Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the India diagnostic labs market generated approximately USD ~ billion according to healthcare industry assessments referenced by the Federation of Indian Chambers of Commerce and Industry and healthcare analytics reports aligned with National Health Authority datasets. The market is driven by increasing demand for preventive healthcare, rising chronic disease prevalence, expansion of private pathology networks, and technological advancements in diagnostic imaging, molecular testing, and laboratory automation systems deployed across hospitals and independent diagnostic laboratories nationwide.

Major metropolitan regions including Mumbai, Delhi NCR, Bengaluru, Hyderabad, and Chennai dominate the India diagnostic labs market due to the presence of advanced healthcare infrastructure, large hospital networks, and established pathology laboratory chains. These cities host major diagnostic service providers supported by strong medical talent pools, research institutions, and high healthcare spending populations. Urban centers also benefit from advanced laboratory automation technologies, integrated diagnostic platforms, and extensive sample collection networks that support large scale clinical testing services.

Market Segmentation

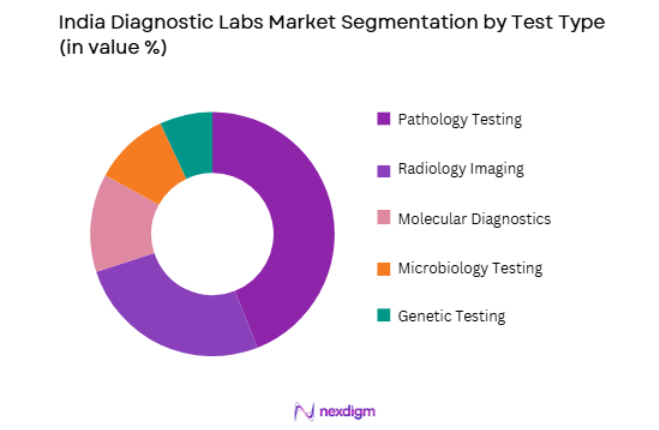

By Test Type

India Diagnostic Labs market is segmented by test type into pathology testing, radiology imaging, molecular diagnostics, genetic testing, and microbiology testing. Recently, pathology testing has a dominant market share due to factors such as widespread demand for routine blood testing, clinical chemistry analysis, and diagnostic screening across hospitals and independent laboratories. Pathology tests are essential for diagnosing chronic diseases including diabetes, cardiovascular disorders, and infectious conditions, which significantly increases test volumes across healthcare providers. Hospitals rely heavily on pathology laboratories for routine clinical decision making and patient monitoring. Diagnostic chains operate centralized pathology laboratories that process thousands of samples daily through automated testing equipment and standardized laboratory workflows. Preventive healthcare programs and corporate health checkups further increase demand for pathology testing services.

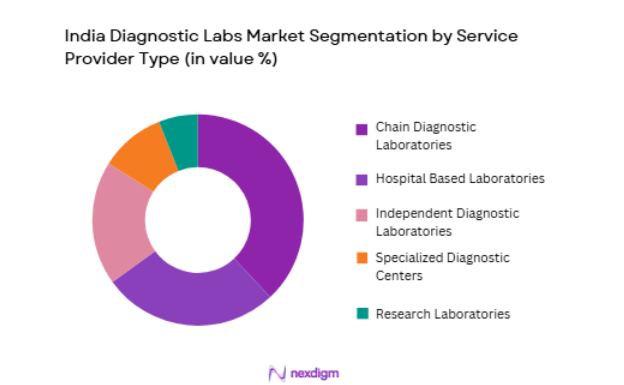

By Service Provider

India Diagnostic Labs market is segmented by service provider into hospital based laboratories, independent diagnostic laboratories, chain diagnostic laboratories, research laboratories, and specialized diagnostic centers. Recently, chain diagnostic laboratories have a dominant market share due to factors such as strong brand presence, nationwide sample collection networks, and advanced centralized laboratory infrastructure. Large diagnostic chains operate automated processing laboratories capable of handling high testing volumes while maintaining standardized quality control protocols. These networks provide patients with convenient sample collection services including home sample pickup and digital test reporting platforms. Chain laboratories also collaborate with hospitals, clinics, and physicians to deliver diagnostic testing services across multiple medical specialties. The expansion of franchise based collection centers enables diagnostic chains to reach smaller cities and regional healthcare markets. Investment in laboratory automation, high throughput analyzers, and integrated diagnostic information systems further strengthens operational efficiency for these diagnostic networks.

