Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The India Counter IED market is estimated to be valued at USD~ billion, driven primarily by the increasing threat of terrorism and insurgencies within the region. Advancements in detection technologies, such as sensors and robotics, are playing a pivotal role in the market’s growth. Additionally, the Indian government is heavily investing in military modernization, particularly in counter-terrorism measures and securing critical infrastructure, which further propels demand for counter IED solutions.

India remains a dominant player in the Counter IED market, with significant investment in defense technology and collaboration with international allies. The country’s emphasis on enhancing its defense capabilities against regional security threats, particularly from neighboring countries, has strengthened its position. Strategic cities like New Delhi, Mumbai, and Bangalore are central to the development and deployment of counter IED systems, driven by the presence of defense contractors, government agencies, and defense research organizations.

Market Segmentation

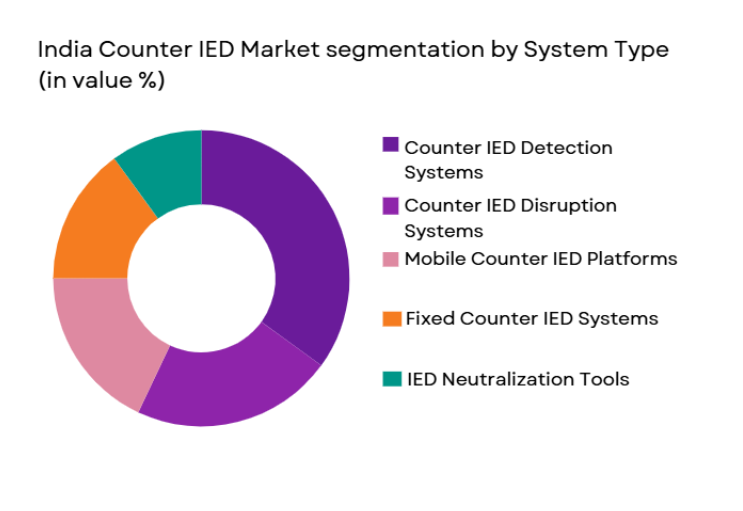

By System Type

The India Counter IED market is segmented by system type into counter IED detection systems, counter IED disruption systems, mobile counter IED platforms, fixed counter IED systems, and IED neutralization tools. The dominant sub-segment in this market is counter IED detection systems, due to the growing need for advanced detection capabilities to identify explosive threats in real-time. The rise in urbanization and the increase in terrorist activities have driven the demand for highly sophisticated and reliable detection systems. As security challenges evolve, there is a significant emphasis on integrating the latest technologies such as radar, sensors, and artificial intelligence for detecting IEDs, particularly in high-risk areas like borders, military zones, and urban centers.

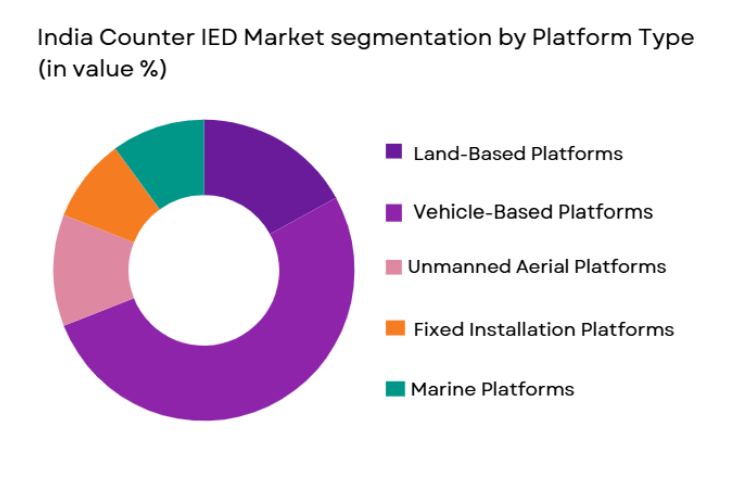

By Platform Type

The market is segmented by platform type into land-based platforms, vehicle-based platforms, unmanned aerial platforms, fixed installation platforms, and marine platforms. Vehicle-based platforms dominate the market, driven by their mobility and adaptability to various terrains and environments. These platforms are equipped with advanced counter IED systems that enhance the operational flexibility of military forces. Vehicle-based systems provide rapid response capabilities, making them ideal for use in both urban and rural settings. Their growing presence is particularly seen in defense operations, where real-time, high-stakes countermeasures are required to neutralize IED threats effectively.

