Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The India Electric Tractor & Autonomous Farm Equipment market reached approximately USD ~ billion based on a recent historical assessment, supported by electrification initiatives and precision agriculture adoption documented by the Ministry of Agriculture and Farmers Welfare and NITI Aayog mobility transition reports. Demand is driven by rising fuel costs, decarbonization targets in farm mechanization, and pilot deployments of autonomous equipment by domestic manufacturers. Subsidy-linked electric farm machinery programs and startup innovation clusters further stimulated commercialization and early-stage fleet procurement.

Major activity clusters are concentrated in Punjab, Haryana, Maharashtra, and Tamil Nadu due to mechanization intensity, agri-equipment manufacturing ecosystems, and state-level electric mobility incentives. Cities such as Pune, Chennai, and Ludhiana host core tractor OEM production and engineering facilities, enabling localized electrified and autonomous platform development. Agricultural universities and smart-farming pilot zones in these regions provide testing environments, while strong dealership networks and progressive farming cooperatives accelerate technology uptake across commercial cultivation belts.

Market Segmentation

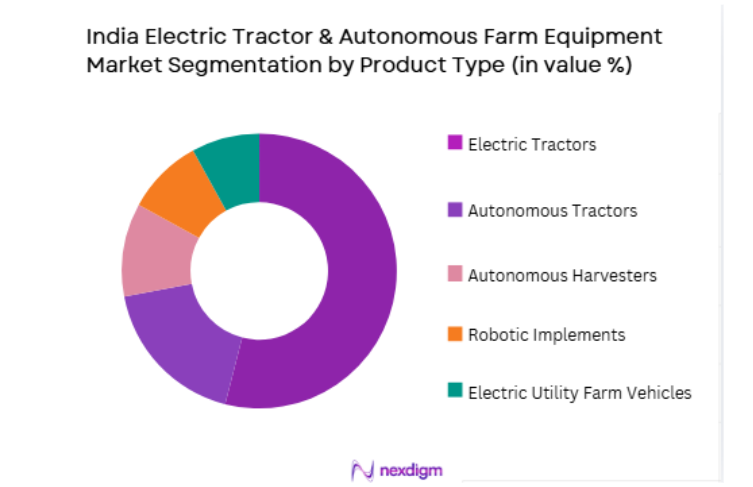

By Product Type

India Electric Tractor & Autonomous Farm Equipment market is segmented by product type into electric tractors, autonomous tractors, autonomous harvesters, robotic implements, and electric utility farm vehicles. Recently, electric tractors has a dominant market share due to factors such as compatibility with existing farming practices, government subsidy eligibility under electric mobility schemes, and strong domestic OEM manufacturing capacity. Electric tractors align with small and medium farm power requirements and benefit from battery localization initiatives, while autonomous platforms remain in pilot phases with limited commercial scale and higher acquisition complexity for average farm operators.