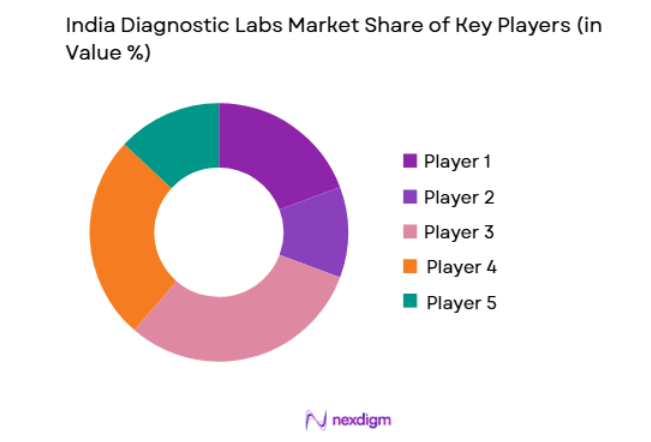

Competitive Landscape

The India diagnostic labs market is moderately consolidated with several large pathology chains and hospital laboratory networks dominating testing volumes through extensive sample collection infrastructure and advanced laboratory technologies. Major diagnostic service providers operate nationwide laboratory networks supported by centralized processing laboratories and digital diagnostic platforms. Consolidation continues as large laboratory chains expand through acquisitions, franchise partnerships, and regional laboratory integration to strengthen nationwide diagnostic service coverage.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Diagnostic Network Size |

| Dr. Lal PathLabs | 1949 | New Delhi, India | ~ | ~ | ~ | ~ | ~ |

| Metropolis Healthcare | 1980 | Mumbai, India | ~ | ~ | ~ | ~ | ~ |

| Thyrocare Technologies | 1996 | Mumbai, India | ~ | ~ | ~ | ~ | ~ |

| SRL Diagnostics | 1995 | Gurugram, India | ~ | ~ | ~ | ~ | ~ |

| Redcliffe Labs | 2017 | Noida, India | ~ | ~ | ~ | ~ | ~ |

India Diagnostic Labs Market Analysis

Growth Drivers

Rising Prevalence of Chronic Diseases and Increasing Demand for Preventive Diagnostic Testing

The India diagnostic labs market is expanding significantly due to the rising prevalence of chronic diseases including diabetes, cardiovascular disorders, cancer, and respiratory illnesses that require continuous diagnostic monitoring and early detection through laboratory testing services. Chronic diseases have become a major healthcare challenge across India due to lifestyle changes, urbanization, dietary patterns, and aging populations which collectively increase the demand for regular health screening programs and diagnostic evaluations. Diagnostic laboratories play a critical role in detecting early disease symptoms through blood tests, biomarker analysis, imaging diagnostics, and molecular testing technologies that assist physicians in accurate medical diagnosis and treatment planning. Preventive healthcare awareness is increasing among urban populations as individuals recognize the importance of routine medical checkups and health monitoring programs to identify potential health risks before severe disease progression occurs. Corporate wellness programs organized by employers further increase demand for diagnostic services because organizations offer preventive health screening packages to employees as part of workplace healthcare initiatives. Hospitals and clinics also rely heavily on diagnostic laboratories for clinical testing that supports patient diagnosis, disease monitoring, and treatment evaluation. Technological advancements in laboratory automation and high throughput diagnostic analyzers enable laboratories to process large volumes of samples efficiently while maintaining high levels of diagnostic accuracy and reliability. Increasing healthcare spending across India also supports diagnostic testing adoption as patients seek advanced medical services including specialized diagnostic procedures and genetic testing programs.

