Download PDF

Download PDFMarket Overview

The India Dairy Free Ice Cream Market was valued at approximately USD ~ million in 2024 and has emerged as one of the fastest-growing segments within the broader plant-based food industry. The market is supported by the rapid expansion of India’s vegan and flexitarian consumer base, rising awareness regarding lactose intolerance, and increasing adoption of health-focused food products. India’s population increased from 1.43 billion to 1.45 billion, while private final consumption expenditure exceeded USD 2.4 trillion, supporting demand for premium and specialty food categories. The growth of organized retail, quick-commerce platforms, and direct-to-consumer food brands has further improved accessibility of dairy-free frozen desserts. Product innovation across coconut, almond, oat, soy, and cashew-based formulations has broadened consumer appeal and strengthened category expansion across metropolitan and tier-I cities.

Market Segmentation

By Base Ingredient Type

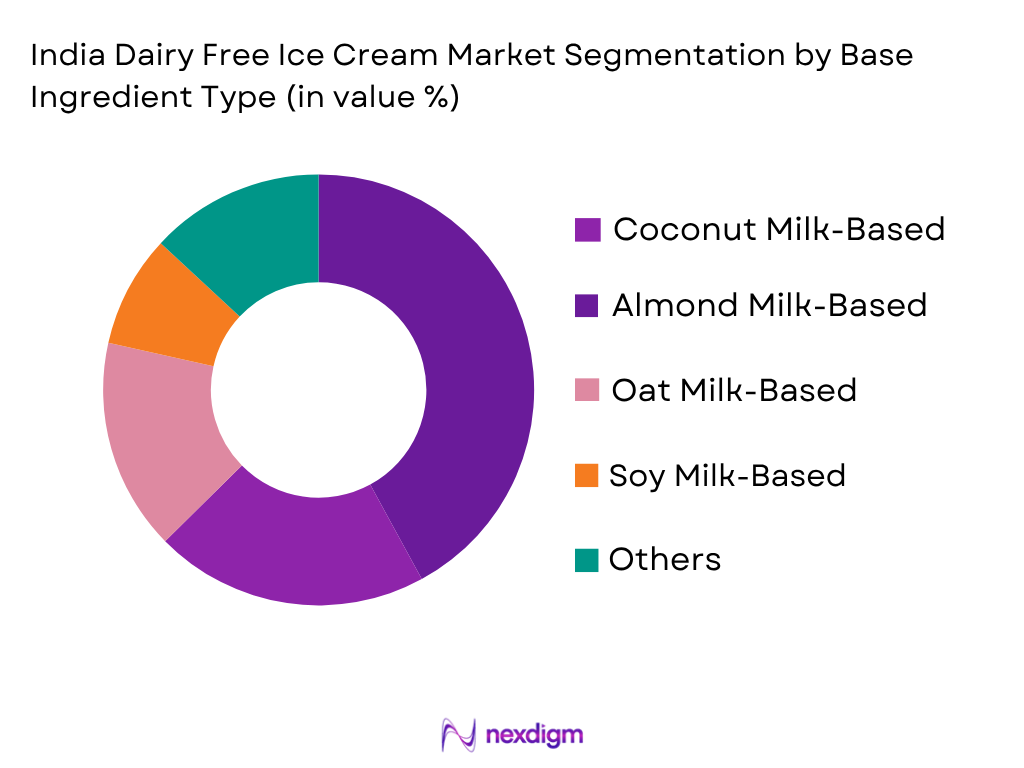

India Dairy Free Ice Cream Market is segmented by plant-based base type into coconut milk-based ice cream, almond milk-based ice cream, oat milk-based ice cream, soy milk-based ice cream, cashew milk-based ice cream, pea protein-based ice cream, and mixed plant-based formulations. Recently, coconut milk-based ice cream has a dominant market share under this segmentation due to its strong compatibility with Indian taste preferences and abundant local availability of coconut-derived ingredients. Coconut-based formulations offer a naturally creamy texture, making them one of the easiest substitutes for conventional dairy ice cream. Indian consumers are already familiar with coconut-based food products, particularly in southern and western regions, which supports faster adoption. Manufacturers also benefit from relatively stable domestic sourcing compared to imported alternatives such as almonds and oats. Brands increasingly utilize coconut milk as a base for premium, vegan, and lactose-free frozen desserts because it complements both traditional Indian flavors and international flavor profiles. These advantages have strengthened coconut milk’s leadership position within the Indian dairy-free ice cream category.

