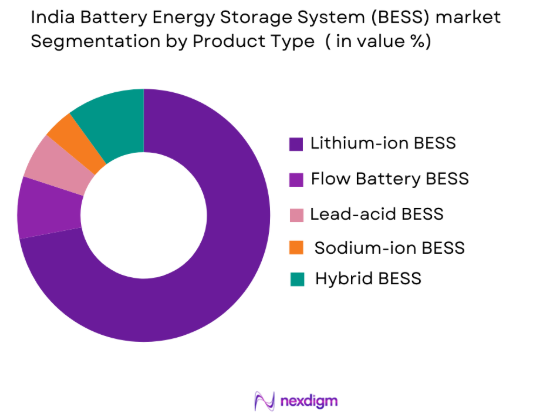

By Product Type

India Battery Energy Storage System (BESS) market is segmented by product type into Lithium-ion BESS, Flow Battery BESS, Lead-acid BESS, Sodium-ion BESS, and Hybrid BESS. Recently, Lithium-ion BESS has a dominant market share due to factors such as strong domestic cell manufacturing incentives, proven performance in utility-scale deployments, high energy density, and declining global battery pack prices. Its compatibility with solar and wind projects and established supply chains further reinforce its leadership position across grid-scale and commercial installations.

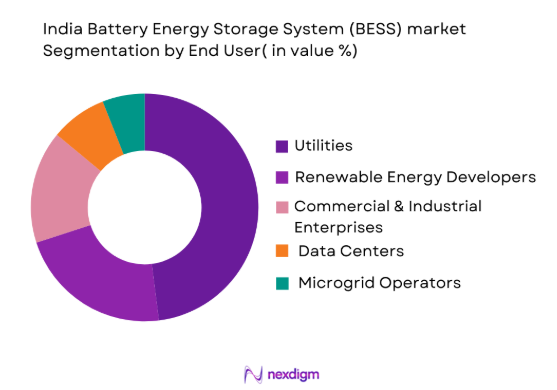

By End-User Segment

India Battery Energy Storage System (BESS) market is segmented by end-user segment into Utilities, Renewable Energy Developers, Commercial & Industrial Enterprises, Data Centers, and Microgrid Operators. Recently, Utilities have a dominant market share due to large-scale storage procurement through centralized tenders, grid stability requirements, and peak load management mandates. State distribution companies and transmission operators are deploying multi-megawatt projects to balance intermittent renewable output and maintain frequency regulation standards, positioning utilities as the primary demand generator.

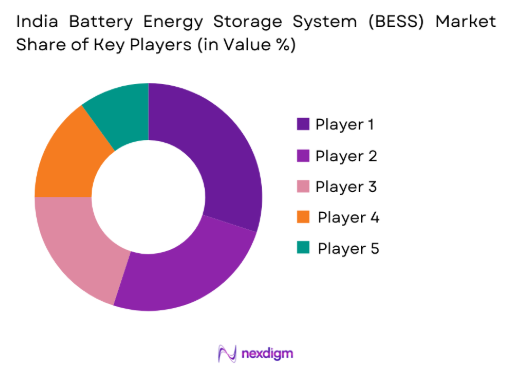

Competitive Landscape

The India Battery Energy Storage System (BESS) market reflects moderate consolidation, with large conglomerates and global technology providers securing major utility-scale contracts. Strategic alliances between domestic energy firms and international storage technology companies are common, particularly for large government-backed projects. Established players leverage integrated EPC capabilities and financing strength, while emerging firms focus on niche long-duration and distributed storage solutions.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Installed Storage Capacity in India |

