Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The India Electric Vehicle market reached a value of USD ~ billion based on a recent historical assessment, driven by rapid electrification across two-wheelers, three-wheelers, and public transport fleets. Strong policy support through demand incentives, reduced GST, and production-linked incentives for battery manufacturing has accelerated adoption. Rising fuel costs, urban pollution concerns, and improving battery efficiency continue to strengthen consumer interest, while domestic manufacturing expansion reduces costs and improves supply chain resilience.

Major metropolitan regions including Delhi NCR, Bengaluru, Mumbai, Hyderabad, and Chennai dominate adoption due to high population density, supportive state policies, and expanding charging infrastructure. These cities benefit from fleet electrification initiatives, last-mile delivery demand, and progressive urban mobility mandates. Southern and western industrial corridors also lead due to strong automotive manufacturing ecosystems, technology talent availability, and state-level incentives encouraging EV production, research, and charging infrastructure deployment.

Market Segmentation

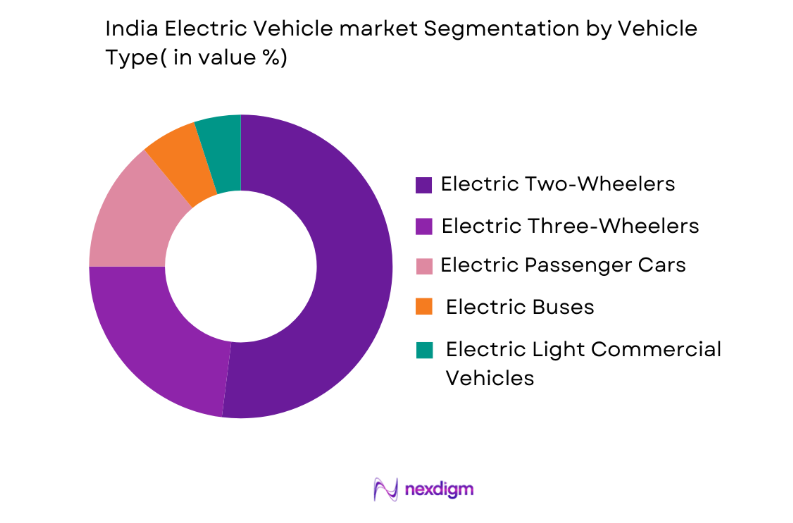

By Vehicle Type

India Electric Vehicle market is segmented by vehicle type into electric two-wheelers, electric three-wheelers, electric passenger cars, electric buses, and electric light commercial vehicles. Recently, electric two-wheelers have a dominant market share due to affordability, suitability for urban commuting, strong presence of domestic manufacturers, and widespread adoption among gig economy workers. Expanding battery swapping networks and government subsidies further support growth. The segment benefits from lower operating costs, minimal maintenance requirements, and increasing fuel price sensitivity among consumers, making it the preferred entry point into electrified mobility.

