Download PDF

Download PDF Download PDF

Download PDFMarket Overview

India’s courier, express, and parcel market is valued at USD ~ billion based on a recent historical assessment, supported by industry findings published by Research and Markets. Demand is driven by strong e-commerce order volumes, wider use of digital payments, rising preference for same-day and next-day fulfillment, and increasing adoption of automation in sorting, routing, and shipment tracking. Government support for logistics infrastructure and expansion of organized retail supply chains are also reinforcing parcel movement across business and consumer segments.

Delhi NCR, Mumbai, Bengaluru, Hyderabad, and Chennai dominate the India CEP ecosystem because they combine dense consumer demand, large merchant bases, airport and warehouse connectivity, and strong presence of national delivery networks. These cities support high shipment throughput for e-commerce, document delivery, healthcare logistics, and quick commerce. Their dominance is reinforced by better road infrastructure, concentrated fulfillment capacity, and wider availability of technology-enabled delivery fleets, enabling courier operators to maintain faster pickup, sorting, and last-mile distribution cycles.

Market Segmentation

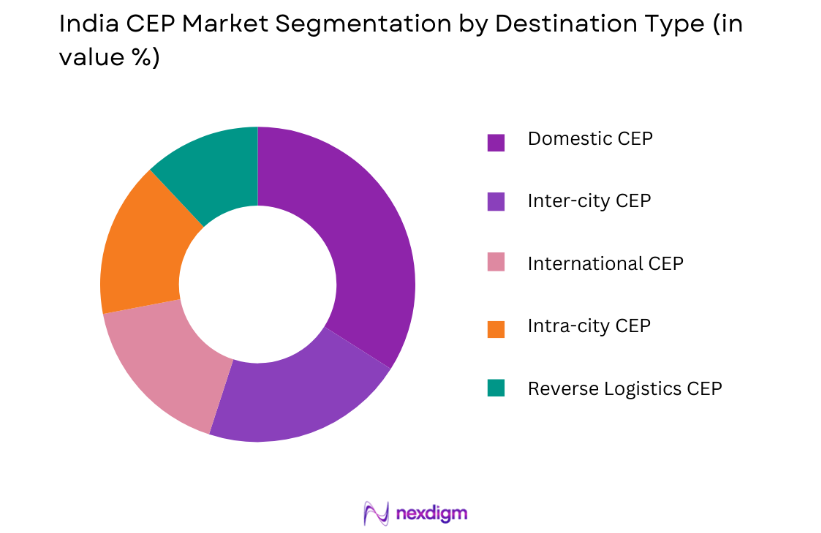

By Destination Type

India CEP market is segmented by Destination type into Domestic CEP, International CEP, Intra-city CEP, Inter-city CEP, and Reverse Logistics CEP. Recently, Domestic CEP has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Domestic parcel traffic is anchored by online retail, marketplace replenishment, banking documents, healthcare shipments, and direct-to-consumer brands that require frequent nationwide movement. Large operators maintain denser pickup points, sorting hubs, and delivery fleets for domestic lanes than for cross-border flows. Lower transit complexity, faster turnaround, wider serviceability across pin codes, and stronger integration with Indian e-commerce platforms continue to keep domestic shipments at the center of overall CEP demand.

