Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The India Combine Harvester market is valued at approximately USD ~ billion based on a recent historical assessment derived from agricultural machinery production statistics and farm mechanization program expenditure data published by the Ministry of Agriculture and industry associations. Market expansion is primarily driven by mechanization subsidies, labor shortages during peak harvest seasons, and productivity gains from large-scale cereal cultivation. Increasing custom hiring center deployment and government-backed financing schemes have also strengthened demand for combine harvesters across major grain-producing states.

Dominant regions in the India Combine Harvester market include Punjab, Haryana, Uttar Pradesh, and Madhya Pradesh due to extensive wheat and rice cultivation, higher mechanization adoption, and strong rural credit penetration. Northern agricultural belts maintain leadership because of large contiguous farmland, established dealer networks, and custom hiring ecosystems. Southern states such as Andhra Pradesh and Telangana are expanding rapidly due to paddy mechanization programs and irrigation-supported multi-cropping patterns that necessitate efficient harvesting solutions.

Market Segmentation

By Product Type

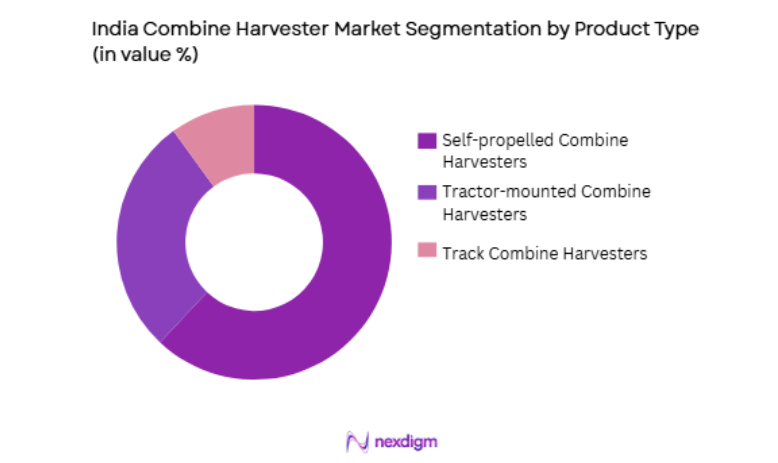

India Combine Harvester market is segmented by product type into self-propelled combine harvesters, tractor-mounted combine harvesters, and track combine harvesters. Recently, self-propelled combine harvesters has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Their dominance is supported by higher field efficiency, ability to operate across varied crop types, and suitability for custom hiring models prevalent in northern grain belts. Government mechanization subsidies favor high-capacity machines, while contractors prefer self-propelled units for multi-state seasonal migration, strengthening utilization rates and economic returns across harvesting cycles.

By Crop Type

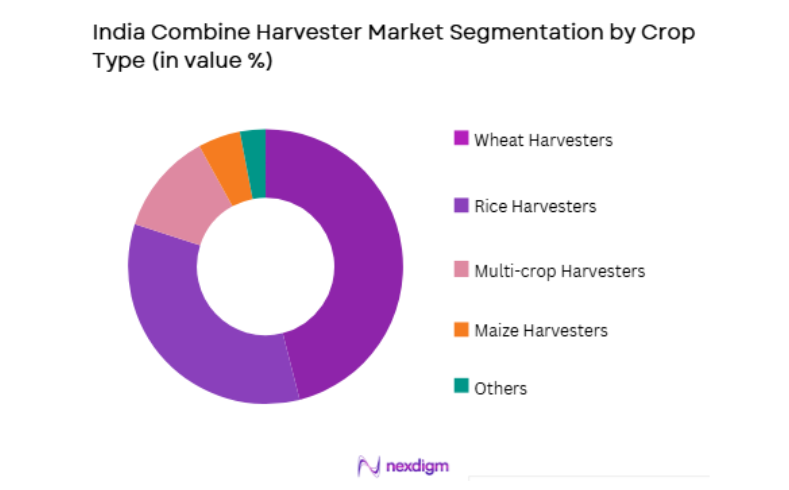

India Combine Harvester market is segmented by crop type into wheat harvesters, rice harvesters, multi-crop harvesters, maize harvesters, and others. Recently, wheat harvesters has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Wheat harvesting dominates because northern plains produce large contiguous wheat acreage requiring rapid mechanized harvesting to prevent yield losses. Seasonal harvesting windows are short, encouraging contractor-led machine deployment. Established machine designs optimized for wheat straw management and threshing efficiency further reinforce adoption, while procurement support prices maintain stable cultivation economics sustaining equipment utilization across core grain states.

