Download PDF

Download PDF Download PDF

Download PDFMarket Overview

India EV charging infrastructure market reached approximately USD ~ billion based on a recent historical assessment, driven by rapid electric vehicle adoption, public charging network expansion, and government incentive programs such as FAME and state EV policies. Deployment of fast-charging corridors along highways and urban clusters has accelerated capital investment by utilities, oil marketing companies, and private charging operators, while rising two-wheeler electrification and fleet electrification demand have increased installed charging points across metropolitan and tier-2 cities nationwide.

Major urban regions such as Delhi NCR, Bengaluru, Mumbai Metropolitan Region, and Pune dominate charging infrastructure deployment due to high EV registrations, supportive state policies, and dense commercial mobility demand. Southern and western states lead infrastructure rollout through proactive utility participation and manufacturing ecosystems, while national highway corridors connecting industrial and logistics hubs are emerging as high-capacity charging clusters. Public transport electrification programs in large municipal corporations further reinforce concentration of depot and fast-charging installations in major metropolitan areas.

Market Segmentation

By Charger Type

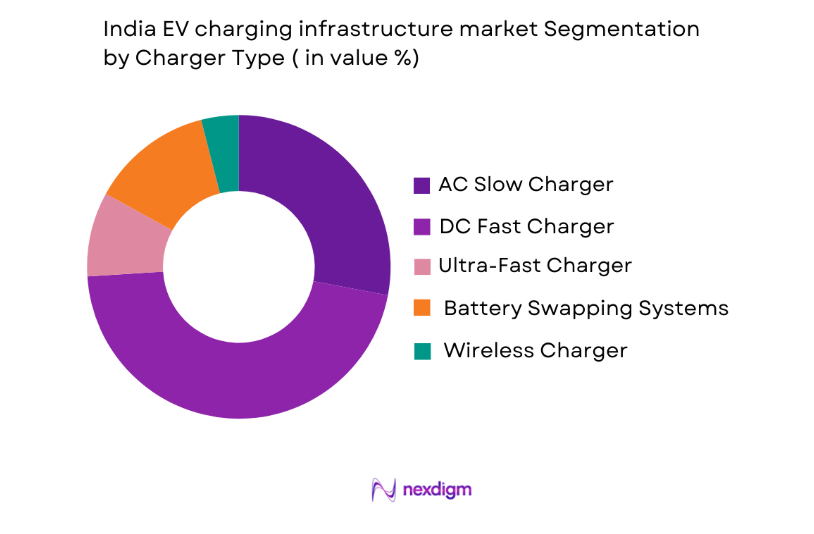

India EV charging infrastructure market is segmented by charger type into AC slow chargers, DC fast chargers, ultra-fast chargers, battery swapping systems, and wireless chargers. Recently, DC fast chargers has a dominant market share due to factors such as growing intercity travel demand, fleet electrification requirements, and highway corridor development. Commercial fleet operators, ride-hailing services, and public transport agencies require high-throughput charging to maintain vehicle utilization, which has accelerated deployment of DC charging stations across urban hubs and transport corridors. Government incentives and oil marketing company investments have prioritized fast-charging installations at fuel stations and logistics nodes. Increasing battery capacities in electric cars and buses also necessitate faster charging infrastructure, reinforcing DC charger dominance in public and commercial segments nationwide.