| Tata Power Solar Systems | 1989 | Mumbai, India | ~ | ~ | ~ | ~ | ~ |

| Adani Green Energy | 2015 | Ahmedabad, India | ~ | ~ | ~ | ~ | ~ |

| Reliance New Energy | 2021 | Mumbai, India | ~ | ~ | ~ | ~ | ~ |

| Fluence Energy | 2018 | Virginia, USA | ~ | ~ | ~ | ~ | ~ |

| Larsen & Toubro | 1938 | Mumbai, India | ~ | ~ | ~ | ~ | ~ |

India Battery Energy Storage System (BESS) Market Analysis

Growth Drivers

Rising Renewable Energy Capacity and Grid Stability Requirements

India’s aggressive renewable energy expansion program has resulted in solar and wind additions exceeding 180 GW of installed capacity, creating variability in power supply that necessitates reliable storage integration to maintain grid stability and frequency regulation. Utility-scale solar parks in Rajasthan and Gujarat, along with wind clusters in Tamil Nadu and Karnataka, generate intermittent output that increases curtailment risk and operational inefficiencies without storage buffering solutions. Battery Energy Storage Systems provide fast-response balancing services, enabling grid operators to manage peak demand and ramping needs more effectively. The national transmission operator has increasingly emphasized ancillary service procurement to address real-time frequency deviations. Storage projects are being integrated within hybrid renewable bids to ensure firm and dispatchable power supply commitments. This shift is influencing tariff structures and procurement models that embed storage within renewable contracts. As renewable penetration deepens in the energy mix, the technical requirement for storage becomes structurally embedded in grid planning frameworks. Long-duration storage solutions are also being evaluated to support evening peak demand created by residential and commercial consumption growth. These factors collectively establish renewable expansion as a fundamental driver of BESS deployment across multiple states and applications.

Government Incentives and Policy Framework for Energy Storage Deployment

The Government of India has introduced multiple policy initiatives to accelerate domestic battery manufacturing and storage deployment, including a USD ~ billion Production Linked Incentive scheme for Advanced Chemistry Cells that aims to localize supply chains and reduce import dependency. Central agencies have conducted large-scale storage tenders exceeding 4 GWh capacity, providing visibility and demand certainty for investors and developers. Regulatory frameworks now permit storage participation in ancillary service markets and capacity auctions, expanding revenue streams beyond energy arbitrage. State-level renewable purchase obligations increasingly include storage-linked requirements to ensure reliability. Financial institutions have extended concessional green financing lines to storage-integrated renewable projects. The inclusion of storage in transmission planning has enabled grid operators to consider non-wire alternatives for congestion mitigation. Policy clarity around open access and behind-the-meter installations is supporting commercial and industrial adoption. Standardization of technical guidelines for interconnection and safety compliance is reducing project approval timelines. These coordinated policy interventions significantly enhance investor confidence and accelerate capital deployment into the BESS ecosystem.

Market Challenges

High Capital Intensity and Financing Constraints for Large-Scale Projects

Battery Energy Storage Systems require substantial upfront capital investment due to battery cell costs, power conversion systems, civil infrastructure, and grid interconnection components, creating financial barriers particularly for smaller developers and distribution companies. While lithium-ion prices have declined globally, imported components and currency fluctuations increase project cost volatility. Domestic manufacturing capacity remains under development, limiting economies of scale and local sourcing advantages. Lenders often perceive storage as a relatively new asset class with evolving revenue models, leading to conservative risk assessment and higher financing costs. Long-term revenue visibility remains dependent on policy-backed tenders and hybrid renewable contracts. Merchant market participation for storage is still emerging, restricting diversified income streams. Project developers must structure complex contracts that integrate energy arbitrage, capacity payments, and ancillary services. Delays in payment cycles from state utilities further elevate counterparty risk concerns. These financial complexities constrain rapid scaling despite strong underlying demand fundamentals.