Expansion of Organized Diagnostic Laboratory Chains and Digital Diagnostic Service Platforms

The expansion of organized diagnostic laboratory chains across India represents a major growth driver for the diagnostic labs market as large laboratory networks invest heavily in advanced diagnostic infrastructure, digital platforms, and nationwide sample collection systems. Organized diagnostic chains operate centralized laboratory facilities equipped with automated testing equipment capable of processing thousands of diagnostic samples daily with standardized quality control procedures. These networks offer comprehensive diagnostic testing services including pathology, radiology, molecular diagnostics, and preventive health screening packages designed for hospitals, physicians, and individual patients. Large laboratory chains also deploy digital healthcare platforms that allow patients to schedule diagnostic tests online, access digital reports through mobile applications, and arrange home sample collection services without visiting laboratory centers physically. These digital services significantly enhance patient convenience and improve accessibility to diagnostic testing services across urban and semi urban regions. Diagnostic chains also collaborate with hospitals, clinics, and physician networks to provide integrated diagnostic services that support clinical decision making across multiple medical specialties. Franchise based sample collection centers operated by diagnostic chains enable expansion into smaller cities and regional healthcare markets where access to advanced diagnostic services was previously limited. Investments in laboratory automation technologies and high throughput analyzers also improve operational efficiency while reducing diagnostic processing time. Digital healthcare ecosystems further integrate diagnostic laboratories with telemedicine platforms and electronic health record systems that allow physicians to access diagnostic results instantly for patient consultations.

Market Challenges

Fragmented Diagnostic Service Landscape and Quality Standardization Issues

The India diagnostic labs market faces significant challenges due to the fragmented nature of diagnostic service providers and inconsistent quality standards across thousands of independent laboratories operating throughout the country. A large number of small pathology laboratories operate without advanced automation technologies or standardized diagnostic protocols which can lead to variations in testing accuracy and result reliability. Quality control remains a critical issue because smaller laboratories may lack access to certified diagnostic equipment, trained laboratory professionals, and internationally recognized accreditation standards required for high quality diagnostic testing. Regulatory oversight across the diagnostic laboratory sector is evolving but enforcement of standardized testing protocols remains inconsistent across different regions. Patients may experience varying levels of diagnostic reliability depending on the laboratory provider selected for medical testing services. Independent laboratories may also face financial limitations that restrict investment in advanced laboratory technologies such as molecular diagnostic analyzers, automated sample processing systems, and digital laboratory information management systems. These technological limitations can reduce the ability of smaller laboratories to compete with large organized diagnostic chains that operate sophisticated centralized laboratory facilities. Fragmentation within the diagnostic laboratory sector also complicates data integration across healthcare providers because patient diagnostic records may not be easily shared between laboratories, hospitals, and physicians. Healthcare providers therefore face challenges when attempting to consolidate patient diagnostic data for comprehensive clinical evaluation.

High Capital Investment Requirements for Advanced Diagnostic Technologies

Another major challenge affecting the India diagnostic labs market involves the substantial capital investment required for implementing advanced diagnostic technologies and modern laboratory automation systems. Diagnostic laboratories increasingly rely on sophisticated equipment such as molecular diagnostic analyzers, genetic sequencing platforms, digital pathology systems, and automated sample processing machines capable of delivering high precision test results within shorter processing times. These advanced diagnostic technologies require substantial financial investment in equipment procurement, laboratory infrastructure, maintenance systems, and specialized technical personnel training. Smaller diagnostic laboratories often struggle to finance these capital intensive technology upgrades which limits their ability to offer advanced diagnostic testing services compared with large laboratory chains operating centralized facilities. Continuous technological innovation within diagnostic medicine also requires laboratories to regularly upgrade their equipment and software systems to remain competitive and maintain testing accuracy. Equipment depreciation, maintenance expenses, and reagent supply costs further increase operational expenditures for diagnostic laboratories. Laboratories must also invest in secure digital infrastructure capable of managing patient data, laboratory information systems, and digital test reporting platforms required for modern healthcare service delivery. Compliance with regulatory standards and accreditation requirements also requires financial investment in quality assurance programs and laboratory management systems.

