Download PDF

Download PDF Download PDF

Download PDFMarket Overview

India’s cold chain logistics sector has expanded significantly due to increasing demand for temperature-controlled supply chains across agriculture, pharmaceuticals, dairy, and processed foods. Based on a recent historical assessment, the India cold chain logistics market is valued at approximately USD ~ billion according to supply chain infrastructure assessments referenced by the Ministry of Food Processing Industries and the National Centre for Cold-chain Development. Market growth is driven by rising consumption of perishable food products, expansion of organized retail, pharmaceutical distribution requirements, and government initiatives supporting refrigerated storage and transportation infrastructure.

Cold chain logistics operations are concentrated in major agricultural and industrial hubs including Maharashtra, Gujarat, Uttar Pradesh, Punjab, and Tamil Nadu, where food processing industries and pharmaceutical manufacturing facilities operate extensively. Cities such as Mumbai, Delhi-NCR, Hyderabad, and Chennai function as major distribution centers due to their connectivity to ports, airports, and national highways. These locations host large cold storage warehouses, food processing clusters, and pharmaceutical logistics networks, supporting efficient movement of temperature-sensitive products.

Market Segmentation

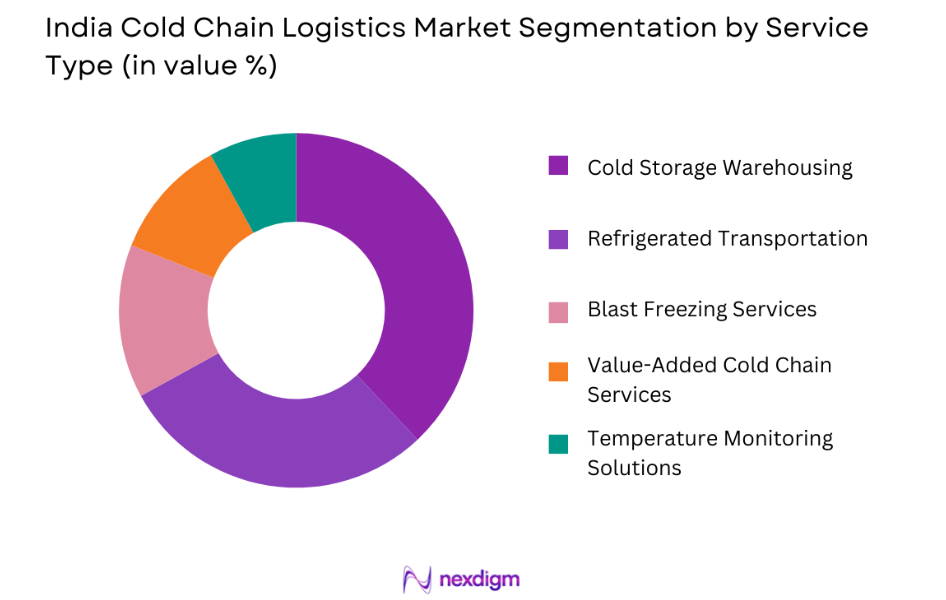

By Service Type

India Cold Chain Logistics market is segmented by Service type into refrigerated transportation, cold storage warehousing, blast freezing services, value-added cold chain services, and temperature monitoring solutions. Recently, cold storage warehousing has a dominant market share due to factors such as large agricultural production volumes, increasing food processing activities, and the need for long-term storage of perishable commodities. Cold storage facilities play a crucial role in maintaining product freshness and preventing post-harvest losses in fruits, vegetables, dairy products, and meat. Food processing companies and pharmaceutical distributors rely heavily on temperature-controlled warehouses to preserve product quality during storage and distribution. Government incentives supporting cold storage infrastructure development and private investment in large refrigerated warehouses further strengthen this segment’s dominance within the cold chain ecosystem.