By Distribution Channel

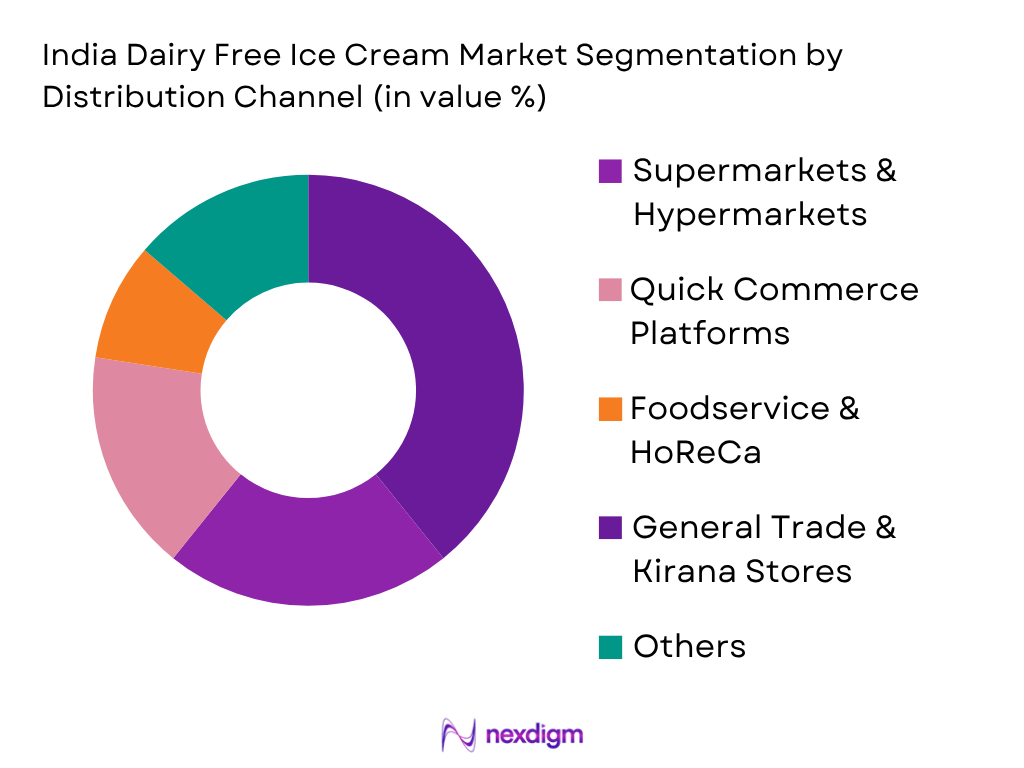

India Dairy Free Ice Cream Market is segmented by distribution channel into supermarkets & hypermarkets, general trade & kirana stores, convenience stores, health & organic retail stores, online retail platforms, quick commerce platforms, foodservice establishments, and dessert chains. Recently, supermarkets and hypermarkets have a dominant market share under this segmentation due to their extensive product assortment, superior cold-chain infrastructure, and growing presence across metropolitan and tier-I cities. Retail chains such as Reliance Fresh, Nature’s Basket, Spencer’s, Star Bazaar, and DMart provide consumers with access to a wide range of dairy-free frozen desserts from both domestic and international brands. These stores often dedicate specific sections to vegan and health-focused products, improving visibility and encouraging trial purchases. In addition, consumers prefer supermarkets because they allow product comparison, promotional purchases, and access to premium imported offerings. The rapid expansion of organized retail in India continues to support the dominance of supermarkets and hypermarkets within the dairy-free ice cream distribution ecosystem.

