Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The India car finance market has experienced substantial growth, driven by increasing consumer demand for both new and used vehicles. The market size, based on a recent historical assessment, has seen significant expansion, valued at ~ billion USD. This growth is attributed to a notable rise in financial institutions offering tailored auto loan products. Major factors contributing to the growth include the expansion of digital lending platforms, increasing disposable income, and favorable interest rates for borrowers. In addition, a higher preference for vehicle ownership in tier II and tier III cities has been key in driving market dynamics.

The market’s dominance is largely concentrated in metropolitan cities such as Delhi, Mumbai, and Bengaluru, where higher disposable incomes, increased financial inclusion, and better access to financing options contribute to the thriving market. These cities experience a significant amount of vehicle sales and financing activity, owing to their well-developed infrastructure and consumer behavior that leans toward vehicle ownership. Additionally, the expansion of digital platforms for auto loans is further enhancing financial accessibility, even in semi-urban regions.

Market Segmentation

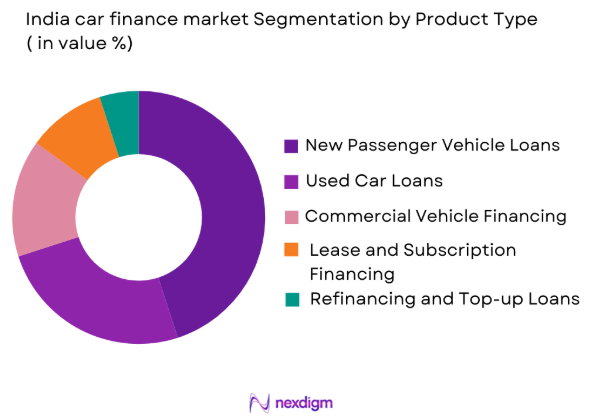

By Product Type

The India car finance market is segmented by product type into new passenger vehicle loans, used car loans, commercial vehicle financing, lease and subscription financing, and refinancing and top-up loans. Recently, new passenger vehicle loans have captured the dominant market share due to rising demand for personal vehicles, particularly in urban areas. Consumer preference for owning new cars with attractive financing terms, along with dealer promotions and favorable government policies for vehicle sales, contributes to the dominance of this sub-segment.

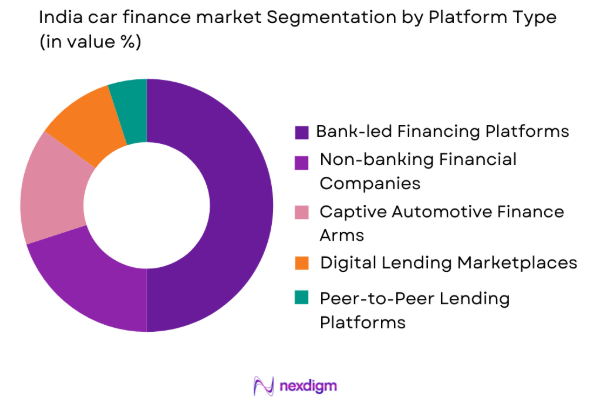

By Platform Type

The market is segmented into bank-led financing platforms, non-banking financial company platforms, captive automotive finance platforms, digital lending marketplaces, and peer-to-peer lending platforms. Bank-led financing platforms dominate due to their established customer base and access to affordable capital. These platforms benefit from long-term relationships with consumers and a wide reach across both urban and rural areas, supported by the extensive branch network of major banks.