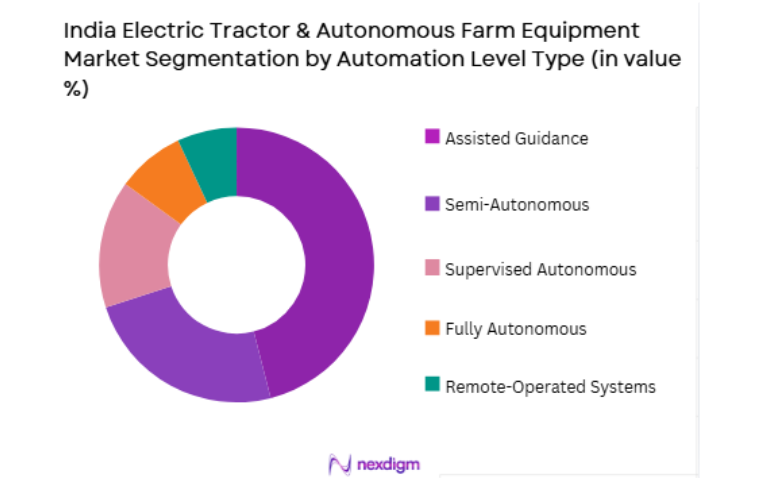

By Automation Level

India Electric Tractor & Autonomous Farm Equipment market is segmented by automation level into assisted guidance, semi-autonomous, supervised autonomous, fully autonomous, and remote-operated systems. Recently, assisted guidance has a dominant market share due to factors such as lower cost integration with conventional tractors, immediate productivity gains in row-crop operations, and compatibility with precision agriculture retrofitting kits. Farmers adopt guidance and auto-steering systems earlier than full autonomy because they reduce operator fatigue and improve field efficiency without requiring regulatory approvals or major workflow transformation.

Competitive Landscape

The India Electric Tractor & Autonomous Farm Equipment market remains moderately consolidated with strong influence from established tractor manufacturers integrating electrification and automation capabilities, alongside emerging agri-robotics startups. Domestic OEMs leverage extensive dealer networks and manufacturing scale, while technology firms contribute autonomy software and battery systems. Strategic collaborations between tractor companies, EV startups, and precision agriculture providers shape competitive positioning, with pilot deployments and state partnerships determining early leadership across electric and autonomous farm equipment segments.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Autonomy Capability Level |

| Mahindra & Mahindra Farm Equipment | 1945 | India | ~ | ~ | ~ | ~ | ~ |

| TAFE | 1960 | India | ~ | ~ | ~ | ~ | ~ |

| Escorts Kubota | 1944 | India | ~ | ~ | ~ | ~ | ~ |

| AutoNxt Automation | 2016 | India | ~ | ~ | ~ | ~ | ~ |

| Monarch Tractor | 2018 | USA | ~ | ~ | ~ | ~ | ~ |

India Electric Tractor & Autonomous Farm Equipment Market Analysis

Growth Drivers

Government-Backed Electrification and Farm Mechanization Incentives

The expansion of electric tractor and autonomous farm equipment adoption in India is strongly supported by targeted policy frameworks that integrate agricultural mechanization and clean mobility objectives into unified subsidy structures. National and state-level programs encourage farmers to replace diesel tractors with electric alternatives through capital subsidies, concessional financing, and pilot procurement initiatives linked to rural sustainability missions. These policies reduce total ownership cost barriers while accelerating domestic manufacturing of electric drivetrains, battery systems, and power electronics tailored to farm duty cycles and climatic conditions. Electrification incentives are complemented by farm mechanization schemes promoting higher horsepower penetration and advanced implements, which naturally align with electric and semi-autonomous platforms capable of precision operations and variable-rate input application. State electric mobility policies in Maharashtra, Tamil Nadu, and Telangana extend incentives to agricultural vehicles, expanding addressable demand beyond urban transport electrification frameworks. Public sector agricultural research institutions collaborate with OEMs to validate electric tractor performance across soil types, crop systems, and seasonal workloads, creating confidence among farmer cooperatives and financing agencies. Demonstration programs and rural electrification improvements enhance charging infrastructure feasibility in farm clusters, enabling operational reliability for electric machinery fleets. The policy environment also supports domestic supply chain localization for batteries and electric motors, reducing import dependence and stabilizing pricing for agricultural equipment manufacturers.