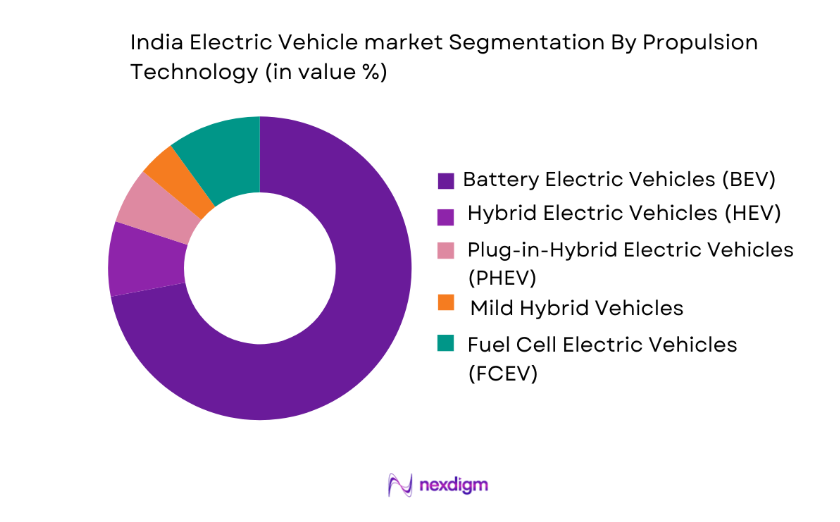

By Propulsion Technology

India Electric Vehicle market is segmented by propulsion technology into battery electric vehicles (BEV), hybrid electric vehicles (HEV), plug-in hybrid electric vehicles (PHEV), fuel cell electric vehicles (FCEV), and mild hybrid vehicles. Recently, battery electric vehicles have a dominant market share due to strong policy incentives, zero tailpipe emissions, simpler drivetrain architecture, and rapidly improving battery costs. Charging infrastructure expansion and localization of battery manufacturing further strengthen adoption. Consumers and fleet operators prefer BEVs for lower lifetime operating costs and regulatory compliance in low-emission zones.

Competitive Landscape

The market is moderately consolidated, with domestic manufacturers leading mass-market segments while global automakers compete in premium categories. Strong vertical integration strategies, battery partnerships, and software-driven mobility platforms are shaping competition. Companies are investing heavily in localization, charging ecosystems, and fleet partnerships to strengthen market presence and reduce costs.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Battery Strategy |

| Tata Motors | 1945 | Mumbai, India | ~ | ~ | ~ | ~ | ~ |

| Mahindra Electric | 2010 | Bengaluru, India | ~ | ~ | ~ | ~ | ~ |

| Ola Electric | 2017 | Bengaluru, India | ~ | ~ | ~ | ~ | ~ |

| Ather Energy | 2013 | Bengaluru, India | ~ | ~ | ~ | ~ | ~ |

| BYD India | 2007 | Chennai, India | ~ | ~ | ~ | ~ | ~ |

India Electric Vehicle market analysis

Growth Drivers

Rapid Urbanization and Rising Fuel Costs

The accelerating pace of urbanization across India is reshaping transportation demand, pushing millions of new commuters into dense metropolitan corridors where traditional internal combustion vehicles exacerbate congestion and pollution. Rising petrol and diesel prices have significantly increased the total cost of ownership for conventional vehicles, prompting consumers and fleet operators to seek more economical alternatives. Electric vehicles offer substantially lower operating costs per kilometer, making them particularly attractive for ride-hailing drivers, delivery fleets, and daily commuters. Government subsidies and tax incentives further reduce upfront costs, narrowing the price gap with ICE vehicles. Expanding charging infrastructure in cities enhances usability and reduces range anxiety among consumers. Corporate sustainability commitments are also driving fleet electrification, particularly in logistics and last-mile delivery. Financial institutions are introducing EV-specific financing products, improving affordability and accessibility. Additionally, improved battery technology has extended driving ranges and reduced charging times, making EVs more practical for everyday use. Together, these factors are accelerating consumer confidence and strengthening long-term demand for electric mobility solutions.

Government Incentives and Localization Policies

Strong policy support from central and state governments is a major catalyst for electric vehicle adoption across India, with initiatives designed to promote domestic manufacturing, reduce emissions, and enhance energy security. Demand incentives under national programs reduce purchase costs for consumers and fleet operators, making EVs more financially viable. Production-linked incentive schemes encourage local manufacturing of batteries and components, reducing reliance on imports and lowering costs. State governments provide additional benefits such as road tax exemptions, registration fee waivers, and priority permits for commercial EVs. Investments in public charging infrastructure are expanding accessibility across urban and semi-urban regions. Localization policies are fostering the development of a domestic supply chain, creating jobs and strengthening industrial capabilities. These measures also attract foreign investment and technology partnerships, accelerating innovation. Regulatory mandates for electrification of public transport and government fleets further stimulate demand. The policy ecosystem creates a supportive environment that encourages manufacturers to scale production and consumers to transition to cleaner mobility options.