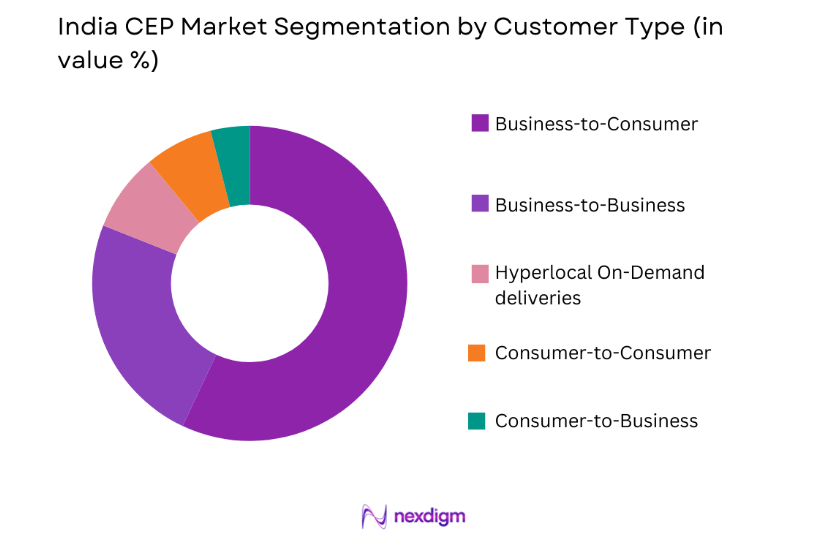

By Customer Type

India CEP market is segmented by Customer type into Business-to-Consumer, Business-to-Business, Consumer-to-Consumer, Consumer-to-Business, and Hyperlocal On-Demand deliveries. Recently, Business-to-Consumer has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. The segment benefits from sustained parcel creation by marketplaces, brand websites, social commerce sellers, and omnichannel retailers serving households across urban and semi-urban locations. CEP companies prioritize B2C capacity because shipment frequency is high, delivery density is improving, and merchants increasingly outsource fulfillment and reverse logistics. Wide geographic coverage, app-based tracking, cashless payment settlement, and structured return management make B2C shipments the most scalable and commercially significant flow within India’s organized parcel ecosystem.

Competitive Landscape

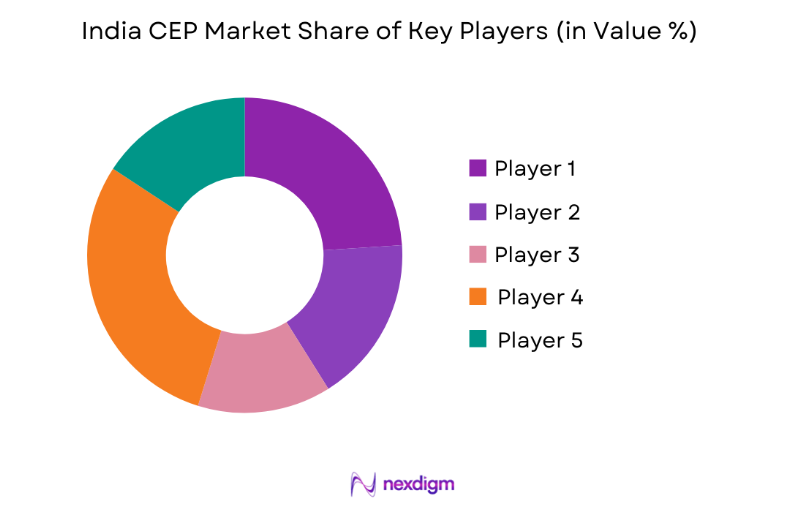

The India CEP market is moderately consolidated, with a few scaled domestic operators and global express companies exerting outsized influence over network standards, pricing discipline, technology adoption, and service levels. Delhivery’s integration of Ecom Express volumes underscores ongoing consolidation in the domestic parcel segment, while Blue Dart, DHL, FedEx, and UPS continue shaping premium express, enterprise, and international parcel flows through stronger automation, air connectivity, and large customer relationships. Competitive intensity remains high, but scale, data capabilities, and network density increasingly determine leadership.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | India CEP Focus |

