Download PDF

Download PDFMarket Overview

The India Defence Maritime Market was valued at USD ~ billion in 2024 and is projected to expand at a CAGR of ~% during the 2026–2035 forecast period. According to data published by the Ministry of Defence (MoD), the Department of Defence Production (DDP), and the Stockholm International Peace Research Institute (SIPRI), India remains one of the world’s largest defence spenders and among Asia’s most active naval modernisation programmes, with the Indian Navy and Indian Coast Guard continuously expanding and upgrading their fleet capabilities in response to evolving strategic requirements across the Indian Ocean Region (IOR). The Ministry of Defence’s capital budget allocations for the Navy have grown consistently over recent years, with the Indian Navy’s Long-Term Integrated Perspective Plan (LTIPP) and the 30-year Maritime Capability Perspective Plan outlining ambitious fleet expansion targets encompassing aircraft carriers, destroyers, frigates, submarines, corvettes, and patrol vessels. Growth is supported by India’s Aatmanirbhar Bharat (Self-Reliant India) defence indigenisation policy, the Defence Acquisition Procedure (DAP) 2020, and the Defence Production and Export Promotion Policy (DPEPP) 2020, which together prioritise domestic shipbuilding and naval systems manufacturing while creating new export opportunities for Indian-origin naval platforms and systems across friendly foreign countries.