Precision Agriculture Adoption and Labor Optimization Pressures

Rising labor scarcity and productivity requirements across Indian agriculture are driving demand for electric and autonomous farm equipment capable of precision operations and reduced manual dependency. Migration of rural labor to non-farm sectors has increased seasonal workforce shortages, particularly in mechanization-intensive states, encouraging farmers to adopt technologies that sustain operational continuity with minimal human intervention. Autonomous and assisted-guidance systems enable consistent field operations such as seeding, spraying, and inter-cultivation with improved accuracy, reducing input wastage and crop variability. Electric drivetrains complement precision agriculture because they support digital control architectures, sensor integration, and software-based torque modulation required for automated tasks. Large commercial farms and cooperative farming clusters prioritize equipment capable of data-driven decision making, including GPS-guided routing, implement automation, and remote monitoring, all of which are more seamlessly integrated into electric and autonomous platforms than conventional diesel tractors. Climate variability and resource constraints further increase the need for optimized input usage, and autonomous electric equipment supports site-specific management practices that enhance yield stability. Technology startups and agri-robotics developers are partnering with tractor OEMs to integrate autonomy stacks and telematics into existing product lines, expanding functional capabilities without requiring farmers to transition to entirely new equipment categories. As digital agriculture ecosystems expand, compatibility between farm management software and electric autonomous machinery strengthens adoption incentives.

Market Challenges

High Acquisition Cost and Financing Barriers for Electric and Autonomous Equipment

The India Electric Tractor & Autonomous Farm Equipment market faces significant adoption constraints due to elevated upfront costs compared with conventional diesel tractors and mechanically simple farm implements. Electric tractors incorporate battery packs, power electronics, and software control systems that substantially increase capital expenditure for farmers operating under tight credit availability and seasonal income variability. Autonomous farm equipment adds further cost layers through sensors, computing hardware, and advanced navigation technologies, creating affordability gaps for small and medium landholders who constitute the majority of Indian farmers. Although subsidies reduce effective purchase price, financing institutions often lack standardized valuation models for electric and autonomous agricultural machinery, leading to cautious lending and higher interest margins. Battery replacement uncertainty and perceived technology risk further discourage long-term financing approvals in rural credit systems. Limited resale markets for electric farm equipment reduce collateral value, complicating loan securitization for lenders and increasing down-payment requirements for buyers. Farmers prioritize proven reliability and repair simplicity, and unfamiliar electric and autonomous systems introduce perceived maintenance risk that influences purchasing decisions toward established diesel platforms. Cost disparities are also amplified by fragmented production volumes, as early-stage electric tractor manufacturing lacks scale economies achieved by conventional tractors in India. Import dependence for advanced autonomy components such as lidar and high-precision navigation modules raises manufacturing cost structures and price volatility.

Rural Charging Infrastructure and Operational Reliability Constraints

Deployment of electric tractors and autonomous farm equipment across Indian agricultural regions is challenged by uneven rural power infrastructure and charging accessibility limitations. Farm operations often occur in remote or off-grid locations where electricity supply reliability and voltage stability are inconsistent, affecting feasibility of routine equipment charging and operational planning. Seasonal irrigation demand places additional strain on rural distribution networks, reducing available capacity for high-power charging of electric machinery during peak agricultural cycles. Autonomous equipment requires continuous energy availability for sensors, computing units, and communication systems, making dependable charging infrastructure essential for functional reliability. Farmers require predictable turnaround time between field operations, and slow or uncertain charging processes disrupt workflow scheduling and equipment utilization rates. Battery swapping or mobile charging solutions remain limited in rural India, constraining operational flexibility for electric machinery fleets operating across dispersed fields. Harsh environmental conditions including dust, heat, and moisture pose durability challenges for charging connectors and electronic systems in agricultural contexts, increasing maintenance requirements. Lack of standardized charging interfaces across manufacturers complicates interoperability and infrastructure deployment by cooperatives or rural service providers. Autonomous equipment additionally depends on connectivity for navigation updates and remote monitoring, yet rural broadband coverage gaps restrict functionality in many farming regions.