Competitive Landscape

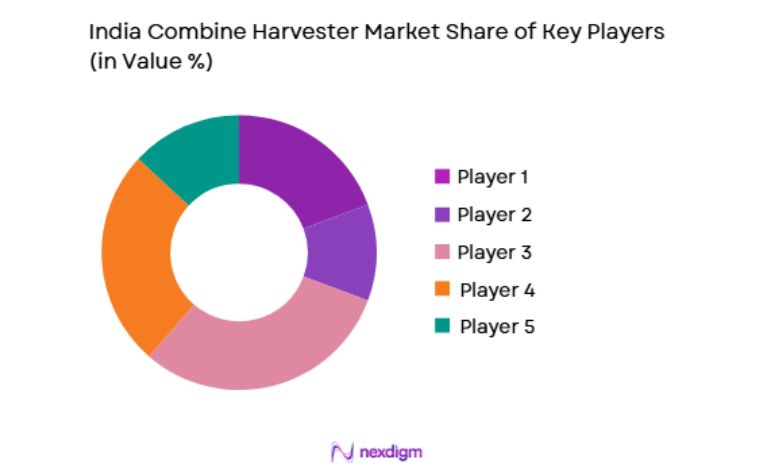

The India Combine Harvester market is moderately consolidated, with domestic manufacturers and joint ventures competing alongside global agricultural machinery brands. Regional specialists dominate wheat belt states through dealer penetration and custom hiring partnerships, while multinational firms emphasize advanced automation and emission-compliant engines. Competitive intensity is shaped by subsidy eligibility, aftersales service networks, and machine adaptability to diverse crop conditions.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Harvesting Capacity Range |

| Mahindra & Mahindra | 1945 | Mumbai, India | ~ | ~ | ~ | ~ | ~ |

| TAFE | 1960 | Chennai, India | ~ | ~ | ~ | ~ | ~ |

| Preet Agro | 1980 | Nabha, India | ~ | ~ | ~ | ~ | ~ |

| Claas India | 1913 | Harsewinkel, Germany | ~ | ~ | ~ | ~ | ~ |

| Kartar Agro | 1978 | Kapurthala, India | ~ | ~ | ~ | ~ | ~ |

India Combine Harvester Market Analysis

Growth Drivers

Government Mechanization Subsidy Programs and Custom Hiring Expansion

India Combine Harvester market growth is strongly supported by national and state mechanization schemes that subsidize combine purchases and promote shared access models through custom hiring centers. Subsidies reduce upfront acquisition costs, enabling small and medium farmers to access harvesting mechanization indirectly through contractors and cooperatives. Public funding has enabled deployment of harvesters across emerging mechanization regions beyond traditional wheat belts. Custom hiring centers improve machine utilization across seasons and crop cycles, improving operator profitability and fleet expansion. Financial institutions increasingly provide collateral-light credit products tailored for farm machinery contractors and rural entrepreneurs. State agriculture departments integrate combine harvesters into crop residue management programs to reduce stubble burning. Demonstration campaigns and mechanization extension services increase farmer awareness and adoption confidence across regions. Policy emphasis on labor productivity and timely harvesting further strengthens mechanized harvesting demand nationwide. These structural interventions collectively sustain long-term combine harvester penetration growth across India.

Seasonal Agricultural Labor Shortages and Rising Rural Wage Costs

India Combine Harvester market expansion is driven by structural labor scarcity during peak harvesting windows and sustained increases in rural wage costs across major grain-producing states. Migration patterns and alternative employment opportunities reduce seasonal farm labor availability during wheat and rice harvesting periods. Delayed manual harvesting directly affects grain quality, yield losses, and procurement schedules, incentivizing mechanized alternatives. Contractors offer predictable and faster harvesting services that align with procurement center timelines and crop insurance requirements. Large contiguous farm plots in northern states favor combine harvester deployment over manual harvesting methods. Mechanized harvesting also reduces post-harvest losses and improves grain recovery efficiency relative to traditional practices. Rural mechanization demand correlates with rising minimum support price procurement volumes that require rapid field clearance. Farmers increasingly view harvesting mechanization as risk mitigation against weather variability and labor uncertainty. These structural labor and cost dynamics sustain combine harvester adoption across India’s cereal production zones.