Market Challenges

High Upfront Costs and Financing Barriers

Despite declining battery costs and supportive incentives, the upfront purchase price of electric vehicles remains higher than comparable internal combustion engine vehicles, creating a significant barrier for price-sensitive consumers. Many buyers evaluate vehicles based on initial cost rather than total cost of ownership, slowing adoption. Limited availability of tailored financing products and higher perceived risk among lenders further restrict access to affordable loans for EV purchases. Insurance premiums for EVs can also be higher due to expensive battery components and limited repair infrastructure. Small fleet operators and individual drivers often lack access to capital required for fleet electrification. Residual value uncertainty and concerns about battery degradation discourage long-term investment decisions. The absence of standardized resale markets for used EVs compounds financial risk perceptions. Although subsidies reduce costs, delays in disbursement can strain cash flows for buyers and dealers. These financial barriers collectively hinder widespread adoption, particularly in rural and semi-urban markets.

Charging Infrastructure Gaps and Grid Constraints

While urban charging infrastructure is expanding, significant gaps remain in semi-urban and rural areas, limiting the practicality of electric vehicles for long-distance travel and intercity logistics. Range anxiety continues to influence consumer decisions, especially among first-time buyers unfamiliar with EV technology. Power distribution networks in some regions face reliability challenges, affecting consistent charging availability. High installation costs for fast chargers deter private investment, particularly in low-demand areas. Standardization issues across charging connectors and payment systems create user inconvenience and interoperability challenges. Residential charging is difficult in densely populated areas with limited parking and shared electrical infrastructure. Peak electricity demand from fast charging stations may strain local grids without proper load management systems. Limited renewable energy integration reduces the environmental benefits of EV adoption. These infrastructure and grid challenges must be addressed to ensure seamless and scalable EV deployment across the country.

Opportunities

Battery Manufacturing and Supply Chain Localization

The push for domestic battery manufacturing presents a transformative opportunity for India’s electric vehicle ecosystem by reducing reliance on imported lithium-ion cells and strengthening energy security. Investments in gigafactories and advanced chemistry cell production are fostering technological innovation and cost reductions. Localization enables better control over supply chains, mitigating risks associated with geopolitical tensions and raw material price volatility. Domestic production also shortens lead times and enhances quality control. Collaboration between government, industry, and research institutions is accelerating the development of next-generation battery technologies. Recycling and second-life battery applications are emerging as new business models, improving sustainability and resource efficiency. Localized manufacturing creates employment opportunities and stimulates regional economic growth. Cost reductions from economies of scale will make EVs more affordable to mass-market consumers. These developments position India as a potential global hub for battery production and EV exports.

Expansion of Electric Mobility in Logistics and Public Transport

Electrification of logistics fleets and public transportation systems represents a significant growth opportunity as cities aim to reduce emissions and improve air quality. E-commerce growth has increased demand for last-mile delivery solutions, where electric two- and three-wheelers offer cost and efficiency advantages. Municipal authorities are adopting electric buses to modernize public transit and meet sustainability goals. Fleet operators benefit from predictable routes that simplify charging infrastructure planning. Corporate sustainability commitments are accelerating adoption of zero-emission delivery vehicles. Government tenders and subsidies support large-scale fleet electrification projects. Integration of telematics and fleet management software enhances operational efficiency and cost savings. Battery swapping solutions reduce downtime for commercial vehicles. As urban freight demand continues to grow, electric mobility solutions will play a central role in sustainable logistics and public transport transformation.

Future Outlook

The India Electric Vehicle market is expected to witness strong expansion over the next five years, supported by falling battery costs, rapid charging innovations, and broader model availability across price segments. Government incentives, localization policies, and urban emission mandates will continue to accelerate adoption. Advancements in battery chemistry, swapping ecosystems, and renewable energy integration will improve efficiency and sustainability. Rising fleet electrification and consumer awareness will further strengthen long-term demand.