Market Segmentation

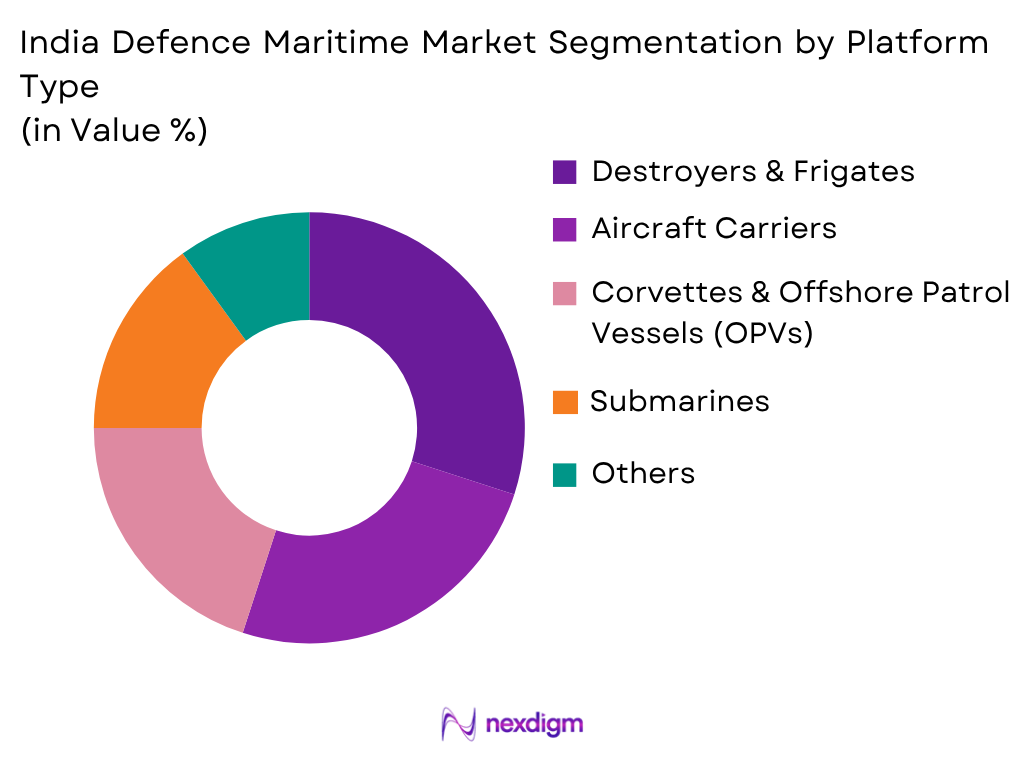

By Platform Type

Destroyers and frigates represent the highest-value platform segment within the India Defence Maritime Market, driven by the Indian Navy’s sustained investment in large multi-mission surface combatants equipped with advanced weapon systems, stealth features, and network-centric warfare capabilities. The Project 15B Visakhapatnam-class guided-missile destroyers, under construction at Mazagon Dock Shipbuilders Limited (MDL), represent the most advanced surface combatants ever built in India, incorporating BrahMos supersonic cruise missiles, Barak-8 long-range surface-to-air missiles, indigenous combat management systems, and advanced sonar and electronic warfare suites. The Indian Navy’s Project 17A stealth frigates, also under construction at MDL and Garden Reach Shipbuilders & Engineers (GRSE), represent another major high-value programme contributing significantly to market revenue. Submarines represent the second most strategically critical and capital-intensive segment, encompassing the ongoing Project 75 Scorpène-class conventional submarine programme and the planned Project 75I Advanced Submarine programme that will see six next-generation conventionally powered submarines constructed in India with Air Independent Propulsion (AIP) capability. The nuclear submarine fleet, including the Arihant-class ballistic missile submarines under the Strategic Forces Command, further contributes to the overall market value. Continuous investments in indigenous naval construction capability, technology transfer agreements, and integration of DRDO-developed systems across all major platform classes continue to strengthen India’s domestic defence maritime industrial base.