| Delhivery | 2011 | Gurugram, India | ~ | ~ | ~ | ~ | ~ |

| Blue Dart Express | 1983 | Mumbai, India | ~ | ~ | ~ | ~ | ~ |

| DHL | 1969 | Bonn, Germany | ~ | ~ | ~ | ~ | ~ |

| FedEx | 1971 | Memphis, United States | ~ | ~ | ~ | ~ | ~ |

| UPS | 1907 | Atlanta, United States | ~ | ~ | ~ | ~ | ~ |

India CEP Market Analysis

Growth Drivers

Rapid expansion of e-commerce and marketplace-led parcel generation

India’s CEP market is being accelerated by the continuing rise of online retail platforms, direct-to-consumer brands, social commerce sellers, and omnichannel chains that create massive daily parcel flows across the country. Consumers increasingly expect dependable home delivery for categories such as apparel, electronics, beauty, grocery, healthcare, and essential household products, pushing merchants to rely on organized courier networks. CEP operators are responding by expanding sortation centers, dark stores, hub-and-spoke infrastructure, and technology-driven last-mile fleets across metropolitan and tier-two cities. Marketplace sale events, festive peaks, and high-frequency reorder categories have increased shipment density and improved route economics for parcel companies. Integrated tracking, return handling, COD reconciliation, and delivery promise management have made specialist CEP providers central to digital commerce operations. Rising merchant digitization among small businesses also broadens the addressable base for parcel logistics beyond large branded retailers. As more sellers move online and consumers continue shifting routine purchases to digital channels, shipment volumes remain structurally supported across domestic networks. This sustained order creation strengthens utilization, supports network expansion, and encourages continuing investment in technology, automation, and service-level upgrades by organized CEP providers serving both urban clusters and increasingly important semi-urban consumption centers.

Technology-led network optimization and faster service expectations

CEP operators in India are gaining market momentum by investing in automated sortation, route-planning software, shipment visibility tools, handheld delivery applications, and predictive analytics that improve speed and reliability. Customers now compare logistics brands on delivery assurance, real-time tracking, return convenience, and exception management rather than only basic transport. In response, companies are redesigning operating models around data-driven dispatch, dynamic rider allocation, and better line-haul coordination between origin hubs and destination centers. These investments reduce failed deliveries, lower turnaround time, improve utilization of fleets and hubs, and support premium services such as same-day and next-day delivery. Automation also helps companies manage scale during festive demand spikes without proportionate increases in manual overhead. Merchant clients benefit from better service integration through APIs, order management connectivity, and analytics that improve fulfillment planning. As service expectations rise across retail, healthcare, financial documents, and enterprise shipments, technology-enabled CEP networks become more attractive to both senders and recipients. The result is stronger customer retention, wider service differentiation, and higher operational resilience across India’s increasingly time-sensitive parcel ecosystem. This especially matters in large cities where congestion, address complexity, and narrow daily delivery windows reward operators with superior planning precision.

Market Challenges

High last-mile delivery costs and urban operating inefficiencies

CEP companies in India face persistent cost pressure because final-mile delivery remains labor intensive, congestion prone, and operationally fragmented across dense urban environments. Riders and vans must navigate traffic bottlenecks, inconsistent parking availability, gated communities, narrow streets, and repeated delivery attempts that reduce productivity per route. Same-day and next-day service promises intensify this burden by shrinking allowable delivery windows and limiting consolidation flexibility. Companies must therefore maintain larger fleets, extensive sortation infrastructure, and broad rider networks even when daily shipment demand fluctuates sharply. Fuel expenses, maintenance needs, and workforce incentives further elevate variable operating costs across large city networks. Reverse logistics adds another layer of complexity because returns require extra pickups, inspections, and routing adjustments that dilute margin performance. Although technology improves route planning, delivery economics remain difficult in low-density or highly variable service zones. This challenge is especially severe for operators balancing premium speed expectations with price-sensitive customers, since strong service levels do not always translate into proportionately higher yields or sustainable profitability. Network underutilization outside peak periods can further weaken asset efficiency, forcing companies to spread fixed infrastructure expenses across inconsistent shipment volumes, uneven route density, and shifting merchant demand.