By End-Use Application

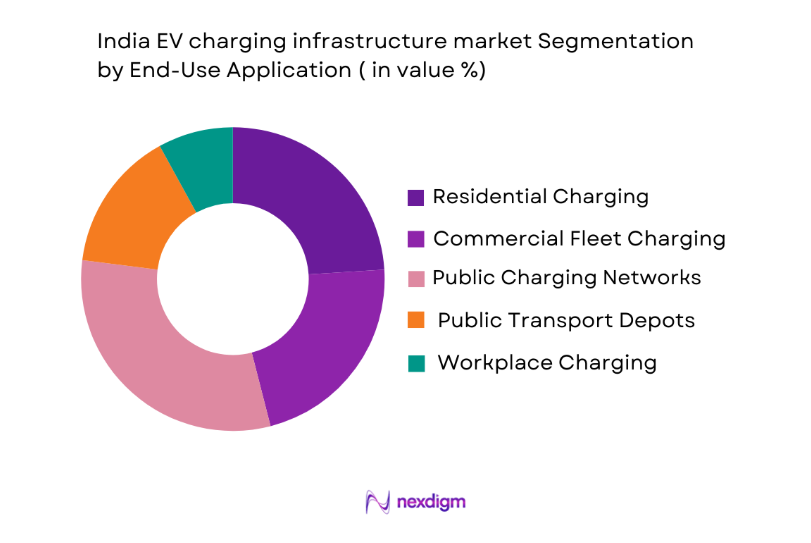

India EV charging infrastructure market is segmented by end-use application into residential charging, commercial fleet charging, public charging networks, public transport depots, and workplace charging. Recently, public charging networks has a dominant market share due to factors such as urban apartment constraints, long-distance travel requirements, and expanding shared mobility fleets. Limited private parking availability in dense cities has increased reliance on public charging hubs, while government programs and private operators are rapidly expanding urban public chargers. Ride-hailing fleets and intercity EV travel depend on accessible public networks, driving utilization and revenue concentration. Integration of charging with retail, fuel stations, and mobility hubs has further strengthened public network adoption across metropolitan regions and highways.

Competitive Landscape

India EV charging infrastructure market exhibits a moderately consolidated structure with participation from utilities, oil marketing companies, EV startups, and global technology suppliers. Large power and energy companies leverage grid access and capital to scale nationwide networks, while specialized EV charging firms focus on software platforms and urban deployment. Strategic partnerships between automotive OEMs, fuel retailers, and charging operators are expanding interoperability and coverage. Technology providers supply hardware and software ecosystems enabling network management and payment integration.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Charger Network Scale |

| Tata Power EV Charging Solutions | 2019 | Mumbai, India | ~ | ~ | ~ | ~ | ~ |

| Charge Zone | 2018 | Vadodara, India | ~ | ~ | ~ | ~ | ~ |

| Ather Energy | 2013 | Bengaluru, India | ~ | ~ | ~ | ~ | ~ |

| Fortum Charge & Drive India | 2017 | Gurugram, India | ~ | ~ | ~ | ~ | ~ |

| Statiq | 2019 | Gurugram, India | ~ | ~ | ~ | ~ | ~ |

India EV charging infrastructure Market Analysis

Growth Drivers

Government-Led EV Infrastructure Incentives and National Electrification Programs

India EV charging infrastructure expansion is strongly supported by central and state government incentive frameworks that subsidize charger installation, electricity tariffs, and capital expenditure for network operators, utilities, and public agencies. Programs such as national electric mobility missions and public charging guidelines have standardized deployment norms, encouraged private investment, and enabled rapid rollout across highways and cities. Oil marketing companies and public utilities are mandated to establish charging networks, creating predictable infrastructure expansion and demand aggregation. Fiscal incentives reduce project payback periods and de-risk early-stage deployment in emerging EV clusters. State EV policies provide land access, grid connection priority, and tariff concessions that further accelerate infrastructure density in urban regions. Public procurement of electric buses and fleets drives depot charging installations at scale. Combined policy support across transport, power, and urban development sectors is creating a nationwide charging backbone that stimulates sustained infrastructure investment by both public and private stakeholders.

Rapid Electrification of Two-Wheelers, Fleets, and Public Transport

India’s EV adoption pattern is dominated by two-wheelers, commercial fleets, and public buses, all of which require accessible and reliable charging networks to sustain high vehicle utilization and operational efficiency. E-commerce logistics fleets, ride-hailing operators, and delivery services are electrifying vehicles to reduce operating costs and meet sustainability commitments, driving concentrated demand for depot and fast charging hubs. Municipal bus electrification programs require large-capacity depot chargers and opportunity charging infrastructure, increasing installed charger capacity in metropolitan regions. High daily utilization of commercial EVs necessitates faster charging cycles, favoring DC and high-power charging deployments. Growth of shared mobility and last-mile logistics further increases dependence on public and semi-public charging points. As fleet electrification scales nationwide, charging infrastructure investment is accelerating to support commercial mobility ecosystems, creating a reinforcing cycle between EV adoption and charger deployment.