Battery Lifecycle Management and Recycling Infrastructure Limitations

As deployment volumes increase, concerns regarding end-of-life battery disposal, recycling efficiency, and environmental compliance are becoming more prominent in project evaluation frameworks. India’s recycling ecosystem for advanced lithium-ion batteries is still developing, with limited large-scale facilities capable of processing grid-scale battery modules. Transportation and hazardous material handling regulations add operational complexity to lifecycle management. Developers must incorporate recycling provisions within project financial modeling, affecting overall return calculations. The absence of standardized second-life application frameworks limits value recovery potential from used batteries. Environmental clearances and waste management compliance requirements can extend project timelines. Dependence on imported raw materials such as lithium and cobalt exposes the industry to global supply chain disruptions. Ensuring traceability and sustainability across the value chain is becoming critical for institutional investors and international financiers. These lifecycle and sustainability challenges require coordinated regulatory and industrial responses to ensure long-term viability.

Opportunities

Expansion of Domestic Cell Manufacturing and Value Chain Localization

India’s strategic push to establish domestic advanced chemistry cell manufacturing under the Production Linked Incentive framework presents significant opportunities for cost optimization and supply chain resilience within the BESS market. Localization of cell production can reduce dependency on imports and mitigate foreign exchange exposure risks. Integrated manufacturing clusters are expected to stimulate ancillary industries including battery management systems, enclosures, and thermal management solutions. Domestic production enhances eligibility for government-backed procurement preferences and financing incentives. Technology partnerships with global battery innovators can accelerate knowledge transfer and process optimization. As domestic gigafactories scale production capacity, economies of scale can drive competitive pricing for grid-scale projects. Local sourcing can also reduce project lead times and logistics costs. Industrial policy alignment with renewable expansion targets further strengthens investment attractiveness. This opportunity positions India as a potential regional hub for battery storage exports in the long term.

Integration with Electric Mobility and Distributed Energy Ecosystems

Rapid electric vehicle adoption and charging infrastructure expansion create complementary demand for distributed energy storage systems capable of managing localized peak loads and grid stress. Integration of BESS within EV charging hubs can reduce demand charges and enable smart load management. Urban commercial complexes and industrial parks are exploring hybrid systems combining rooftop solar, storage, and EV charging. Bidirectional charging technologies open prospects for vehicle-to-grid applications that can support ancillary services. Distributed storage installations enhance resilience against grid outages in metropolitan areas. The convergence of mobility electrification and renewable energy adoption generates cross-sector investment synergies. Data-driven energy management platforms enable optimization of distributed storage fleets. Policy support for clean mobility strengthens the business case for storage integration. This convergence expands addressable market segments beyond traditional utility-scale deployments.

Future Outlook

The India Battery Energy Storage System (BESS) market is expected to witness sustained expansion over the next five years, driven by deeper renewable penetration and continued policy support. Advancements in lithium iron phosphate and emerging sodium-ion technologies are likely to enhance cost efficiency and safety. Regulatory frameworks encouraging ancillary service participation will broaden revenue streams. Rising demand from utilities, data centers, and industrial users is expected to reinforce long-term deployment momentum.

Major Players

- Tata Power Solar Systems Limited

- Adani Green Energy Limited

- Reliance New Energy Limited

- Fluence Energy India Private Limited

- Larsen & Toubro Limited

- Exide Industries Limited

- Amara Raja Energy & Mobility Limited

- Siemens Energy India Limited

- Hitachi Energy India Limited

- Sterling and Wilson Renewable Energy Limited

- WaareeEnergies Limited

- HBL Power Systems Limited

- Delta Electronics India Private Limited

- ReNewPower Private Limited

- AES India Private Limited

Key Players

- Tata Power Solar Systems Limited

- Adani Green Energy Limited

- Reliance New Energy Limited

- Fluence Energy India Private Limited

- Larsen & Toubro Limited

- Exide Industries Limited

- Amara Raja Energy & Mobility Limited

- Siemens Energy India Limited

- Hitachi Energy India Limited

- Sterling and Wilson Renewable Energy Limited

Research Methodology

Step 1: Identification of Key Variables

Key variables including installed storage capacity, project pipeline, regulatory mandates, investment flows, and technology mix were identified. Primary interviews with developers and utilities were combined with secondary government data sources to validate scope and assumptions.