Opportunities

Integration of Artificial Intelligence and Automation Technologies within Diagnostic Laboratories

The integration of artificial intelligence technologies and laboratory automation systems presents a major opportunity for the India diagnostic labs market by improving diagnostic accuracy, operational efficiency, and large scale data analysis capabilities within laboratory workflows. AI powered diagnostic algorithms can analyze complex medical data including imaging results, pathology slides, and genomic datasets to assist laboratory specialists in identifying disease patterns and abnormalities with high precision. Digital pathology platforms equipped with AI image analysis software allow pathologists to examine microscopic tissue samples more efficiently while reducing the risk of human interpretation errors. Automation technologies also enable laboratories to process large volumes of diagnostic samples with minimal manual intervention which significantly increases operational efficiency and reduces turnaround time for diagnostic reports. Robotic sample processing systems and automated biochemical analyzers allow diagnostic laboratories to maintain consistent testing quality while handling high testing volumes across centralized laboratory facilities. AI analytics platforms can also support predictive healthcare insights by analyzing large datasets generated through diagnostic testing programs which may help identify population level disease trends and emerging health risks. Integration of AI technologies within laboratory information systems allows physicians to access detailed diagnostic insights during clinical decision making processes. Healthcare providers also benefit from AI assisted diagnostic systems because these technologies can highlight abnormal test results that require immediate clinical attention.

Expansion of Preventive Healthcare and Personalized Medicine Diagnostic Services

The expansion of preventive healthcare programs and personalized medicine represents another significant opportunity for the India diagnostic labs market as healthcare providers increasingly focus on early disease detection and individualized treatment strategies. Preventive diagnostic services including health screening packages, genetic testing, and biomarker analysis allow patients to monitor health risks before the onset of serious medical conditions. Diagnostic laboratories are developing specialized testing services that analyze genetic predispositions, metabolic health indicators, and lifestyle related disease risks through advanced molecular diagnostic technologies. Personalized medicine approaches use diagnostic data to guide physicians in designing targeted treatment plans tailored to individual patient characteristics including genetic profiles and disease biomarkers. Pharmaceutical companies also rely on diagnostic laboratories for companion diagnostics that support targeted drug therapies and clinical trial research programs. The growing adoption of wellness programs by employers and healthcare insurers further increases demand for preventive diagnostic testing services delivered through corporate health screening initiatives. Digital healthcare platforms also integrate preventive diagnostic services with telemedicine consultations and health monitoring applications that provide patients with comprehensive healthcare management solutions. As healthcare awareness continues increasing among consumers and medical technology advances improve diagnostic capabilities, preventive healthcare and personalized medicine will become major growth areas within the India diagnostic labs market.

Future Outlook

The India diagnostic labs market is expected to experience strong growth over the next five years as healthcare providers expand diagnostic infrastructure and adopt advanced laboratory technologies. Automation systems, molecular diagnostics, and AI powered diagnostic tools will improve testing accuracy and operational efficiency. Government healthcare initiatives supporting preventive healthcare programs will further increase diagnostic testing demand. Rising healthcare awareness and expansion of organized diagnostic laboratory chains will continue strengthening the market outlook.