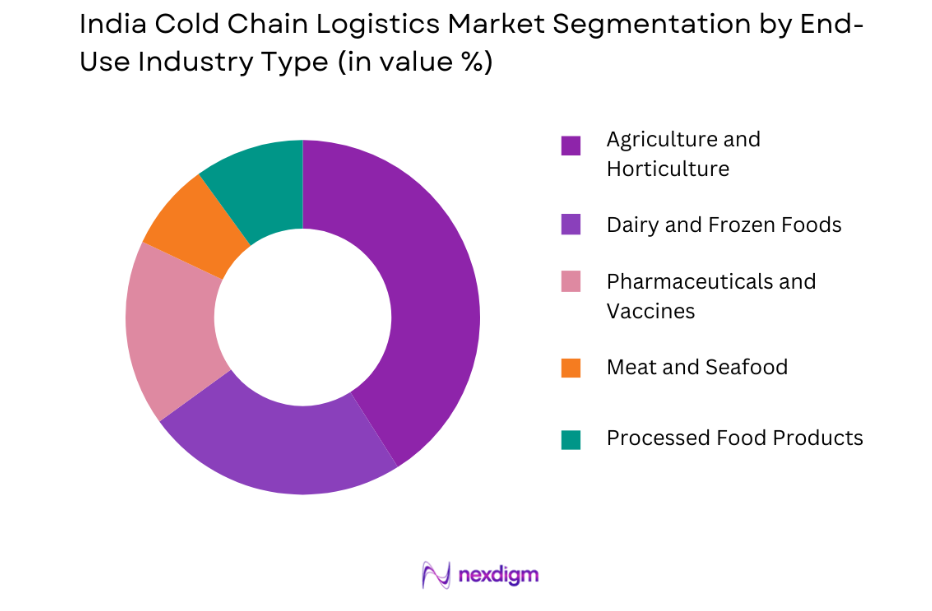

By End-Use Industry

India Cold Chain Logistics market is segmented by end-use industry into agriculture and horticulture, dairy and frozen foods, pharmaceuticals and vaccines, meat and seafood, and processed food products. Recently, agriculture and horticulture has a dominant market share due to factors such as high production volumes of fruits and vegetables, seasonal harvesting cycles, and the need to prevent post-harvest spoilage. Temperature-controlled storage facilities enable farmers and distributors to extend product shelf life and maintain quality before reaching wholesale markets or retail outlets. Large agricultural states require extensive cold chain infrastructure to manage crop supply and reduce food wastage during transportation. Food export operations also rely on cold storage and refrigerated transport to maintain product quality during international shipment. These factors collectively strengthen the role of agricultural supply chains in driving demand for cold chain logistics services.

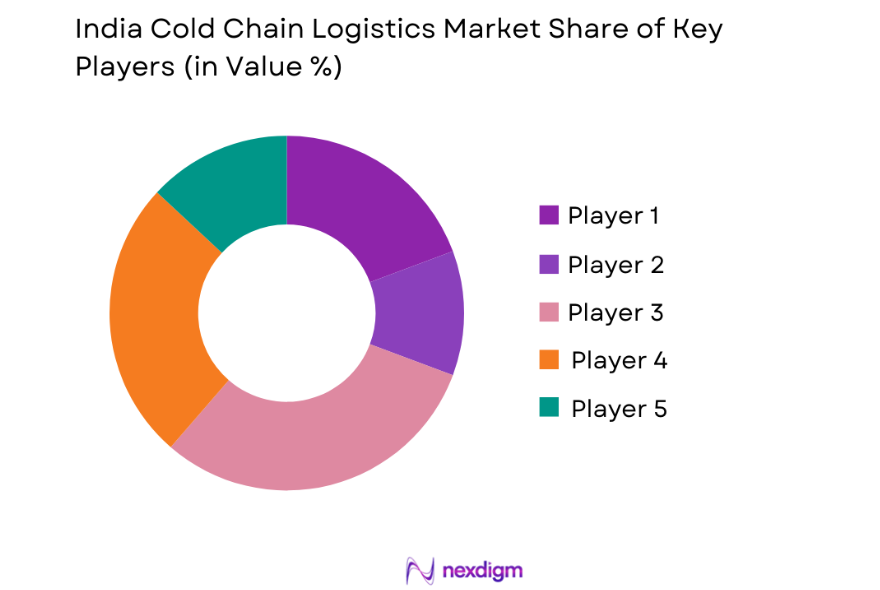

Competitive Landscape

The India cold chain logistics market consists of specialized logistics providers operating refrigerated warehouses, transportation fleets, and integrated cold storage networks. Competition is shaped by infrastructure scale, technology adoption, and nationwide distribution capabilities. Major players invest heavily in automated cold storage facilities, energy-efficient refrigeration systems, and temperature monitoring technologies to maintain product integrity. The market also experiences consolidation as large logistics providers acquire regional operators to strengthen their presence across agricultural and pharmaceutical supply chains.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Refrigerated Fleet Size |