Market Challenges

Fragmented Land Holdings and Field Accessibility Constraints

India Combine Harvester market faces structural challenges from highly fragmented landholdings and irregular field geometries that limit machine maneuverability and operational efficiency in several agricultural regions. Small plot sizes reduce economic feasibility of direct combine ownership for individual farmers outside major grain belts. Narrow field access roads and uneven terrain constrain machine transport between farms in eastern and southern states. Custom hiring operators face logistical inefficiencies when servicing dispersed micro-plots across villages. Machine turning radius and header width requirements restrict operation in fragmented landscapes with boundaries and irrigation channels. Seasonal movement costs increase when harvesters must be transported long distances between scattered fields. Farmers with diversified cropping patterns may not achieve sufficient utilization to justify mechanized harvesting investments. Regional crop calendars vary, reducing continuous deployment opportunities across fragmented agricultural zones. These structural land and accessibility constraints slow combine harvester penetration outside consolidated farming regions in India.

High Capital Cost and Maintenance Complexity for Smallholders

India Combine Harvester market adoption is constrained by high capital acquisition costs and ongoing maintenance complexity that deter direct ownership among small and marginal farmers across most agricultural states. Combine harvesters require substantial upfront investment relative to farm income levels and seasonal utilization patterns. Specialized components such as threshing drums, cutting headers, and hydraulic systems demand skilled maintenance and periodic replacement. Spare parts availability and service technician access remain uneven across remote rural districts. Financing barriers persist where collateral requirements or credit histories limit machinery loans for smallholders. Fuel consumption and transport costs add to operational expenditure during multi-location harvesting operations. Off-season storage and preservation requirements increase ownership burden for individual farmers. Contractor models partially mitigate ownership barriers but reduce farmer control over harvesting schedules. These financial and technical barriers collectively limit combine harvester ownership diffusion among India’s fragmented smallholder farming population.

Opportunities

Expansion of Multi-Crop and Residue Management Compatible Harvesters

India Combine Harvester market opportunities are expanding through development of multi-crop harvesters and integrated residue management technologies aligned with evolving agricultural diversification and environmental regulations. Multi-crop capable machines allow contractors to harvest wheat, rice, maize, and pulses across multiple seasons, improving annual utilization. Residue management attachments support straw incorporation and collection, addressing stubble burning regulations in northern states. Government incentives increasingly favor harvesters compatible with crop residue management equipment. Diversified cropping systems in central and southern India require adaptable harvesting solutions beyond cereal specialization. Manufacturers are investing in modular header systems enabling crop switching without replacing entire machines. Contractors benefit from broader service offerings across varied crop calendars and regions. Environmental compliance programs encourage adoption of residue-friendly mechanization technologies. These technological adaptations expand combine harvester relevance beyond traditional wheat harvesting markets. Such innovations create sustained growth opportunities across India’s diversified agricultural landscapes.

Integration of Precision Agriculture and Automation Technologies

India Combine Harvester market growth opportunities are emerging from integration of precision agriculture, telematics, and semi-autonomous operation technologies that enhance productivity and contractor fleet management efficiency. Telematics systems enable real-time monitoring of machine performance, fuel consumption, and harvesting throughput across dispersed operations. Precision guidance and auto-steering improve harvesting accuracy and reduce grain losses during operation. Data analytics allow contractors to optimize route planning, field scheduling, and machine utilization across states. Automation reduces operator fatigue during long harvesting hours and improves operational consistency. Precision harvesting supports uniform grain quality and residue management compliance. Large-scale contractors increasingly adopt digitally enabled machines to differentiate services. Government digital agriculture initiatives support technology integration across mechanization equipment. Manufacturers are developing India-specific automation solutions adapted to crop conditions and field sizes. These advancements position technologically enabled combine harvesters as a high-value segment within India’s mechanization transition.

Future Outlook

The India Combine Harvester market is expected to experience steady expansion over the next five years driven by mechanization policy continuity, labor scarcity, and contractor-led service models. Technological developments including residue management compatibility and precision harvesting systems will reshape equipment preferences. Regulatory emphasis on crop residue management will accelerate replacement demand in northern grain states. Expansion into eastern and central agricultural regions through custom hiring ecosystems will broaden geographic adoption. Increasing farm consolidation and diversified cropping will further strengthen mechanized harvesting demand.

