Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the India Electric Two-Wheeler market was valued at approximately USD ~ billion, supported by strong domestic demand, government incentive frameworks such as FAME, and accelerating urban mobility electrification. Growth has been driven by rising fuel costs, expanding last-mile delivery networks, and increasing consumer preference for low operating cost transportation solutions. Domestic manufacturing expansion and production-linked incentive schemes have further strengthened supply-side capabilities and pricing competitiveness.

Major urban centers including Bengaluru, Delhi NCR, Mumbai, Hyderabad, and Chennai dominate adoption due to higher disposable incomes, supportive state-level EV policies, and stronger charging infrastructure presence. Southern and western states have emerged as manufacturing hubs supported by industrial ecosystems and policy backing. Concentrated startup activity, established OEM production facilities, and logistics-driven fleet demand have reinforced regional leadership in electric two-wheeler adoption across metropolitan clusters.

Market Segmentation

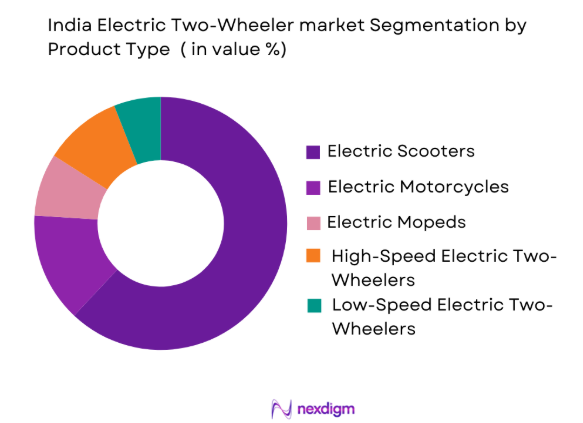

By Product Type

India Electric Two-Wheeler market is segmented by product type into electric scooters, electric motorcycles, electric mopeds, high-speed electric two-wheelers, and low-speed electric two-wheelers. Recently, electric scooters have a dominant market share due to factors such as strong urban commuter demand, broad product portfolios from established OEMs, ease of charging, favorable pricing structures, and compatibility with government subsidy frameworks. Their practicality for short-distance travel, lightweight design, and expanding dealership networks further strengthen their dominance across metropolitan and tier-2 cities.

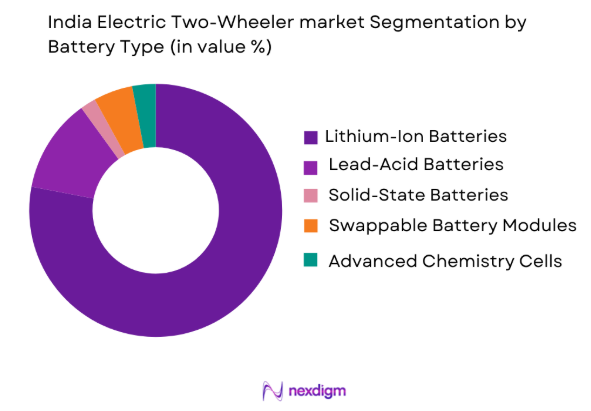

By Battery Type

India Electric Two-Wheeler market is segmented by battery type into lithium-ion batteries, lead-acid batteries, solid-state batteries, swappable battery modules, and advanced chemistry cells. Recently, lithium-ion batteries have a dominant market share due to factors such as higher energy density, longer lifecycle, faster charging capability, declining cell costs, and integration within modern high-speed scooters and motorcycles. Government support for advanced chemistry cell manufacturing and performance advantages over traditional alternatives reinforce their widespread adoption among manufacturers and consumers.

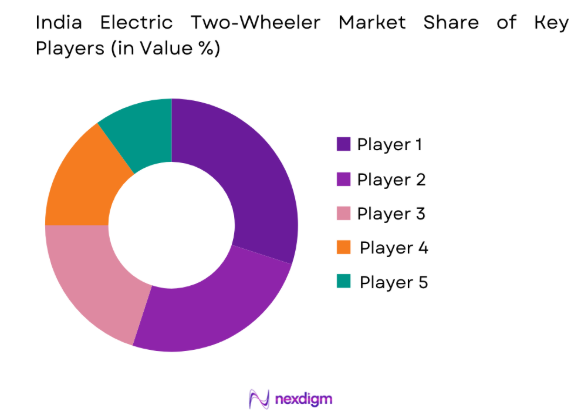

Competitive Landscape

The India Electric Two-Wheeler market demonstrates moderate consolidation, with leading domestic startups and established automotive manufacturers competing on pricing, battery technology, distribution reach, and connected mobility features. Strategic partnerships for battery sourcing, localization initiatives, and scale-driven cost efficiencies influence competitive positioning, while continuous product innovation strengthens brand differentiation in urban and fleet-focused segments.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Manufacturing Capacity |