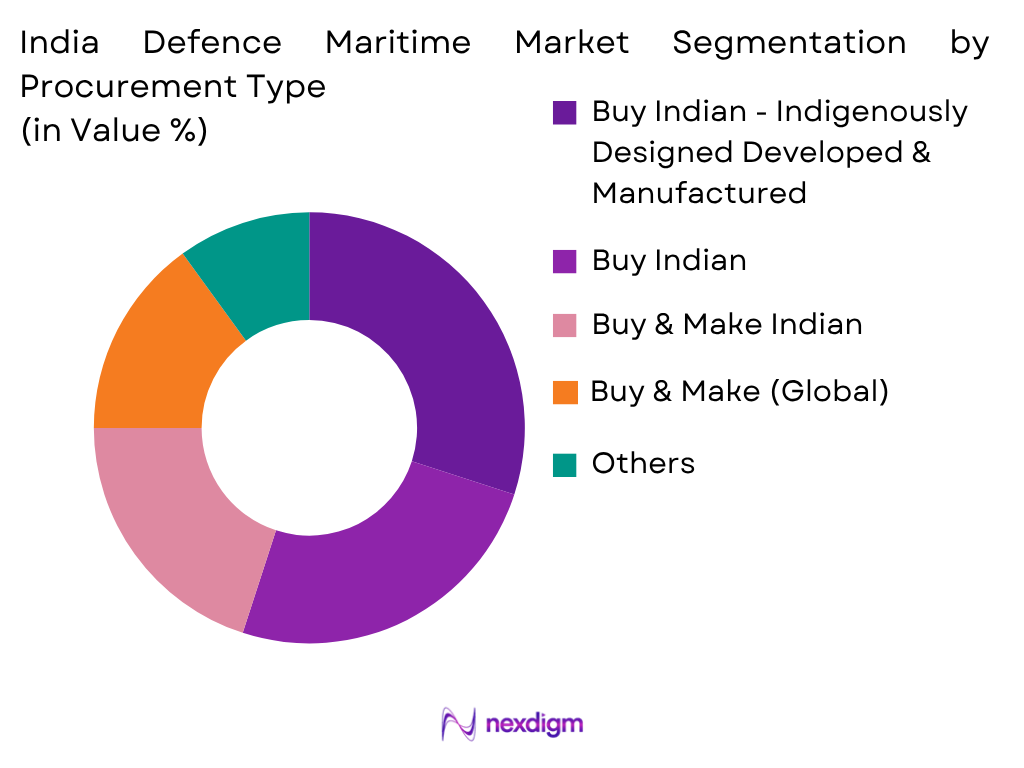

By Procurement Mode

Buy Indian – Indigenously Designed, Developed and Manufactured (IDDM) platforms have progressively emerged as the highest-priority procurement category within the India Defence Maritime Market under the Defence Acquisition Procedure (DAP) 2020, reflecting the Government of India’s strategic commitment to building a self-reliant defence industrial base. Under this category, naval platforms that are wholly designed, developed, and manufactured within India by Indian entities, incorporating a prescribed minimum indigenous content threshold, receive preferential consideration in capital acquisition planning. Major programmes falling under this category include INS Vikrant (India’s first indigenously designed and built aircraft carrier, commissioned in 2022), the Project 15B destroyer programme, and the Project 17A frigate programme. Buy & Make Indian programmes, which involve the procurement of technologies or platforms from foreign OEMs with mandatory licensed production and technology transfer to Indian partners, represent another significant procurement mode, as seen in the Project 75 Scorpène submarine programme executed through a transfer of technology arrangement between DCNS (Naval Group) of France and MDL. The Ministry of Defence’s Positive Indigenisation Lists (PIL) for defence equipment, including dedicated lists for naval systems, munitions, and shipborne equipment, have progressively restricted imports of designated items, mandating domestic procurement and stimulating investment in Indian naval supply chains. The Strategic Partnership (SP) model introduced under DPP 2016 and refined in DAP 2020 enables private Indian companies to partner with foreign OEMs in large strategic programmes such as the Project 75I submarine acquisition.

Competitive Landscape

The India Defence Maritime Market is structured around a core group of public sector shipyards with decades of naval construction experience, a growing private sector shipbuilding capability, a network of defence public sector undertakings (DPSUs) supplying naval systems and equipment, and an expanding base of private defence technology companies and foreign OEM partners. Public sector shipyards including Mazagon Dock Shipbuilders Limited (MDL), Garden Reach Shipbuilders & Engineers (GRSE), Goa Shipyard Limited (GSL), and Cochin Shipyard Limited (CSL) hold dominant positions in major naval construction programmes, supported by the Ministry of Defence’s preference for DPSU engagement in strategic platform programmes. Private sector players including Larsen & Toubro Shipbuilding, Tata Advanced Systems Limited, and Mahindra Defence Naval Systems are increasingly capturing roles in complex naval programmes through the Strategic Partnership model and Make in India initiatives. DPSUs including Bharat Electronics Limited (BEL) and Bharat Dynamics Limited (BDL) are major suppliers of naval electronic systems, weapons, and sensor packages across all major surface and subsurface platforms.

| Company | Establishment Year | Headquarters | Primary Product Focus | Manufacturing Facilities

|

Export Presence | Technology Partnerships | Certifications & Standards | Value-Added Capabilities |

| Mazagon Dock Shipbuilders Ltd (MDL) | 1774 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| Garden Reach Shipbuilders & Engineers (GRSE) | 1884 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| Larsen & Toubro (L&T) Shipbuilding | 1938 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| Goa Shipyard Limited (GSL) | 1957 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| Cochin Shipyard Limited (CSL) | 1972 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

India Defence Maritime Market Analysis

Growth Drivers

Aatmanirbhar Bharat Indigenisation Drive and Rising Defence Capital Budget

The Government of India’s Aatmanirbhar Bharat initiative and sustained increase in defence capital expenditure continue to be the most fundamental structural growth drivers for the India Defence Maritime Market. According to the Ministry of Defence’s Annual Report, India’s total defence budget exceeded INR 6.21 lakh crore (approximately USD 75 billion) in the Union Budget 2024-25, with the capital outlay allocated for new acquisitions and construction programmes continuing to grow year-on-year to support the Indian Navy’s ambitious fleet modernisation agenda. The World Bank estimated India’s GDP at approximately USD 3.7 trillion in 2024, reflecting the world’s fifth-largest economy and a growing fiscal capacity to sustain elevated defence capital investment. The Department of Defence Production’s Positive Indigenisation Lists, which have progressively restricted imports of naval equipment, weapons, and systems across multiple tranches, are compelling the Indian naval industrial base to develop domestic alternatives across a wide range of shipborne systems, from hull mounted sonars and combat management systems to marine gas turbines and torpedo tube launchers. The Stockholm International Peace Research Institute (SIPRI) consistently identifies India as one of the world’s largest arms importers, a status that the Government of India is actively working to reduce through mandatory indigenisation, technology transfer requirements, and offset obligations embedded in major defence contracts. The Defence Production and Export Promotion Policy (DPEPP) 2020 targets USD 5 billion in annual defence exports by 2025, with naval platforms and systems identified as key export product categories, further incentivising investment in domestic maritime defence manufacturing capacity and international marketing initiatives by Indian shipyards and defence companies.