Fragmented service quality and dependence on external delivery partner

A major challenge in India’s CEP market is maintaining consistent service quality across a vast geography that includes metros, tier-two cities, small towns, and remote delivery zones. Many operators rely on franchise partners, third-party agents, or gig-based delivery workforces to extend network reach quickly and economically. While this model improves coverage, it can create variability in pickup punctuality, handling standards, proof-of-delivery accuracy, and customer experience. High attrition among delivery personnel adds training costs and increases the risk of operational inconsistency during peak demand periods. Delivery exceptions caused by address ambiguity, customer unavailability, failed OTP verification, or localized staffing gaps can damage reliability metrics. Enterprises shipping high-value goods, regulated items, or time-sensitive documents often require tighter control than decentralized networks can always provide. The need to integrate thousands of service points, local partners, and customer touchpoints also complicates standardization of processes. As competition increases, even small quality lapses can shift merchant volumes toward rivals with stronger execution and more dependable network governance. Sustaining uniform quality therefore demands tighter audits, better training systems, improved partner incentives, and stronger digital controls that many smaller networks still struggle to implement consistently nationwide every day effectively.

Opportunities

Expansion of quick commerce, hyperlocal fulfillment, and scheduled same-day services

India’s CEP market has a major opportunity in serving merchants that require ultra-fast intra-city movement of parcels, essentials, and replenishment inventory. Quick commerce platforms, pharmacies, food-adjacent retailers, and neighborhood merchants are creating demand for pickup and delivery models built around short distances and compressed timelines. CEP companies can leverage existing urban hubs, rider fleets, and route intelligence to enter these segments with higher frequency services. Hyperlocal demand also encourages development of micro-warehousing, dark stores, and localized sortation nodes that improve delivery speed and reduce failed attempts. Beyond groceries, same-day services are becoming increasingly relevant for electronics accessories, beauty products, apparel exchanges, medical supplies, and urgent business documents. Operators that design profitable service tiers for scheduled windows, express intra-city movement, and merchant returns can diversify revenue beyond traditional inter-city parcels. This opportunity is especially attractive in densely populated cities where order velocity and delivery density can support better unit economics for organized networks. As consumers normalize paying for convenience and faster fulfillment, carriers that tailor service design, merchant integrations, and neighborhood capacity around repeat urban demand can capture incremental volumes while strengthening relationships with retailers seeking dependable local distribution partners nationwide.

Electrification, automation, and data-driven network redesign

India’s CEP market has a significant opportunity to improve margins and service quality through electric delivery fleets, automated sortation, and deeper use of network intelligence. Electric two-wheelers and compact cargo vehicles can lower fuel exposure, reduce maintenance intensity, and support sustainability commitments for large merchants and logistics operators. Automation within hubs enables faster parcel scanning, sorting accuracy, and throughput without equivalent increases in manual labor during seasonal peaks. Data-led network redesign also helps operators optimize route density, hub placement, delivery sequencing, and return flows across different city clusters. Merchants increasingly prefer logistics partners that provide transparent tracking, lower loss rates, and measurable environmental progress. CEP companies that combine automation with better analytics can improve service predictability while reducing unit handling costs. This creates room for differentiated offerings, stronger enterprise contracts, and better resilience against labor shortages and traffic-related disruption. The companies that invest early in these capabilities are likely to build more scalable operations across India’s rapidly formalizing parcel landscape. Supportive policy emphasis on logistics modernization and cleaner mobility further strengthens this opportunity, especially for organized players able to finance fleet transition, warehouse systems, software integration, and structured performance measurement across large networks nationally.

Future Outlook

The India CEP market is positioned for strong medium-term expansion as parcel intensity rises across e-commerce, quick commerce, healthcare, and enterprise distribution. Over the next five years, operators are likely to scale automated hubs, electric delivery fleets, and data-driven routing systems to improve speed and network economics. Policy support for logistics modernization and infrastructure connectivity should further strengthen service reach and transit reliability. On the demand side, wider digital commerce participation, denser urban order flows, and greater consumer preference for rapid fulfillment are expected to keep shipment volumes on a sustained upward path.