| Snowman Logistics | 1993 | Bengaluru, India | ~ | ~ | ~ | ~ | ~ |

| ColdEX Logistics | 2009 | Gurugram, India | ~ | ~ | ~ | ~ | ~ |

| Gati Kausar | 2011 | Hyderabad, India | ~ | ~ | ~ | ~ | ~ |

| TCI Cold Chain Solutions | 2007 | Gurugram, India | ~ | ~ | ~ | ~ | ~ |

| Stellar Value Chain Solutions | 2016 | Gurugram, India | ~ | ~ | ~ | ~ | ~ |

India Cold Chain Logistics Market Analysis

Growth Drivers

Rapid Expansion of Organized Food Retail and Processed Food Consumption

The rapid expansion of organized retail chains and increasing consumption of processed food products has become a major growth driver for the India cold chain logistics market. Modern retail supermarkets and large food distribution companies require efficient temperature-controlled supply chains to maintain product freshness and quality throughout the distribution process. Rising urbanization and changing consumer lifestyles have significantly increased demand for frozen foods, dairy products, ready-to-eat meals, and packaged perishable goods. These products must be transported and stored within strict temperature ranges to prevent spoilage and maintain safety standards. Food processing companies therefore rely heavily on refrigerated transportation and cold storage facilities to distribute products across national markets. The expansion of quick commerce platforms and online grocery delivery services further strengthens the need for reliable cold chain logistics infrastructure. Retailers expect logistics providers to maintain uninterrupted temperature control across storage, transportation, and distribution stages. Investments in automated cold warehouses, digital temperature monitoring systems, and energy-efficient refrigeration technologies are becoming essential for logistics providers seeking to support modern food retail supply chains across India.

Government Initiatives Supporting Cold Chain Infrastructure Development

Government policies promoting agricultural supply chain modernization and food waste reduction have significantly strengthened the development of cold chain logistics infrastructure in India. Public sector initiatives led by the Ministry of Food Processing Industries encourage investment in refrigerated storage facilities and cold transportation networks. Programs supporting integrated cold chain projects provide financial incentives for building temperature-controlled warehouses, pack houses, and distribution centers near agricultural production zones. These initiatives aim to reduce post-harvest losses that occur due to inadequate storage and transportation infrastructure. Government support also encourages private logistics companies to expand cold storage capacity and adopt modern refrigeration technologies. Infrastructure development programs include improvements in rural connectivity and logistics corridors linking agricultural regions with urban consumption centers.

Market Challenges

High Infrastructure Investment and Operational Costs for Cold Storage Facilities

The India cold chain logistics market faces significant challenges related to the high capital investment required to build and operate refrigerated warehouses and transportation systems. Cold storage facilities require specialized refrigeration equipment, insulated storage structures, and continuous temperature monitoring technologies to maintain product safety. These infrastructure requirements substantially increase construction and operational costs compared with conventional warehouses. Additionally, energy consumption for refrigeration systems contributes significantly to operational expenses. Logistics providers must invest heavily in backup power systems to maintain uninterrupted temperature control during electricity outages. Maintenance and servicing of refrigeration equipment also add to operating costs, particularly in large cold storage facilities handling high volumes of perishable goods. Smaller logistics companies often struggle to finance these investments, limiting their ability to expand cold storage infrastructure. As a result, high capital expenditure requirements remain a major barrier to entry for new participants in the cold chain logistics market.

Fragmented Agricultural Supply Chains and Inefficient Distribution Networks

Fragmentation within India’s agricultural supply chains presents another major challenge for cold chain logistics development. Agricultural production in India involves millions of small-scale farmers who operate across diverse geographic regions. This fragmented production structure complicates the consolidation of agricultural products for efficient cold storage and transportation. Limited coordination between farmers, wholesalers, and logistics providers can lead to delays in moving perishable products to refrigerated storage facilities. Additionally, inadequate pack house infrastructure and limited access to refrigerated transport in rural areas contribute to product losses before reaching distribution centers. Inefficient distribution networks also increase transportation time and reduce overall supply chain efficiency. Cold chain operators must therefore invest in additional logistics infrastructure and coordination systems to ensure reliable product movement. Overcoming these structural challenges will require improved supply chain integration and better collaboration between agricultural producers and logistics providers.

Opportunities

Growing Pharmaceutical Cold Chain Requirements for Vaccines and Biologics

The increasing demand for temperature-sensitive pharmaceutical products presents a major opportunity for the India cold chain logistics market. Modern pharmaceutical supply chains rely on strict temperature control to preserve the effectiveness of vaccines, biologics, and specialized medicines. Pharmaceutical companies require refrigerated storage and transportation solutions capable of maintaining precise temperature ranges during distribution. The growth of biotechnology research and advanced drug development further increases the demand for reliable pharmaceutical cold chain logistics. Hospitals, laboratories, and vaccine distribution programs depend on efficient cold chain networks to ensure safe delivery of temperature-sensitive medicines. Logistics providers that specialize in pharmaceutical cold chain services can benefit from expanding partnerships with pharmaceutical manufacturers and healthcare institutions.

Expansion of Food Export Supply Chains Requiring Temperature-Controlled Logistics

The expansion of India’s agricultural and food export markets offers significant opportunities for cold chain logistics providers. International markets demand strict temperature control for the transportation of fruits, vegetables, seafood, dairy products, and processed foods. Export-oriented food companies require refrigerated logistics infrastructure capable of maintaining product quality during long-distance transportation and international shipping. Ports and airport cargo terminals are increasingly developing specialized cold storage facilities to support temperature-sensitive exports. Logistics providers that operate integrated cold chain networks can support exporters by offering end-to-end refrigerated logistics services from farm collection centers to export terminals. As global demand for Indian agricultural products continues to grow, the development of efficient cold chain infrastructure will become essential for maintaining export competitiveness and meeting international food safety standards.