| Ola Electric | 2017 | Bengaluru | ~ | ~ | ~ | ~ | ~ |

| Ather Energy | 2013 | Bengaluru | ~ | ~ | ~ | ~ | ~ |

| TVS Motor Company | 1978 | Chennai | ~ | ~ | ~ | ~ | ~ |

| Bajaj Auto | 1945 | Pune | ~ | ~ | ~ | ~ | ~ |

| Hero Electric | 2007 | New Delhi | ~ | ~ | ~ | ~ | ~ |

India Electric Two-Wheeler Market Analysis

Growth Drivers

Expansion of Government Incentive Schemes

Expansion of government incentive schemes continues to accelerate India Electric Two-Wheeler adoption by directly reducing acquisition costs and improving affordability across income segments. Central subsidy frameworks combined with state-level incentives lower upfront vehicle prices, making electric models more competitive relative to internal combustion engine alternatives. Production-linked incentive programs for advanced chemistry cells encourage domestic manufacturing, reducing import dependence and enhancing supply chain stability. Fiscal incentives for manufacturers stimulate investment in gigafactories and localized component ecosystems, strengthening economies of scale. Preferential registration policies and road tax exemptions further enhance total cost of ownership benefits for end users. Public procurement initiatives promote fleet electrification across government departments and public utilities. Policy consistency encourages private capital inflows into charging infrastructure and battery-swapping networks. The regulatory push toward emission reduction targets creates structural demand momentum that sustains long-term industry expansion.

Rising Urban Fuel Cost Pressures and Last-Mile Electrification Demand

Rising urban fuel cost pressures and last-mile electrification demand are fundamentally reshaping consumer transportation choices in India Electric Two-Wheeler markets. Elevated petrol prices increase the comparative operating cost advantage of electric mobility solutions, particularly for daily commuters and gig-economy workers. Rapid expansion of e-commerce and food delivery platforms intensifies demand for cost-efficient fleet vehicles with predictable maintenance expenses. Electric two-wheelers provide lower per-kilometer running costs and simplified mechanical structures, reducing servicing downtime. Urban congestion and shorter travel distances align with battery range capabilities of high-speed scooters. Fleet operators increasingly prioritize total cost of ownership optimization rather than initial acquisition cost considerations. Financial institutions are expanding EV-focused financing products to support adoption among delivery riders and small business owners. These structural economic dynamics collectively reinforce sustained consumer and commercial migration toward electric mobility solutions.

Market Challenges

Battery Supply Chain Dependency and Import Exposure

Battery supply chain dependency and import exposure present structural risks within the India Electric Two-Wheeler market due to reliance on imported lithium cells and critical raw materials. Concentration of global lithium processing and cell manufacturing outside India creates vulnerability to geopolitical disruptions and price volatility. Fluctuating input costs directly affect vehicle pricing and manufacturer margins, limiting predictable cost structures. Domestic cell production capacity remains under development, creating transitional supply bottlenecks. Currency fluctuations amplify procurement risk for OEMs dependent on overseas suppliers. Safety compliance standards and certification requirements increase complexity in sourcing decisions. Limited recycling infrastructure constrains circular economy integration within the battery value chain. These supply-side constraints collectively challenge long-term pricing stability and scalability for manufacturers.

Charging Infrastructure Gaps Beyond Metropolitan Regions

Charging infrastructure gaps beyond metropolitan regions continue to restrict widespread adoption of India Electric Two-Wheeler solutions across semi-urban and rural markets. Limited public charging density in tier-2 and tier-3 cities reduces consumer confidence in range reliability. High-speed models require dependable fast-charging solutions that are not uniformly available outside major urban centers. Private home charging remains constrained by residential parking limitations in densely populated zones. Grid stability concerns and transformer capacity limitations affect large-scale charging deployments. Fragmented standards for connectors and battery-swapping interoperability slow ecosystem expansion. Infrastructure capital expenditure requirements delay rapid rollout in lower-demand districts. Without synchronized infrastructure development, geographic penetration of electric mobility remains uneven despite rising interest levels.

Opportunities

Localization of Advanced Chemistry Cell Manufacturing Ecosystem

Localization of advanced chemistry cell manufacturing ecosystem offers transformative potential for the India Electric Two-Wheeler market by reducing import dependence and stabilizing input costs. Establishment of domestic gigafactories strengthens supply resilience and shortens procurement cycles for OEMs. Integration of upstream material processing with downstream pack assembly enhances value capture within national borders. Government-backed production incentives encourage private capital deployment into cell manufacturing infrastructure. Localized research and development capabilities enable adaptation of battery chemistries optimized for Indian climatic conditions. Domestic sourcing improves compliance oversight and quality control within the value chain. Employment generation across manufacturing clusters contributes to regional industrial development. A mature domestic battery ecosystem enhances export competitiveness for Indian electric vehicle manufacturers.