Market Challenges

High Capital Costs and Grid Infrastructure Constraints

EV charging infrastructure deployment in India faces substantial upfront capital expenditure requirements for hardware, grid upgrades, land acquisition, and network integration, which can challenge financial viability in early-stage markets with low utilization. High-power DC chargers require dedicated transformers, distribution upgrades, and grid capacity enhancements that increase project costs and timelines. Utilities may face capacity constraints in dense urban zones, delaying connections and limiting charger density expansion. Return on investment is sensitive to utilization rates, which remain uneven across regions due to variable EV adoption. Financing infrastructure in smaller cities and highways with uncertain demand remains challenging for private operators. Additionally, electricity tariff structures and demand charges can affect operating economics of charging stations. These structural cost and grid barriers slow deployment pace in non-metro regions and create uneven national charging coverage despite policy support.

Land Access, Utilization Variability, and Business Model Uncertainty

Securing suitable urban land parcels for public charging stations in dense Indian cities is complex due to high real estate costs, zoning constraints, and fragmented ownership patterns, limiting deployment in high-demand areas. Charging utilization varies significantly by location, vehicle segment, and time of day, complicating revenue predictability and infrastructure planning for operators. Public charging demand is concentrated in a few metropolitan clusters, while many installed chargers remain underutilized in early-stage markets, affecting profitability. Lack of standardized pricing models and evolving interoperability frameworks create uncertainty for consumers and investors. Competition between battery swapping and plug-in charging ecosystems also fragments investment flows. Long asset lifecycles combined with rapidly evolving EV technologies introduce risk of obsolescence. These structural uncertainties constrain large-scale private capital deployment and require adaptive business models and policy clarity.

Opportunities

Highway Fast-Charging Corridor and Intercity Mobility Expansion

Expansion of national highway EV corridors connecting major industrial, logistics, and tourism routes presents a significant opportunity for high-power fast-charging infrastructure deployment in India. Long-distance electric passenger vehicles, buses, and logistics fleets require reliable intercity charging networks to enable nationwide electrified mobility. Government corridor programs and oil marketing company participation are creating anchor sites at fuel stations and transport hubs along highways. Growth in intercity electric bus routes and commercial transport electrification will further increase demand for high-capacity chargers and energy storage integration. Corridor charging hubs can achieve higher utilization due to predictable traffic flows, improving operator economics. Integration with amenities such as retail, food, and rest facilities enhances user adoption and revenue streams. As EV driving ranges increase and vehicle adoption expands beyond cities, intercity charging infrastructure will become a critical growth segment.

Integration of Renewable Energy, Energy Storage, and Smart Charging Platforms

Integration of EV charging infrastructure with renewable energy generation, battery energy storage systems, and digital energy management platforms creates opportunities for sustainable and cost-efficient charging ecosystems in India. Solar-powered charging stations and grid-interactive chargers can reduce electricity costs, improve grid stability, and support peak-load management. Energy storage integration enables fast-charging deployment in grid-constrained locations by buffering power demand. Smart charging software allows dynamic load management, demand response participation, and time-of-use optimization for operators and utilities. Vehicle-to-grid technologies and distributed energy resources can transform charging networks into flexible energy assets supporting power system resilience. Corporate sustainability initiatives and green mobility commitments further drive adoption of renewable-integrated charging infrastructure. These technology integrations can enhance profitability, environmental performance, and scalability of charging networks across urban and highway segments.

Future Outlook

India EV charging infrastructure market is expected to expand rapidly over the next five years supported by accelerating EV adoption, national electrification programs, and private investment in charging networks. High-power fast charging corridors, urban public hubs, and fleet depot infrastructure will scale significantly. Advancements in smart charging, renewable integration, and interoperability platforms will improve utilization and economics. Continued regulatory incentives, utility participation, and commercial fleet electrification will sustain infrastructure demand across metropolitan and intercity mobility ecosystems.