Competitive Landscape

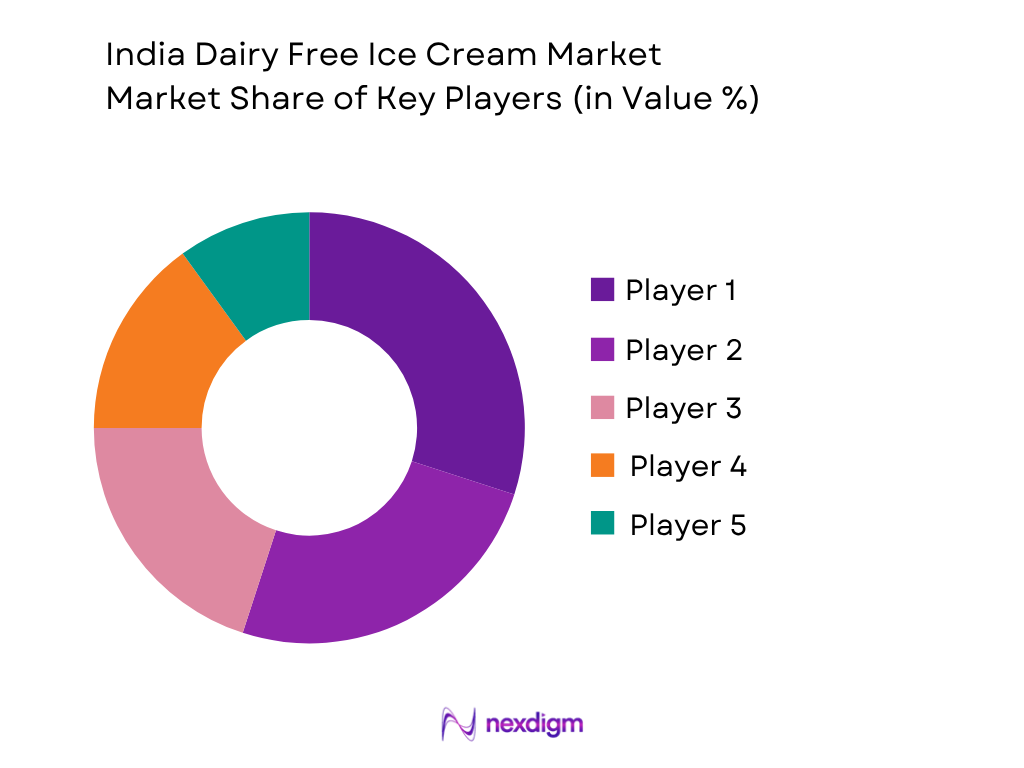

The India Dairy Free Ice Cream Market remains relatively fragmented and is characterized by competition among plant-based food startups, premium frozen dessert manufacturers, international brands, and emerging direct-to-consumer companies. Market participants are focusing on product innovation, vegan certifications, premium flavor offerings, clean-label formulations, and omnichannel distribution strategies. The category continues to attract new entrants due to increasing consumer demand for plant-based alternatives and premium frozen desserts.

| Company | Establishment Year | Headquarters | Plant-Based Base Portfolio | Dairy-Free SKU Count | Distribution Reach | Premium Product Portfolio | Vegan Certification | Packaging Sustainability |

| NOTO Ice Cream | 2019 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| Go Zero | 2022 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| Minus 30 | 2017 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| White Cub | 2018 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| Oatly Frozen Desserts | 1994 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

India Dairy Free Ice Cream Market Analysis

Growth Drivers

Rising Urbanization, Disposable Income Growth, and Premium Food Consumption

The India Dairy Free Ice Cream Market is benefiting significantly from rapid urbanization and rising household purchasing power. India’s urban population exceeded 536 million people and continues to expand as consumers increasingly shift toward organized retail and premium food products. According to IMF estimates, India’s nominal GDP crossed USD 4.1 trillion in 2024, while GDP per capita exceeded USD 2,900, supporting greater discretionary spending on health-focused and premium frozen desserts. Private Final Consumption Expenditure remained above USD 2.4 trillion, reflecting strong household demand across food and beverage categories. Additionally, India’s total population exceeded 1.45 billion, creating one of the world’s largest consumer bases for emerging food categories. The rapid expansion of modern retail chains, premium grocery stores, and food delivery platforms has improved product accessibility in metropolitan cities such as Mumbai, Bengaluru, Delhi NCR, Hyderabad, and Pune. Growing exposure to global food trends, increasing participation of younger consumers in premium food categories, and higher spending on lifestyle-oriented products are accelerating the adoption of dairy-free frozen desserts. As plant-based food awareness rises alongside urban consumption patterns, dairy-free ice cream is increasingly transitioning from a niche category to a mainstream premium food segment.

Expanding Plant-Based Food Ecosystem and Health-Conscious Consumer Behavior

The India Dairy Free Ice Cream Market is also driven by the rapid development of the plant-based food ecosystem and increasing consumer focus on health and wellness. India’s healthcare expenditure exceeded USD 110 billion, reflecting rising awareness regarding nutrition and preventive health. The country maintains a labor force exceeding 590 million people, supporting a large working-age population with growing purchasing power and exposure to wellness-oriented food products. India is also one of the largest consumers of plant-based ingredients such as coconut, cashew, and soy, providing manufacturers with access to raw materials that can support dairy-free product development. Internet users exceeded 950 million, facilitating awareness of vegan lifestyles, lactose-free alternatives, and plant-based nutrition through digital platforms and social media. Furthermore, food processing output continues to expand under government-supported manufacturing initiatives, strengthening the availability of innovative food products across retail channels. Consumers are increasingly seeking alternatives that align with digestive health concerns, clean-label preferences, and sustainability goals. This shift in dietary behavior has encouraged manufacturers to launch dairy-free ice creams featuring coconut milk, almond milk, oat milk, and cashew milk formulations, thereby strengthening category growth and product diversification.