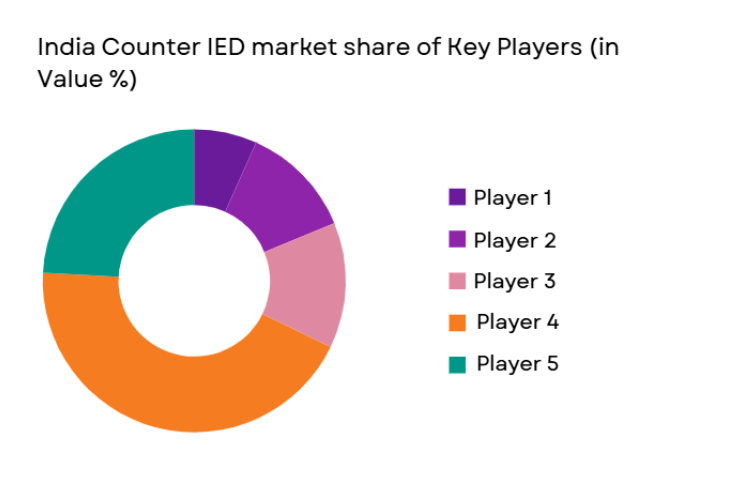

Competitive Landscape

The competitive landscape of the India Counter IED market is influenced by both domestic and international players. Key players, including Rheinmetall Defence, Thales Group, and BAE Systems, continue to dominate through their innovation in countermeasures and detection technologies. These companies have established strong footholds due to their ability to offer comprehensive counter IED solutions, often partnering with local defense contractors to ensure the systems meet India’s specific operational requirements. The market is characterized by heavy investments in R&D and a focus on upgrading and enhancing the capabilities of existing systems.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD) | Additional Market-Specific Parameter |

| Rheinmetall Defence | 1889 | Düsseldorf, Germany | ~ | ~ | ~ | ~ | ~ |

| Thales Group | 2000 | Paris, France | ~ | ~ | ~ | ~ | ~ |

| BAE Systems | 1999 | London, UK | ~ | ~ | ~ | ~ | ~ |

| Lockheed Martin | 1912 | Bethesda, USA | ~ | ~ | ~ | ~ | ~ |

| Northrop Grumman | 1939 | Falls Church, USA | ~ | ~ | ~ | ~ | ~ |

India Counter IED Market Analysis

Growth Drivers

Rising Security Threats and Terrorism

The India Counter IED market is experiencing significant growth due to the increasing threat of terrorism and insurgent activities in the region. As terrorist organizations increasingly use IEDs to target military and civilian infrastructure, India is investing heavily in technologies to counteract these devices. The growing instability in neighboring countries, particularly along the border regions, further exacerbates the need for advanced countermeasures. As such, the Indian government is allocating more resources to enhance its defense infrastructure, thereby driving demand for counter IED solutions. Additionally, the expanding scope of security threats to critical infrastructure and public safety has led to greater emphasis on IED detection and neutralization systems.

Government Investment in Defense and Security

The Indian government’s focus on strengthening its defense capabilities is a major growth driver for the Counter IED market. With the increasing importance of national security, India is continuously modernizing its military forces, and counter-terrorism efforts are central to these initiatives. The government has been ramping up its defense budget, particularly for advanced military technologies such as counter IED detection systems, mobile platforms, and neutralization technologies. This significant investment is enhancing the country’s ability to protect against IEDs, and it is expected that future funding will continue to fuel the market’s expansion. The strategic importance of countering insurgencies and securing critical infrastructure is driving long-term government support for the sector.

Market Challenges

High Cost of Advanced Counter IED Solutions

One of the primary challenges facing the India Counter IED market is the high cost of advanced counter IED systems. These systems require specialized technology, high-quality materials, and significant research and development efforts, which all contribute to their elevated price. The substantial costs associated with procurement, installation, and maintenance can limit the accessibility of these technologies, particularly for smaller or less-funded organizations. While the government is making considerable investments, budget constraints at local and regional levels could pose challenges in scaling up the adoption of these technologies across the country. Additionally, the financial burden of continuous upgrades and technological advancements remains a significant concern for stakeholders in the defense sector.

Integration of Advanced Technologies

The complexity of integrating advanced counter IED systems into existing defense infrastructures presents another significant challenge in the market. As the nature of IED threats evolves, there is a growing need for advanced sensors, communication systems, and data processing technologies that can work seamlessly together. However, ensuring compatibility and integration with legacy systems is often difficult, particularly in a country with a large and varied defense infrastructure like India. The rapid pace of technological innovation also means that systems can quickly become outdated, and keeping up with the latest advancements while maintaining operational efficiency is a significant challenge. Integration of new systems with older ones can result in inefficiencies, reduced system performance, and increased costs.

Opportunities

Expansion of Autonomous Counter IED Systems

One of the major opportunities in the India Counter IED market is the growing development and deployment of autonomous counter IED systems. With advancements in artificial intelligence, robotics, and unmanned systems, autonomous vehicles and drones are becoming increasingly capable of detecting, disrupting, and neutralizing IEDs. These systems offer significant advantages, including improved operational efficiency, greater mobility, and the ability to operate in high-risk environments. India’s military forces and law enforcement agencies are increasingly adopting autonomous systems for their ability to handle threats without putting human personnel at risk. As the technology matures, this segment is expected to experience significant growth, presenting a major opportunity for companies in the market.