Major Players

- Mahindra & Mahindra

- John Deere India

- Escorts Kubota Limited

- CLAAS India

- Preet Agro Industries

- Kartar Agro Industries

- New Holland Agriculture India

- Kubota Agricultural Machinery India

- Dasmesh Mechanical Works

- Fieldking (Beri Udyog)

- Action Construction Equipment

- Manku Agro Tech

- Gomselmash India

- Yanmar Agricultural Machinery India

- Sonalika International Tractors

Key Target Audience

- Agricultural machinery manufacturers

- Farm equipment distributors

- Custom hiring service providers

- Agricultural cooperatives

- Investments and venture capitalist firms

- Government and regulatory bodies

- Rural financial institutions

- Large farming enterprises

Research Methodology

Step 1: Identification of Key Variables

Key variables included combine harvester production, sales volumes, mechanization subsidy disbursement, crop acreage under mechanized harvesting, contractor fleet size, and regional adoption intensity. Data sources comprised government mechanization programs, industry associations, and company disclosures. Variables were standardized to ensure comparability across regions and machine types.

Step 2: Market Analysis and Construction

Market size was constructed using bottom-up aggregation of machine sales, average transaction values, and contractor fleet expansion trends across states. Regional weighting reflected crop acreage and mechanization intensity. Cross-validation used subsidy allocation records and import–export machinery statistics.

Step 3: Hypothesis Validation and Expert Consultation

Assumptions regarding adoption drivers, regional dominance, and technology diffusion were validated through consultation with agricultural machinery dealers, contractor operators, and mechanization program officials. Feedback refined segmentation structure and growth dynamics interpretation across crop systems.

Step 4: Research Synthesis and Final Output

All quantitative and qualitative insights were synthesized into a structured market outlook integrating segmentation, competitive landscape, drivers, challenges, and opportunities. Consistency checks ensured alignment between mechanization trends, policy frameworks, and manufacturer strategies across India.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Rising agricultural mechanization supported by central and state subsidy programs

Seasonal farm labor shortages increasing demand for mechanized harvesting

Expansion of custom hiring centers improving equipment accessibility - Market Challenges

Fragmented landholdings limiting efficient utilization of large harvesters

High upfront acquisition costs for small and marginal farmers

Seasonal usage leading to low annual equipment utilization rates - Market Opportunities

Growth of shared mechanization and rental service business models

Integration of precision harvesting and telematics technologies

Export potential for cost-competitive Indian combine harvesters - Trends

Increasing adoption of tracked paddy combine harvesters in wetland regions

Shift toward higher horsepower and larger cutting width machines

Integration of yield monitoring and remote diagnostics features - Government regulations

Sub-Mission on Agricultural Mechanization subsidy framework

State-level farm mechanization assistance schemes

Agricultural machinery safety and emission compliance standards - SWOT analysis

- Porters 5 forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Self-Propelled Combine Harvesters

Tractor-Mounted Combine Harvesters

Tracked Combine Harvesters

Wheel-Type Combine Harvesters

Autonomous-Ready Combine Harvesters - By Platform Type (In Value%)

Paddy Combine Harvesters

Wheat Combine Harvesters

Maize Combine Harvesters

Multi-Crop Combine Harvesters

High-Capacity Field Combines - By Fitment Type (In Value%)

OEM Factory-Fitted Units

Aftermarket Retrofit Units

Custom Hiring Fleet Units

Cooperative-Owned Units

Leased Combine Units - By End User Segment (In Value%)

Large Commercial Farms

Farmer Producer Organizations

Custom Hiring Centers

- Market Share Analysis

- Cross Comparison Parameters (Engine Horsepower, Cutting Width, Grain Tank Capacity, Threshing Mechanism Type, Mobility Type, Crop Compatibility, Automation Level, Telematics Integration, Fuel Efficiency, Price Band)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Mahindra & Mahindra Farm Equipment Sector

TAFE Limited

John Deere India Pvt Ltd

CNH Industrial India Pvt Ltd

New Holland Agriculture India Pvt Ltd

Case IH India Pvt Ltd

CLAAS India Pvt Ltd

Kubota Agricultural Machinery India Pvt Ltd

Preet Agro Industries Pvt Ltd

Kartar Agro Industries Pvt Ltd

Dasmesh Mechanical Works Pvt Ltd

International Tractors Limited

SDF India Pvt Ltd

Gomselmash India Pvt Ltd

Captain Tractors Pvt Ltd

- Large farms prioritize high-capacity harvesters for operational efficiency

- Custom hiring centers drive utilization across smallholder regions

- Farmer cooperatives pool resources to access mechanization

- Contract harvesters influence seasonal regional demand patterns

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now