Indo-Pacific Strategic Posture and Indian Ocean Region Maritime Security

Escalating strategic competition in the Indo-Pacific region and the Indian Navy’s expanding operational mandate across the Indian Ocean Region (IOR) continue to generate strong and sustained demand for advanced naval platforms, weapons, and maritime surveillance systems. According to the Ministry of External Affairs (MEA) and the Indian Navy’s Maritime Security Strategy, India’s national security environment has grown increasingly complex, with the People’s Liberation Army Navy (PLAN) of China expanding its presence across the Indian Ocean through port development in Sri Lanka, Pakistan, Myanmar, and the Maldives, commonly referred to as the String of Pearls strategy. The Indian Navy’s operational requirements now span from the Persian Gulf and the Horn of Africa in the west to the Malacca Strait and the South China Sea in the east, necessitating a larger, more capable, and technologically advanced fleet. India’s bilateral and multilateral security partnerships, including the Quad (India, USA, Australia, Japan), the India-France strategic partnership, the India-US COMCASA, LEMOA, and BECA foundational defence agreements, and growing naval cooperation with friendly IOR nations including Mauritius, Sri Lanka, Seychelles, and Maldives, are reinforcing demand for interoperable naval systems, communications equipment, and jointly deployable maritime patrol capabilities. The Indian Coast Guard’s expanding mandate for Exclusive Economic Zone (EEZ) surveillance, anti-piracy operations, humanitarian assistance, and disaster relief further adds to procurement requirements for offshore patrol vessels, fast patrol vessels, hovercraft, and coastal surveillance systems. These evolving strategic and operational requirements provide a durable long-term demand foundation for the India Defence Maritime Market through 2035.

Market Challenges

Long Gestation Periods and Technology Gaps in Critical Naval Subsystems

The India Defence Maritime Market faces significant structural challenges arising from long programme gestation periods, technology gaps in critical naval subsystems, and the complexity of executing large-scale indigenisation across strategically sensitive defence platforms. Naval construction programmes in India have historically experienced substantial schedule overruns due to supply chain delays, late delivery of government-furnished equipment (GFE), integration challenges with imported subsystems, and limited industrial capacity at public sector shipyards. The Comptroller and Auditor General of India (CAG) has periodically reported delays in major naval shipbuilding programmes, including Project 15A and 15B destroyer programmes and the Project 17A frigate programme, attributing delays to equipment procurement bottlenecks, design changes, and inadequate pre-production planning. Critical technology gaps persist across strategic naval subsystems including marine gas turbines, where India remains dependent on imported units from General Electric and Rolls-Royce; advanced sonar systems for deep-water anti-submarine warfare; air-independent propulsion (AIP) for conventional submarines; and certain categories of naval combat management system software. The Defence Research and Development Organisation (DRDO) is actively pursuing development programmes across these technology gaps, including the Kaveri Marine Gas Turbine programme and indigenously developed Shakti combat management system, but several of these programmes remain in advanced development stages with commercial qualification pending. These technology dependencies increase programme costs, extend delivery timelines, and create strategic vulnerabilities that the Ministry of Defence and DRDO are working to progressively eliminate through long-term R&D investment, international technology transfer agreements, and the Make in India framework for defence manufacturing.