Future Outlook

The India cold chain logistics market is expected to expand significantly as demand for temperature-controlled supply chains increases across food processing, pharmaceuticals, and agriculture. Technological advancements in refrigeration systems and digital temperature monitoring will improve logistics efficiency. Government incentives supporting cold storage infrastructure development will encourage private investment. Rising consumption of frozen foods, dairy products, and pharmaceutical products will further strengthen demand for cold chain services. These developments position India as one of the fastest-growing cold chain logistics markets globally.

Major Players

- Snowman Logistics

- ColdEX Logistics

- Gati Kausar

- TCI Cold Chain Solutions

- Stellar Value Chain Solutions

- DHL Supply Chain India

- Safexpress

- Dev Bhumi Cold Chain

- Agrostar Cold Chain

- Coldman Logistics

- Gubba Cold Storage

- Fresh and Healthy Enterprises

- InI Farms Cold Chain

- Om Logistics Cold Chain

- Future Supply Chain Solutions

Key Target Audience

- Cold chainlogisticsservice providers

- Food processing companies

- Pharmaceutical manufacturers

- Agricultural export companies

- Retail food distribution companies

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

The research process begins with identifying key variables influencing the India cold chain logistics market including agricultural production volumes, food processing demand, pharmaceutical distribution requirements, and logistics infrastructure availability. These variables help define the analytical framework for evaluating market development.

Step 2: Market Analysis and Construction

Primary industry statistics and secondary logistics infrastructure data are analyzed to construct the overall cold chain logistics market structure. Storage capacity, transportation networks, and distribution infrastructure are examined to determine market composition.

Step 3: Hypothesis Validation and Expert Consultation

Industry assumptions are validated through consultations with cold chain logistics operators, food processing companies, and pharmaceutical supply chain experts. These expert insights help refine market analysis and confirm realistic industry demand patterns.

Step 4: Research Synthesis and Final Output

Validated research findings are integrated into a comprehensive analytical framework that combines market segmentation, competitive landscape evaluation, and supply chain infrastructure analysis to produce the final market research report.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Rising Demand for Temperature-Controlled Logistics in Pharmaceuticals

Rapid Expansion of Organized Food Retail and E-commerce

Government Investments in Integrated Cold Chain Infrastructure - Market Challenges

High Capital Investment Requirements for Cold Storage Infrastructure

Energy Consumption and Power Reliability Issues

Fragmented Supply Chain and Limited Rural Cold Storage Facilities - Market Opportunities

Expansion of Vaccine and Biopharmaceutical Cold Chain Logistics

Development of Mega Food Parks and Integrated Cold Storage Hubs

Adoption of IoT-Based Temperature Monitoring Systems - Trends

Increasing Use of Automation and Real-Time Monitoring in Cold Storage

Growth of Specialized Pharmaceutical Cold Chain Logistics - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Cold Storage Warehousing

Refrigerated Transportation

Blast Freezing and Quick Freezing Systems

Temperature-Controlled Packaging Solutions

Inventory Monitoring and Tracking Systems - By Platform Type (In Value%)

Road-Based Cold Chain Logistics

Rail-Based Cold Chain Logistics

Air Cargo Cold Chain Logistics

Multimodal Cold Chain Logistics - By Fitment Type (In Value%)

Dedicated Cold Chain Logistics Services

Integrated Cold Chain Logistics Networks

Asset-Light Cold Chain Logistics Models

Third-Party Managed Cold Storage Solutions - By End User Segment (In Value%)

Food and Beverage Companies

Pharmaceutical and Healthcare Companies

Agriculture and Horticulture Producers

- Market Share Analysis

- Cross Comparison Parameters (Cold Storage Capacity, Refrigerated Transportation Fleet Size, Technology Integration Level, Geographic Distribution Network, Pricing Competitiveness, Value-Added Logistics Services, Compliance with Temperature Standards)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Snowman Logistics

Coldman Logistics

Gati Kausar

TCI Cold Chain Solutions

Allcargo Logistics

Blue Dart Express

Mahindra Logistics

Container Corporation of India

Future Supply Chain Solutions

Safexpress

DHL Supply Chain India

FedEx Logistics

Kuehne + Nagel India

CJ Darcl Logistics

ColdEX Logistics

- Pharmaceutical Companies Expanding Temperature-Controlled Distribution Networks

- Food Processing Companies Increasing Investment in Cold Storage Facilities

- Agricultural Producers Leveraging Cold Chains to Reduce Post-Harvest Losses

- E-commerce Grocery Platforms Driving Demand for Refrigerated Transportation

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now