Expansion of Battery Swapping and Energy-as-a-Service Models

Expansion of battery swapping and energy-as-a-service models presents scalable growth pathways within the India Electric Two-Wheeler market by decoupling vehicle ownership from battery ownership. Swapping infrastructure reduces vehicle downtime for commercial fleets, increasing asset utilization rates. Energy subscription models lower upfront vehicle prices, improving affordability for cost-sensitive consumers. Standardized battery modules promote interoperability across multiple OEM platforms. Fleet operators benefit from predictable energy expenses under subscription-based billing frameworks. Private energy companies gain recurring revenue streams through integrated charging and swapping networks. Urban density supports economically viable swapping station deployment in high-demand corridors. These alternative business models create diversified revenue ecosystems beyond traditional vehicle sales.

Future Outlook

Over the next five years, the India Electric Two-Wheeler market is expected to experience sustained expansion driven by deeper localization of battery production, continued regulatory incentives, and growing urban electrification mandates. Technological innovation in battery chemistry and connected mobility platforms will enhance performance and consumer confidence. Infrastructure scaling across emerging cities is likely to broaden geographic adoption. Demand from commercial fleets and shared mobility operators will further strengthen volume growth.

Major Players

- Ola Electric

- Ather Energy

- TVS Motor Company

- Bajaj Auto

- Hero Electric

- Hero MotoCorp

- Ampere Vehicles

- Revolt Motors

- OkinawaAutotech

- Pure EV

- Tork Motors

- BenlingIndia

- Greaves Electric Mobility

- WardWizardInnovations

- LectrixEV

Key Target Audience

- Electric Vehicle Manufacturers

- Battery Manufacturers

- Automotive Component Suppliers

- Fleet Operators

- Investments and venture capitalist firms

- Government and regulatory bodies

- Charging Infrastructure Providers

- Automotive Dealership Networks

Research Methodology

Step 1: Identification of Key Variables

Demand drivers, pricing structures, regulatory incentives, battery technology evolution, and production capacity were identified as core analytical variables influencing market performance and competitive positioning.

Step 2: Market Analysis and Construction

Market size validation was conducted using triangulation of industry reports, company disclosures, government policy documents, and trade data to construct a reliable demand and supply framework.

Step 3: Hypothesis Validation and Expert Consultation

Industry stakeholders including OEM executives, battery suppliers, and policy analysts were consulted to validate adoption trends, regulatory impact, and forward-looking strategic developments.

Step 4: Research Synthesis and Final Output

Quantitative and qualitative findings were synthesized into structured analytical sections, ensuring consistency, data integrity, and alignment with macroeconomic and industry-specific indicators.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expansion of Government Incentive Schemes

Rising Urban Fuel Cost Pressures

Growing Last-Mile Delivery Electrification - Market Challenges

Battery Supply Chain Dependency

Charging Infrastructure Gaps in Tier-2 and Tier-3 Cities

High Upfront Acquisition Costs - Market Opportunities

Battery Swapping Network Expansion

Localization of Cell Manufacturing

Integration of Smart Connected Features - Trends

Shift Toward High-Speed Electric Scooters

Increased Adoption of Lithium-Ion Batteries

Strategic Alliances Between OEMs and Energy Companies

Government Regulations

SWOT Analysis of Key Competitors

Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Electric Scooters

Electric Motorcycles

Electric Mopeds

High-Speed Electric Two-Wheelers

Low-Speed Electric Two-Wheelers - By Platform Type (In Value%)

Fixed Battery Platform

Swappable Battery Platform

Connected Telematics Platform

IoT-Enabled Smart Platform

Fleet-Optimized Platform - By Fitment Type (In Value%)

Factory-Fitted Battery Systems

Dealer-Level Custom Fitments

Aftermarket Battery Upgrades

Connected Device Retrofits

Performance Enhancement Kits - By End User Segment (In Value%)

Urban Commuters

Rural Consumers

Commercial Fleet Operators

Last-Mile Delivery Companies

Shared Mobility Operators - By Procurement Channel (In Value%)

OEM Dealerships

Online Direct-to-Consumer Platforms

Fleet Procurement Contracts

Government E-Marketplace Procurement

Third-Party Distributors

- Market Share Analysis

- Cross Comparison Parameters (Battery Capacity, Vehicle Range, Charging Time, Pricing Tier, Distribution Network Strength, Motor Power Output, Top Speed, Battery Chemistry Type, Swappable Battery Compatibility, Connected Features Integration, Warranty Coverage, After-Sales Service Network, Localization Level of Components, Production Capacity, Government Incentive Eligibility)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Ola Electric

Ather Energy

Hero Electric

TVS Motor Company

Bajaj Auto

Hero MotoCorp

Ampere Vehicles

Revolt Motors

Okinawa Autotech

Pure EV

Tork Motors

Benling India

Greaves Electric Mobility

WardWizard Innovations

Lectrix EV

- Urban commuters prioritizing low operating cost mobility

- Fleet operators focusing on total cost of ownership optimization

- Delivery aggregators accelerating electrification targets

- Rural consumers adopting entry-level low-speed models

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now