Complex Procurement Frameworks and Fiscal Constraints on Capital Allocation

The complexity of India’s defence procurement regulatory framework and periodic fiscal constraints on the Ministry of Defence’s capital budget continue to create challenges for the predictable and timely execution of naval acquisition programmes. The Defence Acquisition Procedure (DAP) 2020, while introducing several progressive reforms including the Strategic Partnership model and prioritisation of IDDM procurement, remains a multi-stage approval process requiring Acceptance in Principle (AoN), Request for Proposal (RFP) issuance, technical evaluation, field trials, contract negotiation, and Cabinet Committee on Security (CCS) approval for large-value programmes, a process that can extend over multiple years for complex naval platforms. The Ministry of Defence’s annual capital budget, while growing in absolute terms, faces significant committed liability obligations from existing ongoing contracts, leaving a relatively limited pool of fresh commitment funds available each year for new programme initiations. According to Ministry of Finance data, India’s fiscal consolidation objectives place constraints on the pace of defence capital expenditure growth relative to the Indian Navy’s long-term fleet target of achieving a 175-ship force level by 2035. Delays in budget release, frequent reappropriations between revenue and capital accounts, and compressed procurement timelines during fiscal year-end create additional execution challenges for both naval headquarters and industry partners. Strengthening programme management capabilities at naval headquarters, improving pre-contract planning processes, and providing multi-year budgetary commitments for long-duration shipbuilding programmes remain critical reforms needed to improve acquisition efficiency and industrial capacity utilisation across India’s naval defence manufacturing base.

Market Opportunities

Project 75I Submarine Programme and Next Generation Destroyer Development

India’s Project 75I Advanced Submarine Programme represents one of the largest and most strategically significant procurement opportunities in the India Defence Maritime Market over the 2026-2035 forecast period. The Ministry of Defence has issued a Request for Proposal (RFP) for six advanced conventional submarines under the Strategic Partnership model, requiring a foreign OEM to partner with a designated Indian private sector strategic partner to deliver submarines incorporating air-independent propulsion (AIP), advanced stealth features, land-attack cruise missile capability, and an elevated level of indigenous content. Global submarine OEMs competing for this programme include Naval Group (France), ThyssenKrupp Marine Systems (Germany), Saab Kockums (Sweden), Navantia (Spain), and Daewoo Shipbuilding (South Korea), all of whom would be required to transfer substantial technology to their Indian strategic partner. The total programme value is estimated by defence analysts at USD 5 to 6 billion, making it among India’s largest single defence acquisition programmes, generating extensive industrial activity across shipbuilding, systems integration, weapons, sonar, and support infrastructure segments. Concurrently, the Indian Navy’s development of Next Generation Destroyers (NGD) under Project 18 is expected to define the high-end surface combatant capability of the fleet beyond 2030, creating new opportunities for advanced stealth design, integrated electric propulsion, directed energy weapons, and hypersonic missile integration. Companies investing in submarine technology transfer, AIP system development, advanced combat management systems, and hypersonic naval weapons will be best positioned to capture the high-value opportunities these programmes represent.

Unmanned Maritime Systems, Naval Drones and Coastal Domain Awareness

The rapid global development of unmanned maritime systems, including unmanned surface vessels (USVs), autonomous underwater vehicles (AUVs), and naval drone systems, combined with India’s accelerating investment in coastal surveillance and maritime domain awareness infrastructure, presents a significant emerging growth opportunity for the India Defence Maritime Market. The Indian Navy has identified unmanned and autonomous maritime systems as a strategic priority capability in its technology roadmap, with DRDO’s Naval Science and Technological Laboratory (NSTL) and National Aerospace Laboratories (NAL) actively developing prototype AUVs, mine countermeasure drones, and underwater surveillance systems. The Ministry of Defence’s Defence Innovation Organisation (DIO) and the iDEX (Innovations for Defence Excellence) programme have funded multiple startups and emerging technology companies working on naval unmanned systems, marine robotics, and AI-driven maritime surveillance technologies. India’s National Maritime Domain Awareness (NMDA) initiative, overseen by the National Security Council Secretariat (NSCS), encompasses the integration of coastal radar chains, Automatic Identification System (AIS) networks, satellite-based maritime surveillance, and over-the-horizon radar systems into a unified picture for maritime security authorities, creating procurement opportunities across sensors, communication systems, command infrastructure, and data analytics platforms. The QUAD’s Indo-Pacific Maritime Domain Awareness (IPMDA) initiative, in which India participates alongside the United States, Australia, and Japan, further reinforces investment in interoperable maritime surveillance systems. Defence startups and private technology companies, alongside established DPSUs, are well positioned to develop and supply innovative unmanned maritime systems, AI-enabled surveillance platforms, and counter-drone technologies that address India’s growing maritime security requirements across the IOR.