Step 2: Market Analysis and Construction

Market sizing was constructed using project-level tender data, announced investments, and financial disclosures. Demand segmentation was developed across product types and end-user categories to ensure structured analysis.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts including grid operators, EPC contractors, and policy advisors were consulted to validate assumptions. Scenario modeling was applied to test regulatory and pricing sensitivities.

Step 4: Research Synthesis and Final Output

Quantitative findings and qualitative insights were synthesized into a structured report format. Data triangulation ensured consistency across revenue, capacity, and policy-driven projections.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising Renewable Energy Integration Targets

Expansion of Grid Modernization Programs

Increasing Peak Load Management Requirements - Market Challenges

High Initial Capital Investment Requirements

Battery Recycling and Disposal Constraints

Grid Interconnection and Regulatory Delays - Market Opportunities

Development of Domestic Cell Manufacturing Capacity

Adoption of Long-duration Energy Storage Technologies

Integration with Electric Mobility Infrastructure - Trends

Shift Toward Lithium Iron Phosphate Chemistry

Emergence of Battery-as-a-Service Models

Digital Monitoring and AI-based Energy Optimization

Government Regulations

SWOT Analysis of Key Competitors

Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Lithium-ion Battery Energy Storage Systems

Flow Battery Energy Storage Systems

Lead-acid Battery Energy Storage Systems

Sodium-ion Battery Energy Storage Systems

Hybrid Battery Energy Storage Systems - By Platform Type (In Value%)

Utility-scale Grid-connected Systems

Commercial and Industrial Systems

Residential Rooftop Solar Integrated Systems

Microgrid-based Systems

Electric Vehicle Charging Integrated Systems - By Fitment Type (In Value%)

Standalone Battery Installations

Solar-plus-Storage Integrated Systems

Wind-plus-Storage Integrated Systems

Behind-the-Meter Installations

Front-of-the-Meter Installations - By End User Segment (In Value%)

State Electricity Distribution Companies

Independent Power Producers

Commercial and Industrial Enterprises

Renewable Energy Developers

Data Centers and IT Parks - By Procurement Channel (In Value%)

Government Tenders and Auctions

Direct EPC Procurement

Public-Private Partnership Contracts

Corporate Power Purchase Agreements

Third-party Energy Service Providers

- Market Share Analysis

- Cross Comparison Parameters (Technology Type, Project Capacity Range, Integration Capability, Pricing Model, Geographic Presence, Battery Chemistry Portfolio, EPC Capability, O&M Service Strength, Grid Compliance Standards, Storage Duration Range, Financial Backing Strength, Domestic Manufacturing Presence, Software & Energy Management Platform, Strategic Partnerships, After-Sales Support Network)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Tata Power Solar Systems Limited

Adani Green Energy Limited

Reliance New Energy Limited

Fluence Energy India Private Limited

AES India Private Limited

Siemens Energy India Limited

Larsen & Toubro Limited

Exide Industries Limited

Amara Raja Energy & Mobility Limited

Waaree Energies Limited

ReNew Power Private Limited

HBL Power Systems Limited

Delta Electronics India Private Limited

Hitachi Energy India Limited

Sterling and Wilson Renewable Energy Limited

- Utilities prioritizing grid stability and frequency regulation investments

- C&I sector focusing on demand charge reduction and backup reliability

- Renewable developers integrating storage to ensure firm power supply

- Data centers adopting BESS for uninterrupted operations and sustainability compliance

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Market Outlook to 2035")

Market Outlook to 2035")

Market Outlook to 2035")

Market Outlook to 2035")

Market Outlook to 2035") Request a Sample

Request a Sample Market Outlook to 2035") Ask for Customization

Ask for Customization Market Outlook to 2035") Get a Quote

Get a Quote Market Outlook to 2035") Enquire Now

Enquire Now Market Outlook to 2035")