Major Players

- Blue Dart Express

- Delhivery

- DTDC Express

- FedEx

- DHL Express

- Ecom Express

- Shadowfax

- Xpressbees

- India Post

- Aramex India

- Gati Limited

- TCI Express

- Ekart Logistics

- Amazon Transportation Services

- UPS India

Key Target Audience

- E-commerce Retail Platforms

- Logistics and Supply Chain Companies

- Manufacturing and Industrial Enterprises

- Investments and venture capitalist firms

- Government and regulatory bodies

- Retail Distribution Companies

- Transportation Infrastructure Developers

Research Methodology

Step 1: Identification of Key Variables

Key variables for the India CEP market were identified through assessment of parcel volumes, customer categories, service formats, network density, delivery timelines, and technology usage across organized operators.

Special attention was given to e-commerce dependence, urban delivery intensity, reverse logistics, automation, and cross-border parcel activity.

This step created the base structure for evaluating market demand, service differentiation, and operational performance.

Step 2: Market Analysis and Construction

The market framework was constructed using trade publications, company disclosures, sector reports, logistics infrastructure updates, and parcel industry databases.

Qualitative and quantitative indicators were mapped across destination type, customer type, delivery models, and competitive positioning.

The resulting structure was used to align market size, segmentation, and competitive analysis into one coherent view.

Step 3: Hypothesis Validation and Expert Consultation

Working assumptions were tested against operating realities visible in public filings, industry commentary, and expert perspectives from logistics ecosystems. Validation focused on parcel growth drivers, network economics, city-level concentration, service quality challenges, and technology deployment patterns.

This stage improved consistency between market interpretation and on-ground business conditions.

Step 4: Research Synthesis and Final Output

All findings were consolidated into a final report through comparative review, analytical synthesis, and cross-verification of major data points. The output was organized to reflect market overview, segmentation, competition, opportunities, challenges, and future outlook in a structured format.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Rapid Growth of E-commerce and Online Retail Platforms

Expansion of Digital Payments and Online Shopping Ecosystem

Increasing Demand for Fast and Reliable Parcel Delivery Services - Market Challenges

High Operational Costs in Last-Mile Delivery

Urban Traffic Congestion and Delivery Delays

Fragmented Logistics Infrastructure in Rural Regions - Market Opportunities

Expansion of Express Delivery Services in Tier-II and Tier-III Cities

Adoption of Automation and Smart Parcel Sorting Systems

Growth of Cross-Border E-commerce Parcel Shipments - Trends

Increasing Use of Electric Vehicles for Urban Parcel Delivery

Growth of Micro-Fulfillment Centers and Urban Delivery Hubs - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Courier Services

Express Parcel Delivery

Standard Parcel Delivery

Same-Day Delivery Services

International Parcel Delivery - By Platform Type (In Value%)

Road-Based Parcel Delivery Networks

Air Express Logistics Platforms

Rail-Based Parcel Logistics Platforms

Integrated Multimodal Parcel Networks - By Fitment Type (In Value%)

Dedicated Courier Networks

Third-Party Logistics Parcel Services

Asset-Light Delivery Networks

Integrated E-commerce Fulfillment Services - By End User Segment (In Value%)

E-commerce and Online Retail Companies

Small and Medium Enterprises

Large Enterprises and Corporate Clients

- Market Share Analysis

- Cross Comparison Parameters (Delivery Network Coverage, Parcel Handling Capacity, Technology Integration Level, Delivery Speed and Reliability, Pricing Competitiveness, Sorting Infrastructure Capacity, Strategic Partnerships with E-commerce Platforms)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Blue Dart Express

Delhivery

Ecom Express

DTDC Express

XpressBees

Shadowfax

Amazon Transportation Services India

Flipkart Logistics

Gati Limited

DHL eCommerce India

FedEx Express India

UPS India

Safexpress

First Flight Couriers

India Post

- E-commerce Companies Driving High Parcel Volumes and Delivery Frequency

- SMEs Leveraging Courier Services for Nationwide Market Access

- Large Enterprises Outsourcing Parcel Logistics to Specialized CEP Providers

- Retail Businesses Expanding Omnichannel Delivery Models

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now