Competitive Landscape

The competitive landscape of the India car finance market is highly fragmented, with key players competing across multiple segments, including digital and traditional financing. Banks and non-banking financial companies (NBFCs) dominate the market, while fintech platforms and OEMs’ captive finance arms are gradually gaining market share. The market is expected to witness consolidation, with leading players adopting digital platforms to increase their customer base and enhance service offerings.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Additional Parameter |

| State Bank of India | 1955 | Mumbai, India | ~ | ~ | ~ | ~ | ~ |

| HDFC Bank | 1994 | Mumbai, India | ~ | ~ | ~ | ~ | ~ |

| ICICI Bank | 1994 | Mumbai, India | ~ | ~ | ~ | ~ | ~ |

| Bajaj Finserv | 2007 | Pune, India | ~ | ~ | ~ | ~ | ~ |

| Mahindra Finance | 1997 | Mumbai, India | ~ | ~ | ~ | ~ | ~ |

India car finance Market Analysis

Growth Drivers

Rising Vehicle Ownership Aspirations

The rising aspirations for vehicle ownership, especially among the middle class in urban and rural India, is a primary driver for the growth of the car finance market. As disposable incomes rise, a significant portion of the population is inclined toward owning personal vehicles. This is particularly evident in tier II and tier III cities where consumers are opting for vehicle loans to fulfill their aspirations for personal mobility. The availability of low-interest loans, flexible EMIs, and government subsidies also plays a pivotal role in encouraging vehicle ownership.

Digital Lending Adoption

Another key growth driver is the increasing adoption of digital lending platforms, which have revolutionized the way consumers access auto loans. With the rise of mobile internet penetration and the push for digitalization by financial institutions, more people are turning to online platforms for quick loan approvals and disbursements. Digital platforms enable quick verification processes, real-time loan assessments, and instant loan disbursals, making the process more efficient and accessible to a broader audience, including first-time car buyers in remote locations.

Market Challenges

High Non-performing Assets (NPAs)

One of the primary challenges facing the India car finance market is the increasing rate of non-performing assets (NPAs). A significant portion of car loans, particularly in the used car segment, suffers from high default rates, which impact the profitability of lenders. This challenge is exacerbated by the economic uncertainty caused by fluctuating interest rates and the risk of loans becoming non-recoverable, especially among subprime borrowers. Financial institutions are adopting stricter credit assessment processes to mitigate this risk but it remains a substantial concern for market participants.

Regulatory Constraints and Compliance Issues

The regulatory environment governing the India car finance market presents both challenges and opportunities. While the government has implemented favorable policies for vehicle financing, such as subsidies for electric vehicles, regulations around loan recovery, interest rate caps, and borrower protection continue to evolve. Financial institutions must navigate these regulations while balancing profitability and compliance, which can be complex and resource-intensive. Moreover, stringent Know-Your-Customer (KYC) norms and increased scrutiny on lending practices have created an additional burden for lenders in terms of operational cost and time.

Opportunities

Growth in Electric Vehicle Financing

The rise of electric vehicles (EVs) in India presents significant opportunities for the car finance market. With government incentives aimed at encouraging the adoption of electric vehicles, there is an increasing demand for EV-specific financing solutions. Lenders are introducing specialized financing products that cater to EV buyers, including lower interest rates and longer loan tenures. This segment is expected to grow rapidly as the adoption of EVs continues to rise, supported by favorable government policies, consumer interest in sustainable mobility, and technological advancements in electric vehicle infrastructure.

Partnerships with OEMs and Fintechs

Strategic partnerships between car manufacturers (OEMs) and fintech companies have created new avenues for growth in the car finance market. OEMs are increasingly offering captive financing solutions, allowing customers to finance vehicles directly through the brand’s financial arm. Additionally, collaborations with fintech firms provide enhanced access to auto loans through digital channels, improving loan accessibility and streamlining the loan approval process. This trend is likely to gain traction as the Indian consumer becomes more digitally inclined and car manufacturers seek new ways to offer financing solutions.

Future Outlook

Over the next five years, the India car finance market is expected to witness significant growth, driven by technological advancements, an expanding middle class, and increasing vehicle ownership. The growing preference for digital lending platforms will continue to enhance market accessibility and reduce the barriers to financing. The government’s push for electric vehicles and regulatory support for alternative financing models will create new growth opportunities. With robust economic recovery and the expansion of vehicle ownership in tier II and tier III cities, the market outlook is optimistic.