Market Challenges

Limited Cold Chain Infrastructure and Distribution Constraints

The India Dairy Free Ice Cream Market continues to face challenges associated with cold chain infrastructure limitations and fragmented distribution networks. Although India possesses one of the world’s largest food supply chains, refrigerated logistics infrastructure remains uneven across regions. The country has more than 12,000 cold storage facilities, but a significant proportion is concentrated in agricultural production clusters rather than premium frozen food distribution networks. India’s geographical area of approximately 3.28 million square kilometers creates logistical complexity for temperature-sensitive products such as dairy-free frozen desserts. While metropolitan cities benefit from advanced cold-chain systems, penetration remains limited across many tier-II, tier-III, and rural markets. Additionally, organized retail accounts for only a portion of India’s total retail ecosystem, with millions of small independent outlets lacking adequate freezer capacity for premium frozen products. The challenge becomes more pronounced for dairy-free ice cream manufacturers that require strict temperature management to maintain product texture and quality. As companies seek nationwide expansion, investments in refrigerated transportation, storage infrastructure, and last-mile delivery capabilities remain critical for ensuring consistent product availability and minimizing supply chain losses.

Premium Product Positioning and Limited Consumer Awareness Beyond Metro Markets

The dairy-free ice cream category faces challenges related to consumer awareness and premium product positioning. India’s per capita income remains significantly lower than many developed markets despite GDP growth, resulting in strong price sensitivity among consumers. Traditional dairy ice cream remains deeply embedded within Indian consumption habits due to widespread availability and familiarity. Furthermore, India’s food retail sector includes over 13 million retail outlets, many of which prioritize fast-moving and affordable products rather than emerging premium food categories. Awareness of vegan diets, lactose intolerance, and dairy-free alternatives remains concentrated within metropolitan regions such as Mumbai, Bengaluru, Delhi NCR, and Hyderabad. Outside these urban centers, consumer understanding of plant-based frozen desserts remains relatively limited. Manufacturers must therefore invest significantly in education, product sampling, and marketing initiatives to build category awareness. Additionally, competition from conventional ice cream brands, frozen desserts, and other indulgent snack categories creates barriers to adoption. These factors can slow market penetration despite growing interest in health-conscious and plant-based food products.

Market Opportunities

Expansion of Quick Commerce and Digital Grocery Ecosystems

The rapid growth of India’s digital commerce ecosystem presents a substantial opportunity for the dairy-free ice cream market. India has more than 950 million internet users and over 650 million smartphone users, creating one of the world’s largest digital consumer markets. Unified Payments Interface (UPI) transactions exceeded 170 billion transactions annually, reflecting widespread adoption of digital commerce and cashless payments. Quick commerce platforms such as Blinkit, Zepto, Instamart, and BigBasket have significantly improved accessibility for premium frozen food products by enabling rapid delivery within urban markets. India’s e-commerce sector continues to expand rapidly, supported by rising internet penetration and increasing consumer comfort with online grocery purchases. Dairy-free ice cream brands can leverage these platforms to reach health-conscious consumers without relying solely on traditional retail networks. Digital channels also enable targeted marketing, subscription-based purchasing models, and direct consumer engagement. The combination of growing online grocery adoption, improved cold-chain delivery capabilities, and expanding urban consumer demand creates a favorable environment for dairy-free frozen dessert brands to increase market penetration and strengthen brand visibility.

Growing Demand for Functional, Clean Label, and Plant-Based Nutrition Products

The increasing demand for functional nutrition products creates significant growth opportunities for dairy-free ice cream manufacturers. India’s food processing sector contributes more than USD 400 billion to the economy and continues to expand through investments in value-added food categories. The country produces over 239 million tonnes of horticultural crops, providing access to fruit ingredients, natural sweeteners, and plant-based raw materials suitable for premium frozen dessert innovation. Rising consumer interest in health-focused products has encouraged demand for foods containing added protein, fiber, vitamins, probiotics, and reduced sugar content. India’s young demographic profile, with more than 900 million people below the age of 35, supports experimentation with innovative food categories and wellness-oriented products. Manufacturers are increasingly introducing clean-label formulations free from artificial additives while emphasizing plant-based nutrition and sustainability attributes. The combination of increasing health awareness, expanding modern retail penetration, and growing acceptance of premium food products creates a strong foundation for the development of functional dairy-free ice creams tailored to evolving Indian consumer preferences.