Future Outlook

The India Defence Maritime Market is expected to witness strong and sustained growth throughout the forecast period, supported by the Indian Navy’s ambitious fleet expansion and modernisation plans, rising defence capital budgets, progressive indigenisation under Aatmanirbhar Bharat, and escalating strategic imperatives in the Indo-Pacific. Major programmes including Project 75I submarines, Next Generation Destroyers, Project 17B frigates, new-generation OPVs for the Coast Guard, and expanding naval drone and unmanned systems capabilities are expected to generate significant market activity. Domestic shipyards and defence technology companies are expected to capture a progressively larger share of programme value as indigenisation mandates strengthen and technology transfer programmes mature. Growing defence exports, expanding DRDO-to-industry technology transitions, and India’s deepening strategic partnerships with Quad and Indo-Pacific allies will further strengthen the long-term growth trajectory of the India Defence Maritime Market through 2035.

Major Players

- Mazagon Dock Shipbuilders Ltd (MDL)

- Garden Reach Shipbuilders & Engineers (GRSE)

- Goa Shipyard Limited (GSL)

- Larsen & Toubro (L&T) Shipbuilding

- Cochin Shipyard Limited (CSL)

- Hindustan Shipyard Limited (HSL)

- Bharat Electronics Limited (BEL) – Naval Systems

- Bharat Dynamics Limited (BDL)

- DRDO – Naval Physical & Oceanographic Laboratory (NPOL)

- Tata Advanced Systems Limited (TASL)

- Mahindra Defence Naval Systems

- Alpha Design Technologies

- Elbit Systems India (Naval Division)

- Rolls-Royce India (Naval Propulsion)

- Thales India (Naval Electronics)

Key Target Audience

- Naval Shipbuilders and Shipyard Operators

- Naval Systems and Weapons Manufacturers

- Defence Electronics and Sensor System Integrators

- Naval Platform MRO and Refit Service Providers

- Investments and Venture Capitalist Firms

- Government and Regulatory Bodies (Ministry of Defence (MoD), Department of Defence Production (DDP), Indian Navy Headquarters, Indian Coast Guard Headquarters, Defence Research and Development Organisation (DRDO), Defence Acquisition Council (DAC), Hindustan Aeronautics Limited (HAL) – Naval Aviation)

- Foreign OEMs and Technology Transfer Partners

- Defence Startups and iDEX Innovators

Research Methodology

Step 1: Identification of Key Variables

The research begins by identifying the major stakeholders across the India Defence Maritime value chain, including shipyards, naval systems manufacturers, DRDO laboratories, DPSUs, private defence companies, foreign OEM partners, procurement agencies, and end-user commands. Extensive secondary research is conducted using Ministry of Defence publications, parliamentary standing committee reports, SIPRI databases, defence trade publications, company annual reports, and proprietary defence acquisition databases to establish the key variables influencing market performance.

Step 2: Market Analysis and Construction

Historical market information is compiled and evaluated to estimate overall market size, programme values, construction volumes, system supply revenues, and MRO expenditure across major naval platform and system categories. Both demand-side (fleet composition targets, operational requirements, budget allocations) and supply-side (shipyard capacity, DPSU production output, import values) indicators are analysed using bottom-up and top-down approaches to construct a comprehensive market model.