Major Players

- State Bank of India

- HDFC Bank

- ICICI Bank

- BajajFinserv

- Mahindra Finance

- Kotak Mahindra Bank

- Tata Capital

- Aditya Birla Finance

- Reliance Capital

- Muthoot Finance

- L&T Finance

- Shriram City Union Finance

- Axis Bank

- Bank of Baroda

- Punjab National Bank

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Car manufacturers (OEMs)

- Non-banking financial companies (NBFCs)

- Digital lending platforms

- Insurance companies

- Automotive dealerships

- Private equity firms

Research Methodology

Step 1: Identification of Key Variables

This step involves identifying the critical factors that drive the car finance market, including loan types, interest rates, customer demographics, and platform types.

Step 2: Market Analysis and Construction

Data from multiple sources, including financial reports, consumer surveys, and regulatory frameworks, is analyzed to construct an accurate market model.

Step 3: Hypothesis Validation and Expert Consultation

Experts from the finance and automotive sectors validate the assumptions used in the market model to ensure that the analysis is robust and reflects real-world scenarios.

Step 4: Research Synthesis and Final Output

The insights gathered from various sources are synthesized to produce the final market report, with clear recommendations and a detailed market outlook.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising Vehicle Ownership Aspirations Across Tier II and Tier III Cities

Expansion of Digital Loan Origination and E-KYC Infrastructure

Increasing Penetration of Used Vehicle Financing - Market Challenges

Asset Quality Stress and Rising Delinquencies

Regulatory Compliance and Capital Adequacy Pressures

Interest Rate Volatility Impacting Borrowing Costs - Market Opportunities

Growth in Electric Vehicle Financing Solutions

Partnerships Between Fintechs and Automotive OEMs

Expansion of Credit Access Through Alternative Data Underwriting - Trends

Shift Toward Fully Digital Loan Disbursement Models

Bundling of Insurance and Maintenance with Auto Loans

Adoption of AI-based Credit Risk Assessment

Government Regulations

Porter’s Five Forces

SWOT Analysis of Key Competitors

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

New Passenger Vehicle Loans

Used Car Loans

Commercial Vehicle Financing

Lease and Subscription Financing

Refinancing and Top-up Loans - By Platform Type (In Value%)

Bank-led Financing Platforms

Non-Banking Financial Company Platforms

Captive Automotive Finance Platforms

Digital Lending Marketplaces

Peer-to-Peer Lending Platforms - By Fitment Type (In Value%)

Dealer-arranged Financing

Direct-to-Consumer Financing

Online Aggregator-based Financing

Embedded Finance at OEM Level

Broker-assisted Financing - By End User Segment (In Value%)

Individual Salaried Customers

Self-employed Professionals

Small Fleet Operators

Corporate Fleet Buyers

Rural and Semi-urban Borrowers - By Procurement Channel (In Value%)

Public Sector Banks

Private Sector Banks

Non-Banking Financial Companies

OEM Captive Finance Arms

Digital Fintech Lenders

- Market Share Analysis

- Cross Comparison Parameters (Loan Tenure, Interest Rate Structure, Loan-to-Value Ratio, Digital Disbursement Capability, Geographic Reach, Processing Time, Credit Score Threshold, Prepayment Charges, Documentation Requirements, Dealer Network Integration, EV Financing Support, Risk Assessment Model, EMI Flexibility Options, Customer Acquisition Cost, Portfolio Diversification Strategy)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

State Bank of India

HDFC Bank

ICICI Bank

Axis Bank

Bank of Baroda

Punjab National Bank

Kotak Mahindra Bank

Tata Capital Financial Services

Mahindra Finance

Shriram Finance

Bajaj Finserv

Cholamandalam Investment and Finance Company

Toyota Financial Services India

Volkswagen Finance India

Hero FinCorp

- Increasing Credit Dependence Among First-time Car Buyers

- Growing Demand for Flexible EMI Structures

- Preference for Faster Loan Approvals Through Digital Channels

- Rising Adoption of Used Car Financing in Urban Clusters

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now