Future Outlook

The India Dairy Free Ice Cream Market is expected to witness robust growth over the forecast period owing to increasing awareness of plant-based nutrition, growing incidence of lactose intolerance concerns, and rising demand for premium frozen desserts. Expanding quick-commerce penetration, greater availability of vegan products, and continuous innovation in alternative protein ingredients are expected to support category growth. The market is also likely to benefit from increasing urbanization, rising disposable incomes, and growing consumer interest in sustainable food consumption. Manufacturers are expected to focus on localized flavors, nutritional enhancements, and wider distribution reach. The market is projected to register a CAGR of ~% during 2026–2035.

Major Players

- NOTO Ice Cream

- Go Zero

- Minus 30

- White Cub

- Sequel Foods (Zero Ice Cream)

- Baskin Robbins Non-Dairy Range

- London Dairy Dairy-Free

- Oatly Frozen Desserts

- Ben & Jerry’s Non-Dairy

- Magnum Vegan

- Häagen-Dazs Non-Dairy

- Coconut Bliss

- Goodmylk

- Urban Platter Plant-Based Frozen Desserts

- Nature’s Basket Private Label Plant-Based Desserts

Key Target Audience

- Dairy-Free Ice Cream Manufacturers

- Plant-Based Food & Beverage Companies

- Frozen Dessert Manufacturers

- Modern Retail and Supermarket Chains

- Quick Commerce and E-Commerce Platforms

- Foodservice and HoReCa Operators

- Investments and Venture Capitalist Firms

- Government and Regulatory Bodies (Food Safety and Standards Authority of India (FSSAI), Ministry of Food Processing Industries (MoFPI), Department for Promotion of Industry and Internal Trade (DPIIT))

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map encompassing all major stakeholders within the India Dairy Free Ice Cream Market. This step is supported by extensive desk research using secondary databases, company reports, trade publications, retail audits, and industry sources. The objective is to identify critical variables influencing demand, supply, pricing, distribution, and consumer purchasing behavior.

Step 2: Market Analysis and Construction

In this phase, historical market data is compiled and analyzed to assess product penetration, retail availability, consumption patterns, and revenue generation. Demand-side assessments are combined with supply-side evaluations to estimate market size and segment shares. Additional analysis is conducted across product formats, ingredient categories, and distribution channels.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are developed and validated through computer-assisted interviews with manufacturers, distributors, retailers, foodservice operators, and plant-based ingredient suppliers. These consultations provide operational insights regarding product innovation, production capabilities, pricing trends, and consumer preferences. The feedback obtained is used to refine market assumptions and improve analytical accuracy.

Step 4: Research Synthesis and Final Output

The final phase involves integrating primary and secondary research findings into a validated market assessment. Data triangulation techniques are applied to reconcile top-down and bottom-up calculations. The resulting output includes market sizing, segmentation analysis, competitive benchmarking, future forecasts, and strategic recommendations for stakeholders operating within the India Dairy Free Ice Cream Market.

- Executive Summary

- Research Methodology (Market Definitions and Assumptions, Abbreviations, Market Sizing Approach, Top-Down Analysis, Bottom-Up Analysis, Demand-Side Assessment, Supply-Side Assessment, Retail Audit Analysis, Consumer Purchase Tracking, Primary Industry Interviews, Data Triangulation, Forecasting Framework, Limitations and Future Conclusions)

- Definition and Scope

- Market Evolution and Industry Genesis

- Timeline of Major Industry Developments

- Dairy-Free Frozen Dessert Industry Ecosystem

- Industry Value Chain Analysis

- Growth Drivers (Increasing Lactose Intolerance Awareness, Expanding Vegan and Flexitarian Population, Growth of Plant-Based Food Consumption, Rising Disposable Income, Premium Frozen Dessert Demand, Expansion of Modern Retail Channels)

- Market Challenges (Premium Product Pricing, Limited Consumer Awareness Beyond Metro Cities, Plant-Based Ingredient Supply Constraints, Cold Chain Infrastructure Gaps, Taste and Texture Replication Challenges, Distribution Reach Limitations)