Step 3: Hypothesis Validation and Expert Consultation

Preliminary market estimates and assumptions are validated through structured discussions with naval procurement specialists, shipyard executives, defence systems engineers, programme managers, industry association representatives, and retired naval officers with procurement expertise. These consultations provide critical insights into programme timelines, technology readiness levels, indigenisation progress, budget realities, and strategic priorities that strengthen the reliability and accuracy of market estimates.

Step 4: Research Synthesis and Final Output

The final stage integrates primary research findings with secondary data to develop a comprehensive market assessment covering platform segments, system categories, procurement modes, competitive positioning, and future programme opportunities. Multiple validation techniques including cross-verification with defence budget documents, parliamentary committee reports, and contract announcement data are employed to ensure the consistency and credibility of the final market report.

- Executive Summary

- Research Methodology (Market Definitions and Assumptions, Abbreviations, Market Taxonomy, Market Sizing Approach, Top-Down Analysis, Bottom-Up Analysis, Demand-Side Assessment, Supply-Side Assessment, Primary Industry Interviews, Secondary Research Validation, Data Triangulation, Forecasting Framework, Limitations and Future Conclusions)

- Definition and Scope

- Market Evolution and Industry Genesis

- Timeline of Major Industry Developments

- Industry Value Chain Analysis

- Supply Chain Analysis

- Growth Drivers (Aatmanirbhar Bharat Defence Indigenisation, Rising Geopolitical Tensions in the Indo-Pacific, Maritime Security Investment, Navy Expansion and Fleet Modernisation Plan, Technology Transfer Agreements and Joint Ventures, Indian Ocean Region Strategic Posture, Government Defence Capital Budget Growth, Export Push under Defence Export Policy)

- Market Challenges (Long Gestation Periods for Naval Construction, Technology Gaps in Critical Subsystems, Dependence on Foreign OEMs for Key Components, Complex DPP/DAP Procurement Frameworks, Skilled Workforce Shortages in Advanced Shipbuilding, Integration and Testing Delays, Fiscal Constraints and Budget Prioritisation, Export Control Compliance)

- Market Opportunities (P75I Submarine Programme, Next Generation Destroyers (NGD), Frigate and OPV Export Opportunities, Unmanned Maritime Systems, Autonomous Underwater Vehicles (AUVs), Naval Drone and Counter-Drone Systems, Indigenous Aircraft Carrier Development, Coastal Surveillance and Domain Awareness Systems)

- Market Trends (Indigenisation of Naval Combat Systems, Adoption of Artificial Intelligence in Naval Platforms, Unmanned and Autonomous Surface and Underwater Vessels, Network-Centric Warfare Capabilities, Directed Energy Weapons Development, Advanced Sonar and Anti-Submarine Warfare (ASW) Systems, Digital Shipyard Technologies, Modular Open Systems Architecture (MOSA))

- Government Regulations and Policies (Defence Acquisition Procedure (DAP) 2020, Defence Production and Export Promotion Policy (DPEPP) 2020, Defence Industrial Licensing, Strategic Partnership Model, FDI in Defence (74% under Automatic Route), Positive Indigenisation List for Naval Systems, DRDO Technology Development Framework, AIF (Acceptance in Principle) and RFP Processes)

- Indigenisation and DRDO Programme Analysis (Indigenously Designed Developed & Manufactured (IDDM) Naval Systems, DRDO-Developed Naval Weapons, BrahMos Integration, Kaveri Marine Engine, NMRL Material Technology, NPOL Sonar Systems)

- Budget and Capital Expenditure Analysis (Ministry of Defence Capital Budget, Navy Share of Capital Outlay, Revenue vs Capital Split, Committed Liabilities vs Fresh Commitments)

- Technology Import Analysis (Critical Foreign Imports, Technology Transfer Agreements, Licensed Production, Offset Obligations)

- Geopolitical and Strategic Threat Assessment (China Naval Expansion, Pakistan Maritime Threat, Indian Ocean Region Contestation, Indo-Pacific Alliance Frameworks)