Opportunities

Domestic Manufacturing Localization of Electric and Autonomous Agri-Technology

India possesses strong potential to localize production of electric and autonomous farm equipment components through its established tractor manufacturing base and expanding electric mobility supply chain. Localization of battery packs, electric motors, controllers, and autonomy sensors can reduce equipment costs while enhancing reliability under local operating conditions. Government production-linked incentives for advanced chemistry cells and electronics manufacturing create industrial momentum that agricultural equipment OEMs can leverage to develop integrated electric tractor platforms domestically. Local component manufacturing reduces import dependence for autonomy hardware and improves supply chain resilience, enabling faster product iteration and customization for Indian crops and terrains. Domestic engineering talent and agri-robotics startups contribute software and automation capabilities tailored to regional farming practices, strengthening indigenous technology ecosystems. Manufacturing clusters in Maharashtra, Tamil Nadu, and Punjab already support tractor production and can evolve into electric and autonomous equipment hubs with targeted investment. Export opportunities exist for cost-optimized electric tractors suited to smallholder agriculture in emerging markets, positioning India as a global supplier of affordable sustainable farm machinery. Localization also facilitates after-sales service networks and spare parts availability, improving farmer confidence in new technology adoption. Integration of domestically produced autonomy modules into conventional tractors allows phased transition toward fully autonomous systems.

Agri-Robotics Services and Equipment-as-a-Service Deployment Models

The emergence of service-based deployment models for electric and autonomous farm equipment offers significant opportunity to overcome ownership cost barriers and expand access among small and medium farmers. Equipment-as-a-service platforms enable farmers to utilize advanced electric tractors, robotic implements, and autonomous harvesters on demand without full capital investment, aligning with existing custom hiring center structures in Indian agriculture. Service providers can aggregate equipment fleets and optimize utilization across multiple farms, improving economic viability of high-technology machinery through shared usage models. Electric and autonomous platforms are particularly suited to service deployment because digital connectivity enables remote monitoring, scheduling, and predictive maintenance across distributed operations. Rural entrepreneurship initiatives and agri-tech startups are establishing mechanization service networks integrating precision agriculture tools and data analytics with equipment access. Government support for custom hiring centers and farm mechanization cooperatives can extend to electric and autonomous equipment fleets, accelerating rural technology penetration. Service models also facilitate operator training and technical support, addressing skill gaps that hinder direct farmer ownership of autonomous machinery. Data generated from service operations enhances agronomic insights and equipment performance optimization, creating additional value streams for providers. Autonomous equipment can operate extended hours under service models, improving return on investment relative to individually owned machinery.

Future Outlook

The India Electric Tractor & Autonomous Farm Equipment market is expected to expand steadily over the next five years, supported by electrification policies, localization of battery and autonomy technologies, and increasing mechanization intensity. Advancements in precision agriculture and digital farm management systems will enhance compatibility with autonomous machinery. Rural charging infrastructure and service-based deployment models are likely to improve accessibility. Regulatory encouragement for low-emission agriculture and smart farming initiatives will further accelerate adoption across diverse crop systems.

Major Players

- Mahindra & Mahindra Farm Equipment

- TAFE

- Escorts Kubota

- AutoNxt Automation

- Monarch Tractor

- Sonalika

- John Deere India

- CNH Industrial India

- Kubota Agricultural Machinery India

- Yanmar Agricultural Equipment India

- AgNext Technologies

- Bosch Mobility India

- Siemens India

- Sona Comstar

- Tractors and Farm Equipment Limited Electric Division

Key Target Audience

- Agricultural equipment manufacturers

- Electric vehicle technology suppliers

- Autonomous farming technology startups

- Investments and venture capitalist firms

- Government and regulatory bodies

- Agricultural cooperatives and farm enterprises

- Rural mechanization service providers

- Battery and power electronics manufacturers

Research Methodology

Step 1: Identification of Key Variables

Key variables including electric tractor adoption rate, autonomy technology maturity, mechanization intensity, and subsidy frameworks were identified through review of government agricultural and mobility transition policies. Technology parameters such as battery capacity, automation level, and operational suitability across crop systems were defined to structure market boundaries.