Major Players

- Tata Motors

- Mahindra Electric Mobility

- Ola Electric

- Ather Energy

- Hero Electric

- TVS Motor Company

- Bajaj Auto

- Ashok Leyland

- Eicher Motors

- BYD India

- MG Motor India

- Hyundai Motor India

- Kia India

- JBM Auto

- Euler Motors

Key Target Audience

- Automotive manufacturers

- Battery manufacturers

- Charging infrastructure providers

- Fleet operators and logistics companies

- Investments and venture capitalist firms

- Government and regulatory bodies

- Renewable energy companies

- Automotive component suppliers

Research Methodology

Step 1: Identification of Key Variables

Key variables such as vehicle sales, battery costs, charging infrastructure growth, policy incentives, and consumer adoption trends were identified. These variables influence demand patterns, pricing dynamics, and long-term market growth potential.

Step 2: Market Analysis and Construction

Market size was constructed using a bottom-up approach, aggregating vehicle sales data, average selling prices, and infrastructure investments. Secondary sources included government reports, industry associations, and company financial disclosures.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts, EV manufacturers, and policy analysts were consulted to validate assumptions related to technology adoption, infrastructure readiness, and regulatory impact. Insights helped refine forecasts and ensure realistic market modeling.

Step 4: Research Synthesis and Final Output

Data triangulation combined primary insights with secondary research to produce a comprehensive market model. Final outputs were reviewed for consistency, accuracy, and alignment with policy and industry developments.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Rising fuel costs and total cost of ownership advantages

Government incentives and FAME subsidy programs

Expansion of charging infrastructure in urban corridors - Market Challenges

High upfront vehicle costs compared to ICE vehicles

Limited charging infrastructure in rural regions

Battery supply chain constraints and import dependence - Market Opportunities

Localization of battery manufacturing under PLI schemes

Growth in electric two- and three-wheeler adoption

Integration of renewable energy with EV charging networks - Trends

Battery swapping ecosystems gaining traction

Connected vehicle and telematics integration

Emergence of EV-focused financing and leasing models - Government Regulations

- Swot Analysis of Key Players

- Porter’s Five Forces

- By Market Value, 2019-2025

- By Installed Units, 2019-2025

- By Average System Price, 2019-2025

- By System Complexity Tier, 2019-2025

- By System Type (In Value%)

Battery Electric Vehicles (BEV)

Plug-in Hybrid Electric Vehicles (PHEV)

Hybrid Electric Vehicles (HEV)

Fuel Cell Electric Vehicles (FCEV)

Mild Hybrid Electric Vehicles (MHEV) - By Platform Type (In Value%)

Two-Wheeler Electric Vehicles

Three-Wheeler Electric Vehicles

Passenger Electric Cars

Electric Buses

Electric Light Commercial Vehicles - By Fitment Type (In Value%)

OEM Factory-Fitted Systems

Aftermarket Conversion Kits

Fleet Retrofitting Solutions

Modular Battery Swapping Systems

Integrated Telematics & Connectivity Units - By End User Segment (In Value%)

Individual Consumers

Ride-Hailing & Mobility Service Providers

Public Transportation Authorities

Logistics & Last-Mile Delivery Companies

Corporate Fleet Operators - By Procurement Channel (In Value%)

Direct OEM Sales

Authorized Dealership Networks

Online Vehicle Marketplaces

- Market Share Analysis

- Cross Comparison Parameters (Battery Capacity, Vehicle Range, Charging Time, Total Cost of Ownership, After-Sales Network, Powertrain Efficiency, Fast-Charging Capability, Battery Warranty Coverage)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Tata Motors

Mahindra Electric Mobility

Ola Electric

Ather Energ

Hero Electric

TVS Motor Company

Bajaj Auto

Ashok Leyland

Eicher Motors

BYD India

MG Motor India

Hyundai Motor India

Kia India

JBM Auto

Euler Motors

- Growing adoption among urban commuters seeking cost savings

- Fleet electrification by e-commerce and logistics providers

- Public transit modernization through electric buses

- Corporate sustainability initiatives driving EV fleet uptake

- Forecast Market Value, 2026-2030

- Forecast Installed Units, 2026-2030

- Price Forecast by System Tier, 2026-2030

- Future Demand by Platform, 2026-2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now