- SWOT Analysis

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Stakeholder Ecosystem

- Competition Ecosystem

- By Market Value (2020-2025)

- By Programme and Platform Volume (2020-2025)

- By Average Programme Value (2020-2025)

- By Platform Type (In Value %)

Aircraft Carriers

Destroyers & Frigates

Corvettes & Offshore Patrol Vessels (OPVs)

Submarines (Conventional & Nuclear)

Mine Countermeasure Vessels (MCMVs)

Landing Platform Docks & Amphibious Vessels

Fast Attack Craft & Patrol Boats

Survey Ships & Research Vessels - By System / Technology Type (In Value %)

Combat Management Systems (CMS)

Naval Weapons & Missile Systems

Underwater Warfare Systems (Torpedoes & Sonar)

Naval Radar & Electronic Warfare Systems

Naval Propulsion Systems

Communication & Navigation Systems

Integrated Platform Management Systems (IPMS)

Ship Self-Defence Systems - By Procurement Mode (In Value %)

Buy Indian – Indigenously Designed Developed & Manufactured (IDDM)

Buy Indian

Buy & Make Indian

Buy & Make (Global)

Buy Global - By End User (In Value %)

Indian Navy

Indian Coast Guard

Ministry of Ports, Shipping and Waterways

Border Security Force (Marine Wing)

Export Customers (Friendly Foreign Countries)

- By Region / Naval Command (In Value %)

Western Naval Command (Mumbai)

Eastern Naval Command (Visakhapatnam)

Southern Naval Command (Kochi)

Andaman & Nicobar Command

Strategic Forces Command (Nuclear Submarine Fleet)

- Market Share Analysis (By Value, Platform Type, Programme Category, Procurement Mode)

- Cross Comparison Parameters (Shipbuilding Capacity in Displacement Tonnage, Number of Active Naval Construction Programmes, Submarine Construction Capability, Technology Transfer Agreements, Export Track Record, DRDO Collaboration Depth, MRO and Refit Capacity, Workforce Strength and Skill Level)

- SWOT Analysis of Major Players

- Pricing Analysis (By Platform Class, Construction Timeline, Technology Content, Indigenisation Level)

- Detailed Profiles of Major Companies

Mazagon Dock Shipbuilders Ltd (MDL)

Garden Reach Shipbuilders & Engineers (GRSE)

Goa Shipyard Limited (GSL)

Larsen & Toubro (L&T) Shipbuilding

Cochin Shipyard Limited (CSL)

Hindustan Shipyard Limited (HSL)

Bharat Electronics Limited (BEL) – Naval Systems

Bharat Dynamics Limited (BDL)

DRDO – Naval Physical & Oceanographic Laboratory (NPOL)

Tata Advanced Systems Limited (TASL)

Mahindra Defence Naval Systems

Alpha Design Technologies

Elbit Systems India (Naval Division)

Rolls-Royce India (Naval Propulsion)

Thales India (Naval Electronics)

- Procurement Pattern Analysis (Capital vs Revenue Procurement, Long-Term Fleet Perspective Plan, Annual Acquisition Plan, RFP and Contract Timelines)

- End-User Demand Analysis (Indian Navy Fleet Composition, Coast Guard Expansion, Export Customer Requirements)

- Budget Allocation and Expenditure Analysis

- Indigenisation Preference and Compliance Analysis

- Technology Priority Analysis (ASW, Air Defence, Surface Warfare, Electronic Warfare)

- MRO and Lifecycle Support Demand

- Platform Attribute Preference Analysis (Stealth, Range, Speed, Weapons Load, Crew Complement, Endurance, Interoperability)

- Joint Venture and Technology Transfer Preference

- Export Customer Procurement Behaviour

- Procurement Pain Point Analysis

- Decision-Making and Approval Process (CCS, DAC, DPB, SCAPCHC)

- By Market Value (2026-2035)

- By Programme and Platform Volume (2026-2035)

- By Average Programme Value (2026-2035)

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now