Step 2: Market Analysis and Construction

Market size and segmentation were constructed using agricultural mechanization statistics, tractor production data, and electrification deployment records. Regional adoption patterns and product category distribution were mapped to determine segment shares and competitive positioning within the India Electric Tractor & Autonomous Farm Equipment market.

Step 3: Hypothesis Validation and Expert Consultation

Assumptions regarding adoption drivers, cost barriers, and technology diffusion were validated through consultation with agricultural engineers, farm equipment manufacturers, and rural mechanization experts. Pilot deployment outcomes and policy implementation impacts were cross-checked against industry insights and institutional studies.

Step 4: Research Synthesis and Final Output

Validated datasets and qualitative insights were synthesized into structured analysis covering market size, segmentation, competitive landscape, and growth dynamics. Consistency checks ensured alignment with agricultural mechanization trends and electrification progress, producing the final India Electric Tractor & Autonomous Farm Equipment market outlook.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Government electrification and farm mechanization incentives

Rising agricultural labor shortages driving automation demand

Transition toward precision and sustainable farming practices - Market Challenges

High upfront cost of electric and autonomous equipment

Limited rural charging and connectivity infrastructure

Low farmer awareness and technical skill gaps - Market Opportunities

Expansion of autonomous retrofitting solutions for existing tractors

Development of battery swapping ecosystems for farm equipment

Growth of equipment-as-a-service mechanization models - Trends

Integration of AI-based navigation and field analytics

Emergence of compact electric tractors for small farms

OEM partnerships with agri-tech and robotics firms - Government regulations

Electric vehicle subsidy and localization policies for farm machinery

Agricultural mechanization and smart farming missions

Safety and certification standards for autonomous equipment - SWOT analysis

- Porters 5 forces

- By Market Value, 2019-2024

- By Installed Units, 2019-2024

- By Average System Price, 2019-2024

- By System Complexity Tier, 2019-2024

- By System Type (In Value%)

Battery Electric Tractors

Hybrid Electric Tractors

Autonomous Tractors

Autonomous Harvesting Equipment

Autonomous Spraying and Seeding Equipment - By Platform Type (In Value%)

Compact Tractor Platforms

Utility Tractor Platforms

High Horsepower Tractor Platforms

Self-Propelled Implement Platforms

Multi-Implement Autonomous Platforms - By Fitment Type (In Value%)

Factory-Fitted Electric Drivetrain Systems

Factory-Fitted Autonomous Systems

Retrofit Electric Conversion Kits

Retrofit Autonomous Guidance Kits

Integrated Electric-Autonomous Platforms - By EndUser Segment (In Value%)

Smallholder Farmers

Large Commercial Farms

Agricultural Cooperatives

Agri-Service Providers

Government and Research Institutions - By Procurement Channel (In Value%)

Direct OEM Sales

Dealer and Distributor Networks

Government Subsidy Programs

- Market Share Analysis

- Cross Comparison Parameters (Technology Architecture, Power Source Type, Autonomy Level, Connectivity Requirement, Farm Size Suitability, Operational Cost Structure, Infrastructure Dependency)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Mahindra & Mahindra Farm Equipment

TAFE Tractors and Farm Equipment

Escorts Kubota

Sonalika International Tractors

John Deere India

CNH Industrial India

AGCO India

Autonxt Automation

Cellestial E-Mobility

Monarch Tractor

Swaraj Tractors

VST Tillers Tractors

Yanmar Agricultural Machinery India

Kubota Agricultural Machinery India

Tractors and Farm Equipment Electric Mobility Solutions

- Smallholder farmers prioritizing low-cost electric mechanization

- Large farms adopting autonomy for labor efficiency

- Service providers deploying shared autonomous fleets

- Government agencies promoting pilot and demonstration projects

- Forecast Market Value, 2025-2030

- Forecast Installed Units, 2025-2030

- Price Forecast by System Tier, 2025-2030

- Future Demand by Platform, 2025-2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now