- Market Opportunities (Quick Commerce Expansion, Functional Dairy-Free Ice Cream Development, High-Protein Plant-Based Formulations, Tier II & Tier III City Penetration, Foodservice Adoption, Private Label Growth)

- Market Trends (Oat-Based Product Innovation, Coconut-Based Formulations, Clean Label Products, Low-Sugar Frozen Desserts, Traditional Indian Flavor Integration, Sustainable Packaging Adoption, Protein-Enriched Dairy-Free Products)

- Government Regulations (FSSAI Food Labeling Requirements, Vegan Food Compliance Regulations, Allergen Declaration Standards, Food Safety and Quality Standards, Packaging Waste Management Rules, Sustainability Compliance Requirements)

- Raw Material Analysis (Coconut Availability, Almond Ingredient Procurement, Oat Ingredient Adoption, Cashew Supply Dynamics, Pea Protein Utilization, Natural Sweetener Trends)

- Consumer Preference Mapping (Taste Expectations, Texture Acceptance, Ingredient Transparency, Health Benefits, Sustainability Preferences)

- Supply-Demand Gap Assessment

- SWOT Analysis

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Stakeholder Ecosystem

- Competition Ecosystem

- By Market Value (2020-2025)

- By Volume Consumption (2020-2025)

- By Average Selling Price (2020-2025)

- By Base Ingredient Type (In Value %)

Coconut Milk-Based Ice Cream

Almond Milk-Based Ice Cream

Oat Milk-Based Ice Cream

Soy Milk-Based Ice Cream

Cashew Milk-Based Ice Cream

Pea Protein-Based Ice Cream

Mixed Plant-Based Formulations

Other Alternative Bases - By Flavor Type (In Value %)

Chocolate

Vanilla

Mango

Tender Coconut

Dry Fruit and Nut-Based Flavors

Coffee Flavors

Traditional Indian Dessert Flavors

Premium Gourmet Flavors - By Distribution Channel (In Value %)

Supermarkets and Hypermarkets

General Trade and Kirana Stores

Convenience Stores

Health & Organic Stores

Online Retail and Direct-to-Consumer

Quick Commerce Platforms

Foodservice and HoReCa

Ice Cream Parlors and Dessert Chains - By Region (In Value %)

North India

South India

West India

East India

Central India - By Packaging Type (In Value %)

Tubs

Cups

Stick and Bar Packaging

Multipack Formats

Family Packs

Sustainable Packaging Formats

- Market Share of Major Players (By Value, Volume, Product Format, Distribution Channel, Plant-Based Base Type)

- Market Concentration Analysis (Top Brand Contribution, Regional Brand Presence, Private Label Penetration, Premium Brand Dominance)

- Cross Comparison Parameters (Plant-Based Base Portfolio, Dairy-Free SKU Count, Distribution Reach Across India, Production Capacity, Vegan Certification Portfolio, Premium Product Penetration, Innovation & New Product Launch Frequency, Quick Commerce Presence)

- SWOT Analysis of Major Players

- Pricing Analysis by SKU, Pack Size and Product Category

- Detailed Profiles of Major Companies

NOTO Ice Cream

Go Zero

Minus 30

White Cub

Sequel Foods (Zero Ice Cream)

Baskin Robbins Non-Dairy Range

London Dairy Dairy-Free

Oatly Frozen Desserts

Ben & Jerry’s Non-Dairy

Magnum Vegan

Häagen-Dazs Non-Dairy

Coconut Bliss

Goodmylk

Urban Platter Plant-Based Frozen Desserts

Nature’s Basket Private Label Plant-Based Desserts

- Consumption Behavior Assessment (Purchase Frequency, Consumption Occasions, Household Penetration, Repeat Purchase Rate, Seasonal Consumption Patterns)

- Demographic Consumption Trends (Age Group, Income Segment, Urban-Rural Split, Family Structure, Lifestyle Preferences)

- Purchasing Power Analysis (Disposable Income, Premium Product Affordability, Food & Beverage Spending, Frozen Dessert Expenditure)

- Premium vs Mass Market Demand Analysis (Willingness to Pay, Premium Brand Adoption, Value Perception, Trading-Up Behaviour)

- Brand Loyalty Assessment (Repeat Purchases, Brand Switching Trends, Retention Drivers, Trial Conversion Rates)

- By Market Value (2026-2035)

- By Volume Consumption (2026-2035)

- By Average Selling Price (2026-2035)

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now