Increased Demand for Mobile and Flexible Counter IED Solutions

As the nature of security threats continues to evolve, there is an increasing demand for mobile and flexible counter IED solutions. Mobile platforms, including vehicles and drones, offer the agility and adaptability required to handle a wide range of IED threats in different environments. These solutions provide rapid response capabilities, allowing defense agencies to quickly deploy countermeasures in areas of concern. The growing need for such flexible solutions presents an opportunity for manufacturers to develop and supply advanced mobile counter IED systems. As urban and rural security needs shift, mobile counter IED systems will become an increasingly integral part of India’s national defense strategy.

Future Outlook

The India Counter IED market is expected to grow significantly in the coming years, driven by advances in detection technologies and the increased focus on counter-terrorism and national security. With the government’s continued investment in military modernization and the growing demand for mobile, autonomous, and integrated counter IED solutions, the market is poised for strong expansion. Technological advancements, particularly in artificial intelligence and robotics, will enhance the effectiveness and efficiency of counter IED systems, contributing to the development of new solutions that can address emerging threats. Regulatory support and defense collaborations are expected to further bolster market growth, ensuring the continued enhancement of India’s counter IED capabilities.

Major Players

- Rheinmetall Defence

- Thales Group

- BAE Systems

- Lockheed Martin

- Northrop Grumman

- General Dynamics

- L3 Technologies

- Leonardo

- Saab AB

- Elbit Systems

- Israel Aerospace Industries

- QinetiQ

- FLIR Systems

- Textron Systems

- Harris Corporation

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Defense contractors

- Private security firms

- Military and law enforcement agencies

- Defense equipment manufacturers

- Border security agencies

- Counter-terrorism units

Research Methodology

Step 1: Identification of Key Variables

Identification of the key factors influencing the India Counter IED market, including technological trends, security threats, and procurement patterns.

Step 2: Market Analysis and Construction

Analysis of current market trends, competitor landscape, and consumer needs, utilizing primary and secondary research sources.

Step 3: Hypothesis Validation and Expert Consultation

Consultation with defense experts, industry professionals, and key stakeholders to validate assumptions and market forecasts.

Step 4: Research Synthesis and Final Output

Consolidation of research findings into a comprehensive report, presenting market insights, forecasts, and strategic recommendations.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Increase in Terrorism and Security Threats

Advancements in Detection and Neutralization Technologies

Government Investment in Defense and Security - Market Challenges

High Cost of Advanced Counter IED Systems

Technological Integration Complexities

Limited Interoperability Among Systems - Market Opportunities

Expansion of Defense Partnerships and Alliances

Advancements in Autonomous Counter IED Systems

Growing Demand for Mobile Counter IED Solutions - Trends

Deployment of AI and Robotics for IED Detection

Increased Use of Drones for Counter IED Operations

Growth in Demand for Portable Counter IED Devices

Advancements in Automated Neutralization Technologies

Government Regulations Supporting Counter IED Technologies - Government Regulations & Defense Policy

Implementation of National Counter IED Standards

Strengthening International Defense Cooperation

New Regulations for IED Detection and Neutralization - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Counter IED Detection Systems

Counter IED Disruption Systems

Mobile Counter IED Platforms

Fixed Counter IED Systems

IED Neutralization Tools - By Platform Type (In Value%)

Land-Based Platforms

Vehicle-Based Platforms

Unmanned Aerial Platforms

Fixed Installation Platforms

Marine Platforms - By Fitment Type (In Value%)

Integrated Systems

Modular Systems

Standalone Devices

Mobile Systems

Portable Systems - By EndUser Segment (In Value%)

National Defense Forces

Law Enforcement Agencies

Private Security Contractors

International Organizations

Government Bodies - By Procurement Channel (In Value%)

Direct Government Procurement

Defense Contractors

International Defense Alliances

Private Sector Procurement

Custom Shipbuilders - By Material / Technology (In Value%)

Advanced Sensors

Electronic Countermeasure Technologies

Robotics and AI Integration

Explosive Detection Systems

Wireless Communication Technologies

- Market structure and competitive positioning

- Market share snapshot of major players

- CrossComparison Parameters (Technology Integration, Deployment Capabilities, Cost-effectiveness, Range of Operation, System Flexibility, Maintenance and Support, User Training, Customization Capabilities, After-sales Service)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

Rheinmetall Defence

Thales Group

BAE Systems

Lockheed Martin

Northrop Grumman

General Dynamics

L3 Technologies

Leonardo

Saab AB

Elbit Systems

Israel Aerospace Industries

QinetiQ

FLIR Systems

Textron Systems

Harris Corporation

- Integration of AI in IED Detection

- Collaborative Counter IED Programs with Allies

- Increased Procurement from Defense Contractors

- Technological Upgrades in Existing IED Systems

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now