Major Players

- Tata Power EV Charging Solutions

- Charge Zone

- Ather Energy

- Fortum Charge & Drive India

- Magenta Charge Grid

- Statiq

- Jio-bp Pulse

- ABB India

- Exicom Tele-Systems

- Delta Electronics India

- EVRE

- Relux Electric

- Volttic

- Sun Mobility

- Servotech Power Systems

Key Target Audience

- Electric vehicle manufacturers

- Charging infrastructure operators

- Oil and gas companies

- Electric utilities

- Automotive component suppliers

- Investments and venture capitalist firms

- Government and regulatory bodies

- Fleet and logistics operators

Research Methodology

Step 1: Identification of Key Variables

Key variables include EV adoption by segment, charger deployment by type, utilization rates, tariff structures, policy incentives, and regional infrastructure density. These factors determine demand patterns and investment economics across public, private, and fleet charging ecosystems.

Step 2: Market Analysis and Construction

Market size is constructed using installed charger base, average system cost, deployment rates, and operator revenue models across AC, DC, and swapping infrastructure. Regional deployment data and company disclosures are synthesized to estimate national infrastructure value.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts from utilities, charging operators, OEMs, and policy bodies validate assumptions on deployment costs, utilization, and adoption trends. Cross-verification ensures alignment with regulatory frameworks and infrastructure rollout programs across states.

Step 4: Research Synthesis and Final Output

Validated data is integrated into segmentation, competitive landscape, and forecast models to produce market estimates and strategic insights. Analytical outputs align infrastructure deployment trends with EV adoption and policy trajectories.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Government Incentives and National EV Adoption Programs

Expansion of Electric Two-Wheeler and Fleet Electrification

Urban Air Quality and Emission Reduction Mandates - Market Challenges

High Upfront Infrastructure and Grid Upgrade Costs

Uneven Utilization and Demand Concentration

Land Access and Urban Installation Constraints - Market Opportunities

Highway Fast-Charging Corridor Development

Integration with Renewable Energy and Storage

Battery Swapping Ecosystem Expansion - Trends

Shift Toward High-Power Fast Charging Networks

Interoperable Payment and Roaming Platforms

Co-Location with Retail and Mobility Hubs - Government Regulations

- SWOT Analysis of Key Competitors

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

AC Slow Charging Stations

DC Fast Charging Stations

Ultra-Fast High Power Chargers

Battery Swapping Stations

Wireless Inductive Charging Systems - By Platform Type (In Value%)

Public On-Highway Charging Networks

Urban Public Charging Hubs

Residential Private Charging Units

Commercial Fleet Charging Depots

Transit and Bus Charging Infrastructure - By Fitment Type (In Value%)

Standalone Ground-Mounted Chargers

Wall-Mounted Chargers

Integrated Parking Infrastructure Chargers

Battery Swapping Dock Installations

Pantograph Bus Charging Systems - By End User Segment (In Value%)

Passenger Electric Vehicle Owners

Electric Two-Wheeler Users

Commercial Fleet Operators

Public Transport Authorities

- Market Share Analysis

- Cross Comparison Parameters (Charger Power Output, Network Coverage, Connector Standards, Software Platform Capability, Pricing Model, Charging Speed, Grid Integration Capability, Interoperability and Roaming Support, Installation Footprint, O&M Service Model)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Tata Power EV Charging Solutions

ChargeZone

Ather Energy

Fortum Charge & Drive India

Magenta ChargeGrid

Statiq

Jio-bp Pulse

ABB India

Exicom Tele-Systems

Delta Electronics India

EVRE

Relux Electric

Volttic

Sun Mobility

Servotech Power Systems

- Rising Home Charging Adoption Among Urban EV Owners

- Fleet Depot Charging Scaling with E-Commerce Logistics

- Public Transport Electrification Driving Depot Chargers

- Two-Wheeler Charging Demand in Dense Cities

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now