Major Players

- Dr. Lal PathLabs

- Metropolis Healthcare

- Thyrocare Technologies

- SRL Diagnostics

- Redcliffe Labs

- Apollo Diagnostics

- Vijaya Diagnostic Centre

- Suburban Diagnostics

- Neuberg Diagnostics

- Agilus Diagnostics

- Medall Healthcare

- Aarthi Scans and Labs

- Anderson Diagnostics

- Core Diagnostics

- Oncquest Laboratories

Key Target Audience

- Hospitals and healthcare providers

- Pharmaceutical companies

- Diagnostic laboratory chains

- Medical device manufacturers

- Healthcare technology providers

- Investments and venture capitalist firms

- Government and regulatory bodies

- Health insurance companies

Research Methodology

Step 1: Identification of Key Variables

Key market variables including diagnostic testing demand, chronic disease prevalence, laboratory infrastructure expansion, healthcare spending patterns, and technological adoption in diagnostic equipment were identified through analysis of healthcare policy reports and industry datasets.

Step 2: Market Analysis and Construction

The diagnostic laboratory market structure was constructed by evaluating service categories such as pathology testing, radiology imaging, molecular diagnostics, and preventive health screening services across hospital laboratories and independent diagnostic chains.

Step 3: Hypothesis Validation and Expert Consultation

Market assumptions were validated through consultations with diagnostic laboratory specialists, healthcare administrators, pathology professionals, and medical technology experts to ensure accuracy regarding industry trends and technological developments.

Step 4: Research Synthesis and Final Output

Research findings were synthesized through triangulation of multiple healthcare datasets, comparative analysis of diagnostic service providers, and evaluation of healthcare technology adoption trends to generate a comprehensive diagnostic laboratory market assessment.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Increasing demand for preventive healthcare and routine health screening services

Rising prevalence of chronic diseases requiring regular diagnostic testing

Expansion of organized diagnostic laboratory chains across metropolitan and tier two cities - Market Challenges

High capital investment required for advanced diagnostic equipment and laboratory infrastructure

Shortage of skilled laboratory technicians and diagnostic specialists

Regulatory compliance requirements for laboratory accreditation and quality standards - Market Opportunities

Expansion of diagnostic laboratory networks in tier two and tier three cities

Growth of home sample collection and digital diagnostic reporting services

Adoption of AI powered diagnostic analysis and automated laboratory technologies - Trends

Integration of digital laboratory information management systems

Growing demand for genomic and precision diagnostic testing - Government Regulations

National Accreditation Board for Testing and Calibration Laboratories standards

Clinical Establishments Act governing healthcare facility registration

Quality standards and certification frameworks for diagnostic laboratories - SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Pathology Testing Services

Radiology and Imaging Diagnostics

Genomic and Molecular Diagnostics

Point of Care Diagnostic Testing

Preventive Health Screening Services - By Platform Type (In Value%)

Standalone Diagnostic Laboratories

Hospital Based Diagnostic Laboratories

Chain Diagnostic Laboratory Networks

Home Collection Diagnostic Platforms

Digital Diagnostic Reporting Platforms - By Fitment Type (In Value%)

Central Reference Laboratories

Regional Processing Laboratories

Collection and Sample Processing Centers

Mobile Diagnostic Testing Units - By End User Segment (In Value%)

Hospitals and Healthcare Providers

Individual Patients and Preventive Health Users

Corporate Health Screening Programs

- Market Share Analysis

- Cross Comparison Parameters (Testing Portfolio Range, Diagnostic Technology Integration, Turnaround Time for Test Results, Laboratory Network Coverage, Digital Reporting Capability)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Dr Lal PathLabs

Metropolis Healthcare

Thyrocare Technologies

SRL Diagnostics

Suburban Diagnostics

Aarthi Scans and Labs

Neuberg Diagnostics

Vijaya Diagnostic Centre

Agilus Diagnostics

Redcliffe Labs

Healthians

Oncquest Laboratories

Core Diagnostics

Lucid Medical Diagnostics

Medall Healthcare

- Hospitals relying on advanced diagnostic laboratories for clinical decision support

- Patients increasingly adopting preventive diagnostic testing for early disease detection

- Corporate organizations implementing employee health screening programs

- Insurance providers integrating diagnostic testing within preventive healthcare packages

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now